SINGY - Singapore Airlines Stock: From Hold To Buy (Rating Upgrade)

2023-03-10 15:54:27 ET

Summary

- Singapore Airlines Limited's results have continued to improve.

- There are significant pressures on cargo results, and capacity expansions from competitors could erode yields.

- While risks remain, I am upgrading Singapore Airlines stock from Hold to Buy, better reflecting the opportunity.

In a previous report , I marked Singapore Airlines Limited ( SINGY , [[SINGF]]) a hold with a speculative buy opportunity. At the time of writing, the stock has outperformed the market with a 3.8% return compared to a 0.2% return for the stock market. In this report, I analyze the most recent quarterly earnings and explain why I am upgrading Singapore Airlines shares from Hold to Buy.

Singapore Airlines: Still A Higher Risk Recovery Airline?

{kind=link}

When I analyzed Singapore Airlines stock in December 2022, I actually liked the stock. However, with the reopening in China my main concerns were that the company could be facing some negative impacts from that, as it could provide several infection waves. My major concern with Singapore Airlines at the time was that capacity expansion at Cathay Pacific ([[CPCAF]], [[CPCAY]]) could provide pressure on airfares, and while that is still a risk today, I do believe that the most recent quarterly results showed overall strength while lower fuel prices are also aiding in managing costs and profitability.

Singapore Airlines Results Surge

{kind=link}

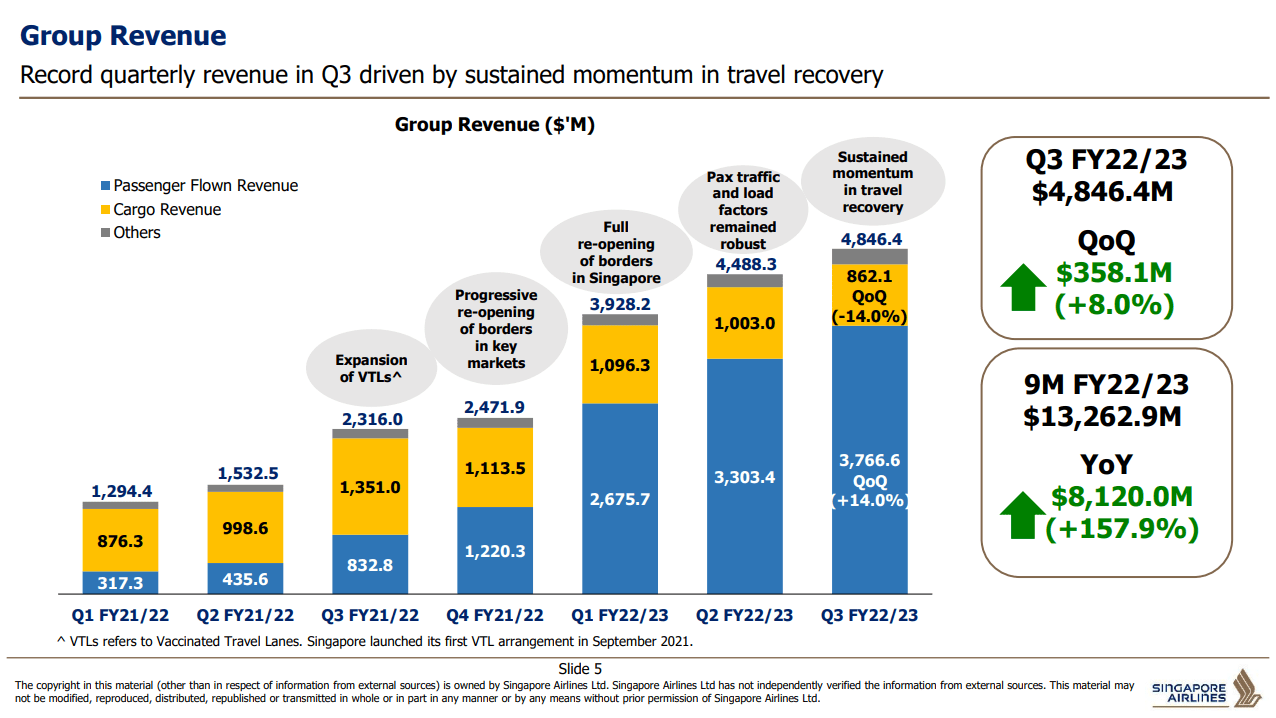

During the quarter, Singapore Airlines saw its Group Financial results improve. Moreover, while the revenue growth of 8% showed a slowdown in the increase in revenues the operating profit growth outpaced revenue growth yet again. Overall, we do see some slowdown in the rate of growth on revenues as well as profitability but the profits are still growing faster than topline growth.

{kind=link}

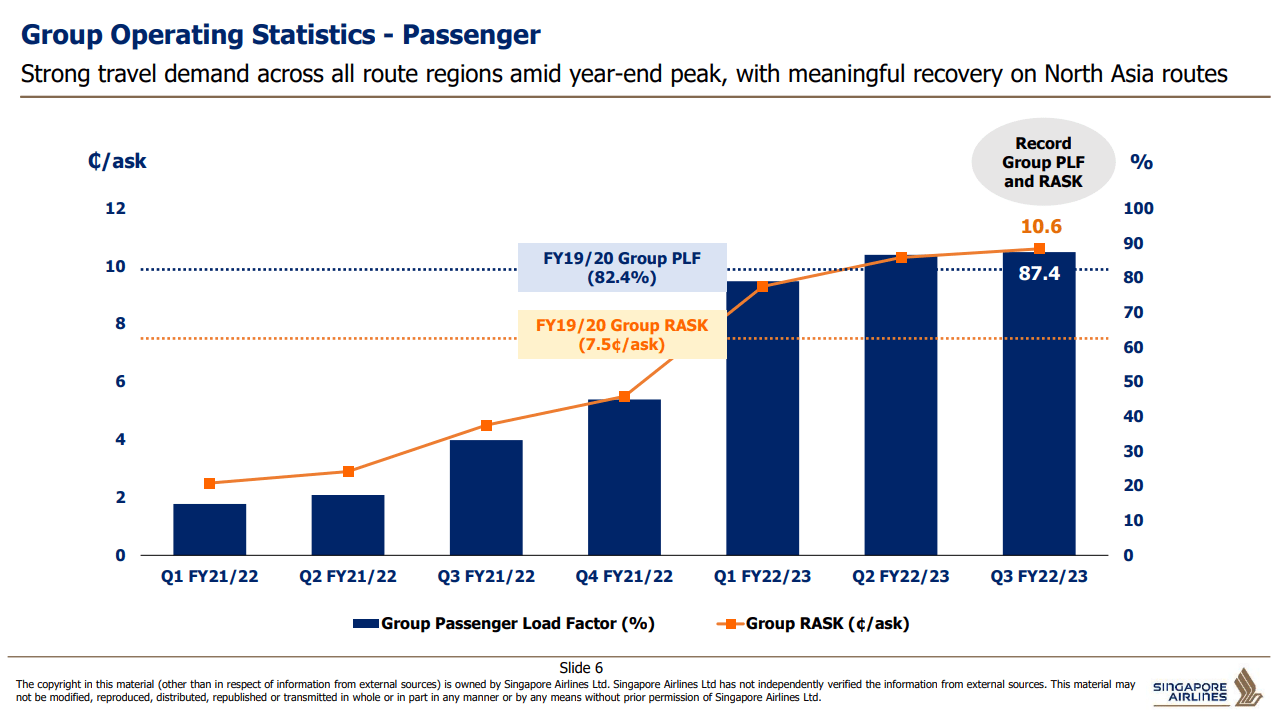

While I had some concerns about yield pressure and those could show up more dominantly in 2023 as other carriers expand capacity, we do see that while the growth in yield is tapering it is still up quarter-over-quarter and the load factors are strong. Both metrics improved quarter-over-quarter and are up from pre-pandemic levels. Yields and load factors for the cargo business are dropping, which is not unsurprising and driven by two main factors. The first is that as international flights are gaining traction, more belly cargo capacity is coming available and that pressures yields but also brings down the load factors as belly capacity is there but it is not always the best solution for air freight transportation. Besides that, due to inflation some companies are burning down their inventory due to decreased consumer spending and that leads to lower demand for air freight.

{kind=link}

So the strong yield of 10.6 cents per available seat-kilometer, 11.1% higher capacity compared to the previous quarter and a 87.4% load factor helped Singapore Airlines realizing 8% in revenue growth. You might say that capacity expansion outpaced topline growth. However, the passenger revenue was up 14%. So on 11.1% higher capacity, revenues were up 14% which is strong. The weakness primarily shows in the cargo operations where demand and yields are falling.

How Is Singapore Airlines doing financially?

So, how is Singapore Airlines doing financially? They are actually doing well. Results continue to improve and the company expects a strong fourth quarter with capacity expected to be 77% recovered compared to pre-pandemic levels. The company sees robust demand in East Asia with the reality that cargo revenues will continue to be under pressure. The big question of course is whether declines in cargo revenues are going to outpace the increases in capacity and revenue recovery for the passenger business. That could indeed happen and there is the risk of competitors bringing capacity to the market and pressuring Singapore Airlines, but that is in part also because Singapore Airlines has been phasing through the recovery quite well and that is not something that should be held against them. They might be more prone to seeing bigger pressures from competitors but they also have been showing that they are executing their business quite well. Further softening in fuel prices could also help the airline cutting costs while further capacity expansion will help with bringing unit costs down as well.

Conclusion: Singapore Airlines Is A High-Risk Buy

With airlines you rarely have low-risk buying opportunities and Singapore Airlines is no exception at this time. There are pressures on cargo results and passenger results might come under pressure, but overall the business is managed well and unit costs as well as fuel costs should be coming down which could help airline maintaining momentum.

Overall, besides a stronger third quarter, I do believe the risks are still there for Singapore Airlines Limited, but a Buy rating marking a high-risk buy opportunity is better fitting than a Hold rating. What does hold is that investment in the airline industry especially under the current circumstances is not for the faint-hearted, but if it pays off it can be very fruitful, as I have seen with various airlines that I have a buy rating on.

For further details see:

Singapore Airlines Stock: From Hold To Buy (Rating Upgrade)