SLP - Simulations Plus: Overhyped With No Growth Left

2023-05-02 12:38:45 ET

Summary

- Simulations Plus, Inc. is a company that develops software for drug discovery and development using artificial intelligence and machine learning technology.

- SLP has seen what was very impressive growth begin to quickly slow.

- Retention data suggests a fundamentally good service but we think the company has already experienced the high growth phase.

- The company has been unable to increase prices annually, let alone upsell customers. ARPC is flat and margins are declining.

- SLP is trading at a 56x multiple, with investors still pricing in growth, solid margins, and SaaS expansion (relative to consulting services), none of which are occurring.

Investment thesis

Our current investment thesis is:

- Organic revenue is declining, with FY23 likely to be the toughest year yet. This may cause markets to reconsider its long-term view.

- Services looking more robust than its Software side is very concerning. This is not a SaaS business as some like to suggest.

- The lack of ARPC improvement suggests SLP is unable to materially upsell customers, or increase their prices annually. This is a fundamental requirement as growth will eventually slow, so the attractiveness long term will come from pricing.

- Margin dilution is value destroying as Management rapidly increases S&A spending, likely to support the top line.

Company description

Simulations Plus, Inc. ( SLP ) is a company that develops software for drug discovery and development using artificial intelligence and machine learning technology. The company has two segments, Software and Services.

Its products include GastroPlus, which simulates the absorption and drug interaction of compounds, and other simulation products based on mechanistic and mathematical models, such as DILIsym, NAFLDsym, IPFsym, RENAsym, and MITOsym. The company also provides products like Absorption, Distribution, Metabolism, Excretion, and Toxicity Predictor, and MedChem Designer.

Additionally, the company offers clinical-pharmacology-based consulting services.

Share price

Simulation Plus' share price has generated monumental returns in the last decade, with over 900% gains. This has been driven by highly attractive gains, as well as the market perception of its commercial profile.

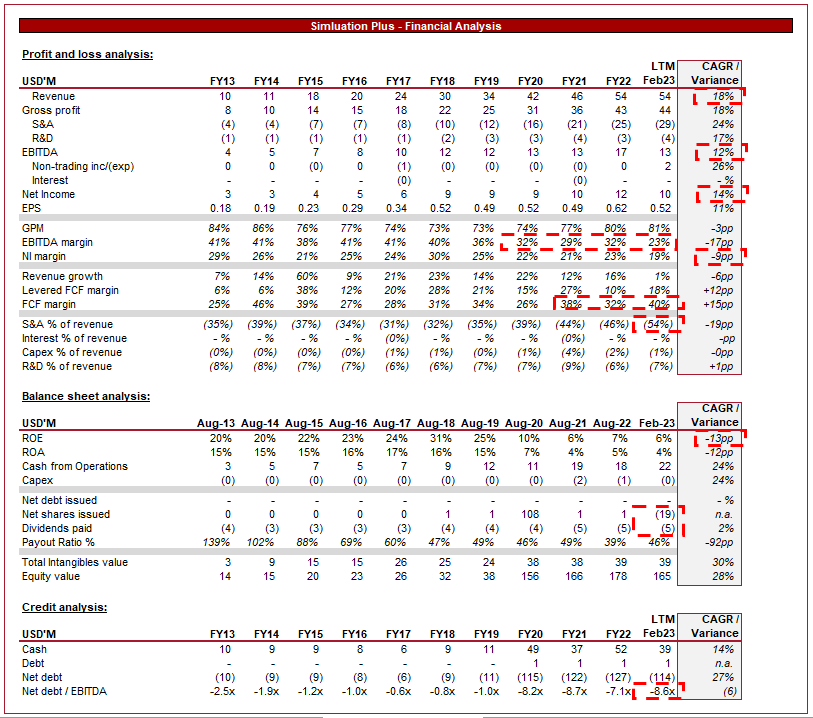

Financial analysis

SLP's financial performance (Tikr Terminal)

{kind=link}

Presented above is SLP's financial performance across the last decade.

Revenue

Revenue has grown at a CAGR of 18%, an impressive level that has been consistently strong for the majority of the decade. This said the company has noticeably slowed in the last 3 years, worrying investors.

Before doing a deep dive into the quality of SLP's revenue, it is worth properly understanding how the company makes money.

The company offers proprietary software and services to support a range of businesses in their product development. The use case here is broad, with pharmaceuticals one of the many industries SLP can and does support. Its software/services can be used in biotechnology, agrochemical, cosmetics, and food companies, as well as by academic and regulatory agencies globally.

SLP's revenue splits into two primary segments, software, such as GastroPlus, and services, such as PKPD. Software currently comprises 60% of revenue (YTD). Both revenue segments are attractive in nature but software is preferable.

Revenue mix (Q2 / YTD data - SLP)

This is because software generates "recurring" revenue, which means users pay an ongoing fee for access. This creates certainty over revenue generation, cash flows, and if the software is good, sticky revenue. These are all things investors love.

When analyzing fast-growing businesses, our process is fairly simple. The key is to understand what "problem" the company is fixing (What is the opportunity?), whether it is truly "fixing" the problem (Does the company offer value above and beyond peers/alternatives?), and what is the impact of "fixing" the problem (The bigger the value creation, the higher the reward and stickier the customer).

The problem

The problems potential clients face is that the development process is time-consuming, complicated, and prone to failure/incorrect development cycles. As a result of this, these companies face significant risk with execution and so invest heavily in mitigation tools. The issue is essentially time and money, two very scarce resources.

The fix

To assess if SLP is succeeding in providing its clients with value, we will consider its key performance metrics. Presented below is SLP's renewal rate in the last 3 quarters which does not materially differ from the annual results. Renewal levels are very high, in line with the top-performing SaaS businesses, although unlike many of the top businesses, it has experienced a noticeable dip.

Renewal rates (SLP)

There is a big difference between being valuable and being invaluable, and this metric in isolation suggests SLP is riding that line. The nuance here is that the pharma businesses are prone to failure if development is unsuccessful or funding runs out, which is a heightened risk in the current economic environment. This is an inherent weakness of SLP, even if it is not a fundamental aspect of the business.

Further, the quality of service can also be judged with upselling. If a company has a valuable suite of products, which SLP claims, it should be successful in upselling its services to existing customers. In the most recent quarter, the company upsold 20 customers across its three software products, significantly higher than the prior quarter. It currently has 250+ customers, which represents a low conversion ratio annually. Further, the company is seeing little movement in its average revenue per customer, which is suggesting the upsells are being offset by onboarding lower-value clients, potentially as a means of maintaining revenue. Also, this suggests the company is unable to implement increased pricing, a key requirement of a SaaS business long term.

ARPC (SLP)

The reward

The value proposition for potential clients is clear. Many pharma businesses spend substantially on R&D. GSK , for example, spent 18% of revenue in FY22. Providing a service that can reduce this cost, or save time (which in effect reduces cost and brings forward revenue) has the potential to materially improve returns.

The question then becomes, why has the business not grown faster? Where is the value transfer to SLP? We think the problem is that the TAM is not what it seems. The size of the pharma/bio industries has given the impression to markets that there is room to accommodate high growth long term. In its Q3-22 filing, Management estimated its TAM to be $2BN (The last time a TAM was disclosed/estimated), yet with $54m of revenue, the company is already seeing growth slow. This slowdown would be logical if SLP had a bad product but we know this is not the case, retention is too high. The only reason we can see is that the market is not large enough. Further, although the product is proprietary, SLP faces competition from Certara ( CERT ) and Icon PLC. Our view is that the large pharma players are likely using a SLP's, and or its competitors' products, leaving the available market to be new and growing pharma businesses. Given the ARPC, this is not a cheap offering that limits the number of businesses which SLP can target. We will explore other factors which support this assertion as we progress through this report.

To summarize our view on the commercials:

- The market needs a product like this, with SLP's retention data and historical growth suggesting its software/service is good.

- Although retention is good, the dip during the most recent quarter suggests a weakness in fundamental demand.

- We cannot see evidence of a large TAM based on growth.

- Upselling and price hikes are small, with no real movement in AVPC in 3 years.

- The company is facing competition, impacting its pricing strategy.

We will now consider the financial side of revenue. Management has supplemented revenue growth with consistent micro-acquisitions. This has supported revenue growth but suggests the organic, underlying growth is inferior to the current 18% CAGR.

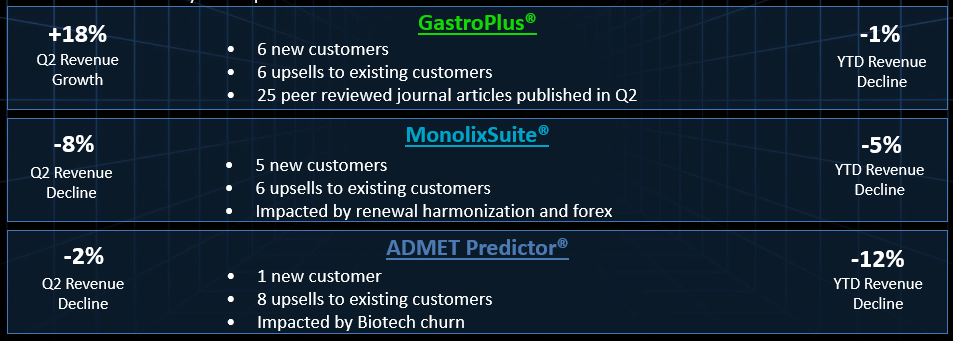

Further, the company experienced a quarterly (Q2) revenue decline across 3 of its 6 key segments, and 4 on a YTD basis. This further supports the view stated above that the product is attractive. This could lead to a difficult year for the business, especially if SLP does not have a clear M&A target.

Software Q2 (SLP)

{kind=link}

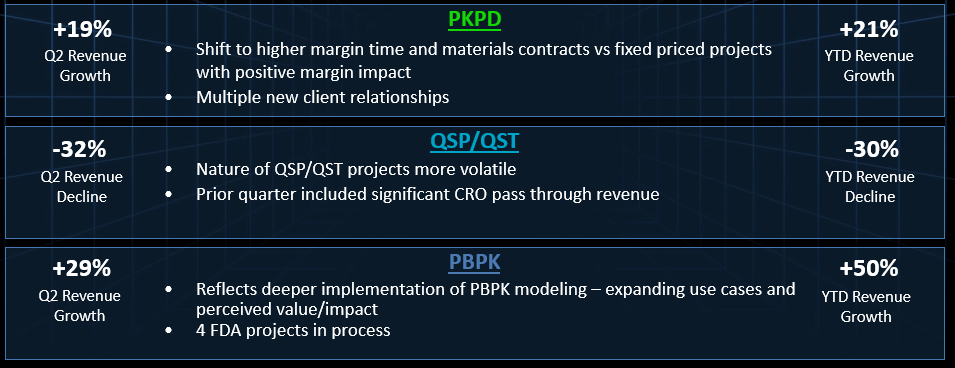

Further, growth is higher in the company's Services segment, which is resulting in a shift away from Software, at least in the near term. As stated prior, a quality business will move toward Software, not against it.

Services Q2 (SLP)

{kind=link}

Economic considerations

The top SaaS businesses are fairly insulated against economic conditions. That is not to say growth continues at a rapid rate, but that customers (for the most part) remain sticky. Many of the tech businesses that sink during uncertain times are those whose customer base relative to growth is skewed to the latter. It is a growth slowdown rather than a revenue decline.

SLP looks overly exposed to economic conditions in our view. Software revenue declined 3% on a YTD basis, and margins are slipping. We expect interest rates to remain elevated for the majority of the year, keeping conditions difficult. There will always be a heightened risk of churn given the potential clientele, especially when the cost of borrowing is high and markets are declining.

Margin

GPM has improved in recent years, driven in large part by the improvement in SLP's Services segment. This is offsetting its own benefits at a total level, however, due to the segment outgrowing Software in the YTD.

The real concern is the company's slippage at an EBITDA level. This is due to a rapid increase in S&A expenses, which has outgrown Revenue. The company is relying less on M&A and the quality of its product as a revenue driver, and leaning more toward customer acquisition expenditure. Once again, this is not a characteristic of SaaS. EBITDA should remain high and trending up, as the marginal cost of a new customer is very small relative to the revenue they bring in.

We believe margins will slip further in FY23. With YTD numbers down, Management will commit further resources to acquire new customers. We believe the significant increase in new customers in Q2 is evidence of this growth tactic, as the OPM in Q2 was 26% vs. 30% the year prior.

Balance sheet

Management's R&D investment is fairly low compared to businesses of its nature. The company currently incurs capitalized expenditure equalling 1% of revenue, with P&L R&D amounting to 7% of revenue. On an absolute basis, this is $4m. To us, this suggests a lack of runway long term, meaning an investment in product development is not required.

Further supporting this is distributions. The company is already a consistent dividend payer and has even begun buying back shares. We cannot see how this would occur (in conjunction with the lack of R&D spending) if Management intended to grow and develop the business long-term.

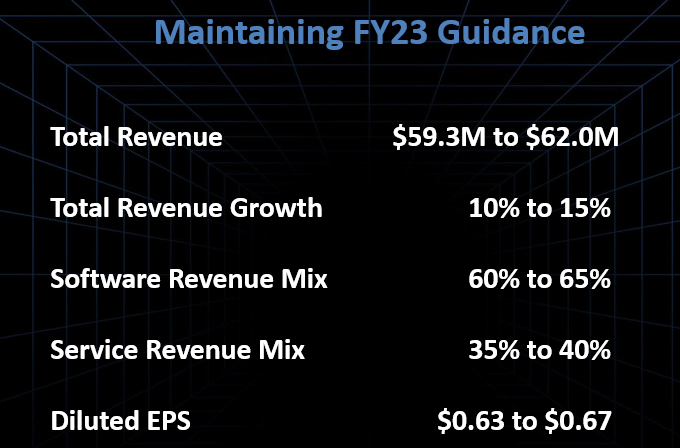

Outlook

Management guidance (SLP)

{kind=link}

Presented above is Management's forecast for the coming year.

Revenue growth is expected to be 10-15%, which would require a noticeable uptick in growth given the LTM is currently $54m. Based on the increase in S&A spending, this remains achievable but looks now like it will come at the cost of margins.

Valuation

{kind=link}

Presented above is SLP's current valuation. The business is trading at a monumentally high valuation, which can only suggest markets are pricing in continued double-digit growth and higher margins than currently achieved.

Given our analysis, it is clear that we cannot see this business warranting such a premium valuation. The route to this valuation is clear for us but we do not see it as achievable.

- A NIM of >25% - Implying SLP's offering is more attractive and less S&A expenditure is required.

- an organic growth rate of >20% - Suggesting sufficient runway to realize such a large premium.

- Evidence the company can successfully upsell/increase customer prices - Implying long-term company value once growth begins to slow.

SLP currently looks far away from all 3 criteria, and we expect it to move further away.

Final thoughts

On paper, SLP looks extremely attractive with all the correct buzzwords. High growth, great margins, SaaS model, pharma, etc. The issue is that under every rock, we find issues. Organic growth is rapidly slowing, margins are declining as management is spending heavily on S&A, and the SaaS side has declined as a % of revenue.

Despite the clearly bearish report, I should be clear, this is a fantastic business. Trust me, I own it. How many businesses can consistently achieve a NIM of >20%, operate in a highly complicated, niche industry, and essentially spend nothing on development costs. The issue is that you have to pay a 56x multiple of EBITDA for the privilege.

For further details see:

Simulations Plus: Overhyped With No Growth Left