SKM - SK Telecom Seems To Be Losing Focus On Its Core Business

2023-07-28 18:47:03 ET

Summary

- SK Telecom is bullish on AI and the Metaverse, aiming to become a global leader in these sectors.

- The company's core telecom business is lagging behind the mature South Korean market, with slow growth and declining ARPU.

- Despite the potential of new business, the downside risk of the core business faltering offsets the upside benefit of AI and the Metaverse in my opinion.

SK Telecom Co., Ltd. ( SKM ) is a leading South Korean wireless telecommunications operator and is part of the SK Group, one of the country's largest chaebols. The company provides various telecommunication services, including cellular voice, wireless data, and wireless internet.

The stock is down nearly 12% over the past year, pushing the dividend yield above 5% and depressing valuation multiples. On the surface, an investment in SK Telecom looks compelling, especially with management bullish on the AI and Metaverse business. However, the core telecom business is lagging behind the mature South Korean market, while 5G and the new AI and Metaverse businesses aren't driving revenue yet. I rate this stock a hold and believe the upside potential from new business is offset by risks to cash flow and profitability from the core business.

Management Bullish On AI And Metaverse

SK Telecom is making significant strides in Artificial Intelligence and the Metaverse. The company has a clear and ambitious vision for these innovative sectors, aiming to become a leading player on the global stage.

The company's CEO, Ryu Young-sang, recently unveiled an " AI to Everywhere " strategy. This strategic direction signifies SK Telecom's commitment to integrating AI across all aspects of its business operations and services. By placing AI at the core of its business, SK Telecom intends to rapidly transform into an AI-centric company , driving innovation in various areas.

In collaboration with AWS , the company is co-developing a set of computer vision services, combining SK Telecom's AI models trained over a decade. It appears management believes this partnership reflects their commitment to leveraging AI to enhance their offerings and create customer value.

Moreover, SK Telecom has also shown a keen interest in the burgeoning Metaverse industry. The company is actively expanding the Mixed Reality (MR) ecosystem with partners both domestically and internationally, developing new technologies in Augmented Reality ((AR)) and Virtual Reality ((VR)) sectors. Their metaverse platform has already seen early success, recording significant uptake in user engagement .

Management seems extremely enthusiastic about the future of this business. The telecom business received one paragraph of coverage in the Q1 2023 press release , while AI and Metaverse had an entire page. The earnings call had a similar vibe, as the CFO quickly covered the telecom business and then launched into a discussion of how the company would "transform and leap forward into an AI company."

I agree that there is significant potential in SK Telecom's strategic pivot. However, the results of this business are not showing up in the financial performance. The earnings call was heavy on stats and partnerships, but not one call out for financial performance. In a similar fashion, the earnings presentation presented a three-page business update on AI and Metaverse with stats but no financials. Neither AI nor metaverse are broken out in the financial results. SK's Telecom business breaks out revenue into MNO (Mobile Network Operator) and Other, where the new business sits. Other only grew from 14.9% of the business in 2022 to 15.7% in 2023.

I believe there is upside potential in the future, but SK Telecom needs a strong core business to drive profitability and cash flow. Until the impact of the AI and Metaverse business starts showing in the financials, I am nervous to estimate the upside.

Core Business Is Lagging The Market

According to the 2023 Telecoms Market Report , South Korea has the second most mature telecom market in the world and is a leader in the 5G race, with 30% of customers already converted. With a mature telecom industry, Mordor Intelligence estimates South Korean telecom will grow at a 3.23% CAGR from 2023-2028.

The problem is that SK's Telecom business lags behind the overall market. The MNO business only grew at 1.5% year-over-year.

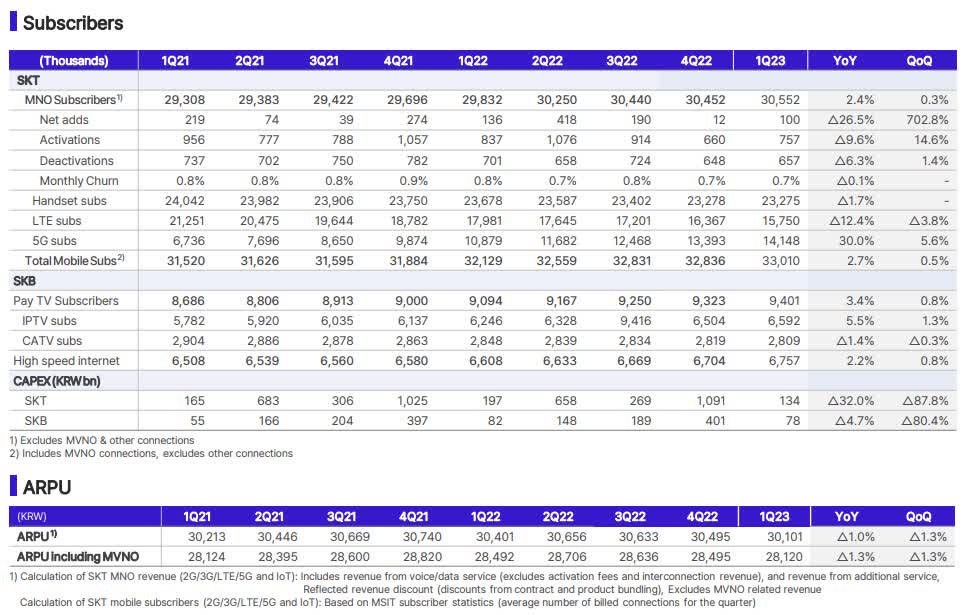

SKM Q1 2023 Financials (SKM Investor Relations)

Regarding rate/volume, subscribers grew 2.7% year-over-year from 32 million to 33 million, but ARPU went backward 1% from 30,401 to 30,101. I believe SK Telecom is struggling to maintain market share without aggressive discounting. This also signals that they have not been able to significantly monetize 5G service, despite a 30% increase in 5G subscribers.

{kind=link}

The ARPU decline presents an issue with the long-term viability of the business, especially with inflation in South Korea running above 5% throughout 2022. As discussed above, Telecom is still 84% of the business and critical to cash flow while the AI and metaverse business spins up. I am concerned that management has turned attention away from the core, and SK Telecom will continue to lose market share and ARPU before the AI and metaverse business drives profitability.

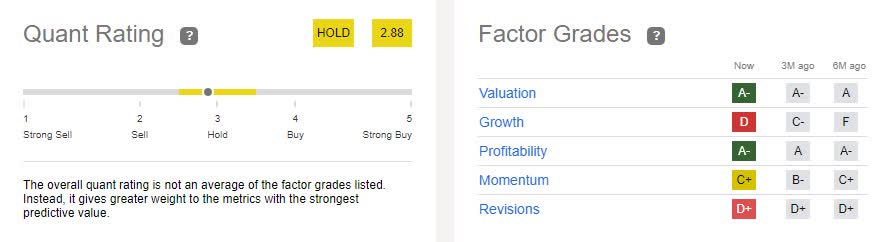

Quant Rating Has It Right

SKM is down nearly 13% over the past year. In addition, valuation multiples are signaling a low valuation. For example, EV/Sales of 1.20 is down 36% to the sector and 13% to the 5-year average. On the profitability side, EV/EBITDA is 4.17, down 57% to the sector and 16% down to the historical average.

Despite the favorable multiples, I believe the quant rating gets it right in recommending a hold.

{kind=link}

As discussed above, growth has stagnated, and SK Telecom is falling behind the market. Revenue and Free Cash Flow earn an F and a D, respectively, driven by the ARPU decline and putting the dividend at risk over the long term. EPS revisions also weigh the quant rating, as excitement over AI is tempered by the reality of declining ARPU and challenged subscriber growth.

While there is certainly upside potential from new business, I would need to see ARPU recover and the telecom business's growth catches up to the industry to switch my recommendation from hold to buy. In my opinion, the downside risk of the core business continuing to falter offsets the upside benefit of AI and Metaverse.

Verdict

SK Telecom, despite its impressive strides in artificial intelligence and metaverse, appears to be faltering in its primary telecom business, which currently accounts for 84% of its operations. Market share and Average ARPU are declining, which raises concerns about the company's long-term profitability and the focus shift away from the core telecom business. I rate this stock a hold as the upside benefit from new business is offset by the downside risk of worrisome trends in both rate and volume for the core telecom business.

For further details see:

SK Telecom Seems To Be Losing Focus On Its Core Business