SSD - Simpson Manufacturing: The Valuation Is Too Generous

2023-10-04 12:23:30 ET

Summary

- Simpson Manufacturing is a well-managed high-quality business with strong financial performance and a shareholder-friendly capital allocation approach.

- The company's revenue has compounded annually at a 13% rate over the past decade, and it has a stable and positive free cash flow margin.

- While the company is well-positioned to capture industry tailwinds, the stock is currently overvalued and better buying opportunities may be ahead.

Investment thesis

The American stock market surprises me every day because I explore new high-quality businesses in different industries regularly. Simpson Manufacturing (SSD) is one of the hidden gems because it is an under-the-radar, well-managed high-quality business. The company demonstrates stellar financial performance over the long term and cares about its shareholders by distributing dividends and conducting stock buybacks. SSD's positions in its core addressable markets are very strong thanks to a strong over half a century reputation and a wide portfolio of offerings to a broad spectrum of end markets. But the valuation looks too generous even for a high-quality business like SSD. I think that better buying opportunities are ahead to wait for on the sidelines and assign the stock a "Hold" rating.

Company information

Simpson Manufacturing Co, through its subsidiaries, designs, engineers, and manufactures wood and concrete construction products aimed to make structures safer and more secure. SSD's products are marketed for residential construction, light industrial, and commercial construction.

The company's fiscal year ends on December 31. The company's segments are the geographic areas it serves. According to the latest 10-K report , the North American segment accounted for approximately 80% of the company's net sales in FY 2022.

Financials

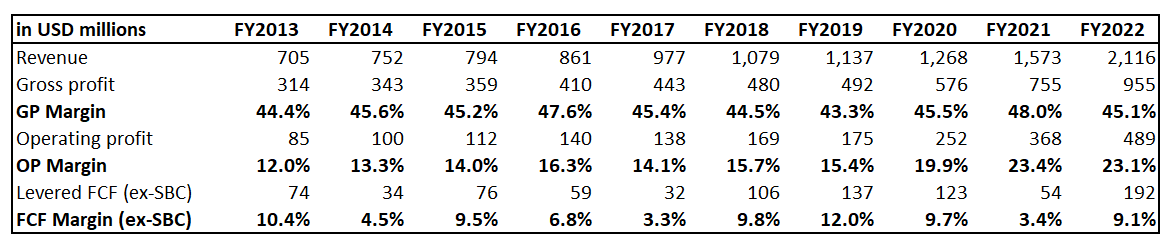

The company's financial performance has been strong over the past decade. Revenue compounded annually at a 13% rate. The gross margin has been stable at about 45% which means the company has been efficient in exercising pricing power to pass on inflationary effects on its customers. The operating margin almost doubled over the past decade which is a solid bullish sign to me since the company has been able to drive growth with the economies of scale effect. The free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] has been volatile over the past decade, but consistently positive, which is also a good sign.

{kind=link}

Having a stable and positive FCF margin allows the company to fuel growth with its own resources and rely less on debt financing. Therefore, despite being in a net debt position, the overall leverage ratio is relatively low and the covered ratio is higher than enough. Current liquidity metrics are also in excellent shape. The company sticks to a shareholder-friendly capital allocation approach with consistent stock buybacks and dividend payouts. The forward yield of below 1% is apparently low, but the long-term 10-year dividend CAGR of 7.7% looks decent. I like how the company balances between fueling growth, keeping shareholders happy, and maintaining a sound balance sheet.

Seeking Alpha

The latest quarterly earnings were released on July 24, when the company topped consensus estimates. Despite harsh macroeconomic conditions, SSD delivered a solid 8.3% YoY revenue growth. The bottom line also demonstrated a robust dynamic with the adjusted EPS expansion from $2.3 to $2.5.

Seeking Alpha

The upcoming quarter's earnings release is scheduled for October 26. Consensus estimates project quarterly revenue at $557 million, which means it will be almost flat YoY with a subtle increase. The adjusted EPS is forecasted by consensus to slightly expand from $2.09 to $2.16.

Seeking Alpha

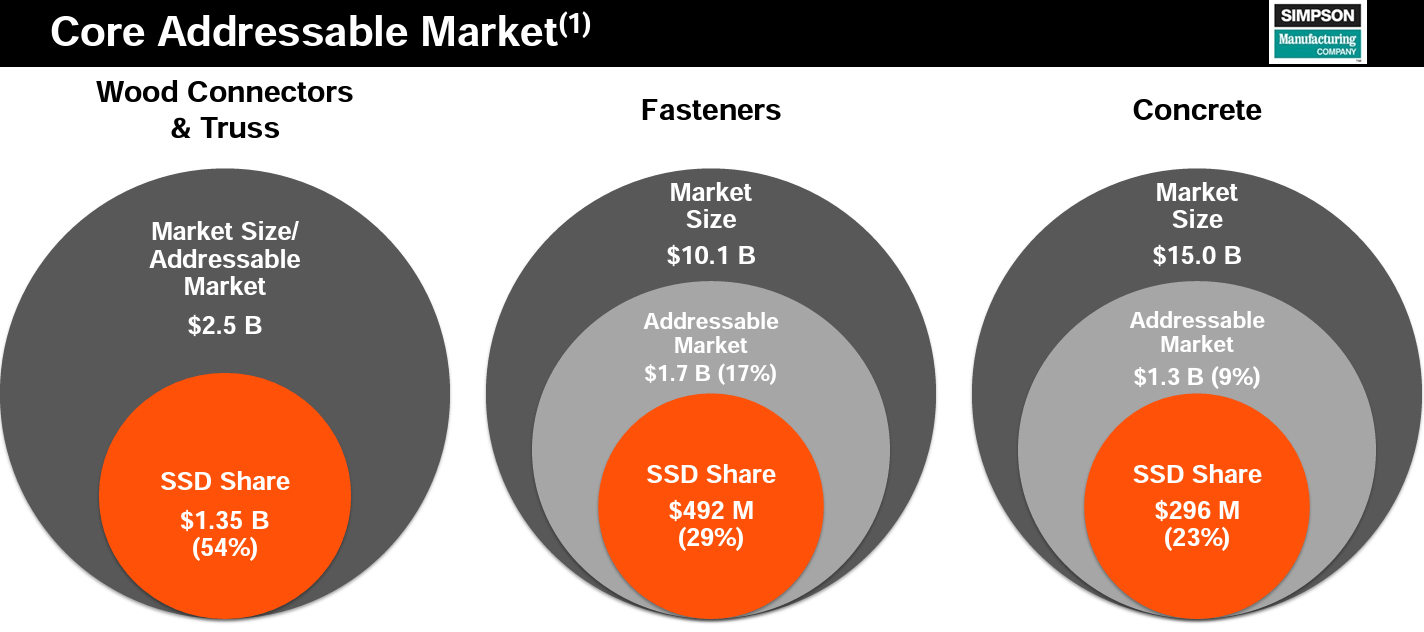

The long-term dynamic of the company's financial performance and sound capital allocation approach suggest the management does the right things to increase value for shareholders. I like the company's comprehensive presence across different end markets including construction for residential, commercial, OEM, and retail purposes. The company has a vibrant history of more than half a century and its strong reputation enabled SSD to gain notable market shares in segments where the company is present. Having strong positions across core addressable markets gives the company a strong pricing power, which is a good bullish sign for investors.

{kind=link}

According to CNN , the U.S. housing market is short about 6.5 million homes, which is a solid secular industry tailwind for SSD, even despite the current environment of macroeconomic turbulence and high-interest rates. The company's vibrant history and strong reputation together with a wide set of offerings and solid positions across core addressable markets, makes SSD well-positioned to capture secular tailwinds.

Valuation

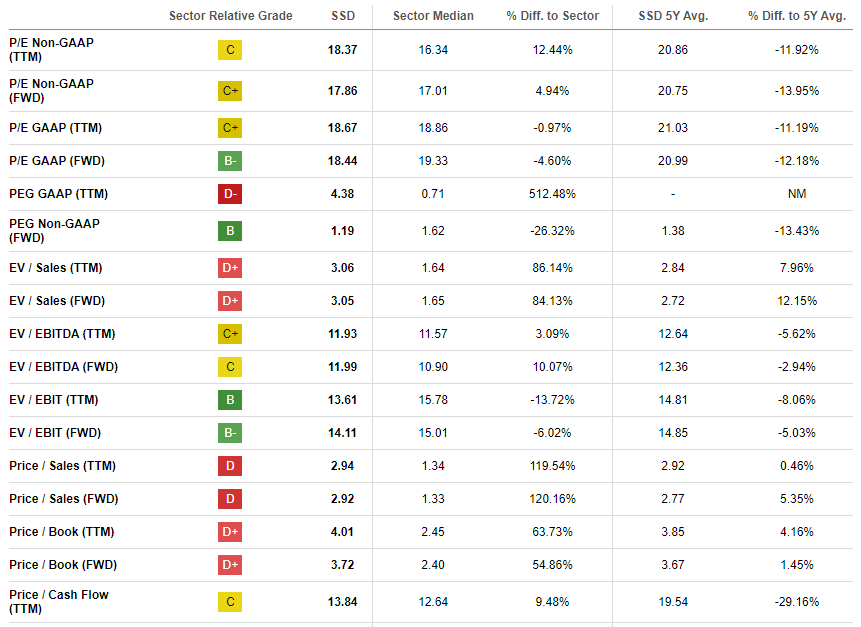

The stock rallied almost 60% year-to-date, significantly outperforming the broader U.S. market. SSD is currently trading not far from its all-time high. Seeking Alpha Quant assigns the stock a low "D-" valuation grade. Multiples are indeed substantially higher than the sector median and close to historical averages.

{kind=link}

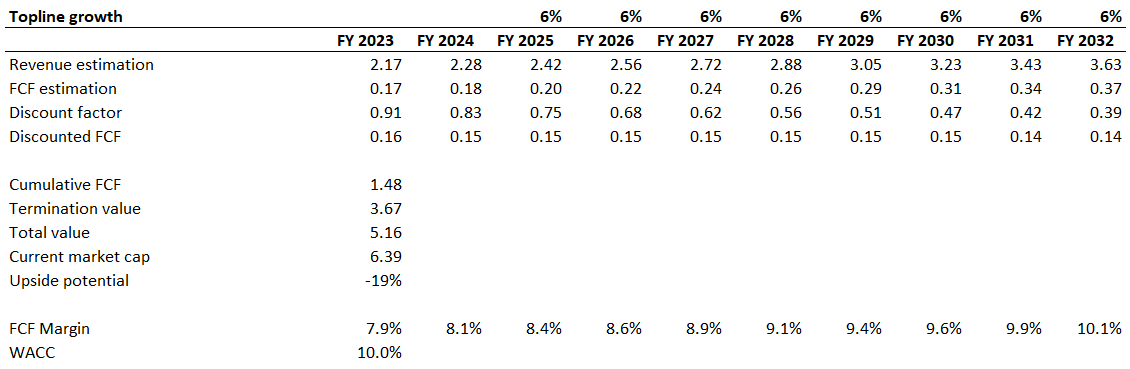

I want to proceed with the discounted cash flow [DCF] simulation. I implemented a 6% revenue CAGR after the projection of consensus for the upcoming two fiscal years. A 10% WACC looks fair given the company's consistently positive FCF margin. I use a 7.9% last decade's average FCF margin and expect it to expand by 25 basis points yearly.

{kind=link}

According to my DCF simulations, the business's fair value is about $5.2 billion, which is 19% lower than the current market cap. That said, the stock is overvalued with a target price of $118.

Risks to consider

The American construction industry is one of the major locomotives of the economy. According to statista.com , the U.S. construction industry is worth about $1.8 trillion. Such a massive industry attracts numerous contenders who want to take a bite of this vast pie. That said, the competition in the industry is poised to be ever-intensifying. Therefore, SSD should ensure that the company's offerings align with the technological landscape's development to stay competitive and protect its market share.

The construction industry is cyclical and significantly depends on the broader economy's health. The current environment of high interest rates also does not favor the sector, where new sales are heavily dependent on leverage. While cyclicality in the economy and interest rates is normal and we cannot avoid it, the key question today is for how long will interest rates stay higher. The recent job openings data suggests that the labor market is still very strong despite Federal Funds rates being at their highest since the beginning of the century. This leaves the door open for the Fed to continue monetary tightening and postpone the pivot to easing.

Bottom line

To conclude, SSD is a "Hold". Despite being an apparently high-quality business with bright future prospects, the valuation does not look attractive at all. The company's stellar financial performance and strong market positioning together with promising dividend growth make it definitely worth being on my watchlist. But I think that better buying opportunities are ahead.

For further details see:

Simpson Manufacturing: The Valuation Is Too Generous