SSD - Simpson Manufacturing Is A Quality Addition

2023-04-18 17:29:39 ET

Summary

- Simpson Manufacturing Co., Inc. is a well-established company that will be able to benefit from market trends and be able to post consistent growth.

- Established within their markets they have the possibility to take even more market share and dive into new territory as well, especially the commercial side.

- The company has one of the strongest balance sheets I’ve seen in the industry and with the stability it offers, I think it deserves a buy rating.

Investment Summary

Simpson Manufacturing (SSD) is a leading California-based company that specializes in designing, engineering, and manufacturing building construction solutions. It primarily focuses on selling wood and concrete products.

Besides what's already mentioned the company also offers a wide range of products and solutions to address various building needs, including structural products, anchoring systems, and software solutions.

This wide list of offers has made the company able to steadily increase revenues, and the last earnings report was no different. Much of the construction and building sector has seen a resurgence in popularity and SSD is no different. Despite the run-up in share price I still think the company offers good potential and I will be rating them a buy.

Market Outlook

The company holds a significant market share in some of the industries operates in. In an investor presentation by the company, they bring some more clarity on this.

Company Market (Investor Presentation)

As seen above they have exposure to several different markets and the ability to still grow within them somewhat. But even if they aren't able to capture more market share, I think there is a good chance they will be able to grow in the same space as these markets themselves. The global concrete market for example is expected to have a 9.1% CAGR between 2022 and 2026 according to a report by researchandmarkets .

Capital Allocations (Investor Presentation)

With the already large presence SSD has in its niche market I think they will experience similar growth. Part of the reason I believe this to be true is the large amount of capital the company is committing to making this true. In 2022 they focused on making strategic acquisitions and they seem to remain confident in this strategy to create a long-term growth picture. This optimism and outlook are not just me talking, it's also shared by the management of SSD. In the last earnings report CEO Mike Olosky said the following "Looking ahead, we are confident in the trajectory of our business despite the softer market forecasts for U.S. housing starts. We continue to believe Simpson remains well-positioned for success given our ongoing focus on expansion of our growth initiatives into new markets, including commercial". I think SSD is a stable addition to a portfolio, I wouldn't expect massive growth but instead, a quality-run company that will consistently be able to meet expectations.

Risks

Looking at the broader building products industry risks like the volatility of the construction market, which is closely tied to the overall strength of the economy. During periods of economic downturn, the demand for new construction projects tends to decline, as businesses and consumers are more cautious about investing in real estate. This can lead to lower sales and revenue for companies in the building products industry.

Another significant risk facing the industry is the increasing costs of raw materials such as lumber, steel, and cement. The prices of these materials can be highly volatile, and sudden changes in the market can have a significant impact on the profitability of building product companies. I think this ties in the most with SSD. If they aren't able to pass on these increased costs to consumers then the likelihood of their margins taking a hit is very high. This I think would bring a lot of uncertainty around the company and potentially push down the share price a fair bit also.

Financials

Simpson Manufacturing Co Inc's balance sheet shows a significant increase in its total assets from $1.48 billion in 2021 to $2.51 billion in 2022, representing a 69% growth in just one year. The increase in total assets is mainly due to the significant increase in goodwill, which jumped from $134 million to $503 million. This increase is something I won't pay too much attention to. Some people include goodwill in their valuation of a company, but for me, I don't place too much importance on it. Instead, I think it's more interesting to see the company maintaining a strong cash position of around $300 million, only decreasing very slightly YoY. I think this puts the company in a very healthy position financially and makes them able to invest into the new market opportunities they seemed to be excited about in the last report.

Assets (Earnings Report)

One very noticeable shift between 2021 and 2022 is the company taking on debt. $554 million to be exact. For a company having over $200 million in levered free cash flow though I am really not that worried about this. If the company prioritizes paying back debt using its current cash flows, then it would be done in just over 2 years. A short timeframe which I think is healthy for the company. I think it will be interesting to see how the company is able to capitalize on this and grow its core business.

Liabilities (Earnings Report)

All in all, I think the balance sheet for SSD is extremely healthy as is with most companies in this sector to be honest. There tends to be a priority on a large amount of cash and strong cash flows that can easily tackle new debt which a company takes on. SSD is no different here. I see now risks here about the company needing to dilute shares in order to raise capital to meet obligations. Instead, I see the possibility of share buybacks continuing to happen and boosting the value shareholders have in the company.

Valuation & Wrap Up

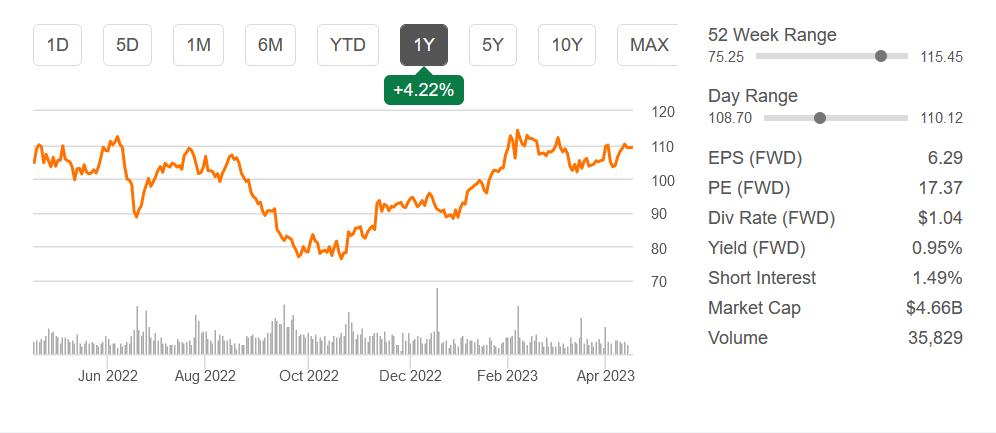

Despite the companies which have exposure to the construction industry I still don't think SSD is unreasonably valued. The stock has rallied quite a bit from the October lows in 2022 of around $78 per share to now around $109 per share.

{kind=link}

One should note that the forward p/e for the company is increasing a fair bit compared to the TTM one. The slowdown in building projects is happening and it will of course affect the revenues and EPS of companies like SSD. However, paying around 17x forward earnings is still not that bad given the quality of the balance sheet the company has and the focus the management places on bringing value to shareholders through either buybacks or dividends.

If you want a high-growth company then I don't SSD is for you. Instead, I think SSD offers a stable opportunity that offers exposure to a right now slowing industry. But when the turnaround happens the rewards will come quickly. In the meantime collecting a decent dividend and sitting pretty stable whilst the rest of the market experiences a lot of volatility doesn't sound so bad.

For further details see:

Simpson Manufacturing Is A Quality Addition