SKSBF - Skanska: At The Right Price I'm A 'Buy' Here

2023-08-12 03:28:31 ET

Summary

- Skanska is a cyclical construction company that has provided double-digit returns in the past, making it an attractive investment opportunity.

- The company has a strong construction segment with solid operating margins and a positive financial position.

- Challenges for Skanska include low sales volume in residential properties and a halt in property investments, but the company has a record high order backlog and profitable projects.

Dear readers/followers,

Skanska (SKSBF) is a company I've owned off and on for a few years - really since I started investing. This is owed to my knowledge of the business, where I believe that I know well the levels where this cyclical construction company becomes a "BUY". I also know, however, when it's time to call it a "HOLD" and when to trim out of the position and take profits.

I've done this 3-4 times in the past decade or so, always with a nice double-digit 30-50% RoR inclusive of dividends at market-beating levels.

So, I believe I can guide others to invest at levels where they may see the same sort of development.

My last official article here on SA on Skanska was all the way back in 2021. Today marks the first update in some time, and I'm happy to enlighten you as to why I am currently "LONG" the company (in a way), and how exactly I am long.

Let's get going.

Skanska - A lot to like, but requires some consideration and strategy to get a "safe" profit here.

So, if you've followed my work for some time, you'll know that I've somewhat shifted my strategy over the last 5-or-so years. I started out writing on SA being very inclined towards the B&H-forever strategy. Never sold dividend companies, and just adding to my portfolio.

However, experience and strategy quickly taught me that in order to make a profit above market-average RoR, you all have to realize overvaluation. Undervaluation is less of a problem, as I see it - beyond that it's really good if you can recognize it. But overvaluation is the biggest problem I see in investing. Specifically, both not selling or buying at overvaluation. That is what sets you back.

So that's what I've been focusing on to avoid, through a mix of trimming strategies, never buying at overvaluation and the use of strategic derivatives such as options and various related strategies.

Skanska is one target for such a strategy for me.

My target is to make an annual RoR of 15%. That's my goal - at least that. So every investment I make has to be able to deliver at least that, based on conservative estimates.

Skanska, if you recall is a construction and infrastructure company. They're active across the entire world and have a near-135-year history, with a specific focus on Scandinavian, Eastern Europe/UK, and US/NA markets. The company exited South America over I've years ago, divesting even the maintenance operations of these regions.

The company is a proven builder of large projects, including things like:

- The Öresund Bridge connects mainland Europe/Denmark to Sweden.

- The MetLife Stadium

- Penn Station

- State Route 99

- 30 st Mary Axe

- Mater Dei Hospital on Malta

- Renovation/Additions to the UN building

- Restoration of the WTC site as well as the creation of the World Trade Center Transportation Hub

So, a lot of things to like in this company. Like most construction or cyclical businesses, it's had an interesting few years. The company's share price goes in clear cycles, and I've "played" these cycles since the GFC.

Skanska Share price (Google Finance)

{kind=link}

Generally speaking, I've bought the company at or below 140 SEK, and sold it close to 200 - the closer to 200 or above 200 SEK the better. That, combined with a 4-8% dividend yield, has generated above-average returns on tens of thousands of dollars allocated to this investment. And that is also how I intend to continue working on this investment.

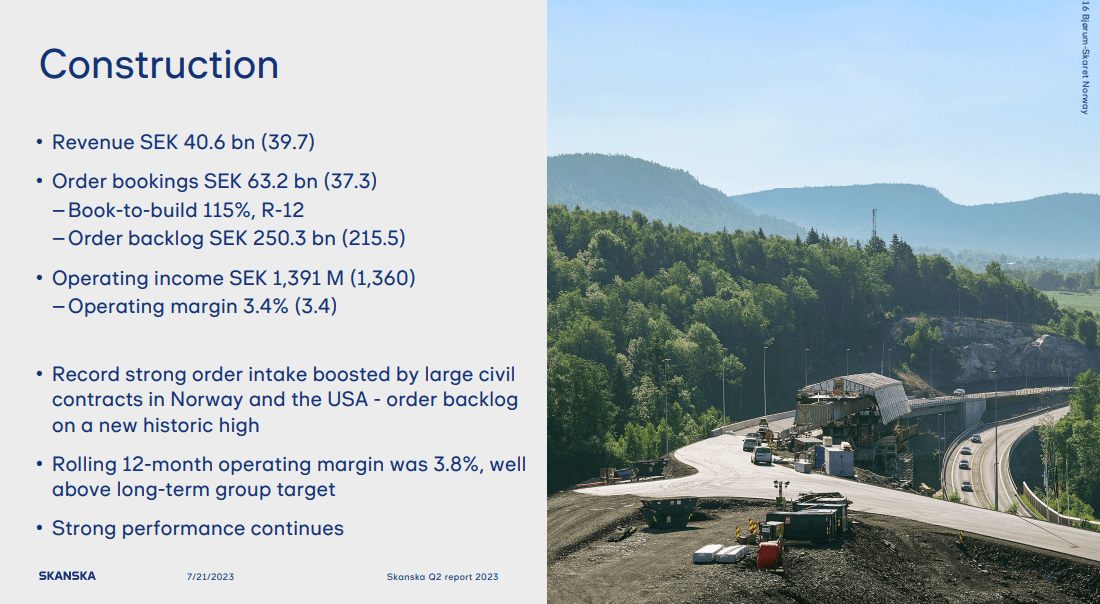

We have 2Q23/6M results. The company has been through a couple of major reorgs over the past few years. This has left the company, as of 2Q23, with record high order backlogs , strong construction results, solid leasing trends, and good underlying profit patterns.

Operating margins in construction are solid, close to 3.5%, and the company operates a t positive ROCE with a RoE of 11%+ a very strong capital/financial position, and positive ESG numbers.

The challenges for Skanska are like with most construction companies - property and residential. The company's current trends mirror the market, with very low sales volume in residential, and problems in the CRE, with solid leasing, but again low sales of properties.

Also, Skanska has completely stopped all investments in properties - no acquisitions at all were made during the quarter.

The company is in "managing inflation"-mode. Revenue and top-line growth were absolutely stellar, driven by key attractive segments...

{kind=link}

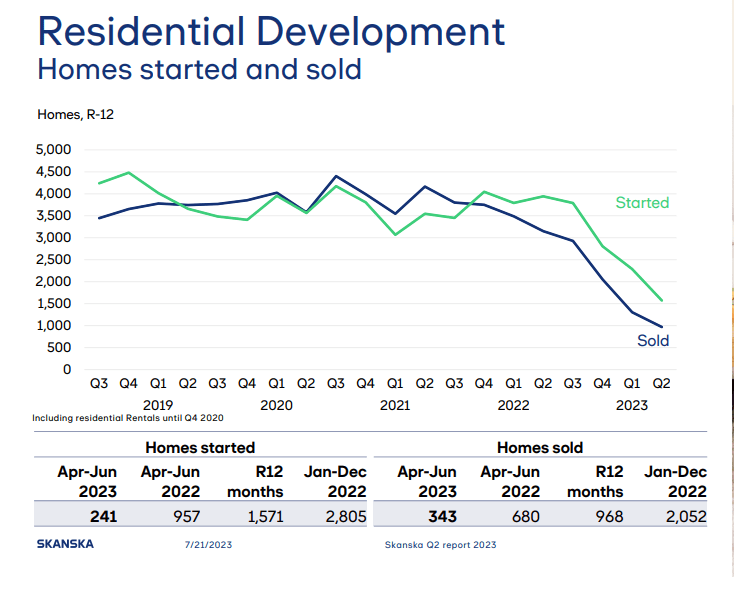

...while comparative revenue in other segments is down significantly. Residential development, for instance, is below 1.7B, only about half of the YoY number, with a near-double-digit decline in the overall operating margin with a ROCE of 0.2%. This is not due to the company or segment being sub-par - it's macro, and other property developers both inside and outside of the context of this geography are seeing very similar overall trends.

Take a look at, for example, the CRE segment.

{kind=link}

You can understand, based on such trends, why the company's share prices are down significantly from previous highs. The company's target for its investment property segment remains to work a high quality, sustainable office portfolio of at or around 12-18B SEK, generating stable cash flow. The company, as such, means to be an owner and lessor of CRE as well as a builder. Skanska has a decent interest in its vacant properties, and operating performance in this segment is actually stable. CRE in Sweden hasn't seen the same sort of drop as we have in other areas, because the supply here is much tighter.

That means that Skanska's vacancies here are comparatively low for a Commercial property developer, and in the investment segment, their occupation rate on an economic occupancy basis is 93% across the company, with over 98% in specific core areas like Malmö.

Highlights for this quarter remain order bookings and backlog in core segments. The company has an order book that's now filled with 250B SEK worth of backlog. What's more important than volume is the fact that these projects are profitable and at good margins, with contracts adjustable. This is different from the picture we had historically, where Skanska and similar businesses went into the trap of working quantity before quality, the result of which was dozens of billions of revenue, but with a margin close to or even below 0.5%, going into the negatives.

That time is now over.

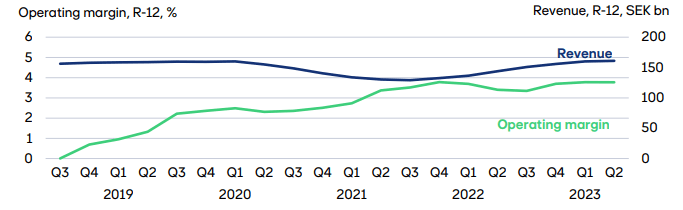

Since the time of 2019, when much of this change was driven, the company's operating margins have gone from below 1% to upwards of 3-4%.

Skanska Operating Margin (Skanska IR)

{kind=link}

This is for the construction segment, and this is exactly what we want to see in order to consider the company an attractive investment.

While residential development is seemingly literally falling off a cliff in some cases...

{kind=link}

...the company's overall mix means that even in this sort of downturn, the company is actually able to deliver earnings not only now, but on a forward basis as well.

Anyone who follows a construction business knows that cash flows are going to be volatile here. The company mostly goes positive during 3/4Q periods, with most of the 2Q periods being cash-flow negative. For now, the R-12 cash flow has gone negative as well.

However, fundamentals remain absolutely stellar. The company has available funds of over 16B, with unused credit facilities of almost 10B, and no relevant maturities during the entire year, with the first (and only 1B+) significant maturity in 2024 in the form of a bilateral loan.

The market outlook going forward is very mixed. The construction business is expected to stay flat with mostly stable or strong trends, while other segments are either expected to remain problematic, or flat. There's an overall polarization in the occupier and investor market, a demand for high-quality spaces with high ESG, but at the same time, a high cost of construction and a muted willingness to take risks.

Overall, 2Q23 was a good quarter due to strong construction trends, even with the problematic backdrop of macro that's driving down certain parts of the company. My focus is on the record backlog and various historic highs.

With that, I'm moving into valuation.

Skanska valuation - Requires consideration and strategy

As I've said, the company is an easy "BUY" for me at very specific levels, but above a 180 SEK price, it becomes more and more of a sell. I've sold calls to that effect at various prices before, and my avenues of entering Skanska as an investment remain open, depending on the situation.

In this context, I would say that the avenues you want to keep open are all of them. I'm talking straight buying shares, I'm talking writing cash-secured put options, and I'm talking buy-writing shares and covered calls. It's all driven by what sort of return and what sort of risk appetite you have.

My current investment in the company is two-fold.

First, I own common shares - though not many. When I say that I own common shares, I mean that they're not exposed to options - they're things that I own with no claim on them.

Second, I've also buy-written a significant set of covered call contracts a few weeks ago, where I was able to secure an annualized yield of over 16.1% by writing 130 SEK strike calls for the Jun -24 period. That's 300+ days from now, and based on my options premium I was able to secure a return of 16.12% if the stock is at 130 SEK or above at that date, at which point it will likely go into the money/sell. This also includes the estimate of a 4% dividend yield for the coming year. This trade was previously announced and clearly stated on our investment community, when it was valuable. It no longer has any return I consider worth investing in.

Based on the options and the shares bought it means that my effective cost basis for owning the stock, if it does not go into the money, is 124.15 SEK, which is a very attractive price for the company and long-term ownership.

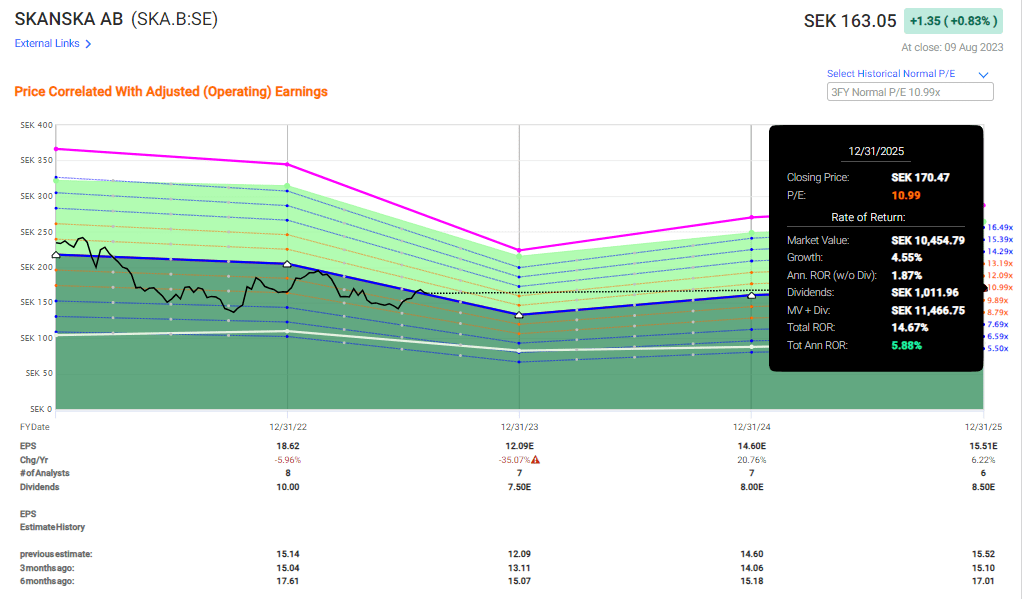

I've been through the current options chains and alternatives open to investors today. Skanska trades at 163 SEK, which is neither a good nor a bad price. It's a "meh" price. Current valuation targets call for the company to be worth between 132 SEK and 210 SEK, with an average of 168 SEK. I would consider this to be a good PT, with perhaps only a slight adjustment, considering it is worth about 165 SEK.

Due to the other alternatives on the market today, however, I would not necessarily go into this investment at this time. Not straight common equity investing. There is a bit too much uncertainty for me for this.

That is also why I went buy-write CCs here. I checked the cash-secured Puts but could not find a satisfying risk-reward-play. In fact, if we consider that the company could underperform based on poor returns in property and CRE may underperform in at least part of the mix, then potential RoRs here can actually become rather poor, and well below 10%.

Skanska remains one of the better construction companies out there, especially in Europe. It's easy why some would consider it undervalued here - and indeed, many analysts and ways of looking at the company do consider it undervalued at this juncture. I would perhaps only caution you that the company, at this time, requires very careful consideration and knowledge before investing to make sure that you're not exposing yourself to too much risk.

Skanska Potential RoR (F.A.S.T graphs)

{kind=link}

I am not arguing that the company has a realistic upside. That's why my stance is "BUY" here. However, the common share investing option comes with too much uncertainty at this specific price point to meet the specific demands for my 15% annualized RoR. You may have lower return demands than that.

Thesis

- Skanska is a very solid construction company with plenty of upside at the right price. The company moves in clear cycles that are macro, not micro/company based.

- At this time, we're down because construction is working well, but everything having to with property or leasing is in a tight spot, despite an overall tight leasing market due to low supply in some of its core areas.

- The overall stance on Skanska is positive and a "BUY" here, but before you invest, you should make sure that you're not exposing yourself to unfavorable risk/reward situations.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of my criteria, making it relatively clear why I view it as a "BUY" here.

Thank you for reading.

For further details see:

Skanska: At The Right Price, I'm A 'Buy' Here