SMTC - Sizing Up Semtech Corporation

2023-11-17 10:57:36 ET

Summary

- Small cap tech concern, Semtech Corporation, has been hit by a downturn in the semiconductor cycle and an ill-timed acquisition of Sierra Wireless, resulting in violations of its net leverage credit covenants.

- The company has a new CEO, aggressive cost reduction initiatives, and signs that the semiconductor cycle may be bottoming, as well as recent insider buying in the shares.

- Semtech's stock has been down sharply, but analysts have mixed opinions on the company's future, with some optimistic about its prospects and others concerned about the acquisition and market demand.

- An analysis around Semtech Corporation follows in the paragraphs below.

It's still magic even if you know how it's done .”? Terry Pratchett.

Today, we take a look at a small-cap tech concern that has been hit by downturn in the semiconductor cycle, followed by an ill-timed acquisition of Sierra Wireless. They have combined to put the company in violation of its net leverage credit covenants twice in 2023.

However, the company has a new CEO, an aggressive cost reduction initiative, and some signs that the semiconductor cycle may be bottoming as well as some recent insider buying in the shares. The stock was down sharply in October on an announcement of a private placement of debt. An analysis follows below.

{kind=link}

Company Overview:

Semtech Corporation ( SMTC ) is a Camarillo, California-based developer of analog and mixed-signal semiconductors, as well as a provider of internet-of-things [IOT] and cloud connectivity services. These offerings are sold into the infrastructure, high-end consumer, and industrial end markets. Semtech was formed in 1960 and listed its shares on the American Stock Exchange in 1967, later switching to the NASDAQ in 1995. The stock is trading around $16.00 a share, equating to an approximate market cap of $1 billion.

The company operates on a 52- or 53-week fiscal year ((FY)) ending the last Sunday of January. For the avoidance of doubt, the 52-week period ending January 29, 2023 is FY23.

Sierra Wireless Acquisition

Semtech somewhat transformed from primarily a semiconductor manufacturer to a split after its acquisition of Canadian cellular IoT solutions provider Sierra Wireless in January 2023. For an all cash consideration of ~$1.3 billion financed primarily by debt, Semtech received a high-speed data IoT solution to complement its low-power, long-range (LoRa) wireless communication capabilities.

Reporting Segments

The onboarding of Sierra also prompted a change in the company’s reportable segments from three to four. Those units now include Signal Integrity; Advanced Protection and Sensing ((APS)); IoT System; and IoT Connected Services (IoTCS).

Signal Integrity provides integrated circuits that permit ultra-high speed point-to-point data transfer to the optical communication, broadcast television, and professional audio-visual markets. This segment generated gross profit of $52.9 million on net sales of $88.1 million in the six months ending July 30, 2023 (FY24YTD), representing significant declines of 54% and 47% (respectively) versus the prior year period. A slowdown in demand combined with a work off of cyclical inventory builds at its distributors and end users were blamed for the performance.

The same holds true for APS, which manufactures devices that protect integrated circuits from electrostatic discharge, electrical fast transients, and cable discharge events. This unit’s offerings are found in mobile and consumer products, such as smart phones, computers, TVs, routers, and automobiles. APS contributed FY24YTD gross profit of $46.5 million on net sales of $84.6 million, down 37% and 39% (respectively) from the prior year period.

IoT System includes Semtech’s LoRa devices and other radio frequency products, which are sold into industrial, medical, and communications verticals and supported by an IoT solutions suite, including modules, gateways, and routers. IoT System accounted for FY24YTD gross profit of $110.3 million on net sales of $254.0 million, up 41% and 137% (respectively) from the prior year period, owing in large measure to modules and other products added from Sierra.

The IoTCS segment was added after the Sierra deal closed. It provides device and data management, geolocation support, reporting, and alert services (amongst other) to customers who purchase its IoT System products. It was responsible for FY24YTD gross profit of $23.1 million on net sales of $48.1 million.

Operating and Share Price Performance

When Semtech began calendar 2020, its stock had been trading in a relatively tight range around $50 per share over the prior two years. FY20 net sales (ending January 26, 2020) were essentially flat versus FY17 (at $547.5 million) as the company appeared to be at the bottom of a semiconductor cycle. Then with the advent of the pandemic, customers looked to increase their inventories over concerns regarding global supply chain constraints. This dynamic continued as the economy rebounded post-pandemic, providing Semtech with a surge in business. FY21 net sales grew 9% to $595.1 million despite the challenges brought by the pandemic. FY22 net sales rose 24% to a (then) record $740.9 million while non-GAAP earnings grew 49% to $2.61.

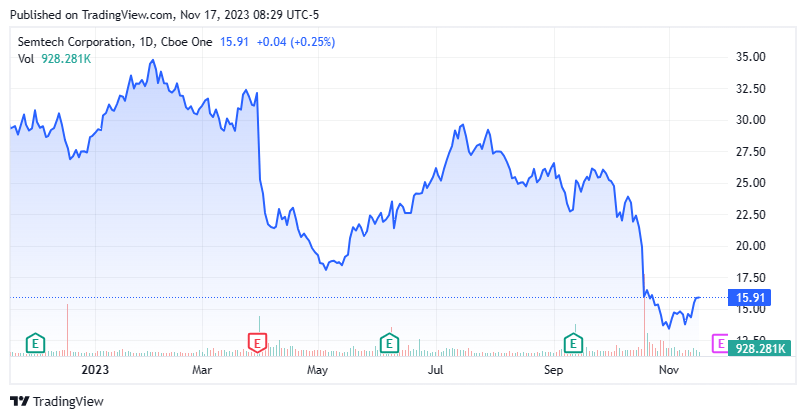

Shares of SMTC reflected these results, rallying from a March 2020 low of $26.03 to an all-time high of $94.92 in November 2021 for a market cap north of $6.0 billion and an aggressive P/E ratio (on FY22 non-GAAP earnings) of 36.4 – aggressive for a cyclical stock.

Then inflation reared its head, hurting many high P/E stocks. However, from an operational perspective, demand remained strong through 1HFY23 with non-GAAP earnings rising 43% (to $1.67 a share) on a 16% uptick in net sales (to $411.4 million). Before those earnings were reported, rumors (and then news) of the Sierra acquisition sent Semtech’s stock sliding at the onset of August 2022. Analysts did not like the deal on many fronts. It seemed to be an inopportune time to leverage its balance sheet (during a global recession) to pursue Sierra’s much lower-margin business – 35% gross margin versus legacy Semtech’s low-to-mid 60s. Analysts also questioned if the acquisition was designed to counteract a slowdown in its core semiconductor business.

They got their answer on the last day of that same month, when the company reported a slightly better than expected quarter but provided a dismal outlook for the balance of the fiscal year, citing a “deteriorating” macro demand environment. Already down 26% to $46.19 since the Sierra news, shares of SMTC cratered another 27% to $33.65 in the subsequent trading session, where they more or less remained until the company’s Q4 2023 financial report in March 2023. That release featured a 1QFY24 organic revenue outlook that was down 40% to 50% from the prior year period and the retirement announcement of 17-year CEO Mohan Maheswaran. Semtech’s stock fell 21% in the subsequent trading session. With one analyst referring to the company as a “mess” and activist investor Lion Point Capital obtaining two seats on its board of directors, shares of SMTC eventually touched a seven-year low ($17.82) in May 2023.

2QFY24 Financial Report

Matters did not improve when the company reported 2QFY24 earnings on September 13, 2023. On the surface the quarter was fine, with non-GAAP earnings of $0.11 a share besting Street consensus by $0.09 a share and net sales of $238.4 million coming in $1.0 million above expectations.

However, the outlook for 3QFY24 was abysmal, with management calling for a loss of $0.16 a share (non-GAAP) on revenue of $200 million (both based on range midpoints), citing “ high channel inventory ” and “ broader economic uncertainties. ” These forecasts were nowhere near the Street consensus, which anticipated a gain of $0.12 a share (non-GAAP) on revenue of $247.7 million.

That said, the market seemed encouraged by the sequential improvements in Signal Integrity (up 12% to $46.5 million, even though that represented a 47% year-over-year decline) and APS (up 35% sequentially and down 26% year-over-year), suggestive of a bottom in its semiconductor business. New CEO Paul Pickle stated that he believed the 3QFY24E $200 million revenue figure for the entire company represented a “ bottom. ” Also, new management’s cost reduction initiatives combined with Sierra synergies have decreased Semtech’s operating expense run rate by ~$100 million. As such, Semtech’s stock rallied 10% in the subsequent trading session to $25.18 a share, but has since returned to is pre-earnings level.

Balance Sheet & Analyst Commentary:

With the acquisition of Sierra financed by debt, the poor outlook is pressuring the company’s net leverage, which currently stands at 5.3 and is projected to spike as the company’s future comps worsen. Management has already negotiated two modifications to its leverage ratio covenants, with a current ceiling of 8.58 for the quarter ending January 31, 2024. As of July 30, 2023, the company held debt of $1.38 billion (weighted average interest rate of 6.37%) against cash and equivalents of $147.9 million with $290 million undrawn on a revolving credit facility. The company announced it is issuing aggregate principal amount of $250 million in convertible senior notes due 2028 in a private placement on October 19th. The bulk of the proceeds will be used to pay down debt from senior credit facilities.

Despite the stock being down 75% since the end of July 2023, the Street is very constructive on Semtech, featuring nine buy or outperform ratings versus three holds and a median price target of $30. Most notably, Susquehanna upgraded the company from hold to buy after its 2QFY24 financial report, stating that consensus estimates were no longer at risk. That said, Benchmark downgraded the stock from buy to hold, citing a lack of synergies with Sierra and insufficient end-market demand to support the acquisition. On average, Street soothsayers expect Semtech to lose $0.03 a share (non-GAAP) on revenue of $891 million in FY24, followed by a gain of $0.71 a share (non-GAAP) on revenue of $953 million in FY25.

Director Paul Walsh Jr. clearly believes his company’s stock is in the process of putting in a bottom based on his purchase of 20,000 shares at an average price of $24.83 on September 18, 2023. Over 25% of the outstanding shares in the stock are currently held short, it should be noted.

Verdict:

Whether a bottom is in place on shares of Semtech Corporation is unknown; however, a V-shape recovery does not appear to be in the offing. Clearly, the Sierra acquisition was ill-timed and Semtech Corporation’s net leverage is going to get worse, which may force an asset divestiture into a buyer’s market to maintain compliance. Barring an upset, this is not a situation Semtech can solve simply by growing its business, although the new CEO has done a solid job on the expense side. As such, the recommendation is to stay to the sidelines until the new CEO determines how the company will grow through subtraction.

We are stuck with technology when what we really want is just stuff that works .”? Douglas Adams.

For further details see:

Sizing Up Semtech Corporation