SITM - SiTime: Small Time Company With Big Time Growth

2023-09-29 06:05:59 ET

Summary

- SiTime Corporation specializes in MEMS timing devices, offering a wide range of products with superior frequency stability and minimal jitter.

- MEMS timing devices have advantages over quartz alternatives in terms of performance, size, power efficiency, and reliability.

- SITM's growth has been volatile, with improvements in revenue and ASP but a decline in sales volume. However, the company's gross margins have improved, supported by rising ASPs.

In this analysis of SiTime Corporation ( SITM ), we evaluated the company's ability to maintain its growth and profit margins. To begin with, we conducted a thorough assessment of the company's MEMS timing devices business, scrutinizing its product portfolio for any potential competitive advantages. Subsequently, we conducted a comparative analysis between the precision timing market and the conventional quartz timing devices market, emphasizing the strengths of MEMS timing devices. Moving forward, we delved into an examination of the company's historical growth patterns, breaking down the analysis by volume and ASP. Lastly, we assessed the company's capacity to sustain its profit margins by thoroughly scrutinizing its pricing strategy and conducting an in-depth expense analysis.

Capitalize on MEMS Timing Advantages

The company specializes in timing devices which are integrated into programmable electronic systems to become semiconductor timing ICs that manage and control timing signals within the system. SiTime's products include oscillators, resonators and clock ICs. An oscillator "causes resonators to vibrate" and generates a regular repeating electronic signal. A resonator "vibrates at a precise frequency and provides the core accuracy and stability in oscillator systems". Finally, clock ICs combine both resonators and oscillators for timing references to produce clock signals used to sequence electronic systems and provide timing signals to synchronize the operation of digital circuits.

The company competes in the DAO market valued at $269.76 bln, which is 48.5% of the total semicon market. In the DAO market, the company only has a market share of 0.1% based on its 2022 revenue of $283.6 mln. Some of its competitors include Microchip (which acquired Discera in 2017) ( MCHP ) and Silicon Labs.

| Company |

| Number of Products |

| Frequency Stability ('ppm') |

| Jitter ('ps') |

| Max Operating Voltage ('V') |

| SiTime |

| 12,253 |

| ±0.008 |

| 0.9 |

| 3.63 |

| Microchip |

| 6,053 |

| ±10 |

| 3 |

| 3.63 |

| Silicon Labs |

| 353 |

| ±20 |

| 1.3 |

| 3.63 |

Source: Company Data, Arrow Electronics , Khaveen Investments

Based on our comparison between SiTime, Microchip and Silicon Labs, SiTime offers a significantly larger number of products (12,253) compared to Microchip (6,053) and Silicon Labs (353), indicating its broader product breadth. Moreover, SiTime boasts impressive frequency stability of ±0.008 ppm and exceptionally low jitter of ±0.008 ps, far superior to Microchip and Silicon Labs respectively. SiTime also matches the other companies in terms of the maximum operating voltage at 3.63V despite its stronger performance, which indicates superior power efficiency. Overall, we believe SiTime's combination of a vast product portfolio, superior frequency stability, minimal jitter and power efficiency highlights its competitive advantage. Furthermore, based on the company's investor presentation , it highlighted its continuous improvement in frequency stability.

{kind=link}

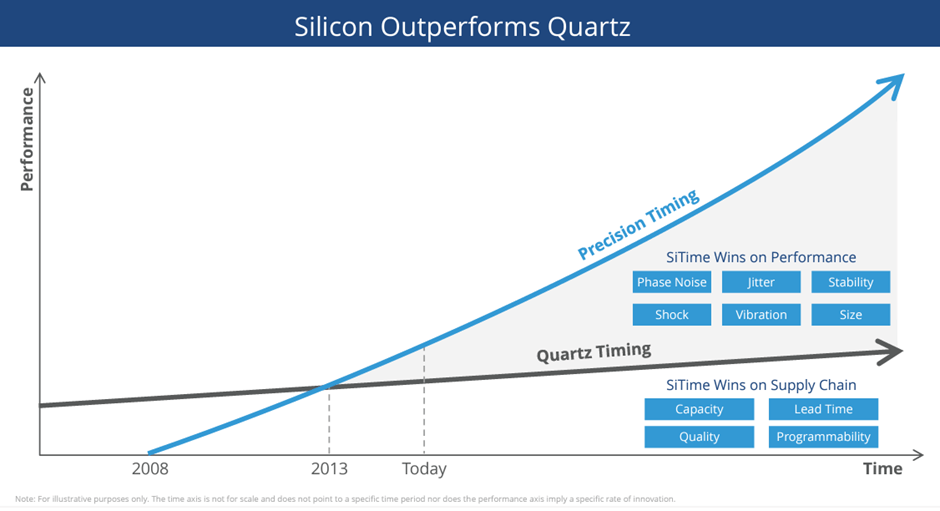

Based on Yole Development, MEMS timing technology is emerging as the preferred choice compared to quartz due to its advantages in performance, size, power efficiency, and reliability. In a study from the Electronic Engineering Journal, SiTime's MEMs products are compared with quartz timing products and tested to be more stable in comparison to quartz-based solutions as it is "designed to perform in extreme conditions and provide the robust system performance and stability required in harsh environments". In terms of jitter, the study found that the MEMS oscillator has a phase noise "about 10 times lower than the quartz device". Furthermore, in terms of AN10025 Reliability Calculations for SiTime Oscillators, the company has a mean time between failure (MTBF) of 1.140 mln hours which is 30x higher compared to quartz competitors IDT (38) and Epson (28). In terms of size, Microchip's MEMS oscillator is 40% smaller. Additionally, the MEMS oscillator has a 4.6x improvement for vibration as well as 60% lower power consumption compared to a quartz-based oscillator. Therefore, we believe that this highlights the advantages of MEMS timing devices in terms of performance (stability and jitter), smaller form factor, lower power usage and reliability.

In summary, we determined that SiTime stands out due to its extensive range of products, exceptional frequency stability, minimal jitter, and energy efficiency, giving it a strong competitive edge. Consequently, we anticipate that the company is well-positioned to seize opportunities arising from the potential transition from quartz timing devices to MEMS-based timing devices, thanks to their superior performance, compact size, power efficiency, and reliability.

Volatile Growth

{kind=link}

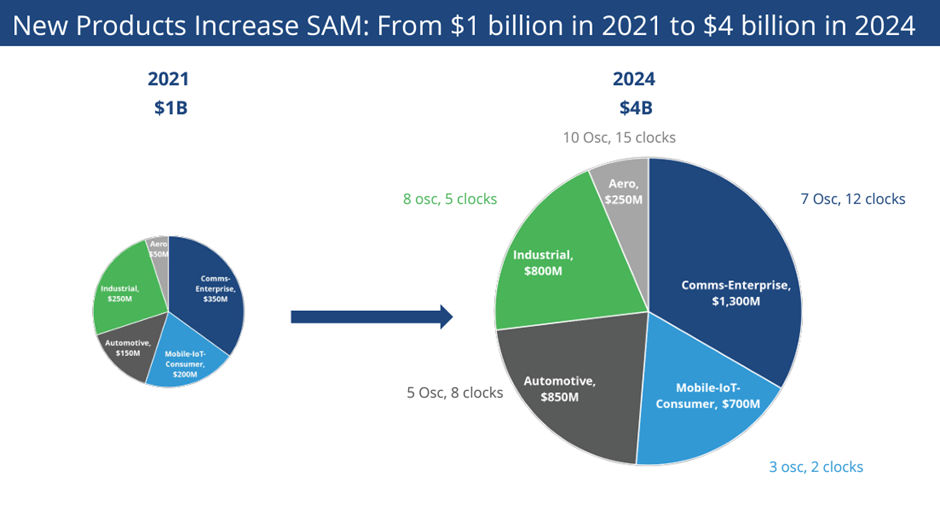

Based on its latest earnings briefing, the company has expanded its SAM from $1 bln in 2020 to $2.5 bln in 2022 in a range of end markets such as enterprise, communications, automotive, and aerospace defense. From its investor presentation, the company projected a SAM of $4 bln by 2024 which is a CAGR of 60%. From the chart, the automotive segment has the largest growth. The company recently added to its product lineup the SiT162X, designed to enhance safety in automotive applications such as ADAS automated driving. According to SiTime...

The number of timing chips in cars has grown and will continue to grow. In 2018, vehicles used up to 20 timing chips, at a price of $5-$8, and today they have about 35 to 60 timing chips because of the electronics added to the car, at a cost of $25-$35 per car. There will be more than 125 timing chips, priced at $50-$70 per car, by 2026, as the automotive industry gets to ADAS Level 4, which will require more electronics, more sensing and more connectivity in the network to ensure split-second decisions when in fully automated mode. - SiTime

| SiTime Revenue ($ mln) |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| H1 2023 |

| Average |

| Sales Volume Growth |

| -1% |

| 27% |

| 34% |

| 2% |

| - |

| 15% |

| ASP Growth |

| 0% |

| 9% |

| 40% |

| 27% |

| - |

| 19% |

| Total Revenue |

| 85.2 |

| 84.1 |

| 116.2 |

| 218.8 |

| 283.6 |

| 66.0 |

| Growth % |

| -15.7% |

| -1.3% |

| 38.2% |

| 88.3% |

| 29.6% |

| -55.9% |

| 39% |

Source: Company Data, Khaveen Investments

Based on the table above, the company's revenue growth has improved over the past 5 years. It had negative growth in 2018 and 2019 but improved sharply in 2020 supported by strong sales volume growth of 27% in that year. Following that, its growth accelerated in 2021 supported by both ASP and sales volume growth. However, its growth moderated in 2022 as sales volume growth slowed down to only 2% but its ASP growth remained strong at 27%. Furthermore, based on its annual report, the company stated that its "increase in sales volume was driven by higher demand for our products from new and existing customers" whereas the "ASP increase was related to change in mix of the higher ASP products". Overall, the company had an average revenue growth of 39% with both sales volume and ASP having strong average growth of 15% and 19% respectively.

Though, in H1 2023, the company's revenue declined by 55.9%. According to the company, its ASPs continued to increase in Q2 2023 compared to the previous year and were stable in Q1 2023 . Thus, we believe indicates its performance was affected by declining sales volume rather than ASPs. In relation, the company stated that its customers had over-ordered in the previous year, stemming from pandemic-related supply shortages affecting multiple companies and estimated that the excess orders amounted to around $40 mln. Nonetheless, the company stated that the inventories have declined.

In past calls, we noted the negative impact of higher-than-normal inventories at a customers' contract manufacturers or CMs on our revenue. For the past few quarters, these inventories have continued to decline. Though the decline is at a slightly slower rate than previously anticipated, we have factored this into our guidance for now. So looking towards Q4, we expect the quarter-over-quarter growth trend over Q3 to continue. - Rajesh Vashist, CEO

Overall, despite the company's high average growth of 39% for revenues, its growth has been volatile as it improved from 2018 to 2022 but had moderated in 2022 and has declined for the first half of the year. Although both its sales volume and ASPs have high average growth over the period, its sales volume growth had been more volatile compared to its ASPs which improved through 2022 and maintained a strong growth in 2022 and continued to grow in H1 2023.

ASP Could Sustain Margins

Company Data, Khaveen Investments

{kind=link}

| Earnings & Margins |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Gross Margin (%) |

| 47.38% |

| 42.49% |

| 47.09% |

| 49.83% |

| 63.76% |

| 64.53% |

| EBIT Margin |

| 5.54% |

| -9.15% |

| -5.83% |

| -6.63% |

| 13.89% |

| 2.50% |

| Net Margin (%) |

| 4.65% |

| -10.92% |

| -7.85% |

| -8.09% |

| 14.76% |

| 8.22% |

| Free Cash Flow Margin |

| -5.33% |

| -7.41% |

| 4.57% |

| 7.57% |

| 11.56% |

| -182.92% |

Source: Company Data, Khaveen Investments

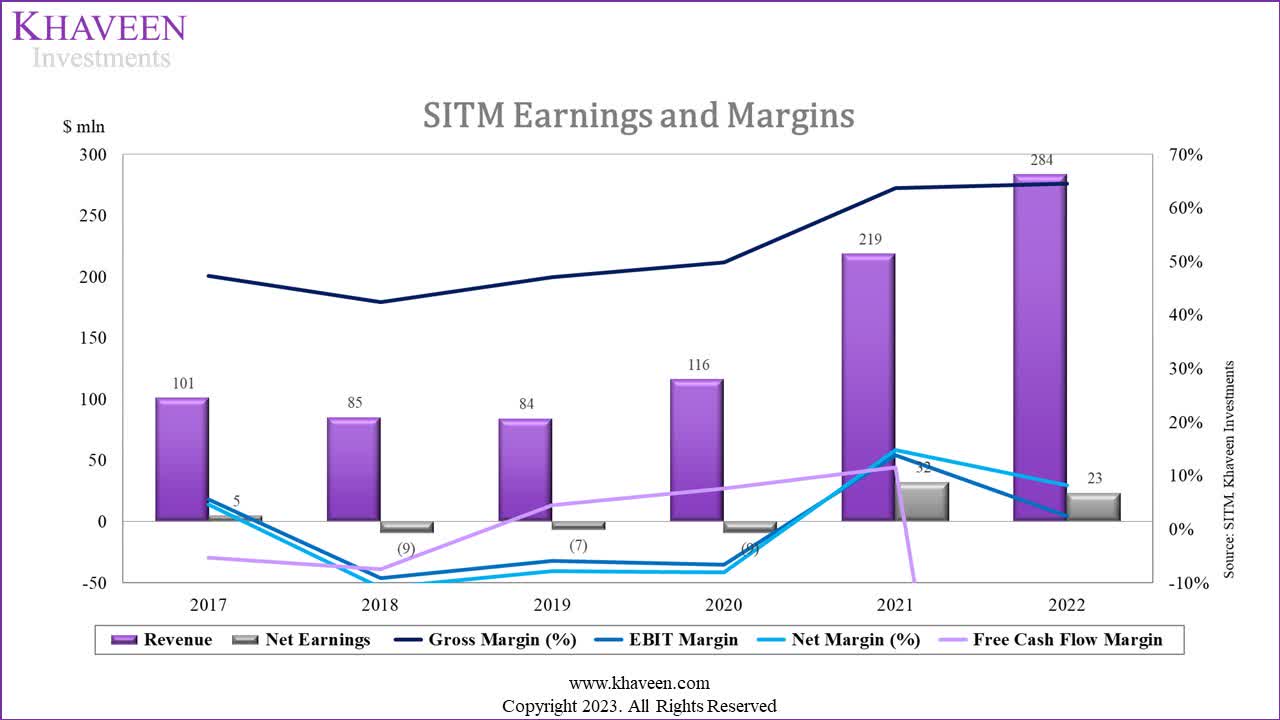

Based on the table, the company's gross margin has improved over the years from 47.38% in 2017 and peaking at 64.53% in 2022. The EBIT margin was negative in 2018 and 2019 followed by a notable increase in 2021 but decreased in 2022. The net margin followed a similar trend, with negative margins in 2018 and 2019, then experiencing significant growth in 2021 before moderating in 2022. However, the company's FCF margin improved from negative in 2017 and 2018 to positive margins except for a substantial drop in 2022. Based on its financial statements, the company had investments in marketable securities of $524 mln in 2022 which was 94% of its investing cash flow.

Company Data, Khaveen Investments

{kind=link}

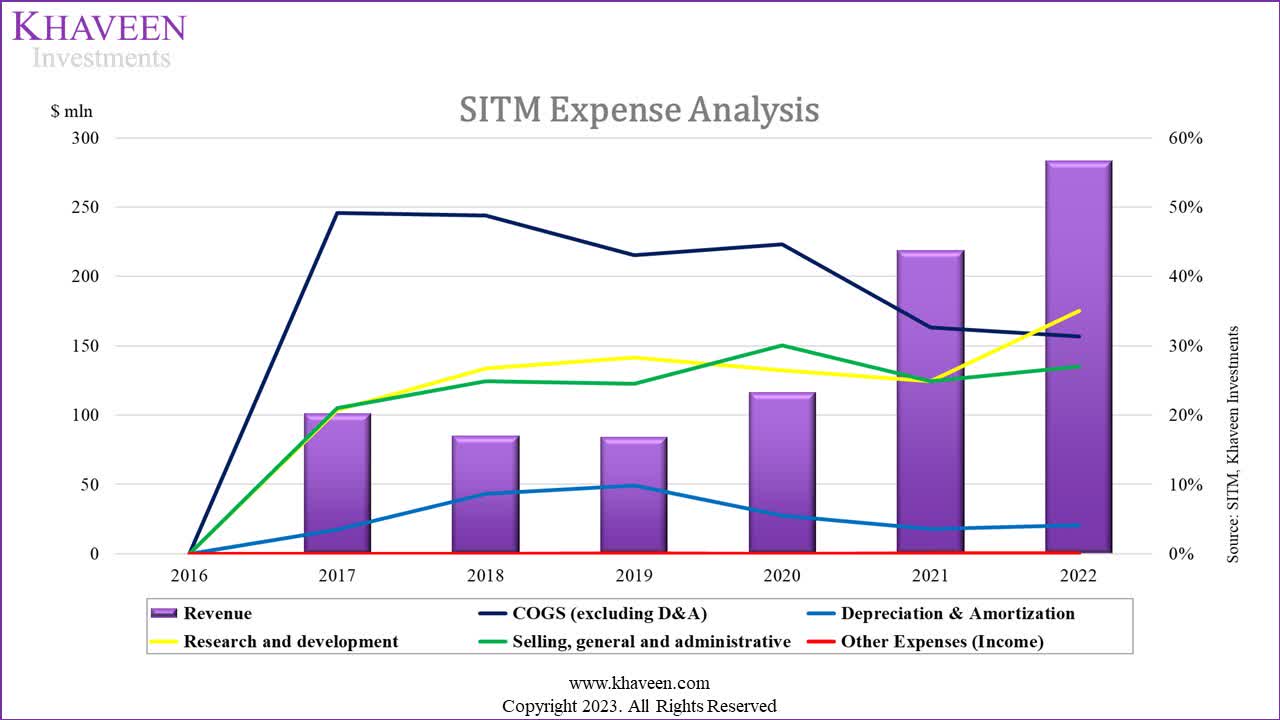

Furthermore, based on its expense analysis, the company's COGS as % of revenue had decreased from 2017 to 2022 with a sharp decline in 2021 as its revenue increased strongly. However, the company operates as a fabless model. The company highlighted its margins benefit from higher ASPs from its earnings briefing. Furthermore, its operating expenses, such as R&D and SG&A have experienced a rising trend over the past 6 years. Though, depreciation increased through 2019 but moderated following that through 2022. Therefore, the company's improvement in margins was attributed to its rising gross margins as its COGS % of revenue declined rather than decreasing operating costs as % of revenue.

Furthermore, based on the company's latest earnings briefing, despite its revenue declining by 55.9% in H1 2023, the company's management highlighted its ASPs were still higher compared to the same period last year which we believe highlights its pricing power.

An insight is that despite the normal supply in the market today, our Q2 2023 ASP was higher than Q1 2022, which you may recall, was at the height of an industry wide shortage. We believe that the higher ASP products that we introduced since Q1 '22 and the increase in business from aerospace defense contributed to this. - Rajesh Vashist, CEO

Additionally, the company stated that it plans to continue introducing new high-performance products that command higher ASPs and could support its gross margins.

Longer term, what we've always talked about and what I still firmly believe will happen is that all of our new products that we have introduced over the past one and two years that we plan on introducing this year are generally much higher performance products, they're going into higher performance markets, we get higher ASPs and generally higher gross margins. - Rajesh Vashist, CEO

Overall, we identified that the company's improvement in its profitability is influenced by its increasing gross margins, which were supported by its rising ASPs as discussed in the first point. Moreover, we believe that the company could sustain its margins as its ASPs rose despite the slowdown in demand.

Risk: Future Competition from Larger Players

We believe one of the key risks for the company is the competition in the timing devices market. While it currently dominates the MEMS timing devices market, we believe larger competitors in the global timing devices market, including NXP (NXPI), Texas Instruments ( TXN ) and Murata ( MRAAY ) could pose a competitive threat to the company.

Verdict

To summarize, we believe SiTime stands out in the market due to its expansive product range, remarkable frequency stability, minimal jitter, and energy-efficient solutions, providing it with a robust competitive advantage. As a result, we anticipate that the company could be positioned to capitalize on the potential shift from quartz timing devices to MEMS timing devices, given their superior performance, compact form factor, energy efficiency, and reliability. However, the company's growth trajectory has been somewhat inconsistent. While there were improvements from 2018 to 2022, there was a moderation in 2022, followed by a decline in the first half of the current year, primarily attributed to excess customer inventory. Although sales volume exhibited fluctuations, with an increase in 2021 and negative growth in 2022, ASP consistently showed growth over the past three years. While MEMS timing devices offer clear advantages over quartz alternatives and could signal an opportunity for market transition, we acknowledge the potential threat posed by larger competitors in the industry. Nevertheless, we believe the company's enhanced profitability can be attributed to the expansion of gross margins, supported by rising ASPs, even in the face of a demand slowdown.

The company has a high P/S of 16.14x which is more than 6x higher than the sector median. Thus, we based our price target on the low range of analyst consensus of $110 which is an upside of -2.5% and rate the company as a Hold.

For further details see:

SiTime: Small Time Company With Big Time Growth