SMPL - Simply Good Foods: Risk/Reward Profile Is Not Favorable For New Investors

2023-06-20 18:26:49 ET

Summary

- I believe Simply Good Foods is slightly overvalued, and so it's not a good time to start a new position, but current investors should not sell.

- SMPL has a solid presence in the health foods category and decent financials, but the company needs to lower prices to entice more consumers to try healthier options.

- I will keep SMPL on my watchlist and reassess the company if the stock price gets closer to the calculated intrinsic value of $26.42.

Investment Thesis

With Q3 around the corner, I wanted to take a look at Simply Good Foods ( SMPL ) outlook and financials to see if the current valuation is justifiable. With decent growth in the e-commerce space through their website and Amazon (AMZN), it looks promising, however, I do not think it is a good time to start a new position as my growth assumptions suggest the company is slightly overvalued right now, coupled with a tough economic environment still potentially coming up, I could see a better entry point within the next 6-12 months.

Outlook

The healthy food industry isn’t going away anytime soon. It is needed now more than before due to the lockdowns and people putting on weight since we weren’t able to go out much for the first year or so. Now that the lockdowns have been lifted for a while now, people are going back to being more active to make up for some of that lost time. It is hard for me to go cold turkey and just eat healthy. That's how Quest Pizza sometimes finds its way to my fridge. It’s not the greatest but it’s better than a Domino’s pizza, nutrition-wise.

Everyone is becoming more health conscious every day and companies like SMPL will stick around for a while if they manage to offer something that is affordable and doesn't sacrifice taste completely. I've had success recently with cauliflower base pizzas and honestly, it tasted better and had a nice crunch to it.

One drawback of healthy foods is the price point. It is hard to get people to start eating healthier if the healthy options are much more expensive than regular foods. Even frozen pizzas sold by SMPL are still slightly more expensive than other brand pizzas which most likely will put off a lot of people.

The company is doing very well in growing its e-commerce presence, with decent sales numbers for both Atkins and Quest product lines. Quest's product line is doing slightly better than Atkins at the moment. If the company can continue its expansion online, it will maintain a good spot among the top leading nutritional brands.

Digitization is the best way to achieve higher margins and the more the companies prioritize going online, the better off the companies will be in the long run. According to the Q2 ’23 transcript, the penetration of health foods in households is still rather low at around 50%, so the growth can be massive if SMPL can find a way to entice more consumers to try out the healthier options, but I believe that they will need to lower prices.

Financials

Just to note that the graphs below will be as of FY22, which ended in August of last year. I will mention the most current numbers also for extra color if needed.

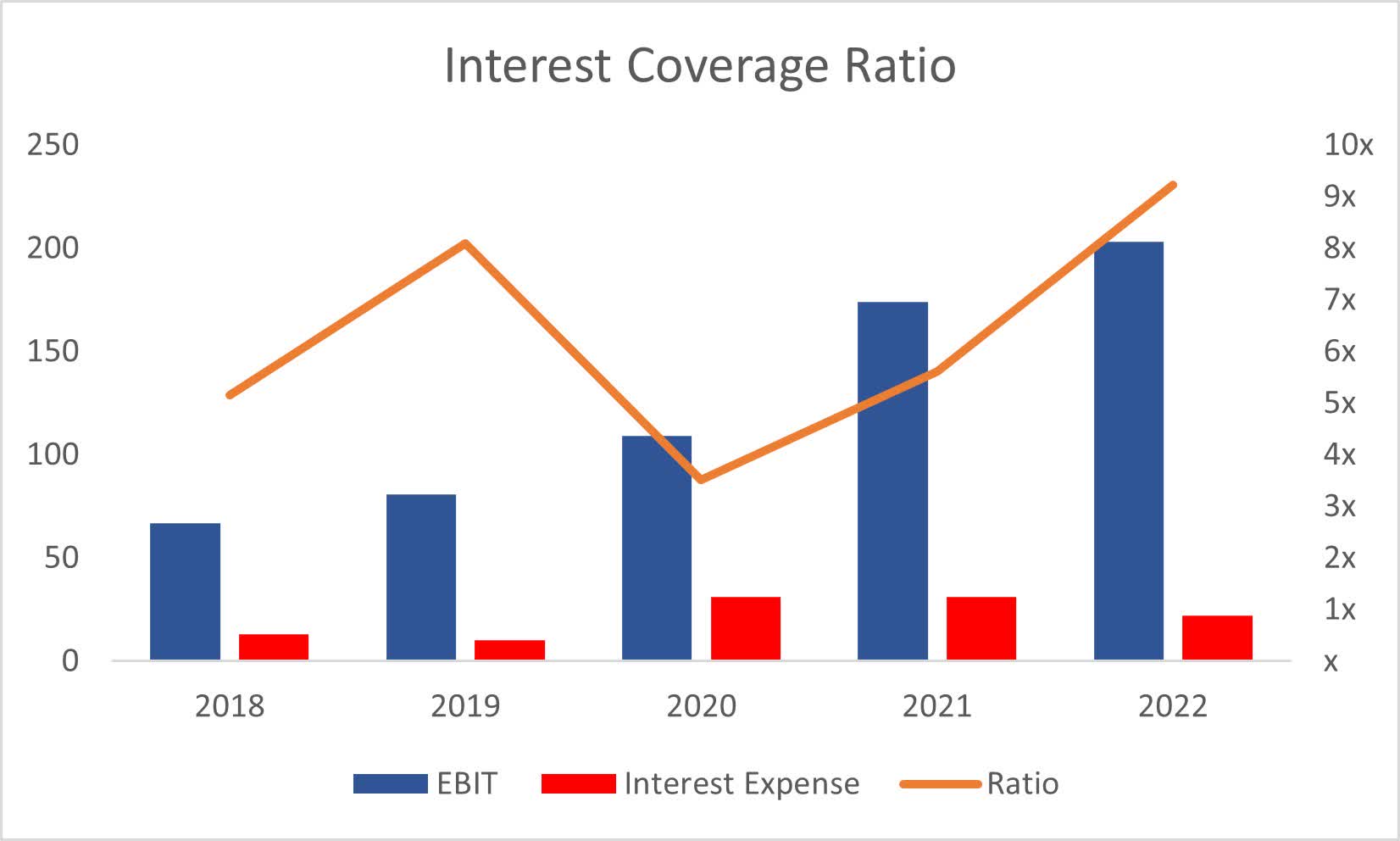

SMPL at the end of Q2 23 had around $63m in cash which decreased slightly from FY22, while having around $363m in long-term debt, which decreased by around $40m since the end of FY22. I like that the company is reducing debt, however, having debt on the books is not necessarily a bad thing especially if the interest payments are manageable. In the case of SMPL, the payments are very manageable. The interest coverage ratio at the end of FY22 was around 9x, which means that EBIT can pay off the interest on debt 9 times over. With further reductions in debt, the company will have more flexibility in the long run to use the money it made on rewarding shareholders in the form of share buybacks, dividends, or M&As.

{kind=link}

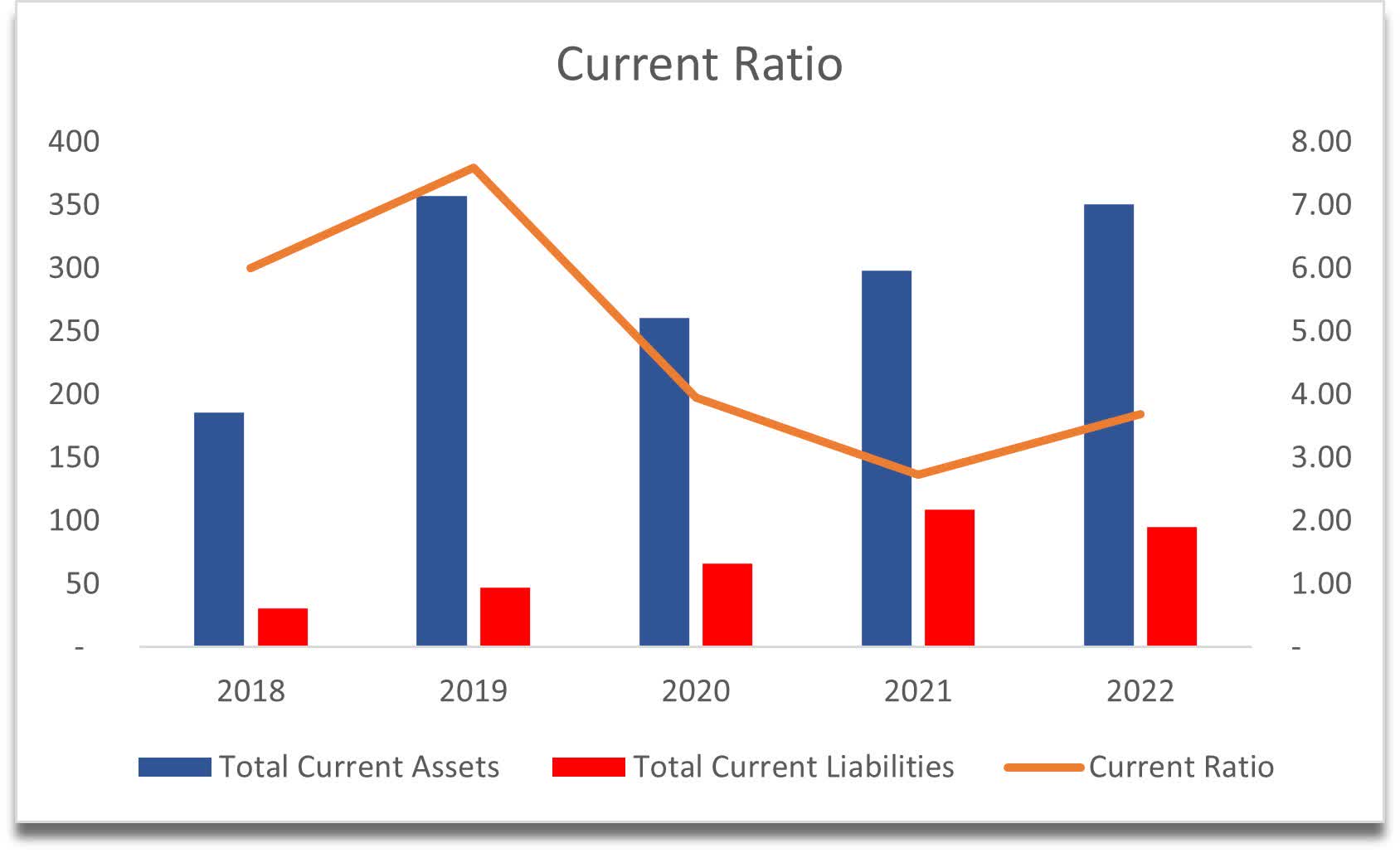

Continuing on to liquidity, the company’s current ratio, or working capital ratio, has been very solid over the years and I don’t think it’s going to change anytime soon. SMPL has no liquidity issues as it can cover its short-term obligations 4 times over.

{kind=link}

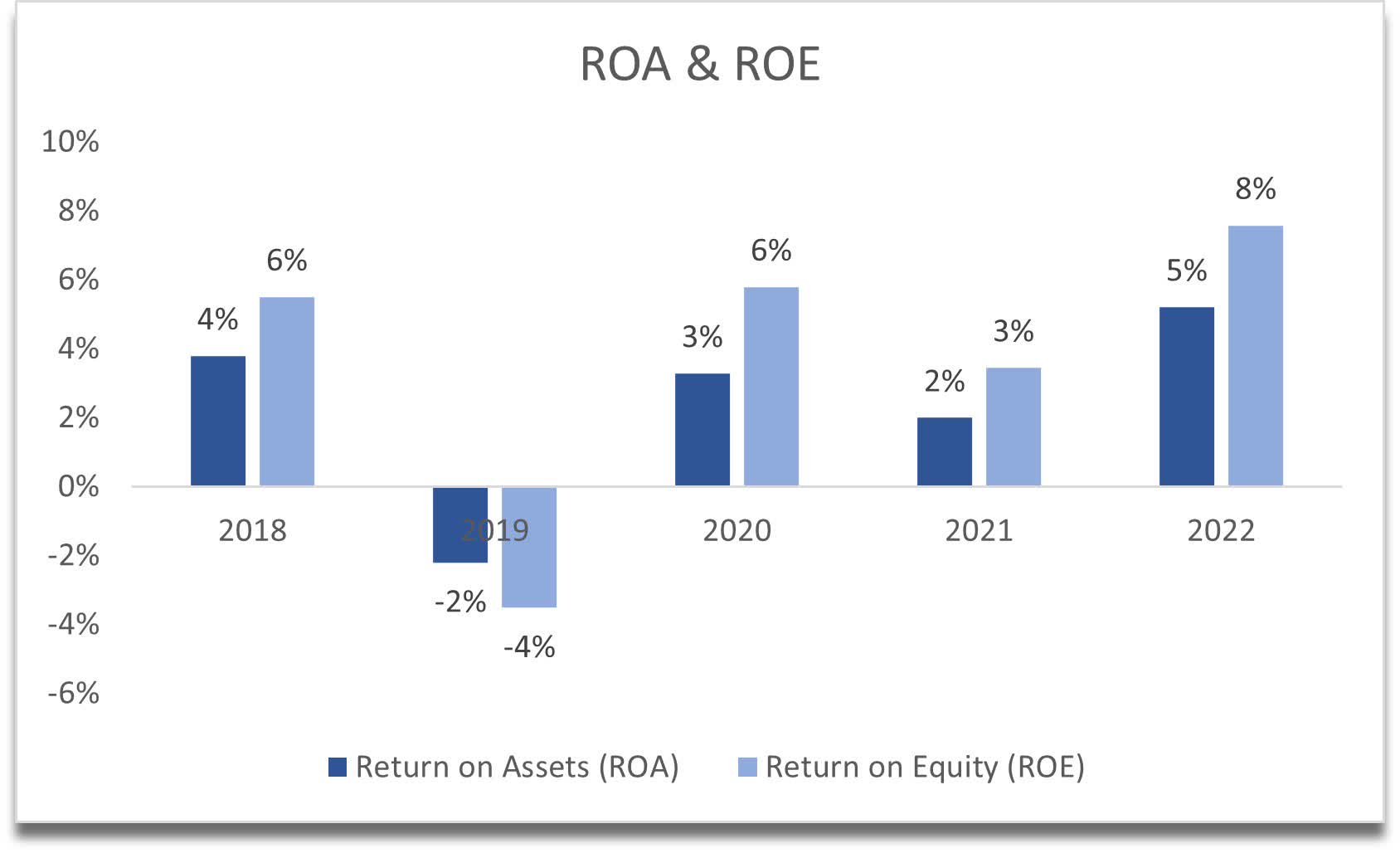

Going into efficiency and profitability, the company has been doing a decent job here also, with ROA and ROE at around the minimum I'd like to see a company achieving. There was a slight dip into the negatives one year but then they quickly recovered to their normal levels. I'd like to see the company increase these, but right now it also looks like the management is utilizing the company's assets and shareholders' capital effectively.

{kind=link}

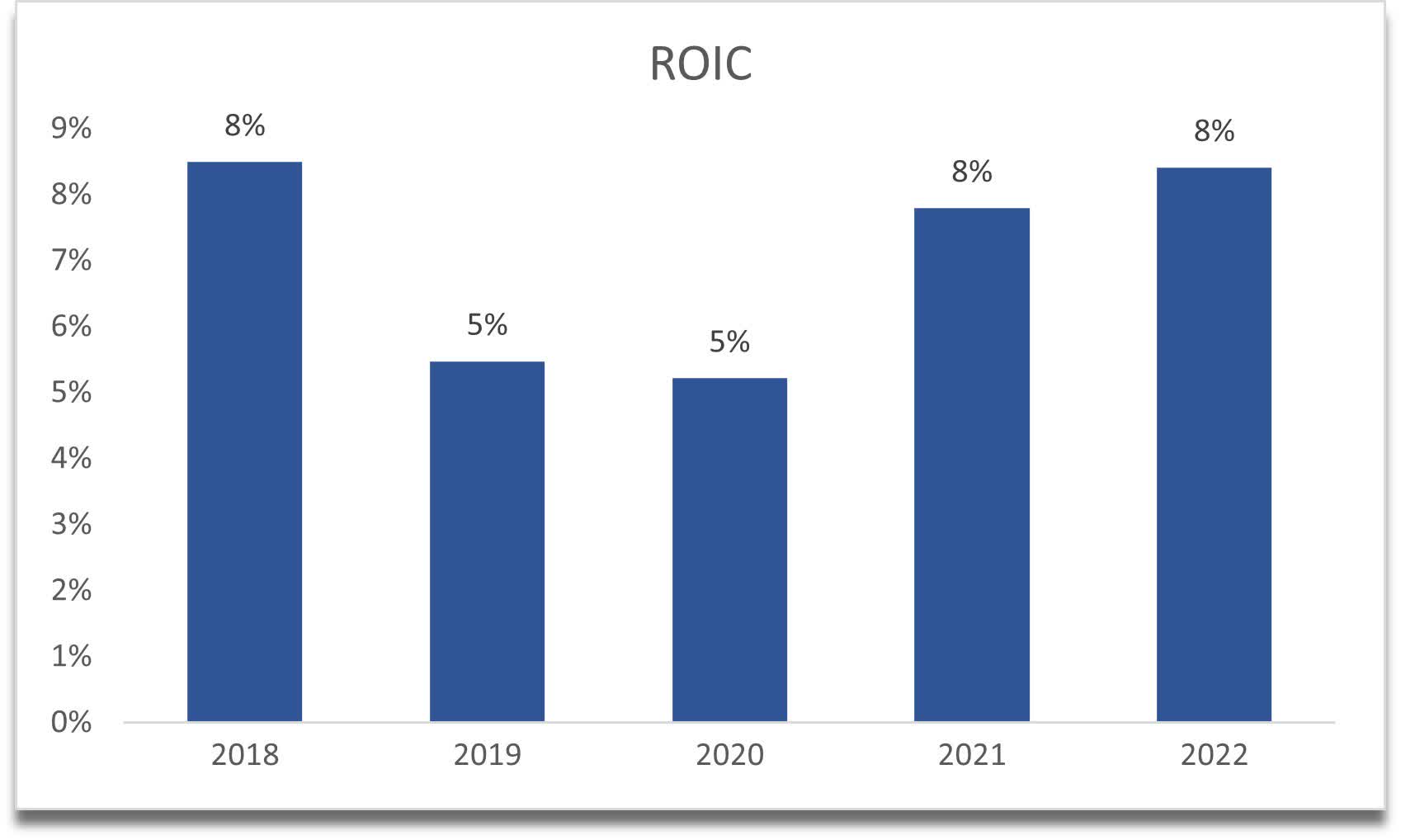

Return on invested capital is also within a respectable range, however, I’d like to see at least 10%. Nevertheless, 8% is still quite good, which means that the company is likely enjoying some sort of competitive advantage and it also has a decent moat.

{kind=link}

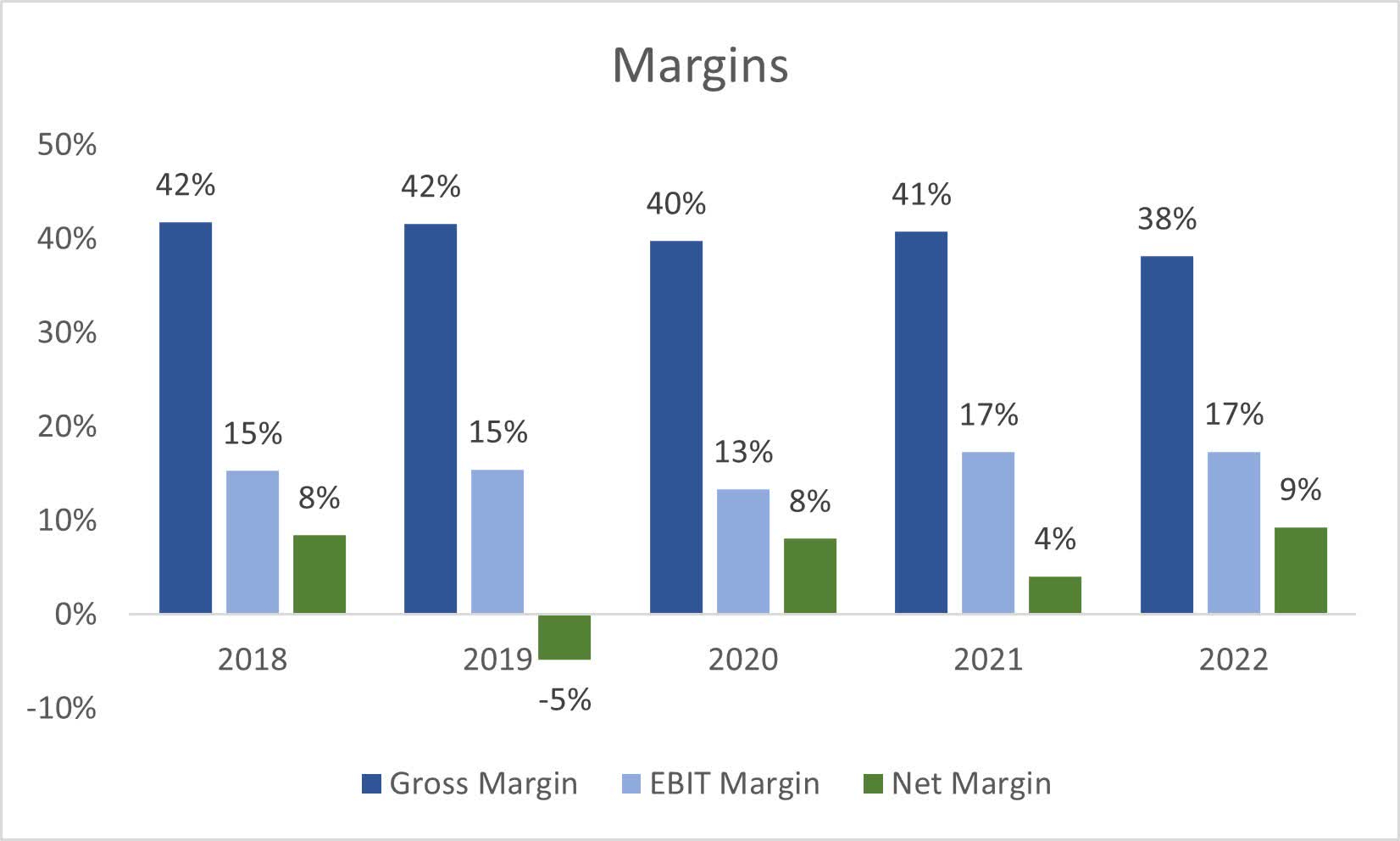

In terms of margins, at the end of FY22, the company saw a decrease from previous years, and during the latest transcript, the company saw slight declines further that may persist for the rest of the year until it gets back to at least the previous margins. I’d like to see the management taking action so the margins can come back to the levels we saw in ’18 or even better in the future.

{kind=link}

Overall, the financials look decent with slight worries about temporary margin declines. Other than that, the company seems to be geared very well for any sort of economic downturn that we may be heading toward in the next 6-12 months. I've been saying this for half a year now and we still haven't experienced much of the supposed economic downturn, but I'd rather be on the cautious side.

Valuation

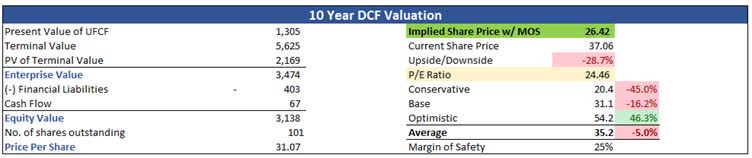

As I want to take a more cautious approach, I will assume that the revenue growth for SMLP will be around 9% for the base case over the next decade. For the optimistic case, it will be around 13% CAGR, while for the conservative case, it's going to be around 7% CAGR for the next decade. These numbers to me seem reasonable and the company may experience any of these outcomes in the future.

On the margins side, I decreased gross and operating margins by around 50bps in ’23 to reflect what the management is seeing. After that, the margins will start to increase linearly to where gross and operating margins will improve by 200bps or 2% in the next decade. I believe that with further digitization efforts and continual growth of the e-commerce space the company will achieve better profitability over the long run, and I could see it becoming more efficient.

On top of these estimates, I will also add a 25% margin of safety. This is the lowest I would like to add to the companies that have decent financials, which I think SMPL does. With that said the intrinsic value of Simply Good Foods is $26.42, implying around 29% downside from the current valuation.

{kind=link}

Closing Comments

Right now, I would say it is not a good time to start a position as I believe the risk/reward profile is not favorable and may underperform in the long run. For the current investors of the company, I wouldn’t suggest selling either because I don’t believe in selling just because it is slightly overvalued, and if you believe in the company in the long run, you will welcome further drops in price. The company has a solid presence in the health foods category with two great brands and with more people becoming healthier every day, the demand for current healthy foods that the company offers is going to stay and maybe even increase in the future if the management is going to experiment with new offers that are cost-efficient not just for the company but for the consumer as well.

I’ll keep the company on my watchlist and have a price alert set closer to the calculated intrinsic value above. If it does get closer, I will reassess the company to see if the thesis has changed over time and decide whether I want to be an investor or not.

The newly appointed CEO may be able to bring some food innovation to the table which can help SMPL penetrate more households around the globe but only time will tell. I will be tuning into the next upcoming quarterly report to see how the margins have developed over the last 3 months and will look out for any clues about the future demand for the company’s products.

For further details see:

Simply Good Foods: Risk/Reward Profile Is Not Favorable For New Investors