PDI - SJNK And SHYG: 8% Yields With Low Duration Risk

2023-03-07 08:00:00 ET

Summary

- We last covered SJNK and SHYG in an era of return free risk.

- Things have changed as the Federal Reserve went from complete complacency to utter panic on inflation.

- The two funds offer an 8% yield today.

- We look at their characteristics and provide our opinion.

It's been two years since we wrote about SPDR Barclays Capital Short Term High Yield Bond ETF ( SJNK ). We had compared it to another junk bond fund, iShares 0-5 Year High Yield Corporate Bond ETF ( SHYG ). While the two had more similarities than differences, we gave a slight edge to SHYG due to its lower average portfolio maturity by a year. The ride has been bumpy since then, but the end result has been virtually no change for the investors on both sides.

While the performance of the two funds does not reflect it, the macro environment has undergone a radical change in the last couple of years. For starters the ZIRP is a thing of lore and the risk free rates are closer to 5%.

Back then we were witnessing historically low price differences between the B rated and CCC rated bonds, a typical sign of high complacency. The spread went as high as 6.4% in the ensuing period, though it has dialed back a bit recently.

We revisit our protagonists in light of the current environment and provide our outlook next.

Fund Overview

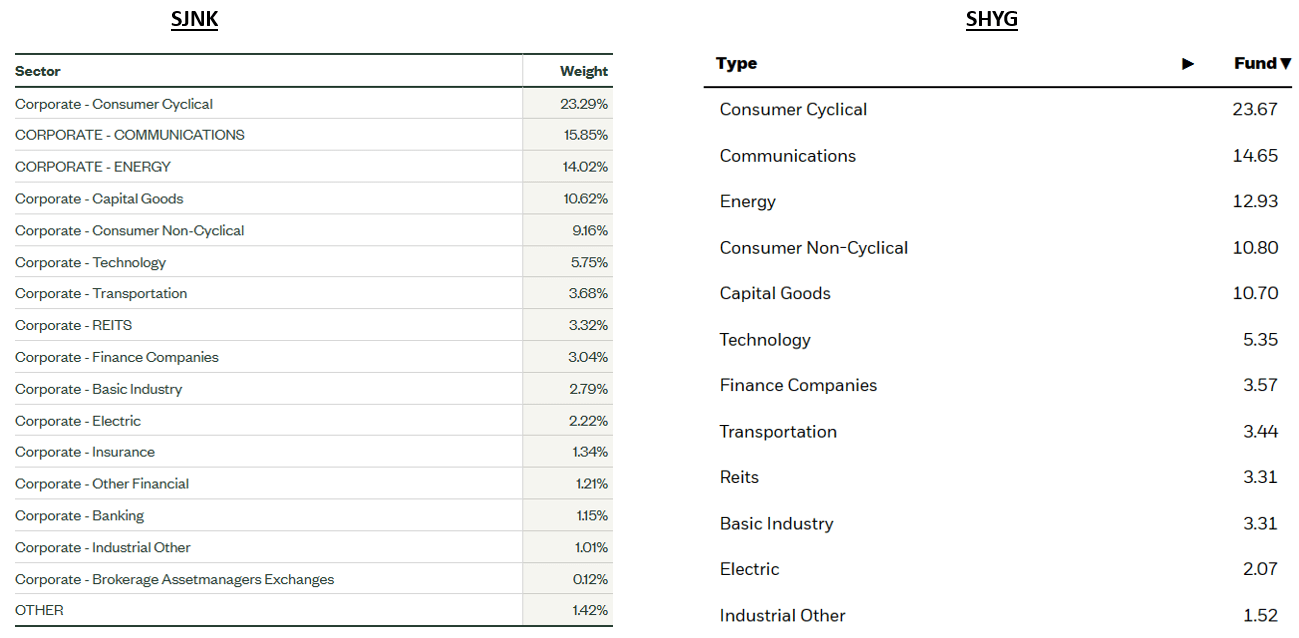

Both the ETFs aim to provide exposure to corporate high yield securities. They control the interest rate risk by going in for shorter duration investments. While being a dynamic number, SJNK had 827 holdings to 800 of SHYG at last count. SJNK benchmarks to the Bloomberg US High Yield 350mn Cash Pay 0-5 Yr 2% Capped Index whereas SHYG the Markit iBoxx USD Liquid High Yield 0-5 Index. Being passive ETFs, both the funds have similar sector concentrations owing to the similarities in their respective benchmarks.

Compiled from the ETF websites

{kind=link}

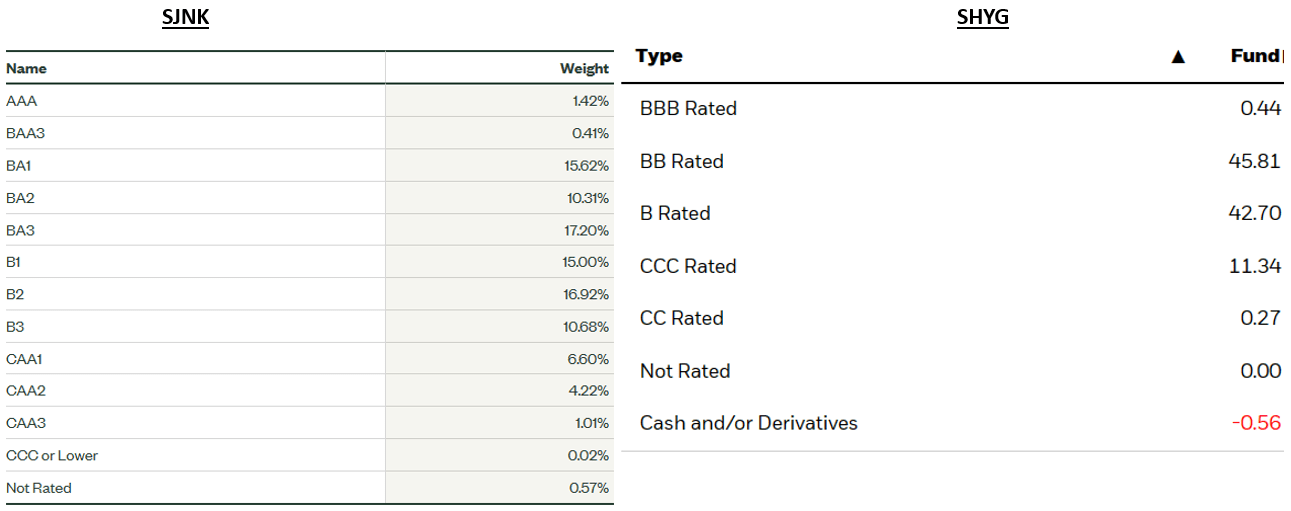

As their name suggests, both the ETFs are primarily comprised of speculative securities.

Compiled from the ETF websites

{kind=link}

Speculative holdings bring with them a dollop of credit risk i.e. the risk that the issuer will not be able to repay the principal on maturity. This risk increases with each rung lower in ratings, which in SJNK's case starts from BA1 and SHYG's case starts from BB rated holdings in the above picture. The ratings shown above for the two come from different sources, Moody's for SJNK and S&P for SHYG. Both funds have close to 50% of their holdings just one rung below investment grade, which bodes relatively well for their unitholders.

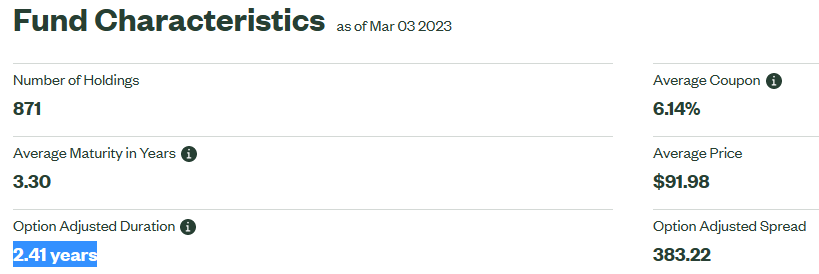

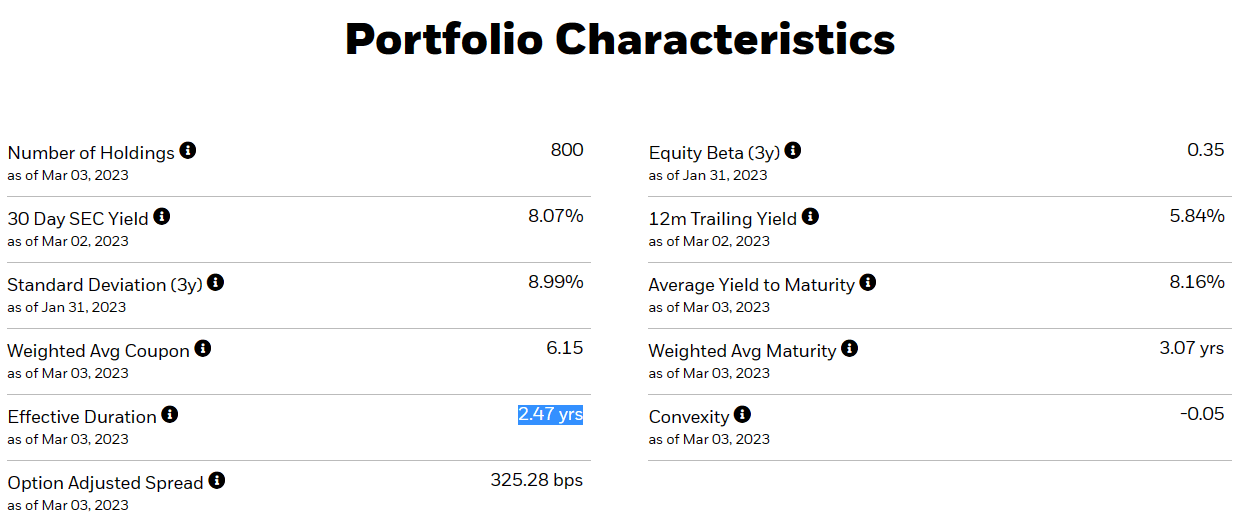

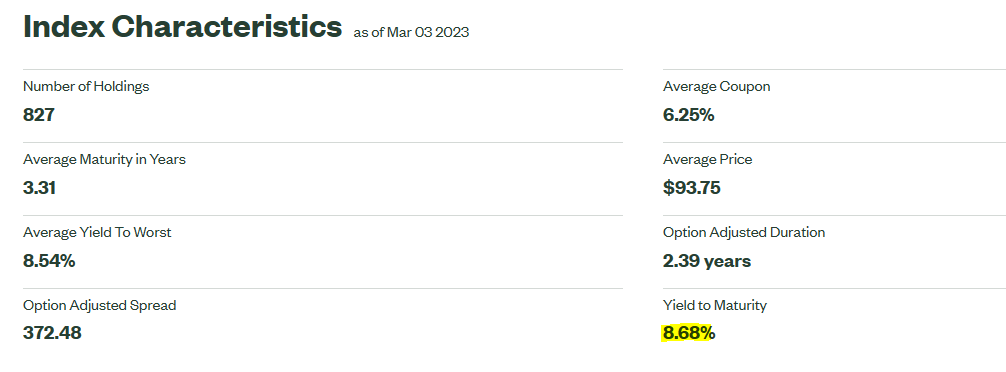

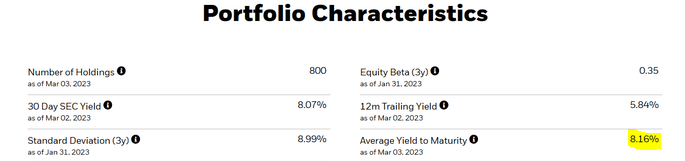

The SJNK portfolio has an average maturity of 3.31 years, closely followed by SHYG at 3.07 years. While we could not locate the current breakdown on the latter's website , we can safely infer that the 800 holdings would be concentrated in a similar fashion to SJNK's due to closeness in average maturities.

SJNK website

The portfolio duration, which is a measure of its interest rate sensitivity, comes in at 2.41 years for SJNK and 2.47 years for SHYG as per data published for March 3.

{kind=link}

{kind=link}

This broadly indicates the extent to which the respective portfolio values will change with a corresponding movement in interest rates. These are very small numbers for both funds and they are taking very little interest rate risk.

Performance

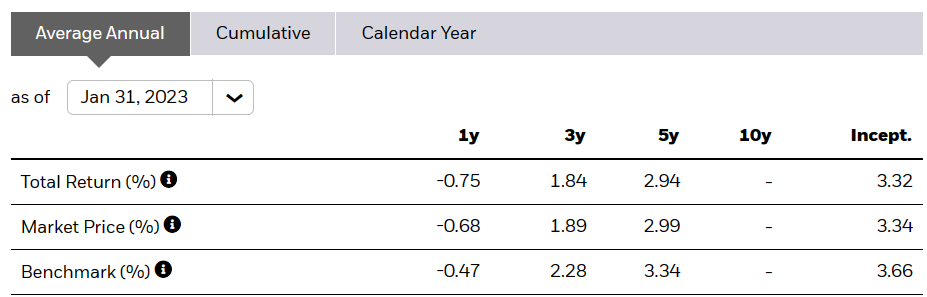

SJNK has kept up with its benchmark index, even outperforming it in some timeframes. This is impressive considering the ETF's performance is net of expenses (annual 0.40%) unlike the index.

{kind=link}

While SHYG has not outperformed its benchmark in any timeframe, it has kept up with it considering its 0.30% in annual expenses.

{kind=link}

Yield

SJNK offers a yield of 8.21% to its investors, as opposed to the 8.07% from SHYG (noted in the "Portfolio Characteristics" snapshot above).

SJNK website

The 30 Day SEC Yield reflects the annualized proportion of investment income earned by a fund in the preceding 30 days to the prevailing price at the time of calculation. Based on the most recent $0.154239 monthly distribution, SJNK provides a 7.5% yield to its unitholders. Whereas SHYG with its corresponding $0.228707 payment, yields 6.7%. With both their 30 Day SEC yields higher than their current distribution, they have room to increase their monthly payouts. A related yield investors should watch is the yield to maturity. Interestingly, the yield to maturity is 8.68% for SJNK.

{kind=link}

This is a little bit higher than what we see for SHYG.

{kind=link}

The bottom line here is that you can expect an approximate 8% yield over the next 1 year.

Conclusion

We are in the camp that thinks we have still some ways to go before the Federal Reserve hits pause on rate hikes. That should create a small pricing risk for these bonds as they are of very short maturity. So we stand by the title, that the duration risk is negligible.

The bigger risk (and this is way bigger) though is the "spread" which we think can really widen in the upcoming recession.

Morgan Stanley-Twitter

Currently, it is all "rainbows and butterflies" for the market. This has been driven by some stronger recent data points that have convinced investors that this time is different. It never is. The recession is coming and while the exact time can be debated, one has to be very careful with credit risk at this point. So on an absolute basis we would avoid these two funds. On a relative basis, yes, these have their merits versus longer duration high yield bond funds like SPDR Bloomberg Barclays High Yield Bond ETF ( JNK ) or even CLO equity focused funds like Eagle Point Credit Company Inc. ( ECC ). We even prefer them over leveraged closed end high yield funds like PIMCO Corporate & Income Opportunity Fund ( PTY ) and PIMCO Dynamic Income Fund (NYSE: PDI ), which are trading at massive undeserved premiums to NAV . Here you will have the trifecta of leverage, credit and duration risks. So SJNK and SHYG are better than a lot of choices today, but we are not sold to move in at this point. We are watching for opportunities in this high-yield space but believe that they will only come when SPX breaks 3,200.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

SJNK And SHYG: 8% Yields With Low Duration Risk