SKSBF - Skanska: Successful Investing In Construction Requires Good Valuation (Rating Downgrade)

2023-12-07 09:00:00 ET

Summary

- Skanska is a cyclical construction company with a strong construction segment and solid operating margins.

- The company's 3Q results showed strong performance in construction and infrastructure but weakness in the property market.

- The company's valuation is currently above its target price, making it a "HOLD" recommendation. I would invest in the company again, if it dropped below 150 SEK/share.

Dear readers/followers,

My last coverage on Skanska ( SKBSY ) was provided in mid-August of this year, at an attractive valuation with a "BUY" rating. Since that particular article, we've seen some outperformance on the part of the company, justifying at the very least a mention given the market during the same time.

Seeking Alpha Skanska (Seeking Alpha )

Skanska is a cyclical construction company that has provided double-digit returns in the past, making it an attractive investment opportunity. The company has a strong construction segment with solid operating margins and a positive financial position. The company has certain challenges that require careful looking at prior to investing for the long-term, but an investment in Skanska is certainly possible - and potentially profitable here - if you catch it at the right price.

This is what I did. I sold options, which have expired worthless, but I've also invested in the common share at bottom-level valuations. That's why I'm currently up almost 19% in less than a month on this investment. I may in fact quickly rotate this position for a "quick buck", or I may keep it.

Infrastructure and construction is not an easy segment to go into here, but Skanska warrants your attention.

Let me show you the reason why that is.

Updating on Skanska after 3Q23

The construction sector, especially in Scandinavia, is in a difficult situation. This is because there is very little residential and commercial building going on. What is going on are infrastructure projects, but some key segments for a company like Skanska are related to homebuilding.

I'm no stranger to owning Skanska. I've owned it on and off for years, in fact since I started investing in the market. I know the company and its cycles well. If you really manage to score it at 120-140 SEK/share, then the upside is potentially massive, coupled with a very good yield. If it becomes too expensive, then it's time to trim and sell and wait for it to drop again.

I've done this 3-4 times in the past decade or so, always with a nice double-digit 30-50% RoR inclusive of dividends at market-beating levels.

So, I believe I can guide others to invest at levels where they may see the same sort of development.

My target is to make an annual RoR of 15%. That's my goal - at least that. So every investment I make has to be able to deliver at least that, based on conservative estimates.

Skanska's 3Q results were a telling story of just how the market currently looks. We saw strong construction and infrastructure performance, resulting from a solid well-filled order book in these segments, but impacted by a very weak overall property market. Skanska took an asset and goodwill impairment of almost a billion SEK, with a decent 3.3% margin in construction, but a ROCE of less than 1% in project development (compared to a 10%) on an R12 basis. The company also delivered a RoE of 9.5%, down almost 8% on a YoY R-12 basis.

That being said, Skanska retains a very strong financial position and has managed to work through its carbon reduction goals - managing a 58% reduction in less than 8 years, which is impressive. These sorts of goals are important when the company doesn't have much else positive to show for its operations.

Here are some segment-specific results.

{kind=link}

I don't expect impairments or downturns in construction or infrastructure on a forward basis. The company is robust here. The main question to me is just how long is the company's downturn in property and projects going to last. The answer is tied, overall, to how long the entire downturn in these markets is going to last in Sweden.

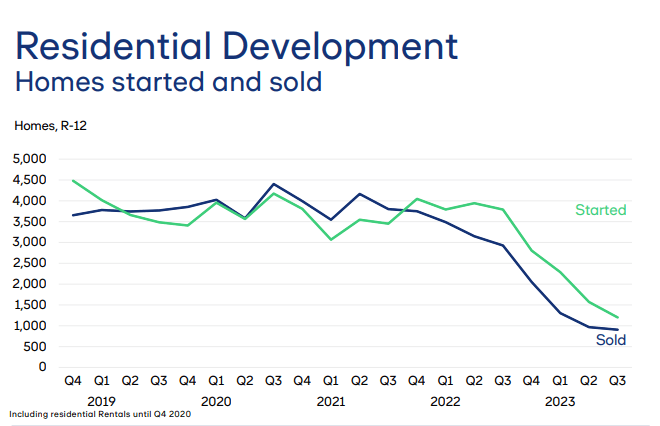

To showcase just how bad things are, I can tell you that while the company managed to sell 277 homes, which isn't bad, the company started 0 new developments. That's right. Zero new residential developments , compared to a YoY number of 371. The company also managed a negative half-billion SEK operating income in the resi development segment, as well as a negative 9.5% ROCE.

This lower-than-normal sales and start volume is Europe-wide , with the exception of central Europe (certain geographies).

CRE is actually a segment that went up for this quarter. The company saw a good gain in sales, even if the operating income was down, and Skanska has 29 ongoing projects at 31B SEK completion, with a 61% completion rate. The occupancy in these projects is sub-par- less than 36%. But again though, even in CRE, the company hasn't started any new projects. It's also divesting some offices, and it continues to hold a qualitative portfolio, but perhaps in a market that has only limited use for it at this time.

In the company's investment property segment, things are far calmer. The company has seen stable operational performance, with an economic occupancy continued to be above the 91% level.

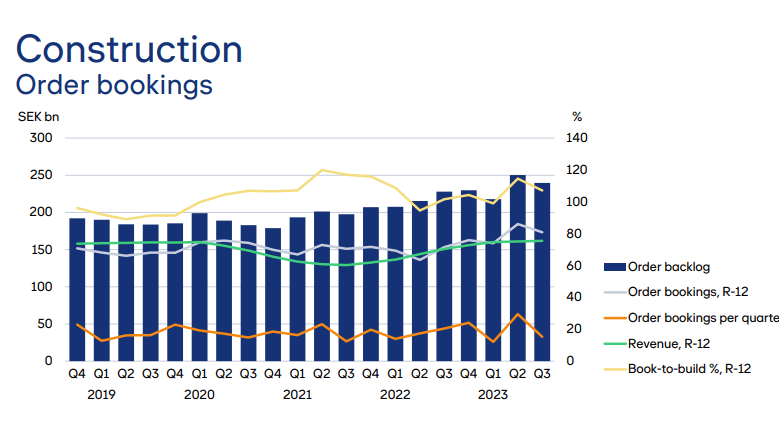

and order bookings are, in fact, better than I would have expected.

{kind=link}

But, illustrations can also serve the purpose of seeing the depth of the residential crash. It brings even my mind, who wasn't around as an adult at the time, to the early 90's real estate crash in Scandinavia.

{kind=link}

The company's realized gains for sales are troughing - as is the number of completed projects, available land, or ongoing projects at completion. The fact is that this current trend implies a fundamental weakness in the company's sales for the next few quarters. In order for us to see a tailwind here, there would have to be several quarters of positive building activity here.

This would require interest rate cuts , which I view as unlikely in this environment in the near term.

Because of that, I don't see a massive near-term potential fundamental improvement for Skanska. We need to focus on Construction and Infrastructure here, as well as the investment portfolio. While these segments can work well, they're not as attractive as a Skanska in full force.

Not a single market is looking "up" on a forward basis either if you follow relevant journals or reports. Construction is flat - the USA is the strongest market for the company here, with civil and social infrastructure. But it's not going "up". Residential development is down, CRE is expected to go down, and investment properties are flat. Skanska is likely to continue to see significant impacts from low transaction volumes, a hesitant overall market, cost of living pressures, low activity in housing, and lower-than-normal expected activity trends until macro changes.

So, Skanska has really become a bit of a macro play - and the macro is currently very difficult to forecast. If it weren't, we'd all know what to do.

Let's clarify this in Risks & Upside.

Risks & Upside

The main risk to Skanska is fairly simple - macro. And it's not something Skanska can do something about. In order for fundamental improvements in the company's earnings, we need lower interest rates and higher buying activity. I expect the first rate cuts toward the end of next year - though it's of course that some over-eager Swedish FED might try to cut while inflation is still above 5%. However, for as long as we lack clarity in 50% of the company's segments, I'm heavily impairing the company's targets based on this, which I view as a significant risk.

The upside for the company is obviously buying Scandinavia's largest construction and residential building business. If done at a proper price with a good upside, this double-digit annualized upside is not only safe, it also comes at a very good normalized yield.

Let's look at the valuation and what you can expect here.

Valuation

Following strong construction results and good performance in IP, the company's weakness is crystal clear - and while maintaining good financial strength and good leverage, the company can do nothing about the pressures that it currently faces.

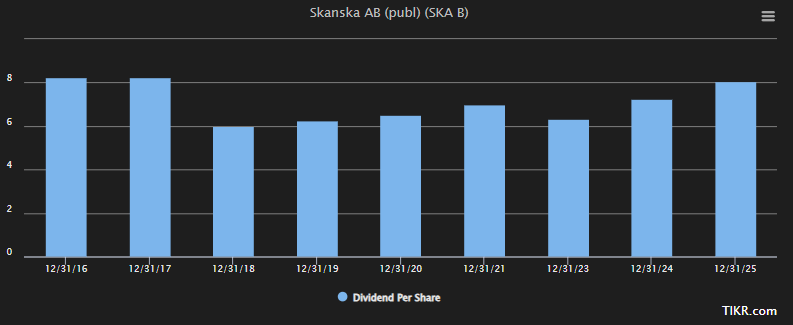

All it can do is "swim". And it does. My forecast for Skanska is a continued high revenue, but lower earnings, which will impact both the dividend and EPS. For 2021, the company paid around 7 SEK - I believe that now, this dividend will be lowered to around 6 SEK to reflect the lower results. I also don't share the positive expectations that analysts have for 2024 and 2025E here.

{kind=link}

While the company's dividend is crucial to the business, Skanska is, as you can see historically, not above-cutting it when needed. That's why I believe the company won't increase it as it's being specified here. That, and I don't believe the upside will materialize as quickly as the analysts seem to expect here.

Due to this weakness in results, I believe it is flawed for the company to trade at anything above 150 SEK/share here, and it's currently 171 SEK. At below 150, the company comes in at a 15%+ annualized to its historical discount of 12x P/E, or over 30% of total RoR to a 2025E and a PT of around 195 SEK including some normalization.

At 170, that upside is close to only single digits with a total RoR of closer to 20%. Not good enough for me. The yield is also below 5%, which isn't that great in an environment where 5% is now "easy".

It also doesn't help that over the long term, Skanska isn't really a significant outperformer here. The company has managed below 9% annualized RoR if invested during 2003, with plenty of negative years. It's more volatile than its quality would suggest, which means, to me, that you really want to make sure about your investment valuation level here, which over time has been clearly stated (using these historical valuations), to be below 13x P/E. (Source: FactSet).

If invested in below 13x P/E, there isn't a single time in the last 20 years, when your investment would not have been profitable to date. But if invested at 16-18x P/E, the same is certainly not true.

That's why analysts are somewhat uncertain here. 8 of them follow Skanska, and most of them are at "HOLD" or "SELL", even if their overall price target is actually just north of 170 SEK per share from a low of 130 SEK to a high of 221 SEK.

As before, I take a lower target due to the overall macro situation and what I see as currently more attractive investment potentials. For that reason, I say "HOLD" here.

Thesis

- Skanska is a very solid construction company with plenty of upside at the right price. The company moves in clear cycles that are macro, not micro/company-based.

- At this time, we're down because construction is working well, but everything having to with property or leasing is in a tight spot, despite an overall tight leasing market due to low supply in some of its core areas.

- The overall stance on Skanska is no longer positive and a "HOLD" here. Before you invest, you should make sure that you're not exposing yourself to unfavorable risk/reward situations - and in this case, i believe you may be doing so.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of my criteria, making it relatively clear why I view it as a "BUY" here.

Thank you for reading.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Skanska: Successful Investing In Construction Requires Good Valuation (Rating Downgrade)