SINGY - Singapore Airlines Books Record Profit

2023-05-19 04:29:02 ET

Summary

- Singapore Airlines ended a strong year with doubling capacity and record profits.

- Long haul network recovery as well as recovery in the China network should be drivers going forward.

- I believe the stock has an upside despite a very tough year to beat.

In a previous report , I marked Singapore Airlines Limited ( OTCPK:SINGY , OTCPK:SINGF ) a buy and the stock indeed did gain 5.6% since issuing that buy rating, but a fully honest view deserve to share that the markets gained 8%. So, while the stock appreciated in value, just putting the money in a market tracker would have been more rewarding. In this report, I will be discussing the most recent results and explain whether I think shares remain a buy or whether the buy rating issued in March was not justified.

Singapore Airlines Results Surge

{kind=link}

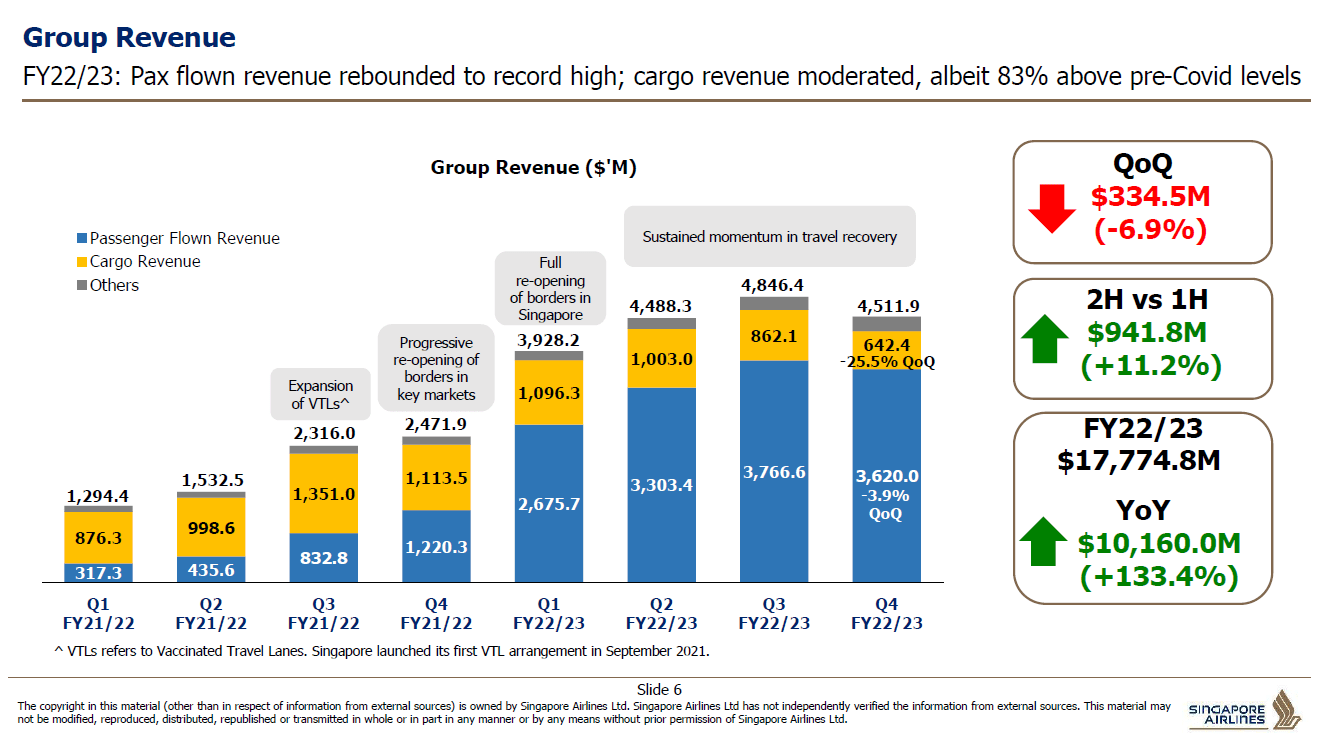

The results really show the strong recovery in air travel demand. Despite fuel prices rising 138% and non-fuel costs rising by 61.5%, the strong unit revenues and capacity growth led to a 133% increase in revenues, enabling the Singapore carrier to swing from a 926 million Singapore dollar loss to a $2.16 billion Singapore dollar profit.

{kind=link}

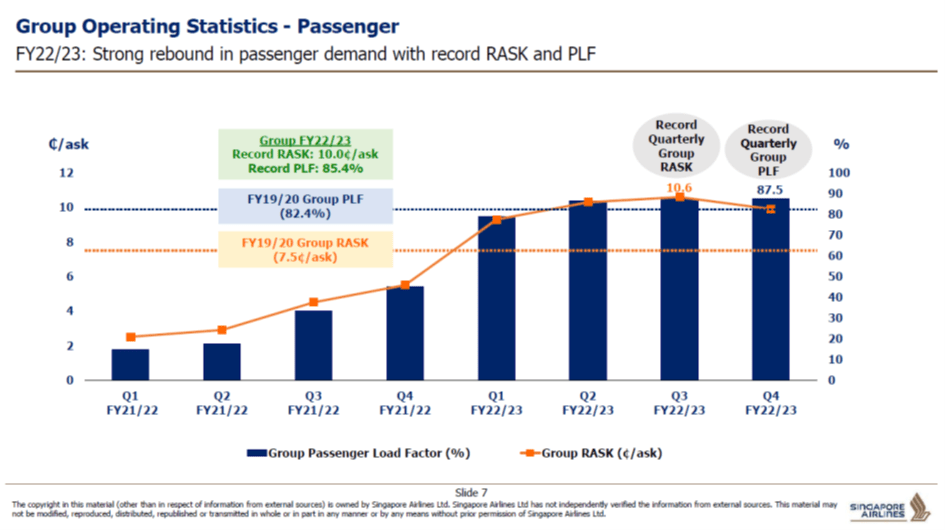

Revenues per available seat kilometer or RASK remained well above the pre-pandemic times and in some way with elevated costs that is also something one would expect. However, we also do see that quarter-over-quarter, the RASK dropped, and while that is not an existential issue at all for Singapore Airlines, I do think investors should keep in mind that the sequential increases in RASK are likely over and we will see seasonality effects being more profound going forward. Passenger load factors reach an all-time high during the quarter but also during the fourth quarter. So, with 94% in capacity growth, we see continued load factor and unit pricing strength. Important to note is that while capacity grew 94%, that only brings the company to a 79% capacity recovery, meaning there is still growth potential ahead.

The weak part of the business without doubt is the cargo business. Macroeconomic uncertainty and increases in cargo capacity a driving down the yield and pressure the load factor. Load factors continue to be below the pre-pandemic load factors, but yield is still strong although we also see significant softening there. While the yields remain elevated, I do suspect that sooner rather than later we are going to see the business hit a more normalized and challenged operations profile.

{kind=link}

Overall, revenues grew 133.4% by the drivers detailed earlier. Cargo revenues declines by 25% sequentially, and with more capacity being recovered throughout the year I do expect we will see more decline in the quarters ahead. Revenues for passenger services dropped 4% quarter-over-quarter, which I believe shows that the strong growth is over in the sense that the capacity recovery is not such in shape and form that it will counter seasonality effects.

How Is Singapore Airlines doing financially?

Despite cargo revenues dropping, Singapore Airlines had its strongest ever year driven by continued capacity expansion and strong unit pricing coupled with record load factors and strong unit revenues. On cost levels, fuel prices were high but eased in the second half of the year while non-fuel costs dropped in the second half of the year as well. And the full year figure showed 64% higher non-fuel costs, but that was lower than the growth in capacity, meaning that there was strong performance on unit cost. For the next year, Singapore Airlines expects to be 83% recovered in the first half of the year compared to the current 79% recovery, and growth can be derived from more international routes as well as strong increases in the China focused networks.

Is Singapore Airlines Still A Buy?

{kind=link}

When processing the numbers for Singapore Airlines, I observed that the 2024 through 2025 expected EBITDA are lower than what Singapore Airlines achieved this year. While I have no doubt that there are revenue pressures mostly from cargo operations, I am not quite sure whether we should be expecting declines in the EBITDA in the years ahead. If that is the case, then the stock has around 8% downside, while based on its most recent performance it is undervalued by 10%. With the recovery of the network in China in mind as well as international growth, I am inclined to maintain my buy rating.

Conclusion: Singapore Airlines Is A High-Risk Buy

With airlines you rarely have low-risk buying opportunities and Singapore Airlines is no exception at this time. There are pressures on cargo results, and passenger results might come under pressure, but overall the business is managed well and unit costs as well as fuel costs came down which helped the airline with booking the strongest profit in history. The cost easing was something I expected and going forward we see continued challenges for the cargo business but also significant opportunities for Singapore Airlines to continue growing. So while analysts expect lower profits, I am not sure whether we will actually be seeing profit declines. If that is the case, then the buy times for Singapore Airlines are over. If not, the stock continues to offer upside, but it will probably be more measured with the capacity additions.

For further details see:

Singapore Airlines Books Record Profit