SPWH - Sizing Up Sportsman's Warehouse

2023-11-26 07:23:22 ET

Summary

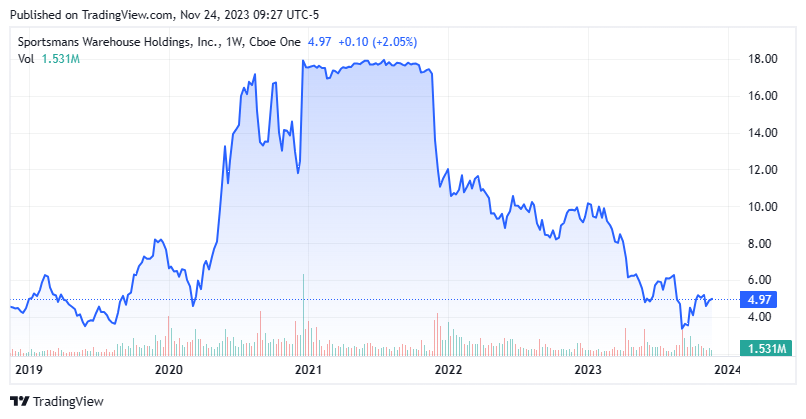

- Shares of Sportsman's Warehouse Holdings have dropped over 70% from the bid the company received in December 2020.

- The company operates 140 stores in 31 states and focuses on the sale of hunting and shooting, camping, and fishing gear.

- The recent insider buying by board members suggests confidence in the new CEO, but the company is facing challenging macroeconomic conditions.

- A full investment analysis around Sportsman's Warehouse stock follows in the paragraphs below.

The fascination of shooting as a sport depends almost wholly on whether you are at the right or wrong end of the gun .”? P.G. Wodehouse

Shares of outdoor specialty retailer Sportsman’s Warehouse Holdings ( SPWH ) are down over 70% from the $18 a share bid it received from Great Outdoors Group in December 2020, which was later nixed by the FTC. A challenging macroeconomic environment and a natural drop off in business from the significant pull though of sales courtesy of pandemic-related dynamics have played an antagonistic role. With a new CEO onboarded in September 2023, the recent insider buying warranted further investigation. An analysis/recommendation follow below.

{kind=link}

Company Overview

Sportsman’s Warehouse Holdings, Inc. is a West Jordan, Utah based outdoor sporting goods retailer focused primarily on the sale of hunting and shooting, camping, and fishing gear. The company operates 140 stores in 31 states, boasting the largest outdoor specialty store base in the Western U.S. and Alaska. It was formed in 1986 as a single location in Utah and went public in 2014, raising net proceeds of $73.3 million at $9.50 per share. The stock trades around $5.00 a share, translating to an approximate market cap of $185 million.

April Company Presentation

The company operates on a 52- or 53-week fiscal year (FY) ending on the Saturday closest to January 31st. For the avoidance of doubt, the 53-week period ending February 3, 2024 is FY23.

Sportsman’s is still a publicly traded concern after the Federal Trade Commission [FTC] interdicted an $18 per share offer by privately held Great Outdoors Group, the parent of Cabela’s and Bass Pro brands, citing anti-trust concerns in December 2021.

April Company Presentation

Disaggregation of Revenue

The company’s stores average ~38,000 sq. ft. and 24,000 SKUs, although it carries a total of ~250,000 SKUs from ~1,600 vendors out of its sole distribution warehouse in Utah. Sportsman’s strategy is to grow through opening new storefronts, with an objective of ~200 properties by January 2026. Each location is organized into six departments: Camping; Apparel; Fishing; Footwear; Hunting and Shooting; and Optics, Electronics, Accessories, and Other (OEAO).

April Company Presentation

In addition to the typical gear from manufacturers such as Coleman, Teton Sports, Honda, and Lost Creek Coolers, Camping sells canoes and kayaks and contributed FY22 (52 weeks ending January 28, 2023) sales of $174.9 million, or 12.5% of Sportsman’s total.

Apparel includes Carhartt, Columbia, and Sitka brands mainly for hunting, fishing, and hiking. The department was responsible for FY22 sales of $130.2 million, or 9% of total.

Fishing consists of gear from Johnson Outdoors, Normark, Plano, Pure Fishing, RoundRocks Fly Supply, Orvis, and Shimano. The product line accounted for FY22 sales of $124.6 million, or 9% of total.

Footwear includes work boots, technical footwear, hiking boots, sport sandals, socks, and waders from Crispi, Danner, Keen, Merrell, Red Wing, and Hey Dude. The department generated FY22 sales of $102.2 million, representing 7% of total.

By far and away the largest product line is Hunting and Shooting, which is primarily rifles, shotguns, handguns, and air guns, as well as attendant ammunition and accessories from Smith & Wesson ( SWBI ), Winchester, Federal Premium Ammunition, Hornady, Browning, and Ruger ( RGR ). This key department contributed FY22 sales of $768.3 million, or 55% of total.

OEAO consists of binoculars, rangefinders, spotting scopes, GPS devices, radios, hunting knives, lighting, and bear spray amongst other accessories. It accounted for FY22 sales of $99.4 million, or 7% of total.

In addition to branded merchandise sold throughout these departments, the company sells private labels and special make-up offerings, which accounted for less than 6% of its FY22 sales, significantly lower than the 20+% share achieved by many of its sporting goods retail peers.

Market and Marketplace

With Hunting and Shooting outdistancing its other departments by at a factor of four, it isn’t surprising to know that the majority of the company’s customer base are middle-class males, between the ages of 35 and 65. That said, approximately one-third of first-time firearms purchases in 2021 were made by women.

The industry in which Sportsman’s competes is fragmented with nearly two-thirds of the $70 billion in FY21 sales conducted by ~50,000 mom and pop shops. The balance is split pretty evenly between national and regional specialty stores. In Hunting and Shooting, ~92% of all federal firearm licenses (~46,700 of ~51,000) are held by small independent retailers. Management believes this disjointed marketplace dynamic provides it an opportunity to expand market share, as its large selection of complementary merchandise at competitive prices affords it an advantage over smaller shops.

Prior Operational and Share Price Performance

That said, the entire vertical benefitted substantially from the pandemic and Sportsman’s was a case-in-point. The company’s sales grew at a 5.8% CAGR from FY15 to FY19 (ending February 1, 2020), and that ‘growth’ was a function of new store openings, which increased at a 12.6% CAGR over the same period from 64 to 103. Post-lockdown, Americans flocked to the outdoors and Sportsman’s top line soared 64% to $1.45 billion with the store count only increasing by nine to 112. That performance attracted investors, who rallied shares of SPWH from a pandemic low of $4.08 to an all-time high of $18.46 in September 2020. After a swift pullback to the $11-$12 range, the company received an $18 per share bid from Great Outdoors Group in December 2020, representing a seemingly cheap bid based on a price-to-FY20 (ending January 30, 2021) sales multiple of 0.54 and a PE on FY20 non-GAAP EPS of 8.1. Further adding to the perception of Great Outdoors obtaining a bargain: Sportsman’s balance sheet was in solid shape with debt (at that time) of only $57.5 million. Even if one were to apply the (then) $228.3 million of lease liabilities to the company’s enterprise value, Great Outdoors was paying and EV/TTM FY20 Adj. EBITDA of 6.6.

While the FTC was assessing the impact this deal would have on the competitive landscape, Sportsman’s top-line momentum slowed to 4% growth in FY21, while non-GAAP EPS fell from $2.23 to $1.72. That deceleration became a concern to the market when the FTC essentially ended the merger by stating it was protecting the consumer from higher prices and was unlikely to clear the deal. As a constellation prize, Sportsman’s received a $55 million termination payment from Great Outdoors equal to $1.26 a share (at that time), which it earmarked to pay off its entire debt.

News of this decision cratered shares of SPWH 20% in the subsequent trading session to $13.61, which would be their highest close from that point forward. Non-GAAP FY22 EPS would fall 41% to $1.02 on a 7% decline in sales to $1.40 billion (despite a 6% increase in square footage after opening another nine locations) as freight inflation and an end to federal stimulus both played significant roles in the poor performance.

2QFY23 Financials

The first two stanzas of FY23 were more of the same with the company losing $0.44 a share (non-GAAP) on a 13% decline in net sales despite nine more stores opening. This revelation came to light when Sportsman’s reported its 2QFY23 financials on September 6, 2023, posting a loss of $0.04 per share (non-GAAP) and Adj. EBITDA of $13.1 million on net sales of $309.5 million versus a gain of $0.36 per share (non-GAAP) and Adj. EBITDA of $30.6 million on net sales of $351.0 million in 2QFY22, representing declines of 111%, 57%, and 12%, respectively. Poor macro conditions leading to lower consumer discretionary spending were blamed.

To mitigate these impacts, the company has been reducing costs commensurate with recent foot traffic at its locations and expects to realize $25 million in annual expense savings. Still, the company – which had been without a permanent CEO since six-year leader Jon Barker abruptly resigned in April 2023 – anticipated losing $0.13 a share in 3QFY23 on net sales of $320 million, marking a 17% decline at its top line. This ugly forecast sent shares of SPWH to an all-time intraday low of $2.98 in the subsequent trading session. (A more ‘permanent’ CEO, Paul Stone, was installed on September 26, 2023.)

Balance Sheet & Analyst Commentary

Furthermore, poor performance and expanding lease obligations over the past 18 plus months have compelled management to onboard debt of $203.1 million as of July 29, 2023. That said, some of those funds were earmarked to repurchase shares of SPWH on the way down. In total, 7.33 million shares (worth $67.5 million) have been bought back since March 2022, leaving $7.5 million on the board authorization. At the close of 2QFY23, the company held cash of $2.9 million, putting net leverage at 3.05 – a figure likely to rise as the fiscal year progresses.

With performance deteriorating, Street analysts are split down the middle, featuring two buys against two holds and a mean price target of $6.00. On average, they expect Sportsman’s to lose $0.53 a share (non-GAAP) on net sales of $1.27 billion in FY23, followed by a gain of $0.10 a share (non-GAAP) on net sales of $1.31 billion in FY24.

Since the installation of CEO Paul Stone, three board members have been buyers of the company’s stock. Specifically, directors Richard McBee (22,413 shares at an average price of $4.05), Gregory Hickey (5,000 shares at $4.04), and Steven Sanson (40,000 shares at $4.57) have all issued votes of confidence in new management.

Verdict

Board members’ temerity notwithstanding, Sportsman’s is another example of a retailer fighting significant macroeconomic headwinds and the pull-through of a significant amount of business due to pandemic-related dynamics. On an EV/TTM Adj. EBITDA basis, its stock is not outrageous at just north of 5 (just over 9 factoring in lease obligations), but that metric is going to get worse before it gets better. With a new CEO only two months at the helm, the future direction of the company is unknown. As such, the recommendation is to adopt a wait-and-see approach on Sportsman’s.

The search for a scapegoat is the easiest of all hunting expeditions .”? Dwight D. Eisenhower

For further details see:

Sizing Up Sportsman's Warehouse