SLP - Simulations Plus' Flagship Software Drives Q3 Growth

2023-07-08 05:36:05 ET

Summary

- Simulations Plus reported a 9% increase in total revenue in Q3 2023, driven by its software segment. However, declining gross margins and rising operational costs could impact future profitability.

- The company's stock has performed well, with a 518% increase in stock price from 2014 to 2023, and a "Strong Buy" rating from Wall Street analysts. However, its P/E ratio suggests possible overvaluation.

- Despite strong revenue growth, concerns over tightening margins, rising costs, and a declining service project backlog could impact future performance. The recent acquisition of Immunetrics.

Thesis

Simulations Plus has been riding a strong wave of growth, as showcased by its Q3 2023 performance, where the company recorded a robust 9% surge in total revenue, largely propelled by its software segment. However, mixed trends, including slightly declining gross margins, escalating operational costs, and dwindling service project backlog, indicate potential headwinds that might hinder future profitability. This article provides an in-depth review of the company's recent financial performance, its potential growth catalysts, and existing challenges, evaluating whether its current market valuation is justified.

Company Overview

Headquartered in the heart of Lancaster, California, Simulations Plus, Inc. stands as a force in the realm of software innovation for drug discovery and development. Its distinguished software applications, suffused with the power of artificial intelligence and machine learning, exhibit a unique capacity to model molecular properties and forecast their behaviors. The company's business operations are neatly divided into two primary branches: Software and Services.

The crown jewel of their product suite, GastroPlus , is a software tool that flawlessly simulates the process of absorption and the interactions between different compounds in both human and animal bodies. Complementing this flagship product are a number of other simulation tools, such as DDDPlus and MembranePlus.

Further strengthening its robust product offering, Simulations Plus, Inc. presents a range of products steeped in mechanistic and mathematical models. These include DILIsym, NAFLDsym, IPFsym, RENAsym, and MITOsym, integral tools in quantitative systems toxicology and analogous fields. They've also developed innovative software like the Absorption, Distribution, Metabolism, Excretion, and Toxicity Predictor, a tool that can predict molecular properties based solely on structural attributes. Moreover, their portfolio features modeling and simulation tools like MedChem Designer, MonolixSuite, and PKPlus.

Simulations Plus' Bullish Q3 2023 Earnings Highlights

In an energizing twist, Simulations Plus has punched in a vigorous Q2, boasting a total revenue surge of 9% that breaks down into a striking 10% climb in its software segment and a 5% bump in services. Interestingly, software shouldered 65% of this quarter's earnings, an uptick of 3% from the previous year. If you take a step back and look at the broader nine-month period, we're seeing a consistent growth pattern with a total revenue increase of 4%, underpinned by a 2% software ascent and a 9% leap in services.

In a compelling revenue mix, GastroPlus, the company's flagship software, claimed a 57% share of the quarter's software earnings. MonolixSuite and ADMET Predictor weren't far behind, chipping in 18% and 19% respectively. Reflecting on their customer relations, Simulations Plus recorded an impressive 96% renewal rate based on fees and 87% on accounts. Notably, the average revenue per customer also ticked upward, thanks to the combination of a price hike and seasonal factors.

On the flip side, there was a minor dip in the quarter's gross margin, ebbing to 82% courtesy of softer services margins. But let's not lose sight of the fact that over the nine months, the gross margin held steady at 81%. In the software department, there was a slight contraction from 92% to 91%, while the services margin clocked in at 63%.

Delving into the operational side of things, the increased R&D expenditure was largely attributed to the roll-out of GastroPlus version 10 and staff cost adjustments. SG&A expenses also saw a 21% rise due to an 11% hike in staff count and costs associated with mergers and acquisitions. As a result, operating income took a 17% hit, and net income nudged down by a modest 2%. Wrapping up the quarter, the company's war chest boasted $122.4 million in liquid assets and short-term investments.

In an exciting development, Simulations Plus threw its hat into the acquisition ring, scooping up Immunetrics in a deal that holds the promise to bolster its services arsenal and create a fresh revenue channel. The agreement specifies an upfront cash payment of $15.5 million, along with two potential earnout installments adding up to a cool $8 million, contingent on Immunetrics' revenue trajectory up until the end of 2024.

Expectations

Currently, Simulations Plus is covered by three Wall Street analysts who have a combined "Strong Buy" rating on the stock with average projected expectations of a +40% upside price target.

{kind=link}

Performance

Relative to its peers within the Health Care (Technology) sector, SLP currently shines as the frontrunner when it comes to it YTD price return.

{kind=link}

Also, in the medium term between 2014 and 2023, the stock price of this company rose dramatically - from $6.68 to $41.29 (an astounding 518% increase) which represents a strong investment return over 8.8 years (see data below).

In fact, SLP's annualized Return on Investment ((ROI)), excluding dividends, stands at a robust 22.9%, outperforming the broader market index S&P 500 Index by a remarkable margin and with an annual compound growth rate of 23.56%, including dividends, SLP has outperformed the S&P considerably, offering nearly twice the return

{kind=link}

The company's dividend distribution also provides interesting insights. Over the past eight years, dividend growth averaged 3.16% annually with one exception in FY 2018 when dividend per share jumped 20%, from $0.200 to $0.240. However, in FY 2023, the dividend per share dipped to $0.180, possibly indicating a shift in capital allocation strategy.

Valuation

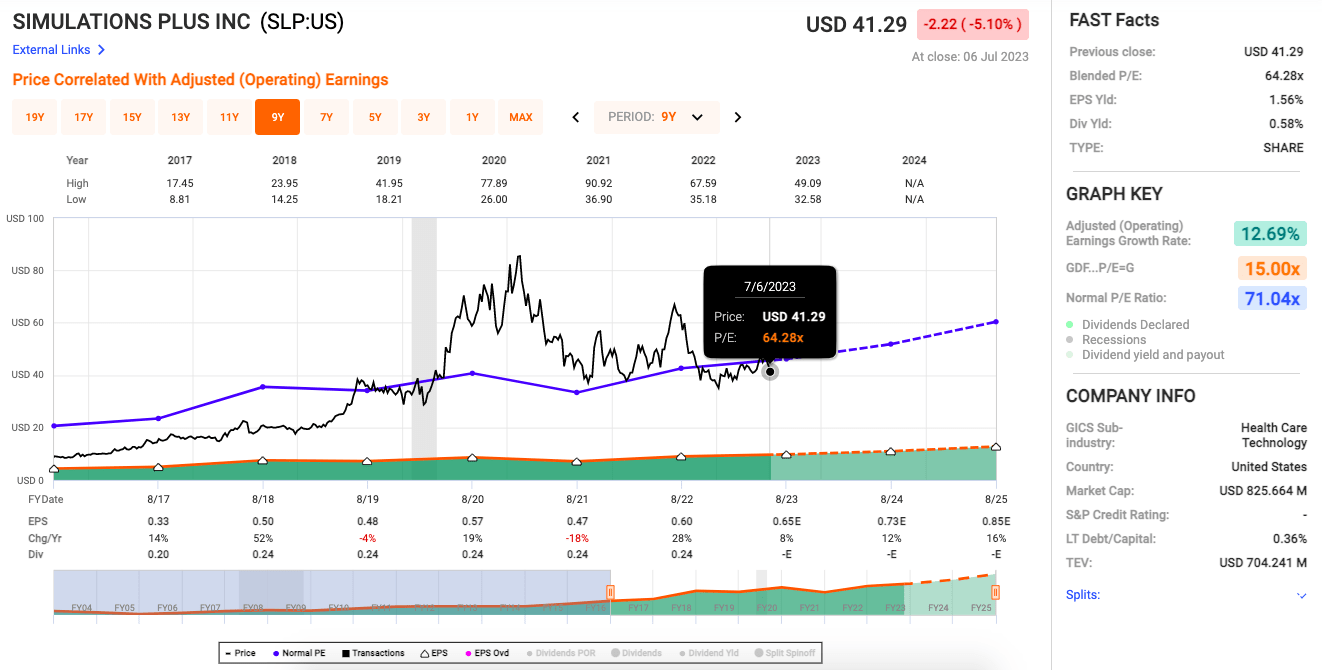

First, let's address SLP's blended P/E ratio of 64.28x (see chart below). It's quite steep compared to the company's growth rate, and it exceeds the Normal P/E Ratio of 71.04x. I am tempted to interpret this as an overvaluation. The stock's price seems to be significantly above what would be expected given its earnings growth, which stands at 12.69%.

{kind=link}

Now, the EPS yield stands at 1.56%. While it's not extraordinarily high, this yield is a reflection of the company's profitability in relation to its stock price. That said, at this level, it's less likely to attract value investors who typically seek higher earnings yields.

When it comes to the dividend yield of 0.58%, I must confess that I'm slightly underwhelmed. Dividend-seeking investors might find this return on investment a bit lackluster. Yet, there is a silver lining for those committed to the long haul, considering that dividends can contribute significantly to total returns over extended periods. In light of these figures, there are concerns, but I wouldn't rush to dismiss SLP as an investment option just yet.

Risks & Headwinds

The first (minor) concern is the erosion of the company's gross margins. Even a very modest dip from 92% to 91% in their software segment and a decline from 66% to 63% in their services segment, are cautionary flags. These downward trends suggest a softening in the pricing power of Simulations Plus and may hint at heightened competition or potential inefficiencies.

Simultaneously, a troubling trend of rising costs is surfacing within the company. Both R&D and SG&A expenses have seen an uptick, eating into the income from operations, which declined by a worrying 17% for the quarter and 37% over the nine-month period. These increases might be justified if they were driving proportional revenue growth, but it appears this is not the case at present. This signals that the firm's operational efficiency is suffering, and it must effectively manage its cost structure to prevent further erosion of its bottom line.

Another disconcerting observation is the shrinking services project backlog, which decreased by about $1 million compared to the prior year. This backlog decline could foretell lower future revenues, and it's particularly concerning given the already diminishing service margins. It raises the question: does Simulations Plus have the demand to sustain its growth and maintain its competitive position? Backlog levels will provide a key indicator of their company's health and potential growth trajectory in coming quarters.

Profitability at the company has come under pressure, as evidenced by declining net income and earnings per share ((EPS)). Net income fell 2% for both quarters combined while nine-month period earnings dropped 18%, and EPS shrunk from $0.20 to $0.46 over that time period - suggesting faltering bottom lines.

Lastly, let's touch upon the inherent risks in Simulations Plus' recent acquisition of Immunetrics mentioned earlier. While it is expected that this acquisition might fuel growth in the long run, it also poses potential challenges. Notably, the integration of Immunetrics into the Simulations Plus structure could carry unforeseen difficulties, and the performance of Immunetrics may not align with expectations. Moreover, the agreement also entails future earnout payments of up to $8 million, contingent on Immunetrics' revenue performance through December 2024. These potential outflows could put additional strain on the financial health of Simulations Plus if Immunetrics fails to meet revenue targets.

Final Takeaway

Based on my analysis, I would rate SLP as a "hold." Despite robust revenue growth and a strong position within the healthcare technology sector, concerns over tightening margins, rising costs, and a declining service project backlog temper my optimism. While the company's recent acquisition of Immunetrics could provide a fresh revenue channel, inherent risks associated with the integration and potential future payments warrant a more cautious stance for now.

For further details see:

Simulations Plus' Flagship Software Drives Q3 Growth