SMPL - Simply Good Foods: Quality At A Reasonable Price

Summary

- Simply Good Foods leans on its pricing power to drive another strong quarter of revenue growth.

- While margins suffered from several one-offs, the underlying brand momentum remains intact.

- The valuation screens reasonably relative to the earnings growth potential.

Simply Good Foods ( SMPL ), a nutritional snacks company operating the Atkins and Quest brands, saw more price-driven growth in Q1, even if it fell short on margins due to one-off factors. Importantly, the underlying fundamentals remain intact for Quest, while the sequential acceleration at Atkins supports the case for a turnaround in the near future. With new innovation coming to market in the coming months, management’s decision to maintain its full-year revenue guidance could even prove conservative, in my view. The earnings outlook, on the other hand, depends on execution, as management rights the missteps of the prior CFO transition and capitalizes on easing supply chain headwinds.

Over the long run, SMPL’s ability to grow without heavy reinvestments is compelling, allowing for more free cash generation and potentially increased shareholder returns down the line. At ~20x fwd P/E for low-double-digit EPS growth and a quality brand portfolio, SMPL is very reasonably priced.

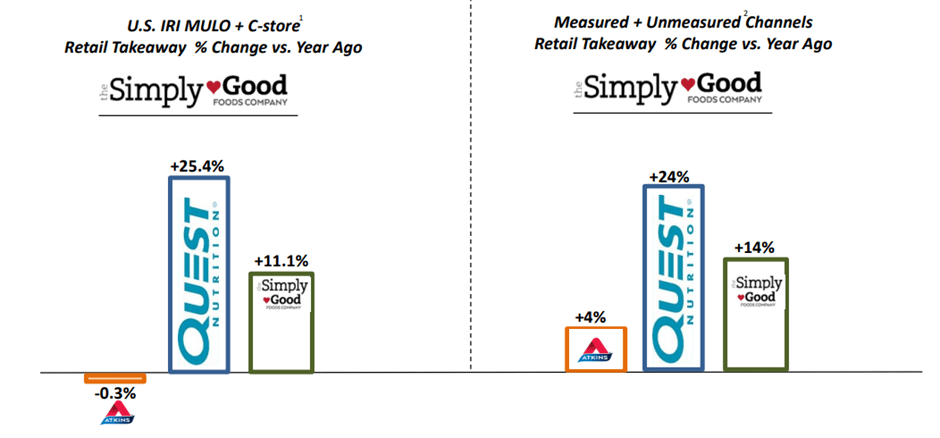

Price-Driven Revenue Strength

SMPL kicked off the fiscal year with solid results - net sales grew +7% YoY to $301m on strong pricing at +9.8%, which more than offset the -1.7% volume decline. Overall, US retail takeaway growth remains strong at +14%, with sales contribution from North America also up +7.8%. International was the detractor at -16.5% on weaker volumes and one-offs like shipment timing and FX movements, though the region’s relatively small contribution kept headline revenue growth strong.

{kind=link}

By brand, Quest remains the key driver at +24% takeaway growth across measured and unmeasured channels, though Atkins’ +4% growth for Q1 (acceleration from the +0.5% growth last quarter) marked a positive momentum shift. The resilient buy rate for Atkins is a highlight as well, particularly given the tough YoY comparison posed by the snack bar and confection innovations last year. And with more innovation in the pipeline post-New Year, Atkins sales could be on track for a near-term rebound.

Transitory Margin Headwinds

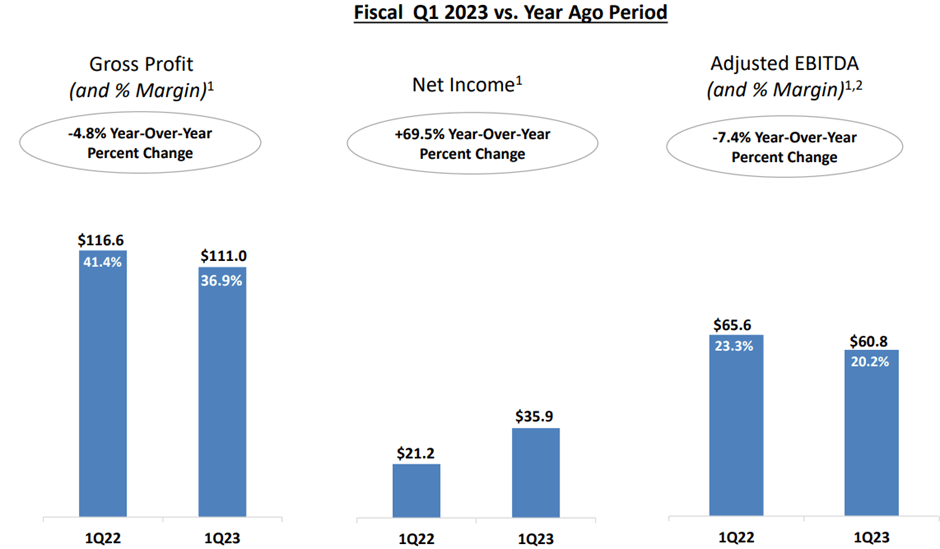

The gross margin performance was the key blemish in Q1 at a below-par ~37%. In contrast to expectations for ingredient and packaging to be the key headwinds, logistics and co-manufacturing issues turned out to be the main detractors this time around (the former two were in line with management expectations). Per management on the Q1 call , both the negative cost surprises were down to errors made during the prior CFO transition. The freight cost charge and increased co-manufacturing charges this quarter, for instance, were accrual charges that should have been budgeted for in previous quarters. In line with the gross margin miss, management-defined EBITDA (i.e., excluding depreciation and stock-based compensation) also disappointed; EPS, on the other hand, outpaced consensus, though this was largely due to a one-off tax rate tailwind.

{kind=link}

Beyond the one-offs, SMPL isn’t entirely out of the woods on input costs. Per management, inflationary pressures are still expected to weigh on Q2 results, although at a slower pace (in line with the easing commodity prices and CPI inflation data). Importantly, management sees signs of easing ingredient and packaging costs flowing through to the P&L later this year. So as inflation further winds down and management implements more robust accounting/operational processes, expect a quicker pace of gross margin improvement in H2 2023.

Upbeat Guidance Confirms Underlying Strength

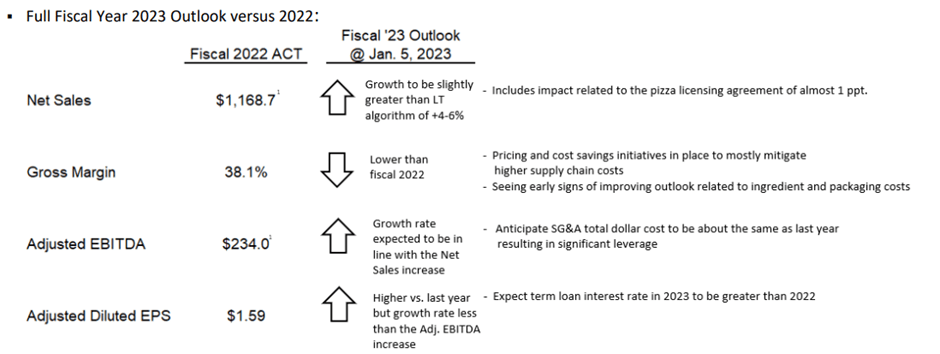

Management now sees the FY23 long-term sales growth guidance running slightly ahead of the +4-6% range, despite an ~1%pt headwind from licensing out the Quest frozen pizza business to Bellisio Foods. The path to achieving the FY23 target won’t be smooth, though, given the implied back-half weighted revenue trajectory - from a modest contraction in Q2, the full-year guide implies a growth rebound in H2 (mostly due to a Q4 acceleration). While this might seem optimistic at first glance, SMPL will benefit from a favorable YoY comparison due to irregular retail activity last year, so that the onus won’t be on a demand acceleration. Even if higher elasticity weighs on retail revenue as we enter a consumer/economic slowdown, SMPL’s mass channel distribution provides some insulation, along with the limited private label competition in its categories. Case in point - December multi-outlet growth remained strong at +16% despite the broader retail weakness and should improve as we approach the ‘New Year, New You’ season in January.

{kind=link}

Prospects for the rest of the P&L are less rosy, but better than expected. The gross margin line remains the key concern and is guided to contract YoY in FY23, though the updated projection for a slight YoY improvement in H2 2023 is positive. I suspect management is being a tad conservative here, given commodity and packaging prices are already off their multi-year highs. And as the rate hikes further impact economic growth, a meaningful decline in input prices resulting in accelerated gross margin improvement in H2 seems likely. Finally, adj EBITDA growth is set to be in line with net sales growth at +4-6%, though this conservatively doesn’t factor in any operating leverage benefits from cost initiatives by the new CFO, Shaun Mara.

Quality at a Reasonable Price

SMPL’s Q1 results may have been weighed down by some negatives on the margin side, but there were positives as well. With the full-year guidance baking in potential macro headwinds this year, there is ample room for earnings upside should management deliver on lowering costs and as inflationary pressures ease.

Most importantly, though, the Atkins brand showed a promising QoQ all-channel growth acceleration in Q1 ahead of new product innovation later in the spring. Alongside the continued strength at Quest, a potential Atkins recovery bodes well for the pace of leverage reduction going forward, along with shareholder returns. Given the projected >30% YoY EPS growth in FY23 and takeout optionality (e.g., the Clif Bar/Mondelez deal was struck at a higher EV/Revenue valuation), the current valuation screens reasonably.

For further details see:

Simply Good Foods: Quality At A Reasonable Price