SSD - Simpson Manufacturing: Multiple Expansion Driving Performance

2023-07-20 12:47:46 ET

Summary

- Simpson Manufacturing's stock has benefitted from a rally in the building products segment.

- A unique set of events has driven the construction market over the past year.

- Existing shareholders may benefit from taking some profits, while new investors may have to wait for a lower valuation.

I rated Simpson Manufacturing Co., Inc. ( SSD ) a hold in April . Since then, the stock has been on a tear, returning 39% compared to the 9.9% return of the S&P 500 Index. The company’s engineered products must meet the strict building code requirements, which bestows the company with a certain level of competitive moat. This moat translates into superior gross and operating margins. But, the stock has run up a lot, and the uncertain economic environment adds to my belief that it is best not to chase this rally. Much of the run-up is due to multiple expansions rather than better growth, profitability, and fundamentals. Existing investors sitting on gains should consider taking some money off the table and let the rest of it run. New investors should wait for a lower entry price point before buying.

Good Q1 revenue growth, but uncertainty remains

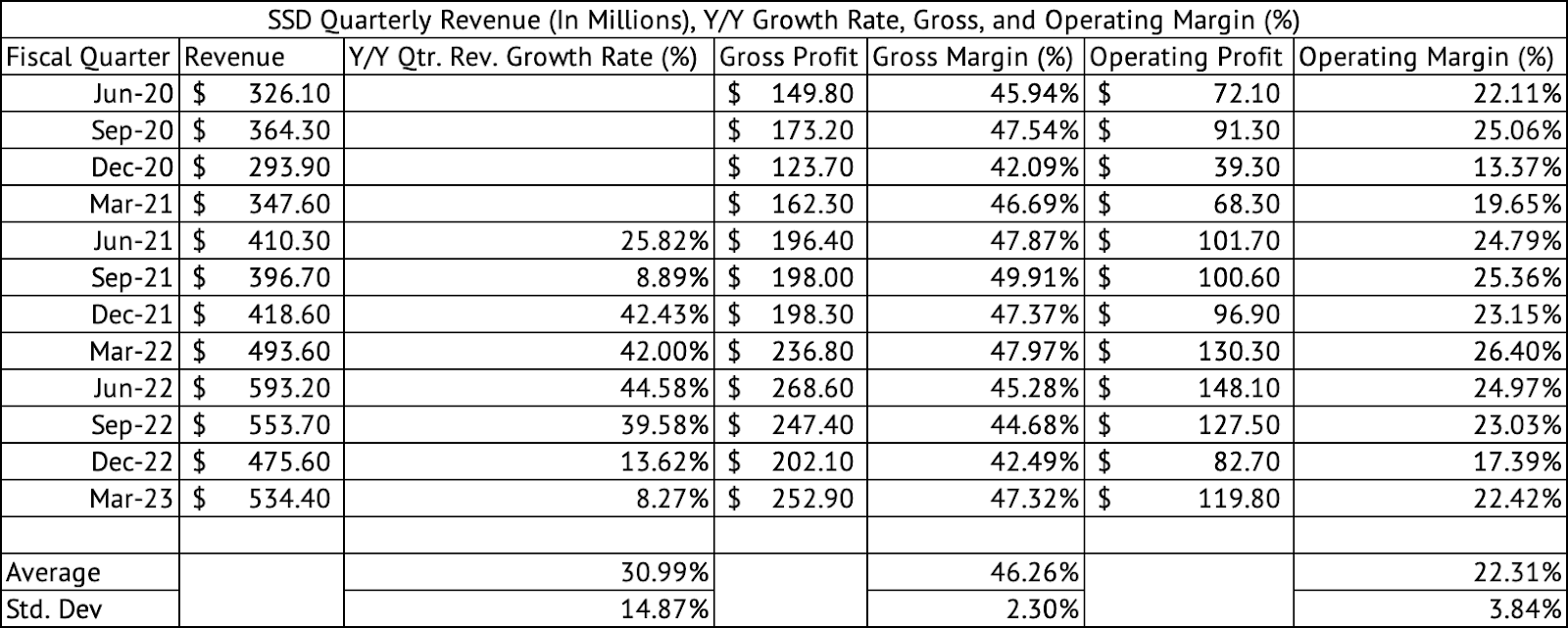

The company registered a net sales growth of 8.3% y/y (Exhibit 1) , but its sales in North America were lower by 7.4% y/y due to lower volumes. The company mentioned that the high levels of precipitation on the West Coast hampered its sales. Unfortunately, disruptions to business activity due to severe weather, such as the record rainfall in California, may be here to stay.

Exhibit 1:

Simpson Manufacturing Quarterly Revenue, Gross, Operating Profits, and Margins (Seeking Alpha, Author Compilation)

{kind=link}

Currently, we are in the midst of concurrent weather-related disasters across the globe , and there are no signs of this trend fading. Businesses such as Simpson Manufacturing and its investors may have to get used to these disruptions, wrecking revenue growth, profitability, and the management’s well-laid plans.

Ironically, these events could also lead to more demand for Simpson Manufacturing as stricter building codes are made law and buildings are reconstructed after being destroyed during severe weather events. These disasters can also significantly impact inflation, especially if food production is hampered. If inflation does not fade to the Fed’s desired 2% target, the central bank could be forced to continue increasing rates, dampening demand for new homes and cars. The CEO, Mike Olosky, mentioned that the western and the southern regions of the United States use a higher volume of Simpson’s products due to the stricter building codes to withstand the higher wind and seismic events.

Multiple expansion drive the stock's performance

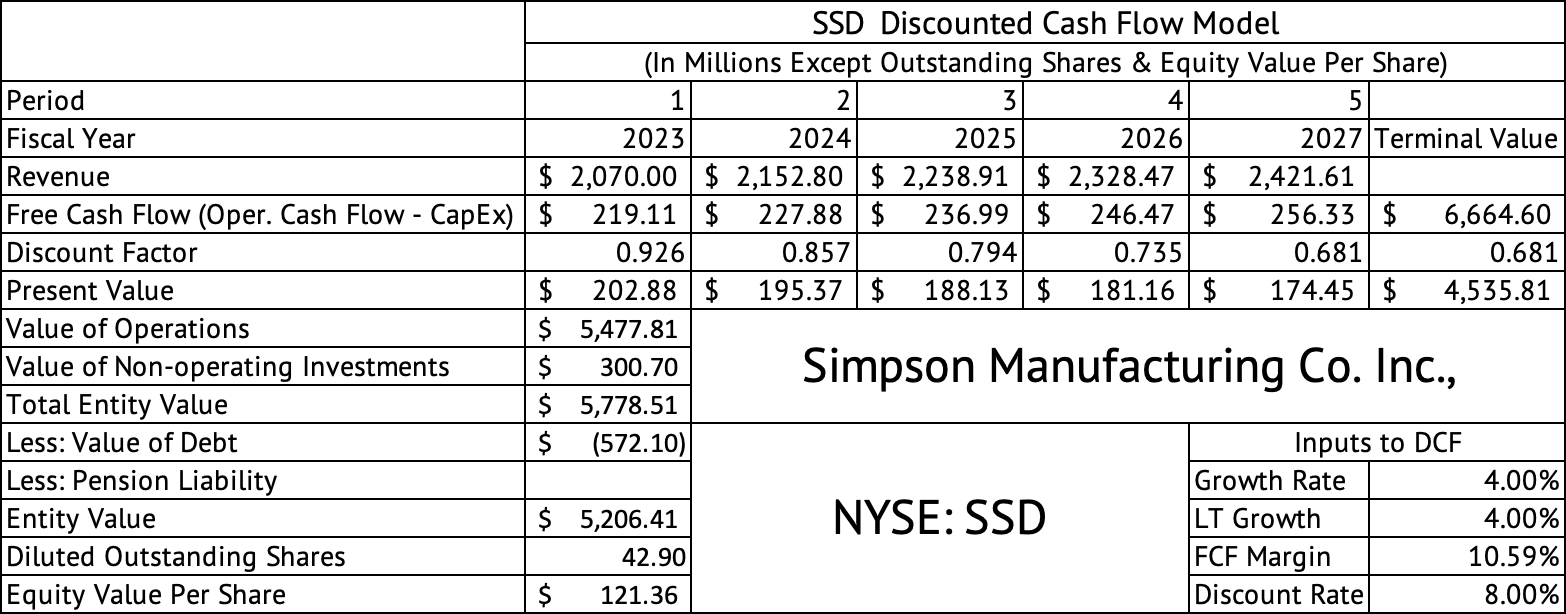

The stock was trading at a forward GAAP PE of 17.4x in April. It now trades at 21.3x its five-year average PE. The stock’s free cash flow yield, which was 7.1% in April, has dropped to 4.5% based on the trailing twelve-month data and the share price of $151. A discounted cash flow model estimates the per-share equity value at $121 (Exhibit 2) . This model assumes a growth rate of 4%, a free cash flow margin of 10.5%, and a discount rate of 8%. This free cash flow margin is its long-term average.

Exhibit 2:

Discounted Cash Flow Model for Simpson Manufacturing Company (Seeking Alpha, Author Calculations)

{kind=link}

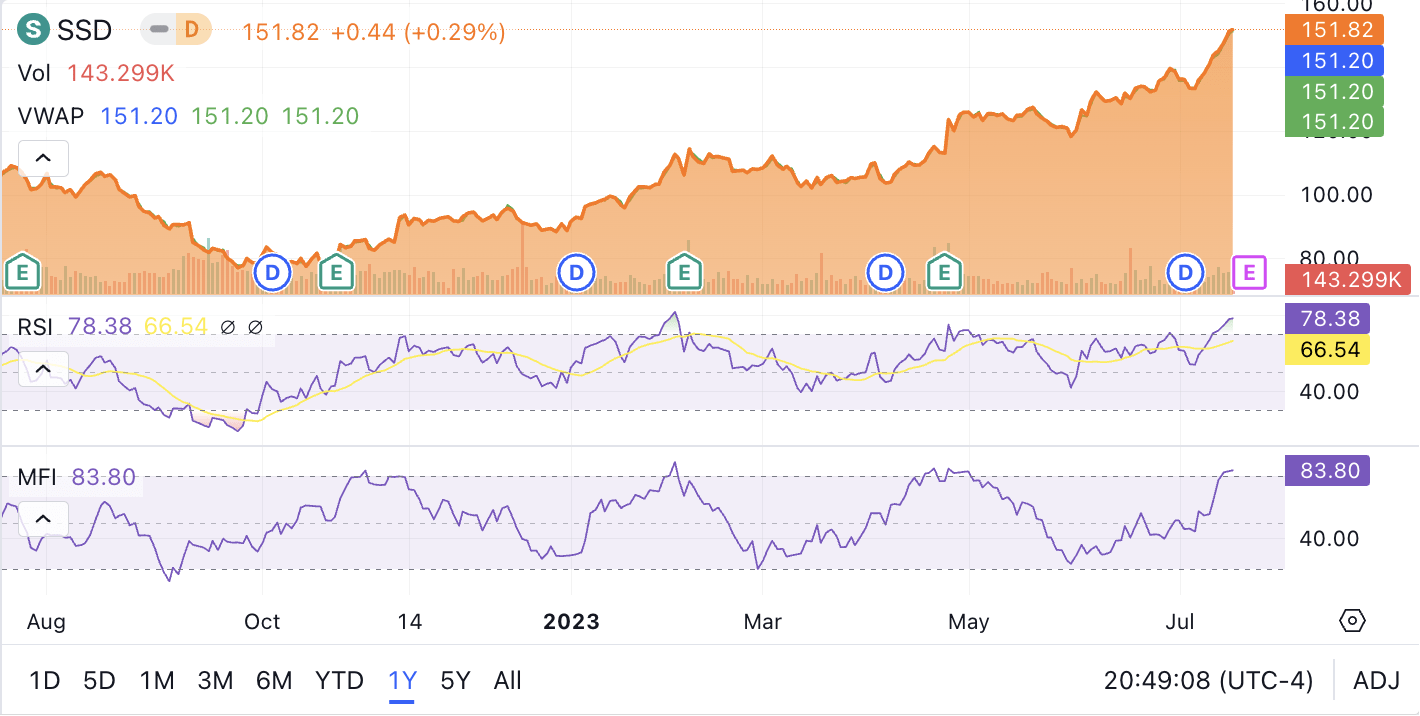

The stock has had great momentum over the past year, gaining over 40%. The company has done exceptionally well in the past three months, returning 36%. The stock trades at overbought levels based on the RSI and MFI technical indicators, raising the risk of a drop in price (Exhibit 3) .

Exhibit 3:

RSI and MFI Technical Indicators for Simpson Manufacturing Company (Seeking Alpha)

{kind=link}

The stock has a beta of 1.22 , meaning it is more volatile than the market. Positive momentum has driven the major indices to new heights, and the building and construction sector found new energy due to the absence of old homes for sale, driving the demand for new homes. Many building products companies , including Simpson Manufacturing, have hit 52-week highs. This synchronized rally is expanding valuations multiples and can quickly fade if the fundamentals do not catch up with the valuations.

The market seems to ignore management’s comments about uncertain economic conditions in the second half of 2023 and their forecast for lower margins for the year. However, the company showed excellent margin improvement in Q1 2023 with a 47.3% gross margin and a 22.4% operating margin. These margins are a significant improvement from the December 2022 quarter (Exhibit 1) .

Best-in-class margins

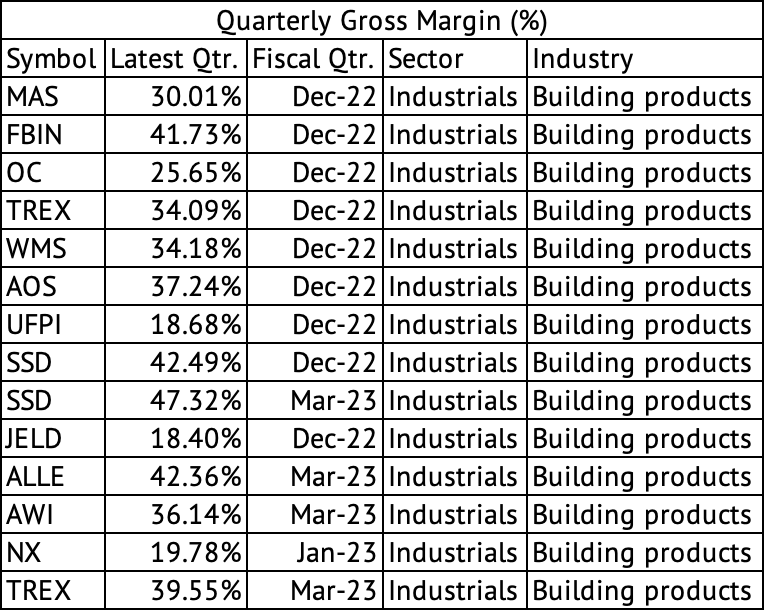

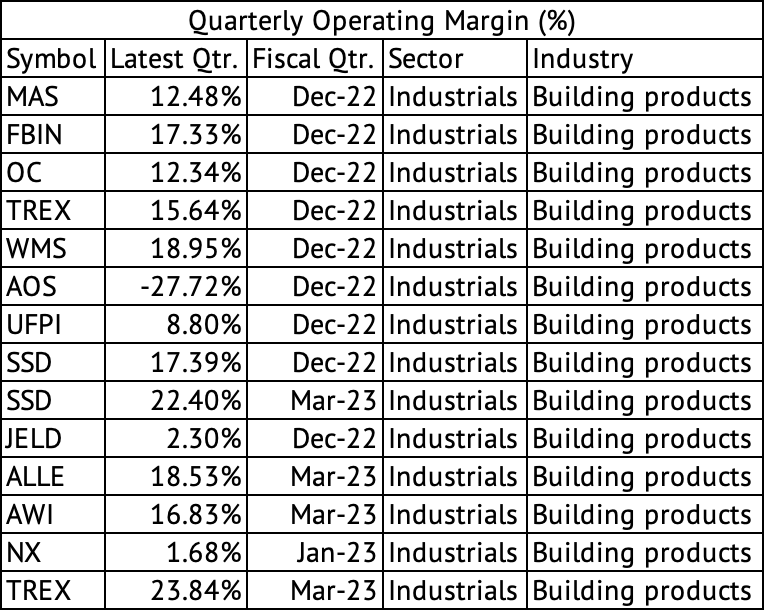

The company’s margins were already best-in-class, which may be why it deserves a valuation premium (Exhibits 4 & 5) . But, the company warned that its operating margins for the year will fall between 19% and 21%, below its average of 22.3% since June 2020. The company is benefitting from lower steel prices but sees weakness in the second half of the year, leading to lower volumes and an increase in headcount to further its strategic initiatives, leading to lower operating margins.

Exhibit 4:

Quarterly Gross Margin Across Building Products Companies (Seeking Alpha, Author Compilation)

{kind=link}

Exhibit 5:

Quarterly Operating Margin Across Building Products Companies (Seeking Alpha, Author Compilation)

{kind=link}

Low debt ratio and dividend yield

The company registered just $3 million in operating cash flow due to increased accounts receivables and inventory. The company used cash to cover its dividend and capex due to the low operating cash flow generation. However, this decrease in operating cash may have more to do with the seasonality since spring and summer are the peak construction season in the U.S. The company carried a total debt of $572 million, down about 0.8% from the $577 million it carried in the December 2022 quarter. Over the past twelve months, the company generated $545 million in EBITDA, resulting in a low debt-to-EBITDA ratio of 1.04x.

This massive run in the stock price has caused its dividend yield to drop to 0.7%. The Vanguard S&P 500 Index ETF ( VOO ) yields double that of Simpson Manufacturing, with a yield of 1.49%. But, this stock has traditionally been a low yielder, with most of its gains coming from its price returns. Over the past five years, the stock’s price return was 140% and a total return of 154.1%. In short, just over 14% of the returns were due to dividends.

Building products companies have benefitted from unique factors driving today’s construction markets. A large group of homeowners are tied to their current mortgages due to the low rates they locked in during the Fed’s zero-rate policy. This factor reduced the homes available for sale and thus drove more home buyers towards new homes. The demand for new construction could quickly disappear if rates increase further. Although the stock has gone on a massive run since I placed a hold rating in April, I am not convinced Simpson Manufacturing can go any higher, given its impressive returns over the past year. The company has benefitted from expansion in its valuation multiple and offers a low dividend yield. Existing investors should consider taking some profits after this run. New investors should continue waiting for a lower valuation.

For further details see:

Simpson Manufacturing: Multiple Expansion Driving Performance