SPNT - SiriusPoint's Preferred Units Are Compelling

2023-05-16 17:34:55 ET

Summary

- SiriusPoint, a global underwriter of insurance and reinsurance products, offers an attractive investment opportunity in its preferred stock for income-oriented investors.

- The company's Series B preferred shares, currently trading at $23.07 with a liquidation preference of $25, offer an 8% annual payout and additional potential upside of 8.4%.

- The preferred units' dividend resets every five years, with the next reset in February 2026, potentially providing further upside for shareholders if rates increase.

One of the oldest industries in the world is, perhaps surprisingly, the insurance industry. The oldest known example of insurance dates back to the 18th century BC in what is known as the Code of Hammurabi. In the thousands of years since then, the space has grown and evolved, eventually morphing into what we know today. It has many different facets to it and was responsible for nearly $6 trillion of global economic activity in 2022.

One small but interesting company in this space happens to be SiriusPoint Ltd. ( SPNT , SPNT.PB ). Generally speaking, I would be drawn to common shares in any company that I consider buying. But every so often, it's the preferred stock that catches my eye. And that happens to be the case here. Based on my own assessment, the preferred units of SiriusPoint represent an attractive investment opportunity that income-oriented investors should most certainly be drawn to.

Assessing SiriusPoint

SiriusPoint traces its current incarnation back to February of 2021 when the company, then known as Third Point Reinsurance Ltd., acquired Sirius International Insurance Group and changed its name to SiriusPoint. Operationally speaking, the company serves as a global underwriter of insurance and reinsurance products. Although based in Bermuda, the company has licenses to write property, casualty, and accident and health insurance and reinsurance across the globe. Its business model is not exactly typical for the insurance space. In all, the company engages in three primary lines of business.

The first involves underwriting insurance where it operates as the risk taker in the relationship. In essence, it holds the policy and takes any profits or losses as they are recognized. Second, the company generates services fee income from what it calls MGAs, or Managing General Agents. Through this set of operations, the company provides insurance products to individuals and corporations through agents who market the company's insurance products while having underwriting authority on its behalf (subject to its own standards). When these arrangements result in a policy being issued, SiriusPoint pays profit commissions to the agents in question. And finally, the company generates income from the investments that it makes with the capital on its books.

SiriusPoint

I think that it's fitting that the very first insurance policy known to exist, mentioned in the Code of Hammurabi, would essentially be likened to property and casualty insurance policy. That's because about 17.3% of gross premiums written by SiriusPoint fall under this category. In particular, we are talking about policies that offer property catastrophe excess of loss, proportional property reinsurance, per risk property reinsurance, and more. Within the Reinsurance segment that comprises 44.7% of all premiums written for the company, this is the largest category. This is followed up by casualty insurance at 15.5%. But the company does offer specialized insurance, such as those dedicated to the aviation and space industry, and the marine and energy markets. Under the Insurance & Services segment, the company that largely focuses on accident and health coverage, which makes up 25.2% of gross premiums written. But it also engages in workers' compensation and environmental offerings.

Operationally, SiriusPoint is a bit difficult to analyze. In addition to the aforementioned combination back in February of 2021, the company is also undergoing some other restructuring efforts. In the final quarter of 2022, for instance, the company incurred about $30 million of costs associated with reducing its property catastrophe business and closing its offices in certain markets. The company also attempted to sell its Lloyd's Managing Agency to Mosaic Insurance last year. However, that transaction ultimately fell through.

In April of this year, it became clear that the company had been approached by Dan Loeb's Third Point about a scenario where SiriusPoint may ultimately be acquired. After setting up a special committee aimed at exploring this opportunity further, SiriusPoint decided that it was in its shareholders' best interests to continue on its "current path." In response to this, Loeb acknowledged that he is no longer exploring a potential purchase of the enterprise.

{kind=link}

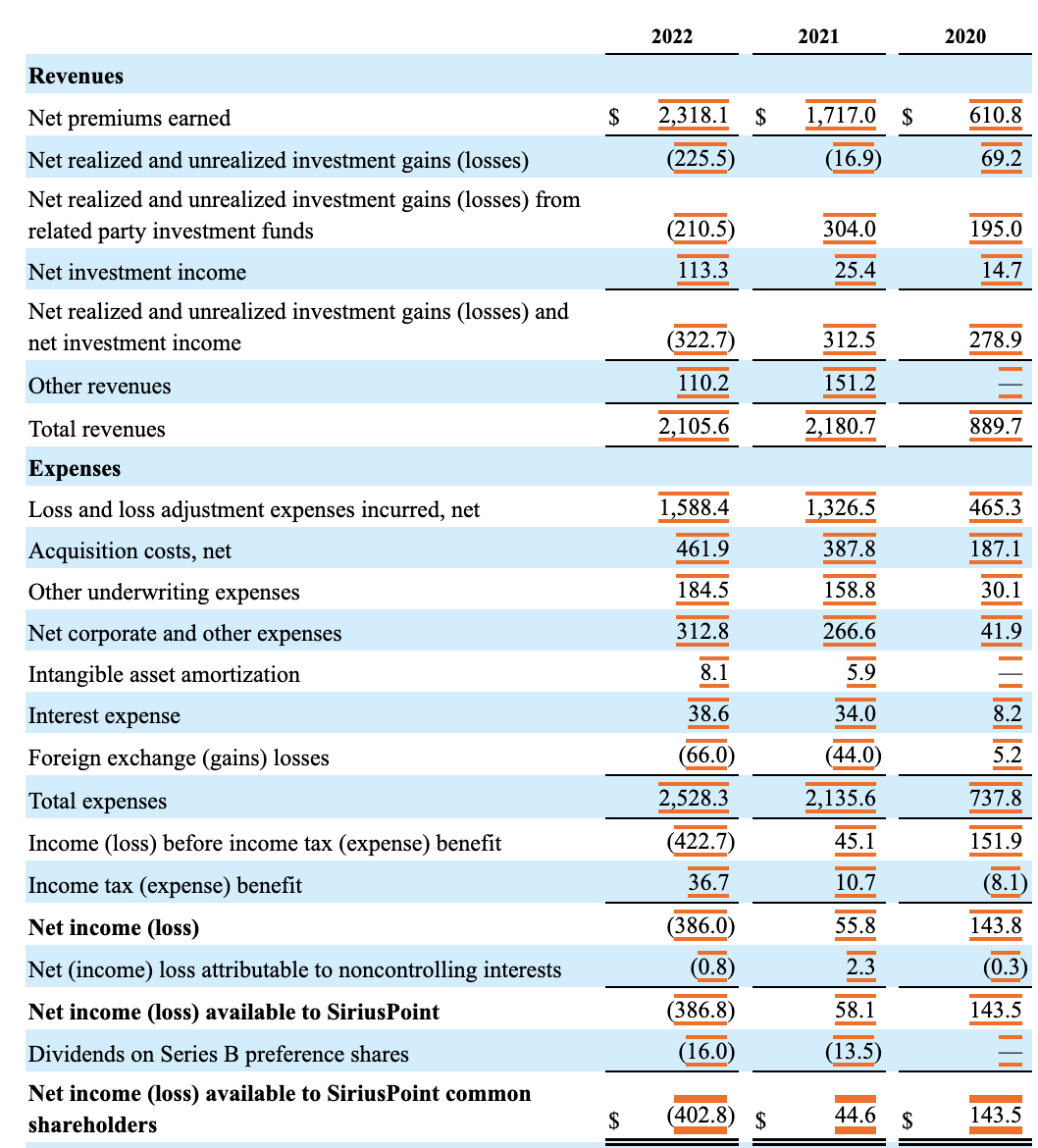

Keeping all of this in mind, SiriusPoint is a rather interesting company from a financial perspective. But as an insurance business, it's important to look at it through a slightly different lens than most other firms. For instance, in 2022, total revenue for the business was $2.11 billion. That was down from a $2.18 billion reported for 2021. But actual net premium revenue jumped during this time from $1.72 billion to $2.38 billion, while net investment income shot up from $25.4 million to $113.3 million. The disparity here is because the company recognizes gains or losses associated with its investments. And from 2021 to 2022, the company saw a massive swing here, including a swing totaling $514.5 million associated with net realized and unrealized investment gains or losses from related third-party investment funds.

{kind=link}

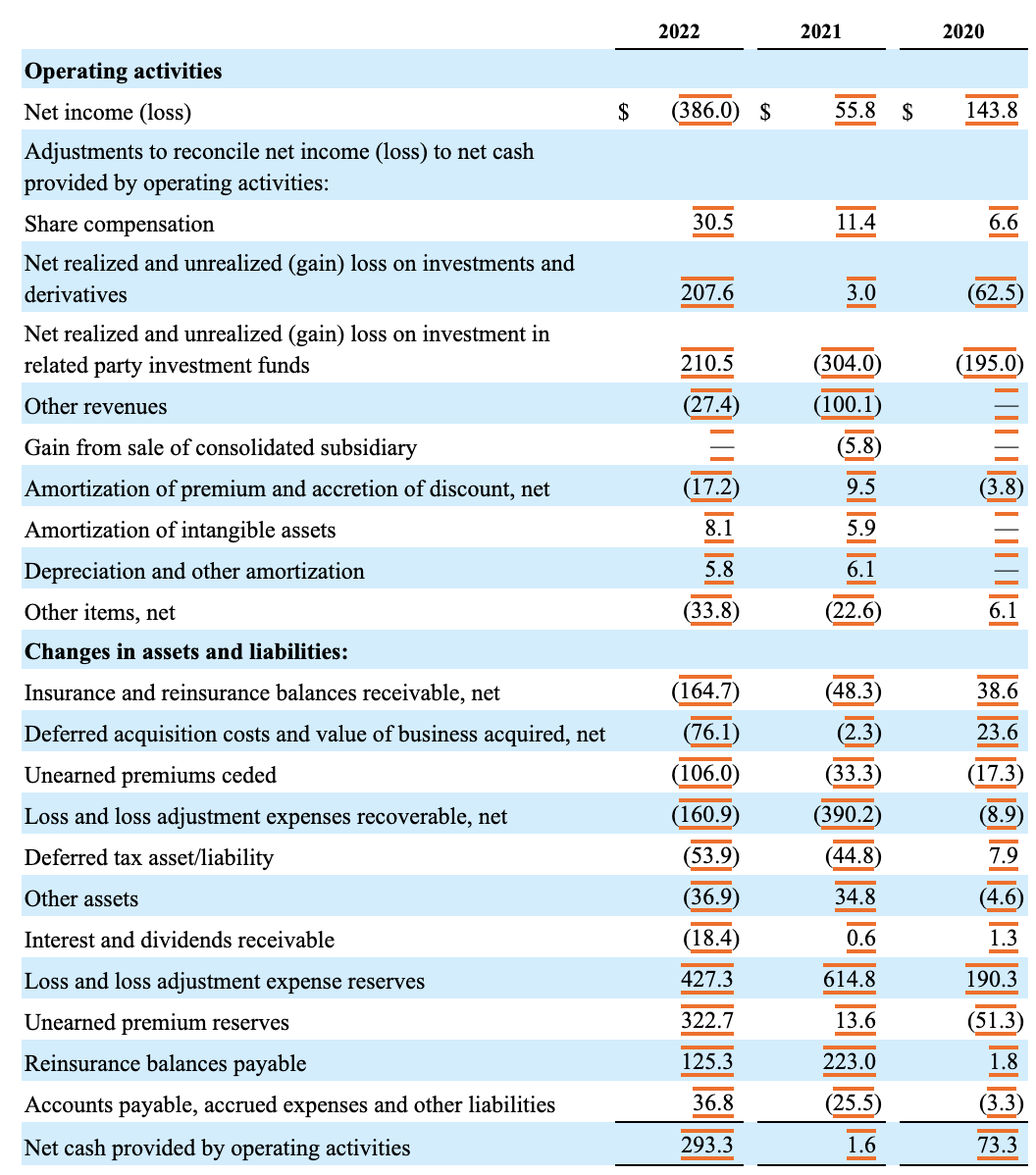

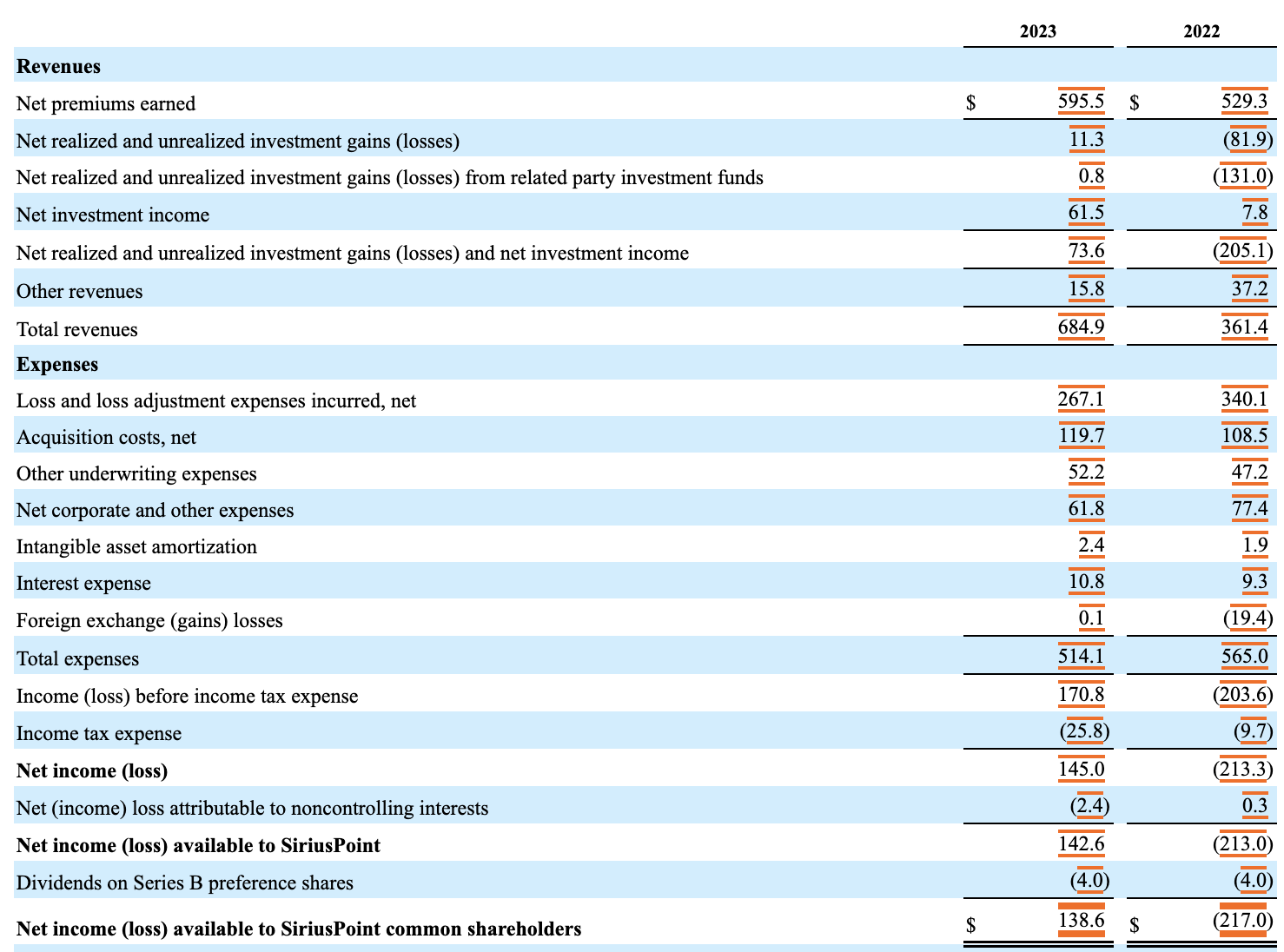

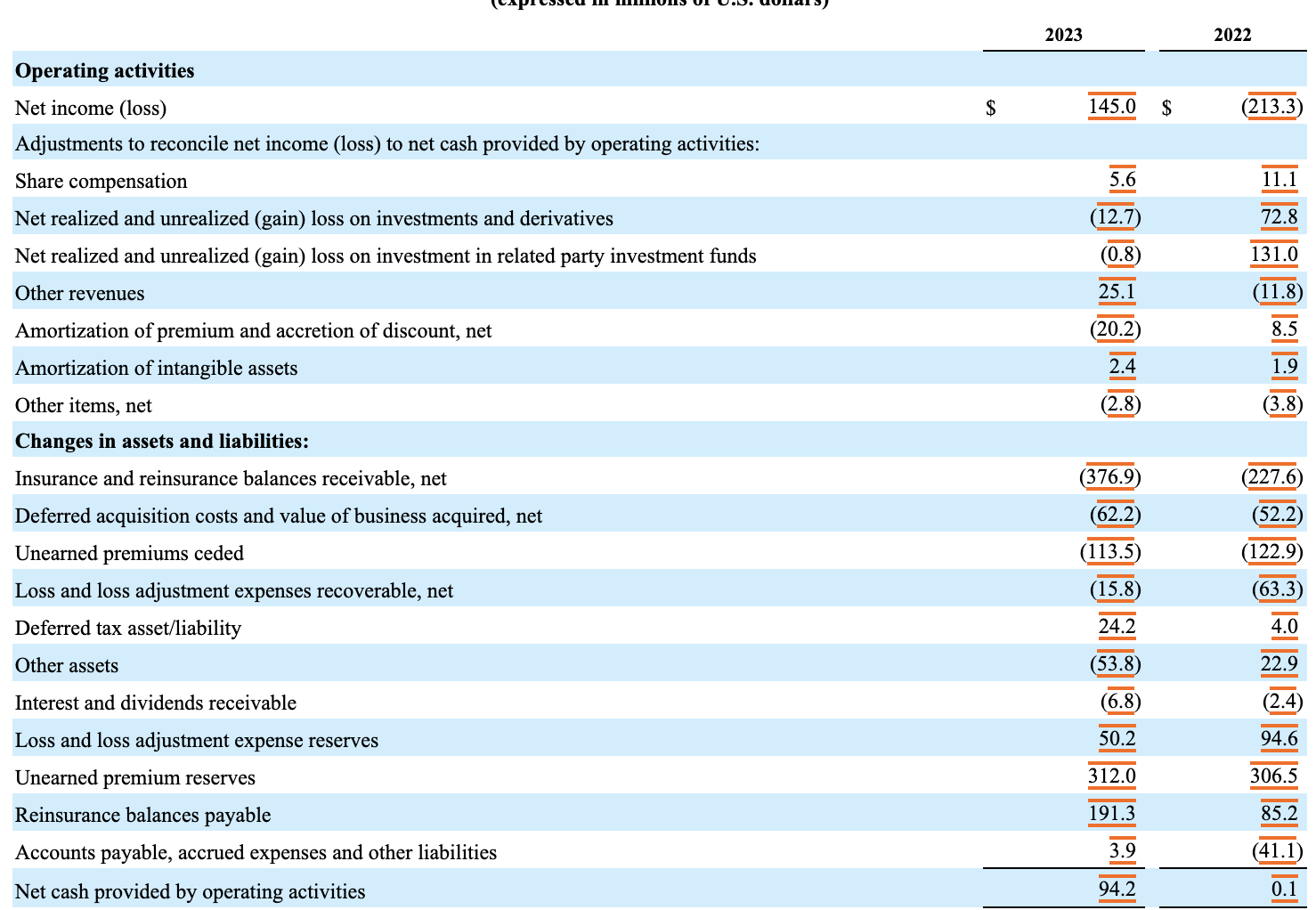

Bottom line results have been similarly volatile. Net income, after paying out preferred distributions, was a decent $44.6 million in 2021. But in 2022, it swung to a loss of $402.8 million. Cash flow data hasn't been much better. Although the company went from $1.6 million in 2021 to $293.3 million in 2022, cash flow on an adjusted basis has not been great. In 2021, it was negative to the tune of $318.2 million. Last year, it was negative by $1.9 million. As you can see in the images below, results for the first quarter of the 2023 fiscal year relative to the same time one year earlier have also been very volatile.

{kind=link}

{kind=link}

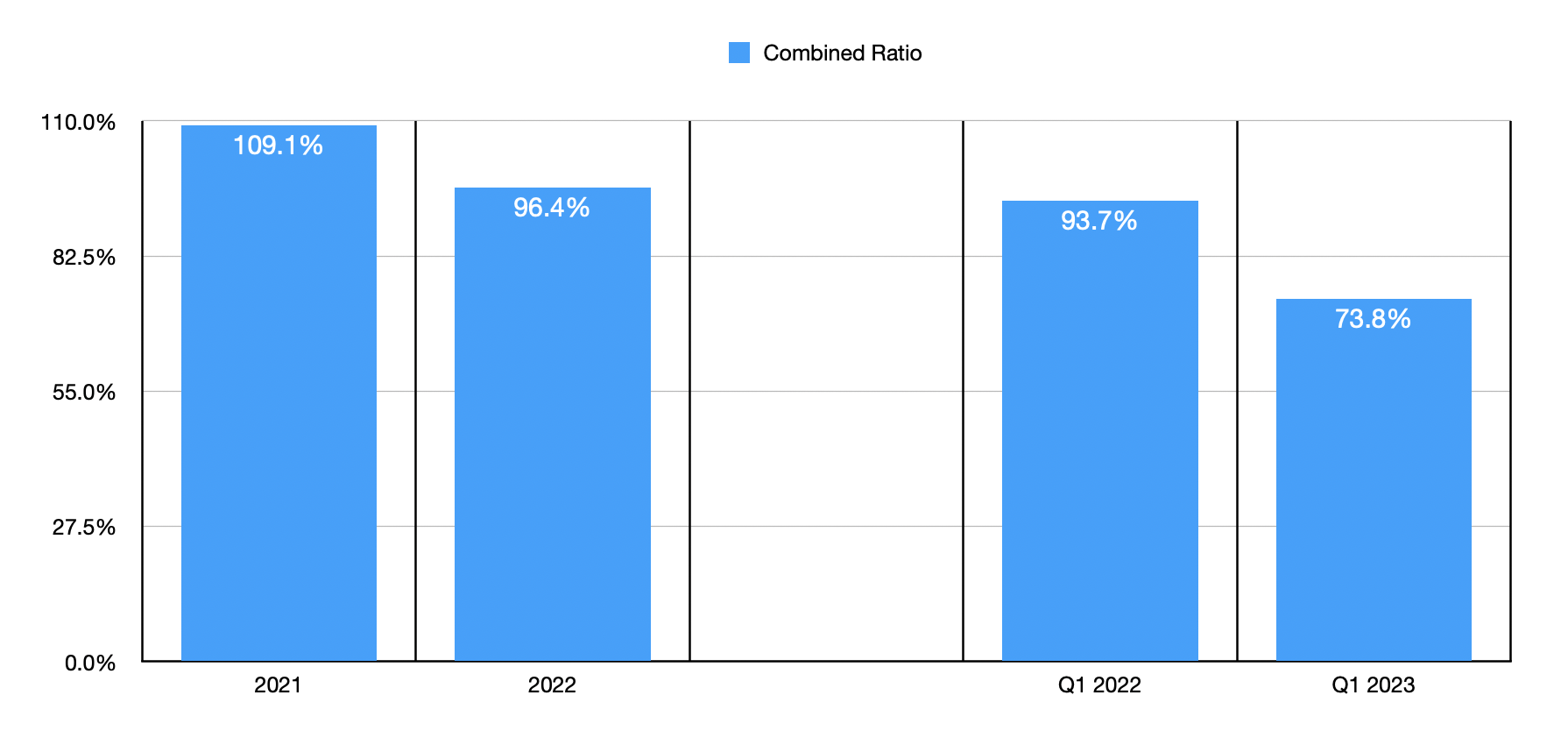

To really dig down into the numbers, and understand the company, we would be best to focus on a couple of key metrics. One of these is what the industry calls the combined ratio. In the insurance industry, the combined ratio is a measure of the profitability of the company's insurance operations. It can be defined as some of the claim-related losses the company incurs and the expenses it incurs, divided by the premium that's earned on its policies. In 2021, the company had a combined ratio of 109.1%. This meant that it was losing $9.10 on every $100 of premium earned. This number dropped to 96.4% in 2022. And recently, it has been falling more. During the first quarter of 2022, it came in at 93.7%. And in the first quarter of 2023, it dropped to 73.8%. This is a great trend to see.

{kind=link}

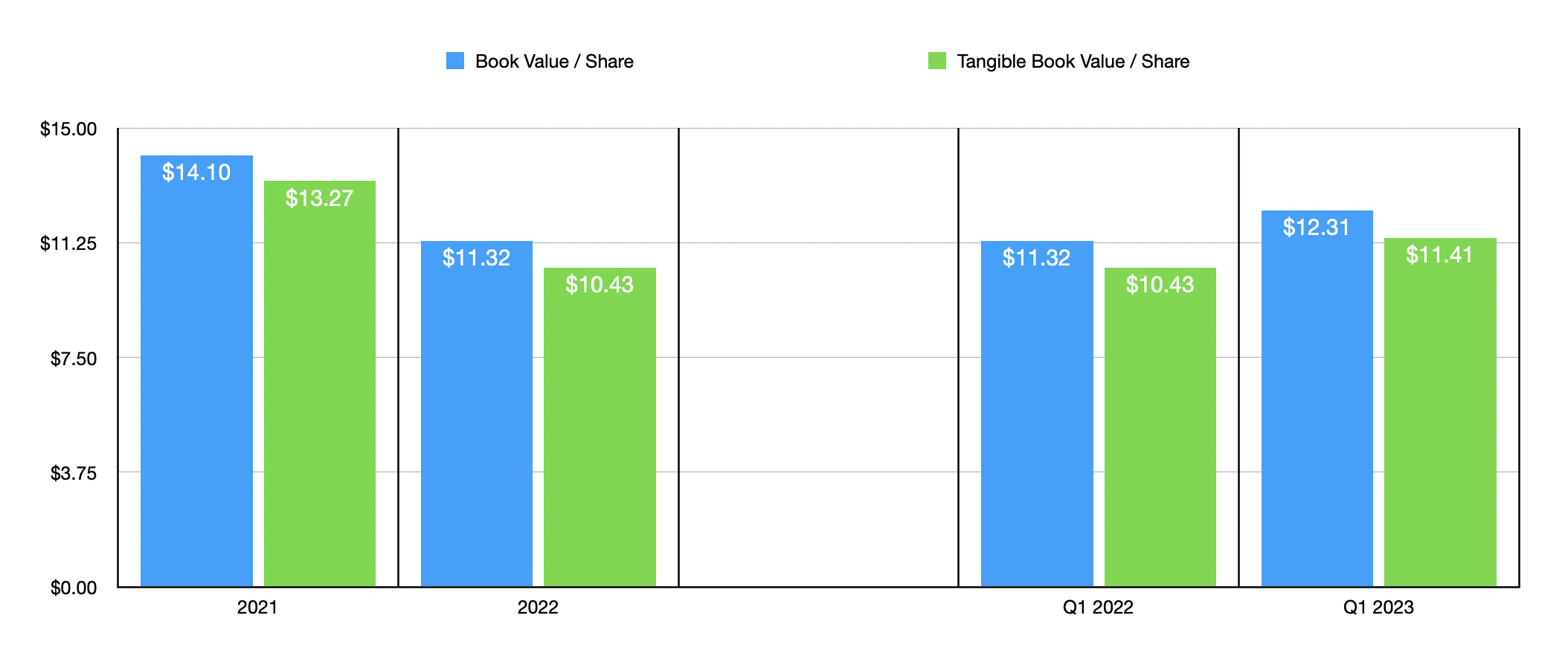

The other important metric to pay attention to is book value per share and tangible book value per share. This has seen some volatility. For instance, the book value per share of the company dropped from $14.10 in 2021 to $11.32 in 2022. Tangible book value declined from $13.27 to $10.43 over the same window of time. Fortunately, we have seen a reversal in this trend recently. In the first quarter of 2023, book value per share came out to $12.31, while tangible book value per share was $11.41. These were both higher than the $11.32 and $10.43, respectively, that the company reported for the same quarter one year earlier. It's typical in the insurance space for a company to be trading at a price that's below its book value per share. At present, SiriusPoint is trading at 73.4% of its book value and at 79.2% of its tangible book value. This provides a good amount of wiggle room for shareholders.

{kind=link}

Although my discussion so far has mostly applied to the common stock, I do think that the best area for investors to focus on might actually be the preferred. Namely, we are talking about the Series B preference shares that are publicly traded. As of this writing, these units are trading for $23.07 apiece. But they have a liquidation preference of $25. That alone offers an upside of 8.4% compared to where shares are trading now. But on top of this, holders of the preferred units are entitled to an 8% payout per year. While not exactly market-beating returns, it is a nice income stream. And with a total cost of only $16 million per year to the enterprise, it's not so much as to break the bank.

These units are interesting because of two primary things. For starters, the dividend on them resets on each five-year anniversary from the issue date. This means that, come February of 2026, the dividend will change from the 8% that is at today. The new rate will be the total of the five-year US treasury rate, plus 7.298%. Given that the five-year US treasury rate is currently 3.446%, resetting today would imply a distribution of 10.744%. The second thing that makes these interesting is that, for the most part, they are not callable. The one exception to this is that, on each five-year anniversary of issuance, they can be called at 100% of their liquidation preference. There are a few other instances in which they can be called, including at a rate of up to 102%. But these scenarios are unlikely to come to pass.

The ability to buy these units back every five years makes sense when you consider that the company is essentially wanting to have the chance to buy said units back before having to commit to another five years of payments that may or may not be higher than what the company is currently paying. And for shareholders, it creates an interesting opportunity because, if rates do get reset higher, and the units are not purchased back, the upside for the subsequent few years could be quite impressive.

I would not say that I am terribly optimistic that a reset will ultimately come to pass. After all, while interest rates are forecasted to be around 2% to 3% per year after the year 2025, having such low rates would, especially when combined with the tax shield that the company would be entitled to from interest payments on debt (a tax shield that does not exist when it comes to preferred distributions), Likely encourage the company to borrow if it has to in order to pay the preferred stock off. But if it does happen a reset and does so at a higher rate, that's an extra bonus for shareholders to enjoy.

Takeaway

From what I can see, SiriusPoint Ltd. is definitely an interesting company that investors should be aware of. The common stock might have some upside potential to it. But for those who want stability and a good income stream, I would argue that the preferred units are most certainly appealing. In the event that they do get reset in a few years, upside could be even greater. But we won't know what will transpire until it comes. In the meantime, the cash flow achieved from holding SiriusPoint Ltd. units, combined with the upside that the units should eventually see between where they are trading at and their $25 liquidation value, should be enough to justify a "strong buy" rating.

For further details see:

SiriusPoint's Preferred Units Are Compelling