SPNT - SiriusPoint Preferred 'B' May Be The Best Preferred Stock In The Market

2023-05-02 12:00:00 ET

Summary

- As Warren Buffet says, buy when others are fearful. I will make the case that the level of fear is unwarranted and that this preferred stock is a great value.

- The fear is that Dan Loeb “might” buy SiriusPoint. I will discuss what happens if he does and what happens if he doesn’t and debunk these fears.

- SPNT Preferred “B” is a preferred from an investment-grade company that currently yields 9.07%, and this yield is “qualified,” providing a very strong after-tax yield.

- Better yet, SPNT.PB has a strong likelihood of being called and has a yield-to-call of 13.36%.

- Lastly, if not called, the dividend will reset to the 5-year treasury note yield plus 7.3%. At today’s price and 5-year note yield, SPNT.PB’s yield will move up to 12.4%.

SiriusPoint

SiriusPoint (SPNT) is an insurance company that came about as a result of a merger of insurance company Sirius with famed hedge fund manager Dan Loeb's Third Point Reinsurance company. Here is what Yahoo Finance says about the company.

SiriusPoint Ltd. provides multi-line insurance and reinsurance products and services worldwide. The company operates through two segments, Reinsurance, and Insurance & Services. The Reinsurance segment provides coverage to various product lines, which includes aviation and space, casualty, contingency, credit and bond, marine and energy, mortgage, and property to insurance and reinsurance companies, government entities, and other risk bearing vehicles. The Insurance & Services segment offers coverage to various product lines comprising accident and health, environmental, workers' compensation, and other lines of business, including a cross section of property and casualty lines. The company was formerly known as Third Point Reinsurance Ltd. and changed its name to SiriusPoint Ltd. in February 2021.

Additionally, even before Dan Loeb's suggestion that he might buy SPNT, SPNT common stock was on a rocket, doubling from August of last year before spiking even higher on Loeb's announced.

And lastly, SPNT has de-risked, first by switching from having an investment portfolio made up of a lot of common stock to one with high quality bonds and debt instruments. They also paid Enstar Group to take their riskier insurance policies off of their hands and exited riskier sectors of the insurance market.

SiriusPoint Preferred "B" Stock

Current Price - $22.40

Current Stripped Price - $21.97

Current Yield - 9.07%

Qualified Dividend - Yes

Call Date - 2/26/2026

Yield-To-Call - 13.36%

Reset Rate - 5 Year Treasury Note yield plus 7.3%

Cumulative - Yes

If SPNT.PB is not called, given today's 5 year note yield, the yield will adjust higher to a "qualified" 12.40%. And if SPNT.PB is called, you will earn an annualized yield of 13.36%. So either of 2 possible scenarios look pretty darn great for a preferred stock from an investment grade company. And if SPNT-B is called, the dividend part of your return will be taxed at the qualified rate, and the capital gains will also be taxed at the 15% and the taxes on that gain will be deferred until April 15, 2027. So this is clearly an extremely attractive security.

And one other goody. Unlike many other 5 year reset-rate preferred stocks, if SPNT doesn't get called when its call date comes, it cannot call it again for 5 years. So no matter how much lower interest rates may go after the call date, your current 12.52% yielding preferred stock cannot be called away from you until 2031.

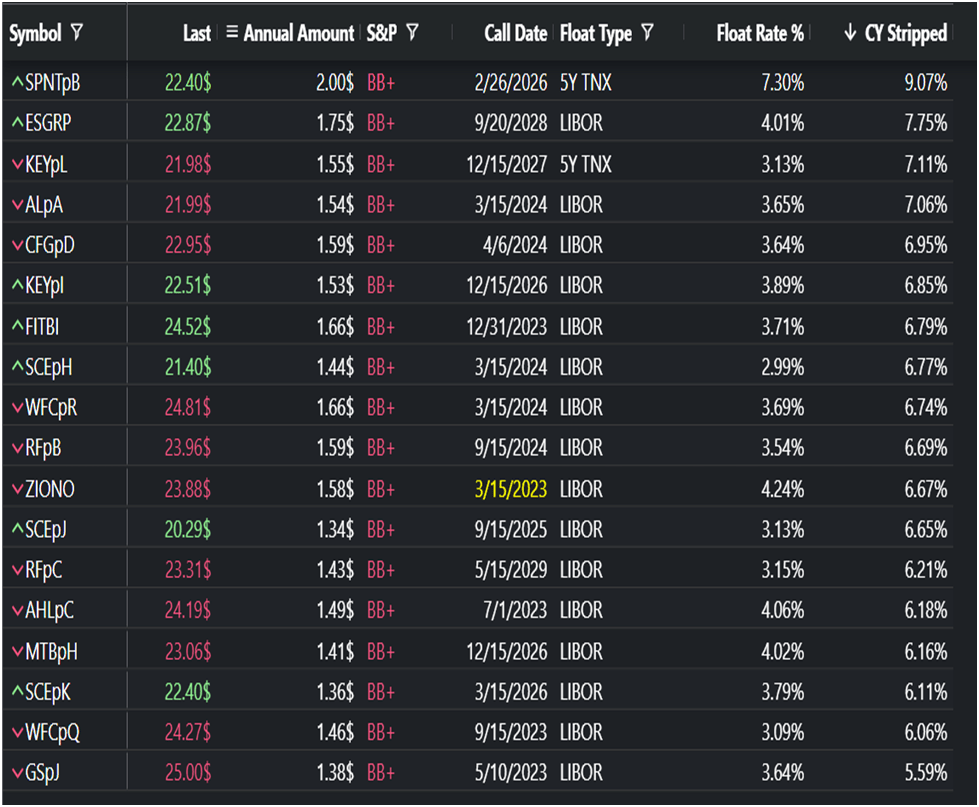

SPNT.PB is by far the best preferred stock in the market with a BB+ rating as you can see from the chart below. This chart compares all BB+ rated preferred stocks that pay qualified dividends that are either LIBOR fixed-to-floaters or 5 year reset-rate preferred stocks.

{kind=link}

As you can see from the right hand column, the current yield of SPNT-B is very large relative to its peers . While most BB+ preferred stocks trade in the 6% range, SPNT-B trades with a yield of over 9%. But even more stark is when you look at the second from the right hand column . The fixed portion of SPNT-B's reset-rate is around double the average BB+ preferred stock . And the other 5 year reset-rate preferred, KEY-L, has a much smaller reset rate (3.13 + 5 year T-note rate versus SPNT.PB's 7.3% + 5 year T-note) and they both sell around the same price. And KEY is in the troubled banking sector and could see a credit downgrade. And while SPNT has more than doubled in price from its low, KEY is down 50% since banking fears arose.

Myths That Make SPNT-B Dirt Cheap

Myth 1: The company will be delisted if Loeb buys SPNT.

First of all, we have had other good quality publicly traded insurance companies bought out before. Two examples that come to mind are PRE and AHL, both with preferred stocks. Neither de-listed its preferred stocks and PRE has issued PRE.PJ as a public preferred even after going private. Both PRE and AHL remain investment grade companies with PRE-J maintaining a very strong BBB rating for a preferred stock. And as you can see in the above chart, SPNT.PB is a far better preferred stock than BB+ peer AHL.PC which is from a private insurance company. And SPNT.PB would be in same situation as AHL.PC if Loeb buys SPNT.PB but would be a much better value.

Generally, insurance companies want to maintain the ability to be able to issue preferred stock in the future. The fact that they are now private doesn't change that. And dividends from AHL and PRE are non-cumulative so it would be easy for them to halt dividends as they would not accrue. But then they would lose trust among investors and never again be able to issue preferred stock again. SPNT-B is unusual in that its preferred stock dividends are cumulative. That is rare among insurance companies and a nice feature. So they can't just stop paying dividends at zero cost to them. So they are even less likely to stop making dividend payments.

Second of all, there is wording in the SPNT-B prospectus which requires that SPNT-B remain listed. Here is the wording.

We are required to use reasonable best efforts to cause the Series B Preference Shares to be listed on the NYSE and to maintain such listing for so long as any Series B Preference Shares remain outstanding and the Series B Preference Shares remain eligible for continued listing on the NYSE, at our sole expense.

So how can they de-list and pretend that they are making their best effort to keep SPNT.PB listed when SPNT.PB has already received approval for NYSE listing.

Third of all, even if some crazy and very unlikely shenanigans occurs and somehow they do delist, the reset rate is so high on SPNT.PB (13.36%)that a call is still likely given the huge dividend that SPNT would have to pay after its call date, and especially given that they would not have another opportunity to call SPNT-B until 2031.

Myth 2: When a company goes private it will stop paying its dividends.

In the comments on my previous SPNT.PB article , not only were a few investors afraid of a de-listing but they also feared that SPNT.PB would stop paying dividends if it goes private. This fear has absolutely no basis . We have had a number of companies go private and in every case they continued to pay dividends. Besides AHL and PRE mentioned earlier, we have seen SEAL, GMLP, HMLP, LTS, AFSI, GLOG, etc . . . and all continue to pay their preferred dividends as private companies. Despite LTS, for example, being taken private by a company with a very poor credit rating, they continue to pay their preferred dividends and did so even during COVID. And the one insurance company that did delist its preferred stocks, AFSI, now has a long history of continuing to pay preferred dividends. And this was an insurance company where nobody trusted management and where Barrons had written them up for questionable accounting practices.

I think that what investors are also missing here is that companies that buy out other companies want to extract their cash flow through having the company they bought pay them dividends. In order for the company to pay their owners dividends, they must continue to pay their preferred dividends . A company, whether private or public, cannot pay common stock dividends without first paying their preferred stock dividends.

Additionally, insurance companies depend a lot on having good credit ratings in order to give confidence to customers that they will be able to make good on their insurance policies. Their A.M Best ratings are very important as well as their credit ratings. What will the ratings agencies think if SPNT is not even paying their preferred stock dividends. Insurance is a regulated business so SPNT cannot simply be stripped of its value like might happen with some other companies.

Here is what Dan Loeb said about buying SPNT in his filing. He said that SPNT may be:

" best positioned to execute on its turnaround strategy as a privately held company while continuing to strengthen its financial position, enhance its credit ratings, and adhere to the highest regulatory standards ."

So unless Loeb is flat out lying, he intends to strengthen the company's financials and improve its credit rating. You don't do that by stiffing your preferred shareholders and have a large unpaid liability that continues to accrue each quarter since their preferred dividends are cumulative. And the fact that Loeb has interest in SPNT can be looked at as a positive as this shows that he is confident in the strength of this company and in its future.

The bottom line is that this myth, that when companies are taken private that they stop paying preferred dividends, is totally false . I know of zero companies suspending preferred stock dividends after they went private . However, I know of many public companies that have suspended their dividends. In my decades of investing experience, no company, public or private, stops paying their preferred dividends simply because they legally can. Preferred dividends are only suspended by companies that are in trouble. ALIN (aka TOO) was taken private and did eventually suspend preferred stock dividends, but as I understand it, that company was having serious problems.

So the fears that people have that have caused the selloff in SPNT.PB look more like imaginations running wild and have no basis in reality. When this happens, we generally have a great investment opportunity.

And let's not forget that Loeb might buy the company, but he also very well might not. The common stock has traded down from its highs which I suppose means there is more uncertainty about the buyout. If he doesn't buy the company, SPNT.PB could very well move up from its current price of $22.40 back to near $25 where it trade in early February. And with the company going ex-dividend 50 cents very soon, you can add that to the potential gain. And if he buys the company, it will take some time for fearful investors to see that SPNT.PB is not being delisted and that preferred dividends continue, but ultimately it will move to fair value like the preferreds of PRE and AHL. In the meantime, you can enjoy the fat qualified dividends.

When I see so much fear, mostly irrational, including from the article comments from my last article as well as in the price movement, I think that the weak hands have already sold and the direction of least resistance is higher.

Summary/Conclusion

SPNT.PB is far and away the best BB+ rated preferred stock in the market, and maybe the best value among all preferred stocks. And the common stock has been rocketing higher for weeks. The current yield is over 9% and qualified, and SPNT.PB has a high likelihood of being called in February of 2026 for a huge 13.36% yield-to-call. And if it is not called, its yield would reset to 12.4% using the current yield on the 5 year treasury note. And you would lock in that yield until at least 2031.

On the news that Dan Loeb might buy SPNT, SPNT.PB has fallen from near $25 to a stripped price below $22.00 (due SPNT.PB going ex-dividend 50 cents very soon). A strong case can be made that even at $25.00, SPNT-B is very undervalued. It once traded as high as $29.75 in 2021.

In the article, I debunked the 2 myths that have caused SPNT.PB to sell off. The first myth is that SPNT.PB will be delisted should a buyout occur. First I showed that other quality NYSE listed insurance companies that went private did not delist their preferred stocks. They often want to continue to have the option of issuing preferred stock and a de-listing would preclude that. But more importantly, the SPNT.PB prospectus states that SPNT must make best efforts to keep SPNT.PB listed on the NYSE , so a de-listing would be a clear violation of the promise made in the prospectus.

The second myth I debunked is the fear that SPNT.PB might stop paying preferred dividends if it goes private. There is absolutely no basis for this fear. There is not one example of a company going private and then turning around and suspending its preferred stock dividends. And we have numerous examples of companies with preferred stocks going private. And SPNT.PB, unlike other insurance companies, pays a cumulative dividend meaning the company can't escape ever paying these dividends simply by suspending.

Additionally, credit ratings, particularly by AM Best, are extremely important for insurance companies. Suspending its preferred stock dividend is almost unthinkable if this company wants to be a successful insurance company and maintain a high credit rating. And Dan Loeb has even stated that he wants to "enhance" the current credit rating which is incompatible with a preferred stock dividend suspension.

The selloff in SPNT.PB is based on fears that are pure conjecture regarding a scenario that is highly unlikely; that 1) that SPNT will go private which is uncertain, 2) that if it does go private it will de-list the preferred stock, and 3) once delisted it will stop making its cumulative preferred dividend payments. As Buffett says, buy when others are fearful (especially when fears are highly likely to be groundless). And what I say is "no guts, no glory". The probabilities are very high that SPNT.PB is a steal at current prices.

For further details see:

SiriusPoint Preferred 'B' May Be The Best Preferred Stock In The Market