SKM - SK Telecom Q3 Earnings: Core Business Still Struggling

2023-11-20 13:33:51 ET

Summary

- Q3 earnings for SK Telecom beat analyst expectations with a 1.4% increase in revenue and a 7% increase in operating income.

- The company is heavily focused on AI, with plans to transform into an AI company by 2028 and generate $18.5 billion in AI revenue.

- The core telecom business is struggling, with declining ARPU and subscribers, posing risks to the company's growth and profitability.

- I rate the stock a hold as without AI in the financials or a clear plan from management on the telecom business, it's hard to tell which way this swings.

I'm revisiting my Q1 thesis on SK Telecom (SKM) in light of Q3 earnings which were released on Nov. 8.

Looking back on my Q1 analysis, I rated SK Telecom a hold. My recommendation was based primarily on the core telecom business lagging the overall South Korean market, while management focused on an AI and metaverse business that had yet to drive profitability. While I saw favorable valuation multiples and upside potential if management delivered on the " AI is Everywhere " strategy, declining ARPU and subscribers put cash flow and the dividend at risk.

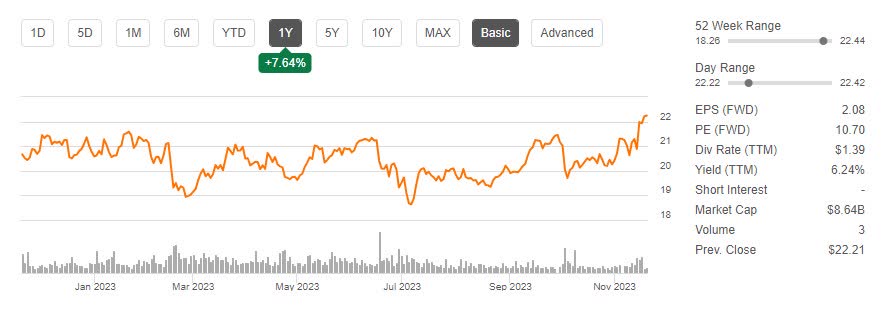

Since my last analysis, SKM is up more than 11% (and 7% across the past year), largely from a run-up following Q3 earnings. Investors responded favorably to a revenue surprise as well as concrete details around the launch of AI products and the strategy through 2028.

{kind=link}

Despite earnings, I continue to rate SK Telecom a hold and feel that risk and reward are balanced. On the downside, the core business seems to be struggling across the board, and management hasn't indicated a plan to right the ship. On the upside, a breakout AI product could catapult the business to new heights. Without AI in the financials or a clear plan from management on the telecom business, it's hard to tell which way this swings.

Key Takeaways From Q3 Earnings

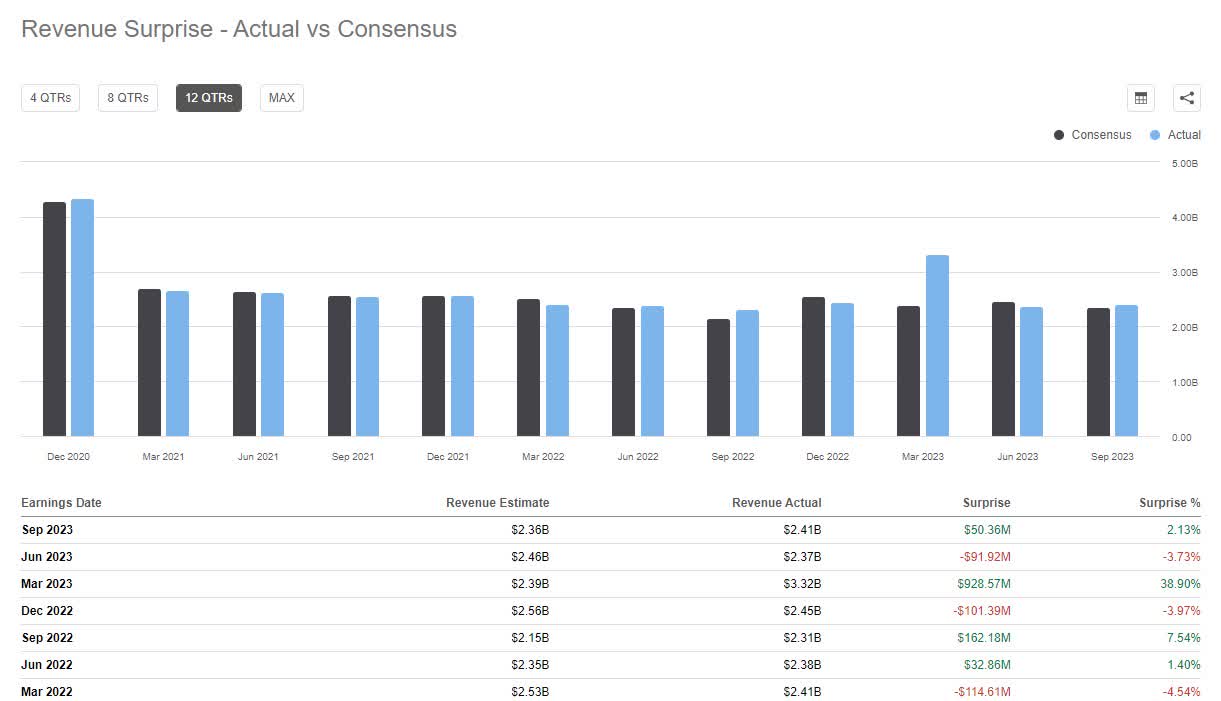

While EPS consensus is not available, revenue of $2.41 billion for the quarter beat analyst expectations by $50 million or 2%.

{kind=link}

Revenue was up just a hair year-over-year at 1.4%. Favorable operating income was up 7%

Q3 Income Statement (SKM Investor Relations)

Digging into the variance explanations, I feel the results become less impressive. SKT revenue upside year-over-year was driven by roaming growth, which is low margin . The quarter-over-quarter upside was driven by handsets, which also are low margin. The benefit to operating income was driven by cost efficiency, not anything favorable happening in the business or to product margin.

Management spent the earnings call focused on AI, with roughly 90% of the prepared remarks on AI and the core business just a footnote. A few interesting points:

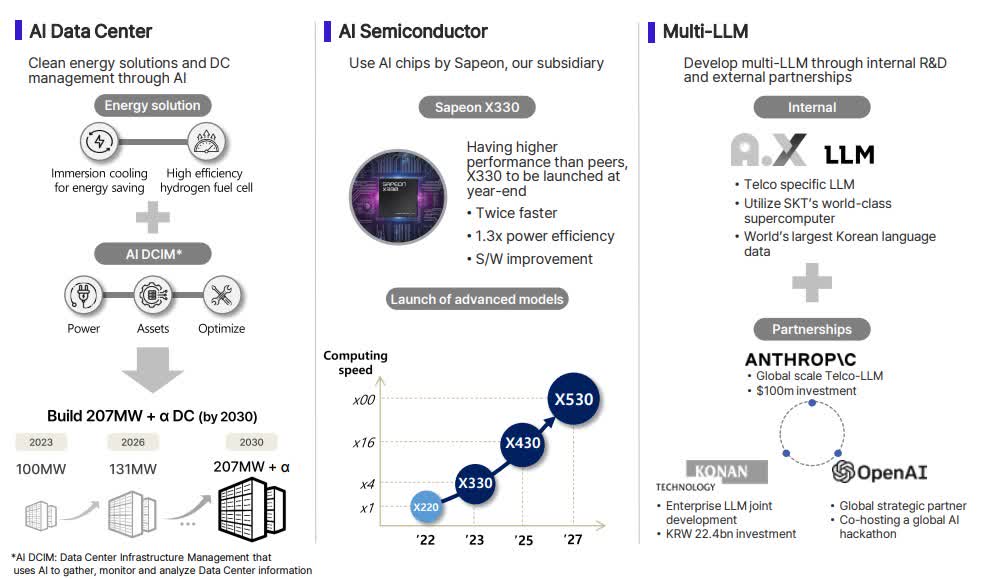

- Sapeon, SKM's AI semiconductor company, will launch an AI chip by the end of the year

- AI data centers are seeing a 30% increase in demand

- SKM's broadband TV will become an AI TV service

- SKM signed a collaboration agreement with Joby Aviation to focus on AI mobility

- SKM will use AI for marketing and to improve cost efficiency

- Share buybacks continue to be underway and on schedule

- AI contribution to revenue is only 9%, with a goal of 36% by 2028

- The fourth quarter may be challenged with higher seasonal expenses

- 66% of handset subscribers are on 5G

- Roaming is the main growth driver for telecom at this point

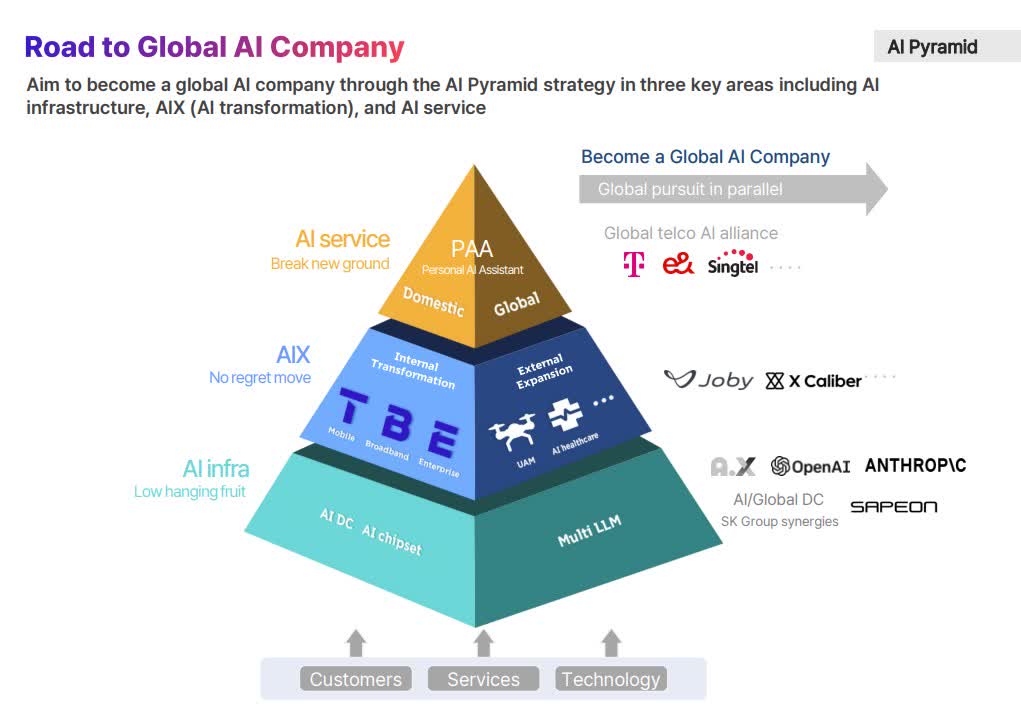

AI Business Is Coming Into Focus

The Q3 earnings release was heavy on details about AI. Most importantly, the AI pyramid, which is how SK Telecom plans to grow.

{kind=link}

Management's stated goal is to transform the company from a telecom company into an AI company by 2028 with $18.5 billion in AI revenue. So I wanted to take a look at what AI initiatives had high-monetization potential versus low.

High Potential

- AI data center provider for AI companies

- AI semiconductor provider with advanced computing speed

- Customized LLMs for enterprise customers

- AI diagnostics for healthcare

{kind=link}

Lower Potential

- AI services as part of mobile and cable packages

- AI shopping offering

- AI assistant

In my opinion, the challenge is that management discusses both the high potential and low potential offerings as equal. They received almost identical coverage in the Q3 earnings call and presentation. To truly drive growth, the focus should be on monetization above all else. That said, the high-potential items, if executed well, could truly be transformative.

Risks Remain On The Way To 2028

While there's great potential from AI, the business has to be strong enough to support AI investment. Going back to the earnings comment that AI is 9% today with a goal of 36% by 2028 and the 2028 revenue goal is $18.5 billion, that implies the rest of the business has to drive $33 billion in revenue or 240% more than it does today.

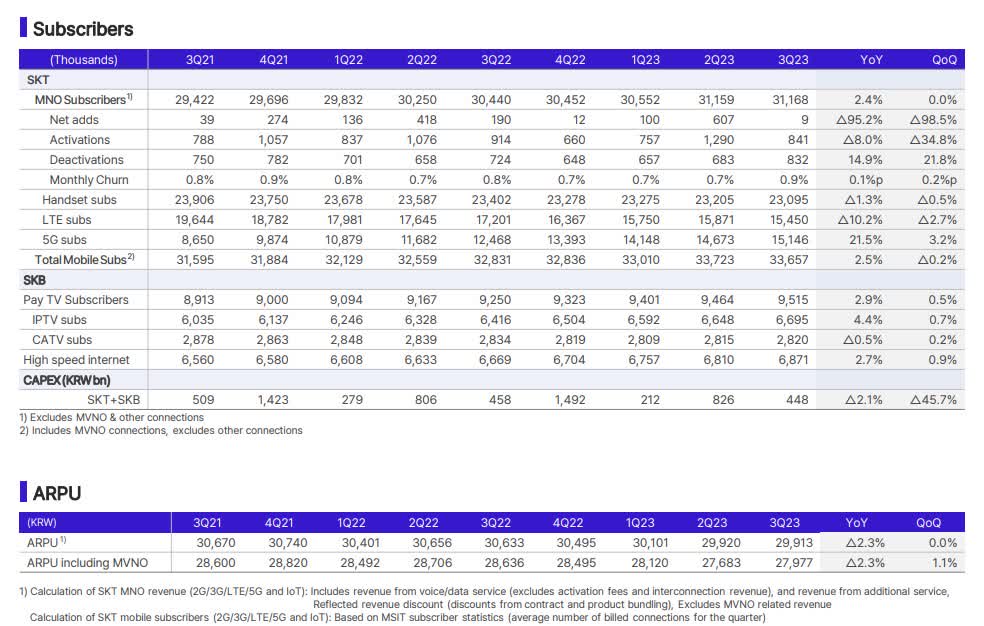

Across nearly every measure, the core business is struggling to grow. In Q3, handset subscribers were down, LTE sub declines more than offset growth in 5G subs, churn was the highest it has been since 2021, and ARPU declined materially.

{kind=link}

5G growth is slowing as the industry matures and 66% of their subscribers already are on the service, limiting opportunities for further ARPU growth.

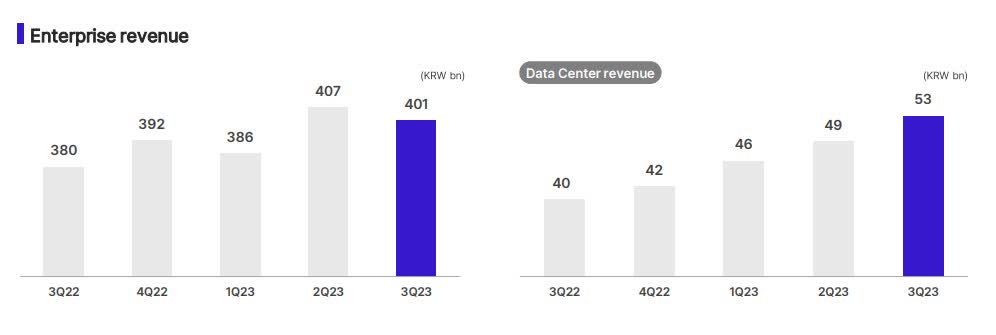

Even more concerning, high-profit enterprise revenue declined substantially despite growth in data centers from AI.

{kind=link}

And again, management spent limited time discussing this aspect of the business, leading me to believe there isn't a plan.

Pricing Signals Mixed

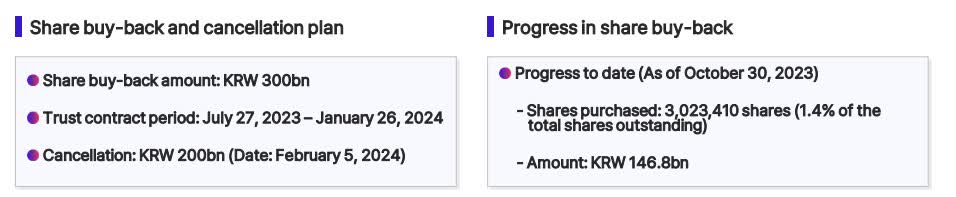

In addition to the AI upside, core business downside, pricing signals are mixed. Management is in the midst of an aggressive share buyback plan which signals underpriced shares.

{kind=link}

On a similar note, valuation multiples are very favorable and my fellow SA analysts as well as Wall Street analysts have issued buy ratings.

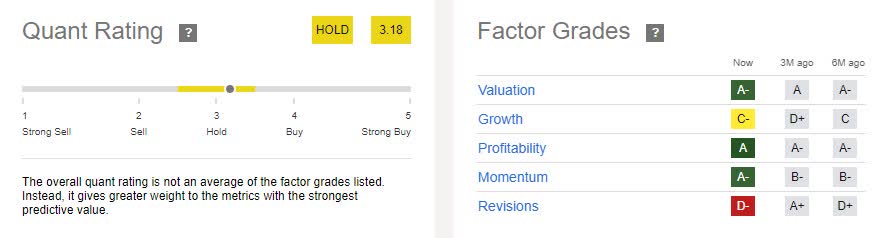

SKM Ratings (Seeking Alpha)

However, I agree with the quant rating because growth is the primary concern. And not only is growth challenged, but expectations keep being revised downward.

{kind=link}

Verdict

Based on Q3 earnings, I believe that while the AI investment shows potential, the core business grapples with growth challenges. While impressive, the target of achieving 36% revenue from AI by 2028 puts a significant burden on the rest of the business.

The third quarter revealed that key metrics such as handset subscribers and ARPU are dipping, and LTE sub declines, outpacing growth in 5G subscribers. Despite the maturing industry, 5G growth also is slowing, with 66% of subscribers already on the service, posing a constraint on future ARPU growth. It's concerning to note that the high-profit enterprise revenue saw a decline despite growth in data centers from AI.

Regarding the company's pricing, signals are mixed. The ongoing aggressive share buyback plan might indicate underpriced shares and favorable valuation multiples have led to buy ratings from many analysts. However, concerns about growth persist, especially with downward revisions in growth expectations.

Given these considerations, my recommendation for now is a Hold rating. While the company's AI ambitions show promise, the challenges in the core business and mixed pricing signals suggest a cautious approach for the time being.

This article represents my personal opinion and does not constitute financial, legal, or tax advice. Please consult a licensed advisor prior to making investment decisions.

For further details see:

SK Telecom Q3 Earnings: Core Business Still Struggling