SIOX - Sio Gene Therapies: Biopharma Liquidation With A Favorable Risk-Reward

2023-04-20 08:17:26 ET

Summary

- This is a failed biopharma liquidation play with a favorable risk-reward.

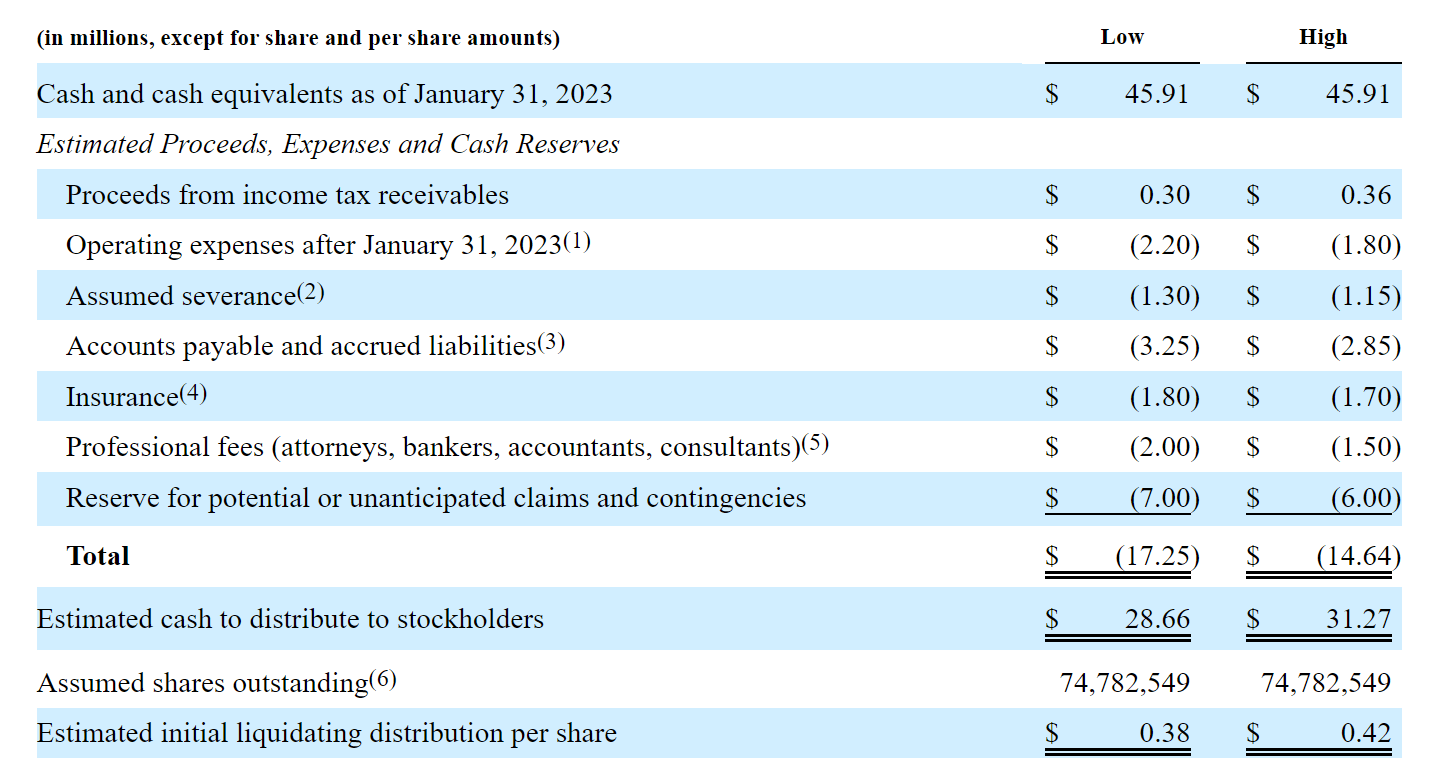

- Sio Gene Therapies is undergoing liquidation, with its shareholders likely to receive $0.38-$0.42/share vs. the current price of $0.40/share.

- An additional upside of up to $0.09/share might potentially come from a CVR and a partial release of the contingency reserve.

- Investors stand to gain up to 28% while I believe that the downside is limited to 5%.

This is an interesting busted biopharma liquidation. The situation is timely as the company is about to get delisted on April 24. Sio Gene Therapies ( SIOX ) is a failed microcap biopharma. SIOX initially attracted my attention last year after the company had announced a wind-down of its remaining two trials, a massive headcount reduction, and commenced a strategic review. Given that SIOX was trading at a wide 50%+ discount to its net cash, I subsequently highlighted SIOX to Special Situation Investing subscribers as a potential liquidation candidate in October.

What has happened since? Well, the situation has played out rather well. In Dec’22, SIOX’s management concluded the strategic review, proposing a liquidation of the company. This month, SIOX shareholders approved the liquidation. The stock has reacted positively to these developments, jumping 33% since my initial write-up.

Having said that, there seems to be further upside remaining here. SIOX’s management expects the initial shareholder distribution to fall between $0.38-$0.42/share vs the current share price of $0.40/share. I believe that at current prices the situation has been derisked as investors are likely to receive full or almost full initial investment back shortly with the initial distribution. Importantly, investors are also receiving an optionality to capture up to $0.09/share in additional distributions. This implies a total potential upside of up to 18%-28% if the additional distributions are paid out in full. Note that in case of no additional distributions, the downside would stand at 5% if the initial distribution is equal to the lower end of the projected range ($0.38/share). I believe that the risk-reward here would remain favorable with the SIOX share price at or below $0.42/share. At this price, the potential upside would stand at 21% whereby the downside would be limited to 10% if the initial distribution is equal to $0.38/share.

The initial distribution seems likely to fall within the management’s guided range. SIOX has already laid off most of its staff and office leases have already been terminated, so what remains should be a pretty clean liquidation process.

Additional distributions might come from:

- $0.036/share from the CVR related to the sale of Arvelle Therapeutics . As part of SIOX’s sale of its preferred stock investment in Arvelle Therapeutics in 2021, the company can receive up to $7m in potential future regulatory and sales milestone payments. SIOX has apparently already received $4.3m in cash proceeds from the CVR (see here , p. 23). This leaves $2.7m or $0.036/share in potential incremental proceeds. Management’s disclosures on the expected timeline and/or proceeds amount have been limited, however, it is not inconceivable that the potential payouts might take several years to materialize.

- $0.04-$0.053/share from a partial release of the contingency reserve . The current reserve for potential and unanticipated claims/contingencies of $6m-$7m seems excessive. Contingency reserve has been materially lower in other ongoing biopharma liquidations, including MTCR ($1m-$3.5m, page 24 ) and OTIC ($2.3m, page 32 ). Worth noting that OTIC’s management sees a chance to distribute to shareholders up to $1.5m out of the $2.3m. In this context, I assume that $3m-$4m or $0.04-$0.053/share might eventually be returned to SIOX’s shareholders.

Management’s initial liquidating distribution estimates:

Sio Gene Therapies Proxy Filing

{kind=link}

The presence of several large shareholders suggests equity holder value might be preserved here. SIOX’s shareholder base includes Roivant Sciences (owns 25%) and Rubric Capital Management (10%). Roivant is a $5bn market cap publicly-listed biotechnology company with a portfolio of subsidiary biopharma companies. Rubric Capital Management is a hedge fund with over $2bn in AUM. As for the management team, most of the directors have already left the company. The only remaining director is David Nassif who has undertaken CEO, CFO and CAO (Chief Accounting Officer) roles. Nassif owns less than 1% of SIOX’s shares, however, it is worth noting that he is set to receive $1.1m in so-called “golden parachute” compensation once the liquidation is completed. It is worth noting that the CEO will also assume a consulting role at the company for which he will receive upfront retainer fees of $75k for his work in May and April. The CEO is also entitled to receive further consulting fees for any additional consulting services provided. This might potentially reduce the additional distributions that will be paid out to SIOX's equity holders. Having said that, given that the management has chosen the most shareholder-friendly path of liquidation (vs a reverse merger), I am inclined to believe that a material portion of the contingency reserve might eventually see the pockets of SIOX’s shareholders.

While the initial distribution is likely to range from $0.38 to $0.42/share, the remaining cash is expected to be returned in the next several years. Note that to preserve cash, the company will be delisted and become non-tradable going forward. Delisting is expected at the market open on April 24.

Risks

- SIOX is a microcap company and has limited liquidity. The average daily volume stood at c. $200k per day over the last year. Limited liquidity implies that investors might be unable to sell the stock at market prices. However, this risk might be mitigated by using limit orders.

- The initial distribution might potentially fall below the lower end of the management's guided range ($0.38/share). This might be driven by expenses turning out above the management's conservative estimates, including potential excess consulting fees paid to the CEO Nassif. SIOX has noted that it is "impossible to predict with certainty the actual net cash amount that will ultimately be available for distribution to stockholders or the timing of any such distributions".

Conclusion

At current prices, SIOX is an interesting investment setup in the event-driven space. In a best-case scenario, SIOX shareholders might receive a distribution that will either fully or substantially cover their initial position and also receive an optionality of additional distributions down the line. While SIOX will get delisted and become non-tradable going forward, I think investors are getting compensated for this fairly well.

For further details see:

Sio Gene Therapies: Biopharma Liquidation With A Favorable Risk-Reward