SIX - Six Flags And Cedar Fair: 2024 Sets Up For A Major Re-Rating

2023-12-30 08:54:33 ET

Summary

- FUN and SIX are merging. Their joint Form S-4 proxy statement reveals management is targeting $1.5 billion of EBITDA in three years.

- A failed transformation at SIX, and lackluster performance at FUN, has left investors disenchanted, but a turnaround is imminent.

- Monthly third-party data, balance sheet analysis, and management commentary is supportive of three key catalysts resulting in a material positive inflection in EBITDA in ‘24/’25.

- At 9x EV/EBITDA, there's a clear path to 50% equity appreciation over the next 12 months, ramping to 100%+ by the end of 2025.

Investment Thesis

Six Flags (SIX) is one of the most attractive small cap situations in the market today. It is hated by investors of all stripes, after failing to execute on a customer transition, seeing attendance fall by double-digit percentages, and having its stock price cut in half over the past 24 months. Layer on an ugly balance sheet with five turns of leverage and it's easy to see why few on Wall Street are big fans.

Despite the bad press, a re-rating is fast approaching, as fundamental catalysts in the form of an attendance recovery, firm pricing, execution against a merger, and a meaningful EBITDA inflection in 2024/2025 materialize. Monthly government data on the industry, balance sheet analysis, and management commentary corroborate this view.

There's a path to $1.4 billion of EBITDA by 2025, confirmed by the proxy, which is over $175 million ahead of consensus. As expectations revise upwards and management executes, there's a clear path to 50%+ returns over the next 12 months, escalating up to 100% by the end of 2025.

Background

In November, Cedar Fair ( FUN ) and Six Flags, amusement park operators who collectively run 51 properties and generated $1 billion of LTM adjusted EBITDA, announced that they would be merging. The economic value of the deal will be split evenly, with Cedar Fair shareholders owning a slight majority of the NewCo equity, with SIX shareholders receiving the remaining equity and a $1 special dividend.

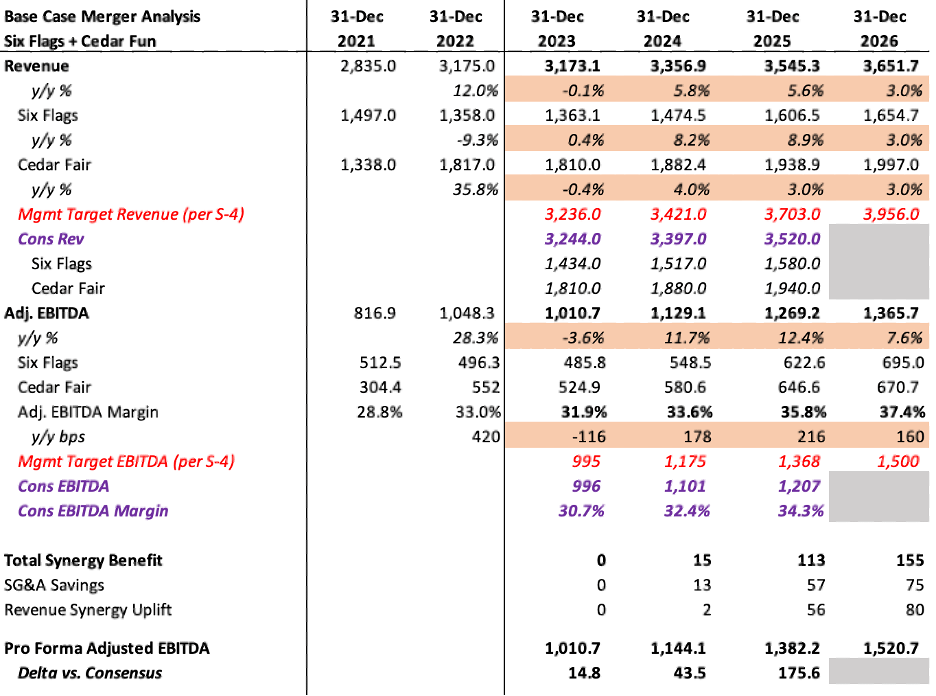

Much has already been written about the deal and I'd direct you to SIX's investor presentation and press release for details, but the basic rationale is that by combining, FUN and SIX can cut overhead and share institutional knowledge, ultimately resulting in more earnings power than if they operated independently. The major thing to note is that buried on page 91 of SIX and FUN's joint Form S-4 proxy , which provides extensive details about the merger, is a table detailing the "NewCo's" goal of reaching $1.5 billion of EBITDA by 2026.

I created a model for the NewCo before the S-4 was finalized, and management's guidance confirms my own work. The rest of the article discusses my diligence of several catalysts and the implications for the NewCo's earnings power.

Catalyst #1: Material Attendance Recovery on the Horizon

In the amusement park industry, there are two key performance indicators that drive revenue: attendance and per capital guest spend. Both Six Flags and Cedar Fair's top-lines are largely determined by the equation: (attendance × per capita guest spend = revenue).

Over the past several years, SIX and FUN have taken different approaches to growing revenue. Six Flags, under CEO Selim Bassoul, has opted to emphasize per capita guest spend at the expense of attendance, while Cedar Fair has taken a more balanced approach, aiming for LSD growth in both categories.

Unfortunately for Six Flags, Selim's strategy has largely failed, with the company backtracking on high-priced ticket sales over the past several quarters, as attendance plummeted and an increase in guest spend was insufficient to make up the shortfall. As I read the situation, SIX's decision to tie the knot with FUN was driven by a recognition of Selim's failure to effectively increase revenue … but the past is the past, and there are tell-tale signs that attendance is poised to inflect over the next year, supporting a strong 2024 performance.

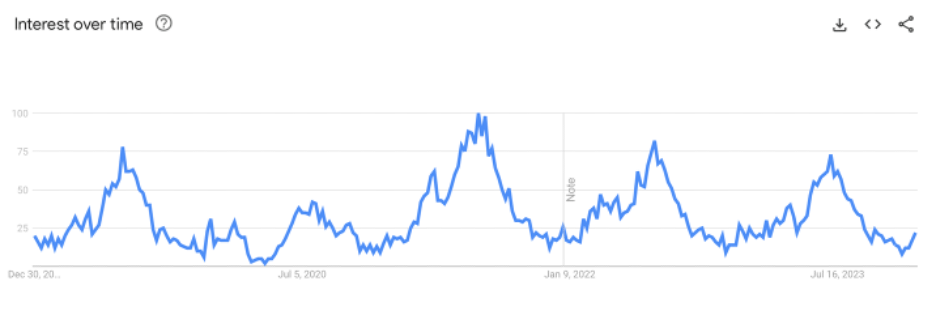

Google Trends Data Supportive of Material Uplift

The public shift in the perception of Six Flags can be seen in Google Trends data, which demonstrates a 30% decrease in peak search interest since Selim stepped into the driver's seat (a time highlighted in red), as radically higher prices dissuaded visitors from spending time at Six Flags.

SIX interest over time (Google Trends)

{kind=link}

The relative stability of interest in the "amusement park near me" search term, which is already consistently meeting pre-pandemic levels of search frequency, highlights the degree to which Six Flags has alienated their guests--but also the opportunity for SIX to capture a willing customer base, still interested in SIX's experiences.

{kind=link}

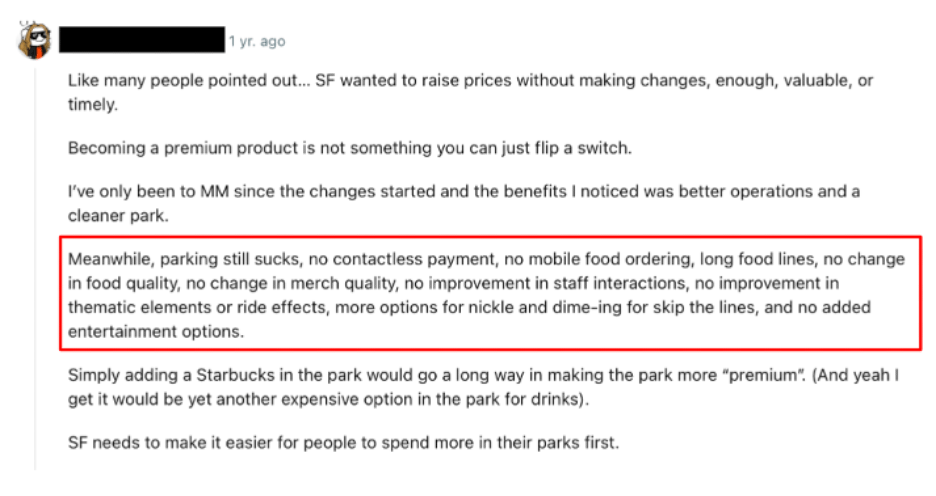

Looking back on the evolution of Six Flags' approach, it can best be summarized as "too much, too soon," as management made the mistake of raising prices at the same time as they improved the experience, instead of improving the experience, then raising prices once customers understood the improved value add that was being offered.

In my diligence, I stumbled across the Reddit forum r/rollercoasters and a common gripe was prices going up without a commensurate increase in quality. The post below sums up sentiment quite well:

{kind=link}

Importantly, people want to go to Six Flags … consistent searches for the park before Selim Bassoul arrived and a Reddit forum full of passionate customers confirm that. It's just that over the past year, guests have felt like they're getting ripped off.

So why am I optimistic about an attendance recovery? Four reasons.

Reason #1: Quality is Catching up to Price

Given that Six Flags is currenting run rating at $165+ million per year in capex, compared to maintenance capex levels of ~$100 million, it's clear that the company is investing a lot in their aspirations for shaded areas, green space, updated rides, and quality dining options across their parks. In short: making up for investments that should have been made years ago but were foregone by a prior management team devoted to maximizing short-term free cash flow. As capital improvement projects wind down and the guest experience improves in 2024/25, attendance should track an improvement in sentiment, as instead of merely claiming to be "premium," by the time Q2 and Q3 of 2024 roll around, Six Flags actually will be.

Additionally, Six Flags has been discounting tickets at the same time as they have been increasing the quality of their offering, driving a 16% YoY increase in attendance last quarter alone. Extrapolating that strength forward into next year supports a strong 2024 for SIX, particularly as they lap easy comps from last year, and word-of-mouth and online reviews drive increased visitation.

Management at both Six Flags and Cedar Fair highlighted on their joint investor call in connection to the merger that improving the customer experience was a chief concern for them and I expect further emphasis on guests to drive enhanced attendance.

Reason #2: Deferred Revenue Indicative of a Rebound

Aside from more intangible evidence, such as cleaner parks and a better guest experience, there's evidence on the balance sheet that's supportive of a strong recovery in 2024 for Six Flags. Over the past several quarters, deferred revenue (revenue received for a good/service not yet delivered), a proxy for season pass sales, is tracking up 17%, versus a decline of 28% last year as customers balked at higher prices.

And although season ticket sales oscillate more than total admissions revenue in response to price changes, since the price point of a season pass starts ~100% higher than a day pass, and thus is more sensitive to changes in customer sentiment, on a directional basis, it's been correlated to overall revenue growth pre-pandemic (0.67 correlation coefficient).

{kind=link}

Cedar Fair's CFO commented on a rebound in deferred revenue on FUN's Q3 call, as well, highlighting that the rebound is broad-based at both companies:

The increase in deferred revenues has been driven by an outstanding start to fall sales of 2024 Season Passes and related all season products. Through this past week, combined sales are pacing up 24% or approximately $30 million over the same time last year. We're confident that our Season Pass strategy and outstanding start position us well for another strong season in 2024 .

Reason #3: Cross-Selling Opportunity Supports Attendance Growth

Season passholders constitute 55% of FUN and SIX's attendance, but only attend 1-2 parks in their area. Selim Bassoul referenced this on the call, but it's a remarkably similar set-up to the ski industry a few decades ago before Ikon and Epic rolled up dozens of independent operators into two nationwide behemoths with an unparalleled value offer for consumers. Ultimately, that roll-up has driven higher attendance across the network, as skiers were willing to frequent more mountains, more often, thanks to the flexibility enabled by a nationwide season pass.

From a competitive positioning standpoint, the merger of Cedar Fair and Six Flags positions both companies well, as management has guided to the creation of this exact season pass program à la Epic. When instituted, this offer of complete access to 42 amusement parks and 9 water parks will further help to differentiate Six Flags and Cedar Fair's properties from regional competitors, who simply don't have the footprint to compete nationally. This dynamic will ultimately be supportive of further attendance growth long-term, as guests are driven into the arms of the most value-adding operator near them.

The NewCo's S-4 quantifies that this should act as a ~$90 million EBITDA tailwind (likely $150+ million revenue impact) over the next five years alone. There's likely additional upside optionality to that projection, given consumers' love of everything "unlimited."

Reason #4: Capacity Is There

This is a basic point. Management at Six Flags has been clear: They aim to have 25-27 million guests per year by 2025, versus 20.4 million last year. Compared to pre-pandemic levels of more than 32 million, that target is achievable, particularly in the context of lower prices and an improved guest experience. SIX also has 700 acres of undeveloped land, which, if developed, could grow their parks' footprints by 12%.

The impact of this tailwind to the top-line is difficult to understate, as hitting just the low-end of that range at 25 million guests implies annual revenue growth of 7% per year … and that's before layering on escalating ticket and concession prices.

Catalyst #2: Per Capita Guest Spend Stabilizing, On Track to Increase in '24/'25

After a rough start to 2023, characterized by a low single-digit drop in SIX's guest spend per capita, dragged down by discounted admissions, 2024 is poised to see a stabilization in guest spending, as in-park pricing remains firm, thanks to a macro backdrop characterized by inflation, at the same time admissions revenue normalizes.

As I wrote earlier, the two determinants of an amusement park's revenue are attendance and per capita spend. Going forward, growth in the latter will be just as important as attendance growth when it comes to growing shareholder value long-term.

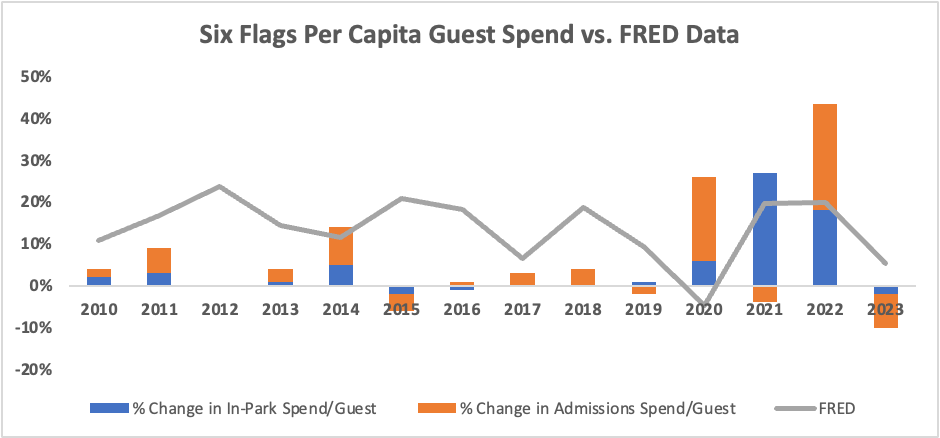

But rather than just shooting in the dark about where per capita spend will end up next quarter, it's instructive to look at alternative data sets. FRED , a data aggregating site run by the Fed, helpfully sweeps admission and concession price data every month as part of formulating their producer price index, giving us a sense of where admission and in-park pricing is month-to-month.

While not predictive enough to base quarterly assumptions off, since Six Flags has different exposures than the industry writ large and leans more into season passes, which offer more consistent pricing, when I layered the FRED data over a table of the change in in-park and admission spending per guest, it's evident the data is directionally correlated.

{kind=link}

And what it shows over the past several months is an acceleration in pricing not seen since before Covid, with prices across the amusement park industry ramping up 7.5% since August alone.

Six Flags and Cedar Fair are uniquely poised to benefit from this dynamic, as despite being familiar to most Americans, their prices are consistent with those of unknown local players. While the incomes of their core demographic prevent SIX and FUN from taking prices too high, it's easy to see pricing slowly creep into the high $30s over time from the low $30s where they are now.

Catalyst #3: EBITDA Inflection Driven by Attendance, Pricing, and Synergies

At the same time as the NewCo will realize higher revenue growth from attendance and pricing growth, there's a major opportunity on the cost front as well.

From a more basic level, there's the three-year $120 million EBITDA synergy target highlighted by management in their investor deck, but that number can likely go much higher, as the proxy statement forecasts a $200+ million opportunity by 2027, which is just four years out. Around two-thirds of that comes from corporate cuts in the back-office, while another third comes from the cross-selling opportunity explained above.

Additionally, it's important to understand that amusement parks operate in a fixed cost industry, where marginal costs are very low and incremental margins are very high, as once a $25+ million amusement park is open and staffed, even a large increase in attendance won't drive a meaningful increase in OpEx.

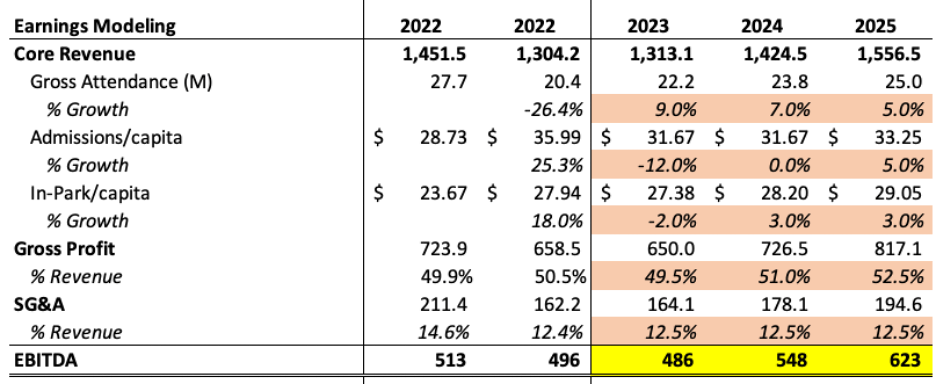

Quantifying the Attendance and Per Capita Impact at Six Flags

Six Flags' guidance for 25 million guests by 2025, combined with low single-digit growth in both admissions and in-park spending per capita supports average annual revenue growth of ~8% over the next three years. With incremental EBITDA margins in the 50%-60% range as OpEx and SG&A are leveraged over a fixed cost basis, there's a clear runway for SIX to hit $600+ million of EBITDA by the end of 2025.

{kind=link}

Management guided for $630 million of EBITDA in the proxy, compared to the Street at $560 million in 2025. Looking even further ahead, Six Flags sees a 5-year opportunity for $800+ million of annual EBITDA. As a quick sanity check, Selim Bassoul's compensation when he was brought on in 2021 was tied to hitting $710 million of EBITDA in 2025 - a target he wouldn't have agreed to if it weren't within the realm of possibility. Making just $100 million more than that over another three years isn't a monumental undertaking.

{kind=link}

But regardless, consensus numbers are just so far behind the ball, that even missing their own projection by $100 million or more would still have the NewCo's stock price appreciating meaningfully.

Impact of Attendance and Per Capita Spending at Cedar Fair

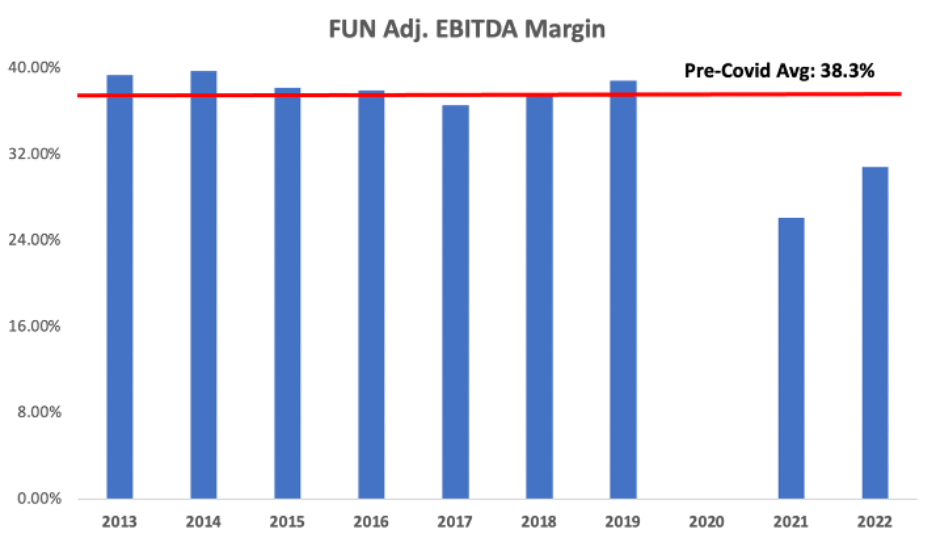

FUN is less interesting when it comes to a top-line inflection, as management wasn't out on a limb with their pricing strategy, so there's no real course-correct to benefit from. Over time, they've realized 3-4% revenue growth at 50%+ incremental margins, allowing them to compound EBITDA at 7% per year for over a decade.

Where things get interesting for FUN though is in the margin picture, as EBITDA margins are still 750 basis points below pre-Covid levels. But as is the case with Six Flags, as pricing, the cost base, and attendance normalize, EBITDA margins will inflect materially higher.

Management at FUN guided to something similar on their most recent earnings call:

First, generate higher demand levels with the goal of recapturing attendance disrupted by weather earlier in the year. And second, aggressively seize upon cost savings opportunities that don't - not only improve our near-term operating margins, but also put us on a path to return to pre-pandemic margin levels over time .

{kind=link}

While a quick search through FUN's financial statements suggest they've already returned to pre-Covid margin levels, that doesn't account for a $155 million one-time gain on a sale leaseback of one of their properties. So, on a normalized basis, there's still an incremental $130+ million margin opportunity, which is supportive of FUN's standalone goal of hitting $625 million of EBITDA by 2025.

{kind=link}

Earnings Power and Valuation

When it comes to valuation, I take a near-term and mid-term approach to assessing value, with a focus on how my models match up against consensus. Given private equity's activity in the space, I'll also go over some go-private comp multiples.

2024 Valuation Framework

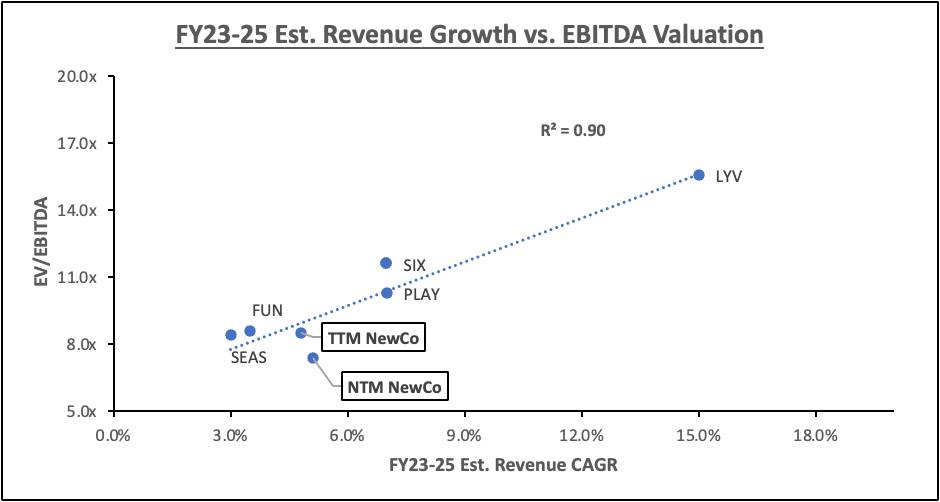

Upon completion of the merger, the NewCo will have an $8.5 billion enterprise value and $1 billion of trailing EBITDA, for an EV/EBITDA multiple of 8.5x. Compared to their peers, that kind of valuation is fairly in-line.

But, where things start to get interesting is when you go from looking at the past year, and forward into 2024, where attendance at Six Flags starts to inflect and Cedar Fair's margin picture begins to improve.

LSD revenue growth at FUN and HSD revenue growth at SIX in 2024 - figures validated by both deferred revenue analysis and FRED data - combined with 50%+ incremental margins, will drive >12% of EBITDA, leaving stakeholders with $1.15 billion next year.

So, on a forward basis, we're looking at a multiple of just 7.4x EV/EBITDA for the NewCo.

{kind=link}

Normalizing up to 9.0x - the blended multiple of SIX and FUN pre-merger and a figure consistent with growth-adjusted peer comps (see scatterplot) - supports equity upside of ~50% next year alone. And while merger costs will depress reported EBITDA as the bulk of one-time expenses flow through the income and cash flow statements next year, sell-side models will adjust to a higher base of earnings power, and the stock price should respond accordingly.

2025 Valuation & Beyond

Profitability at the NewCo should continue to grow robustly in 2025 on both an adjusted and GAAP basis, as attendance at Six Flags reaches their 25 million guest target, the first $100 million of synergies are realized, and one-time merger expenses don't repeat.

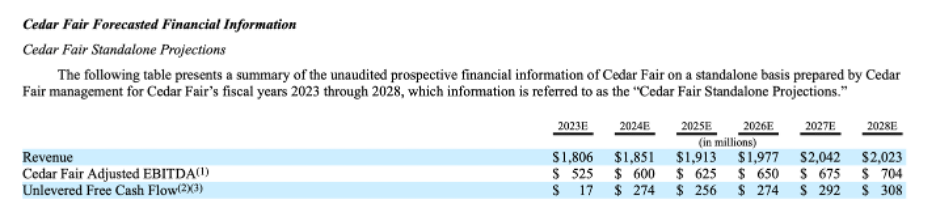

In the S-4 proxy, management at "CopperSteel," the temporary name for the new SIX and FUN company, calls for nearly $1.4 billion of EBITDA in 2025, and I'm at a similar figure in my own model. Most of the EBITDA growth is coming from SIX as they have the benefit of both HSD/MSD revenue growth in addition to 50%+ incremental EBITDA margins, whereas FUN is limited to LSD top-line growth.

Template from Alta Fox Capital; Author's own work

{kind=link}

The Street isn't fully appreciating the OpEx leverage that can be gained by SIX and FUN, hence their pre-synergy estimated EBITDA is ~$70 million lower than me in 2025.

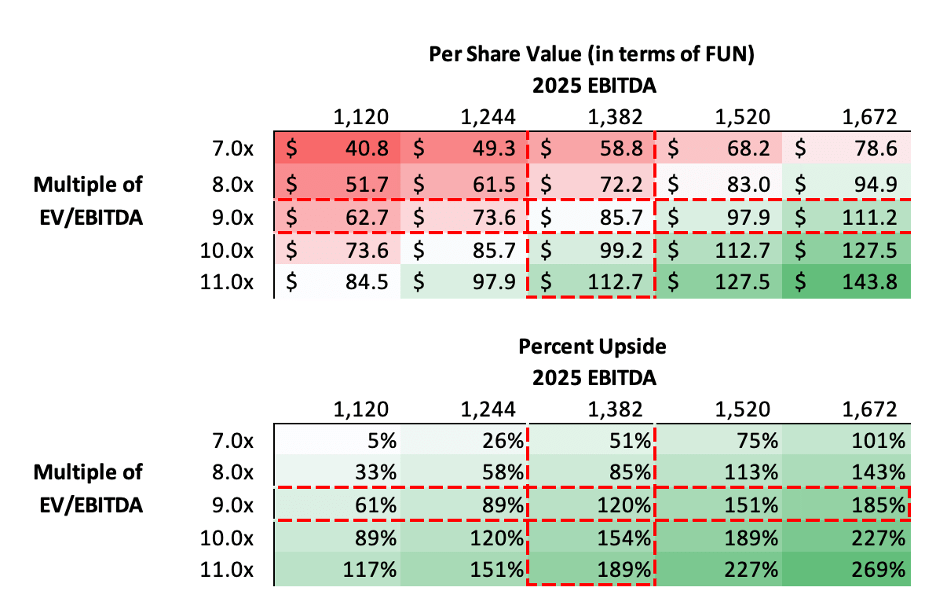

In terms of valuation, the NewCo should generate something on the order of $1.4 billion in EBITDA in 2025. At 9.0x EV/EBITDA and factoring in cash accumulating on the balance sheet, we're looking at an $85 share price (in terms of Cedar Fair), versus FUN's current price of ~$39. That's over 100% upside for both SIX and FUN shareholders from current levels over the next 24 months.

We can quibble about whether the NewCo should trade at 8.0x or 9.0x EBITDA, but even at 7.0x EV/EBITDA, we're still looking at 50% upside over two years (see sensitivity analysis table below).

{kind=link}

Crucially, even in the event of a major miss in synergy realization and attendance growth, which drives the multiple down to 7.0x and slams EBITDA growth, equity holders still make out even. In short, the classic "Heads I win; tails I don't lose much" scenario.

Go-Private Valuation

Given amusement parks' predictable cash flows and asset heavy balance sheets, which lend themselves to leverage, they tend to attract attention from private equity. And although most deals are struck at the regional level, the acquisition of Merlin PLC echoes that of the NewCo.

Merlin is a theme park operator based in the UK. In 2019, it was acquired by a consortium that included Blackstone and the LEGO founding family for $7.5 billion, or 12.5x EV/EBITDA. Merlin was facing similar headwinds to FUN and SIX at the time: attendance was down, and a lot of money needed to be invested to restore guests' trust. While its leverage was low at 1.75x EBITDA and its operations were uniquely important to some of the sponsors, a multiple anywhere near 12.5x for the NewCo would drive 200%+ returns for shareholders.

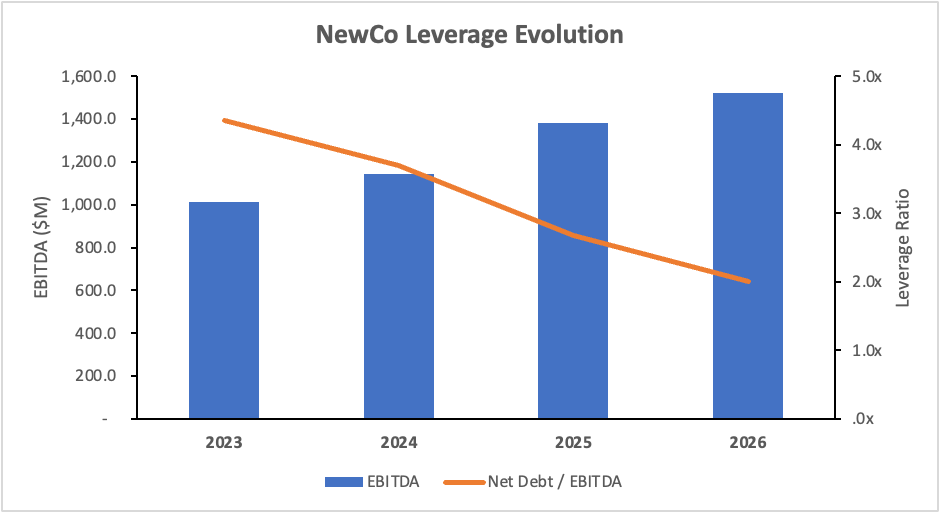

Given the leverage on the NewCo's balance sheet, an acquisition over the next two years is unlikely, though as net debt steps down to ~2.0x in 2026, something could materialize.

Implications for Leverage

As I stated at the outset, leverage at both Six Flags and Cedar Fair is immense. When the deal closes the NewCo will be leveraged to 4.4x net debt/EBITDA … but the kicker for equity investors is that at the same time as EBITDA inflects and free cash flow generation ramps, net debt to EBITDA will drop rapidly.

It may not be immediately obvious, but since the gross debt level of the NewCo will be fixed at $4.65 billion, as EBITDA increases, the effective gross debt/EBITDA multiple will drop. What's more, the NewCo is going to be generating a lot of FCF, meaning on a net (i.e., debt minus cash) basis, leverage will be dropping even faster.

Author's own work; CopperSteel Form S-4

{kind=link}

The beautiful thing about this dynamic is that it helps ensures some degree of returns for equity holders, regardless of market gyrations, since management can just shift the composition of their enterprise value to be more equity heavy as they pay down debt, effectively driving appreciation in the stock price as they do so. To illustrate the enormity of the opportunity here, for every one turn of debt management pays down, the equity appreciates 25%.

Lower leverage also has the added benefit of securing lower interest rates, as fixed income investors are willing to exchange a lower yield for less risk. Considering the blended interest rate on the NewCo's debt will be north of 7%, or $345 million/year, there's a clear path to their interest expense falling by tens of millions of dollars over the next couple years as they refinance at lower rates and pay down gross debt levels.

Risks to the Thesis and Their Implications

I would group the risks to my investment thesis into three groups: operational, financial, and regulatory.

Operational

Risks on the operational front are mostly tied to management's potential inability to execute against merger synergies, increase attendance, and drive per capita spending.

However, given that around two-thirds of merger synergies are coming from slashing corporate expenses, there shouldn't be too much risk on that front.

In my eyes, the only material risk is customers not responding to the lower prices on Six Flags and/or abandoning Cedar Fair for unknown reasons. I've already gone over a lot of data supportive of material growth in 2024 and 2025, but a recession (which looks increasingly unlikely, given the Fed's guidance for cutting rates in '24) could reduce those numbers.

Financial

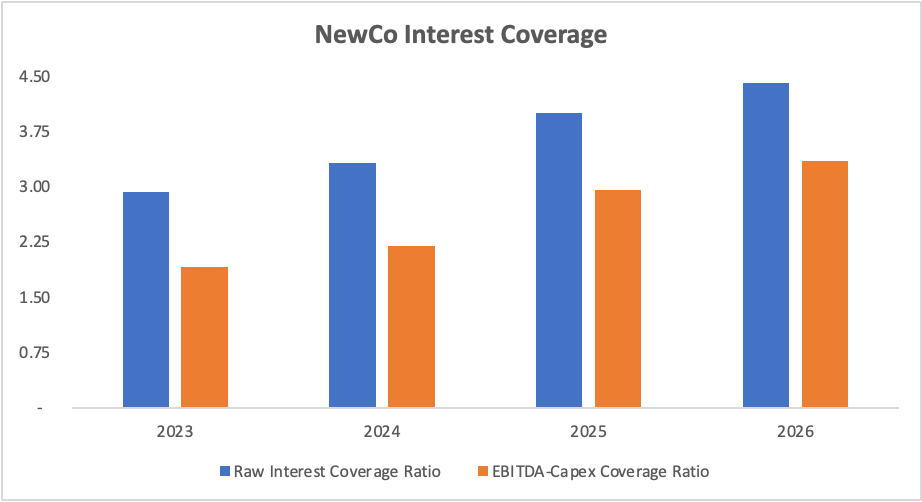

Peter Lynch once said, "It's difficult for a company with no debt to go bankrupt." On the flip side, it's easy for a company with a lot of debt to go bankrupt, and the NewCo will certainly have a lot of debt.

Leveraged 4.4x and facing $345 million a year in annual interest expense, on the face of things, debt seems like it could be an issue. However, given that EBITDA is consistently averaging north of $1 billion/yr., the trailing interest coverage ratio is at a comfortable 2.9x, and as EBITDA inflects due to the litany of factors already described, it should increase up to 4.4x by 2026.

On an EBITDA minus Capex basis, things get a bit more stressed, although even during a time of high rates and capital investment in 2023, interest coverage was still 1.93x, jumping up to 2.2x next year, and 3.35x by 2026.

Author's own work; CopperSteel Form S-4

{kind=link}

Regulatory

On the regulatory front, the Federal Trade Commissions under Lina Khan has proven quite hostile to mergers that results in the big getting bigger. Whether it be Amazon ( AMZN ) attempting to buy iRobot (IRBT), Microsoft ( MSFT ) pursuing Activision Blizzard, or Amgen ( AMGN ) going after Horizon, the FTC has been quite willing to flex its regulatory muscle.

Given the obvious implications for consumers of two gigantic amusement park operators combining, there's a chance this deal winds up in court.

Yet, even in the event of the FTC suing to block the deal, I think the merger still goes through, as given the minimal overlap between SIX and FUN's footprints, as well as the degree to which the amusement park industry is fragmented, it's difficult to craft a credible argument for serious consumer harm.

Additional Optionality

As I wrap up, I thought it worth mentioning two other levers for stock price appreciation over the medium-term.

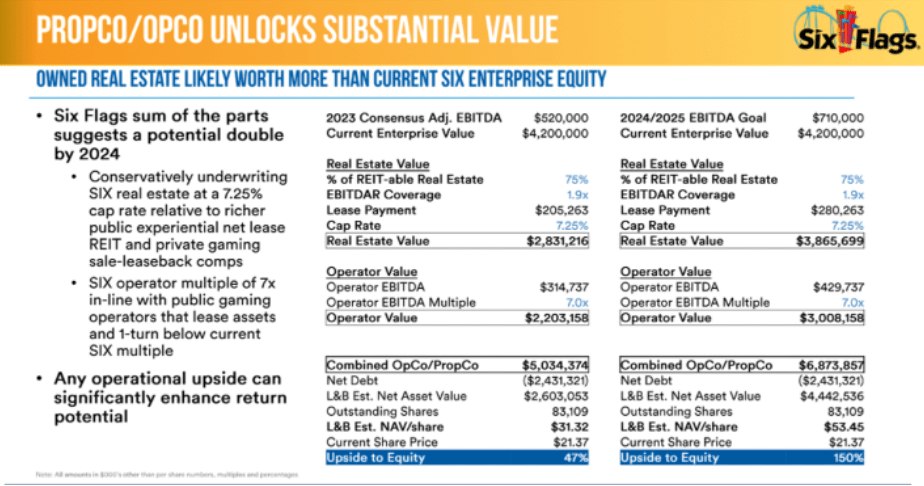

Lever #1: Six Flags Real Estate Opportunity

Six Flags owns a tremendous amount of real estate under their parks, and over the past year-and-a-half, the activist hedge fund Land & Buildings has been engaging with management about a plan to spin off their real estate.

{kind=link}

The story hasn't really changed since I last wrote about L&B's involvement, so I'll include the short excerpt I wrote last year:

The basic math behind the transaction is that if Six Flags were to spin-out the real estate they own (i.e., their theme parks and the land under them) in a REIT and lease the properties back to the operating company, paying $205 million per year as part of the deal, the newly-formed REIT would be worth $2.8 billion at a 7.25 percent cap rate (or 13.8x EBITDA).

By Land & Buildings' calculations the PropCo and OpCo would have a combined enterprise value of $5 billion and an equity value of $2.6 billion, versus SIX's current $1.9 billion market cap.

In terms of how this is relevant for the NewCo, Cedar Fair has signaled a willingness to pursue such transactions, most recently with their California's Great America amusement park, which they sold in a sale leaseback deal in 2022 for $310 million. It's plausible to see them pursuing similar transactions--possibly with some non-core assets, like marinas, campgrounds, or sports facilities--as part of their plan to deleverage and create value for shareholders.

Lever #2: Additional Synergies

This second lever for additional growth is a simpler one. On the investor call discussing the transaction, it was implied that the $120 million EBITDA synergy target is more of a starting point, and the proxy confirms this, with its goal of $200+ million of EBITDA synergies by 2027.

There is probably more upside is on the revenue . That's something we're really excited about. But as you know, that takes a little bit longer. Sometimes get to those revenue synergies, there's a lot of system integration that has to happen. So, I think that may be where there's more upside, longer term."

- Cedar Fair CFO

The opportunity to achieve synergies , which Six Flags and Cedar Fair management estimated could reach or exceed $200 million annually by 2027 .

- Form S-4

Every incremental $10 million of synergies, capitalized at 9.0x EV/EBITDA, adds $90 million to the market cap (+2%).

Takeaway

The NewCo formed by the merger of Six Flags and Cedar Fair represents one of the most attractive investment opportunities in the market today, as short-term concerns over attendance, per capita spending, and leverage dissipate with the playing out of three key catalysts.

There's a foreseeable path to 50%+ returns over the next year, advancing up to 100%+ in 2025 and beyond.

For further details see:

Six Flags And Cedar Fair: 2024 Sets Up For A Major Re-Rating