SKYH - Sky Harbour: A Private Jet Play With Room To Grow

2023-08-24 02:48:22 ET

Summary

- Sky Harbour specializes in building and operating private aircraft hangars, offering dedicated spaces for ultra-wealthy private jet owners.

- The company focuses on a niche market with high demand and limited supply, leading to high occupancy rates and rental revenues.

- Sky Harbour's ambitious growth plans and unique approach to serving customers could result in significant growth potential.

After a boom in private jet sales over the last few years and expected CAGR of 5.3% through 2033, Sky Harbour ( SKYH ) represents a solid growth opportunity. While most SPACs in the space have been more flash-in-the-pan than substance, Sky Harbour is a refreshingly grounded company that is capitalizing on a shrinking supply of aircraft hangars in the US.

While their initial valuation feels overly ambitious to me, a more conservative commercial real estate capitalization rate still puts them above market value today. The firm is showing traction on its plans in recent financials and looks to be an opportunity flying under the radar.

Company Overview

Sky Harbour is a unique business model in the private aviation industry. The firm specializes in building and operating private hangars for jet owners. Unlike many current providers of aircraft storage where aircraft are stored in a community hangar or other shared storage spaces, Sky Harbour offers a unique luxury experience where customers have a hangar completely dedicated to their plane.

This creates unique value for the ultra-wealthy that want to protect their investments. Hangar rash (bumping a plane into a wall or another aircraft) is a common issue in community hangars where there is less space, or ground crews are rushing to move multiple aircraft at the same time. These small incidents add up quickly when moving and insuring multi-million dollar assets - it's estimated hangar rash costs the industry $150 million annually .

Private aviation has had massive growth post-pandemic, and the demand for aircraft storage , particularly in certain markets, well exceeds the supply. Other investments in the industry, like Wheels Up ( UP ) or Blade ( BLDE ) haven't performed well as individual consumer demand for charter flights have declined , but Sky Harbour is targeting a different segment in this space: private jet owners. Ultra-high net worth customers aren't as likely to change their spending habits, even during times of inflation or recession, particularly when what they want is scarce.

Sky Harbour is focusing on an ultra-niche target market with only around 14,000 potential customers in the United States. The scarcity of hangars, lack of airport growth in the US and their unique approach to serving those customers, however, makes the business model very intriguing. Houston, one of its first campuses, is already at 94% occupancy and new locations are hitting record highs of $40+ per square foot ( SKYH Investor Relations ), during a time when private flight demand is down over the previous year. A Gulfstream 650ER, which can be acquired by private owners to the tune of $70 million, needs a minimum hangar size of 100 by 125 feet, raking in around $500,000 per year in certain markets.

I also like their efforts to reduce costs through vertical integration by acquiring RapidBuilt, a manufacturer of pre-engineered metal buildings. The firm is building standardized layouts to make the permit and build process streamlined.

Unlike traditional Fixed-Base Operations (FBOs) like Signature Flight Support ( acquired by Blackstone and others in 2021 ) or Atlantic Aviation ( KKR investment in 2021 ), they will not be offering fueling and other services but arranging those services through the airport authority or FBOs on the airfield, making labor costs much lower than FBOs that offer hangar space, fuel, deicing, and other aircraft services. By not going after fuel revenues, it makes SKYH's entry into certain airports less contentious, as they won't be fighting for fueling rights against the airport authority or competing FBOs.

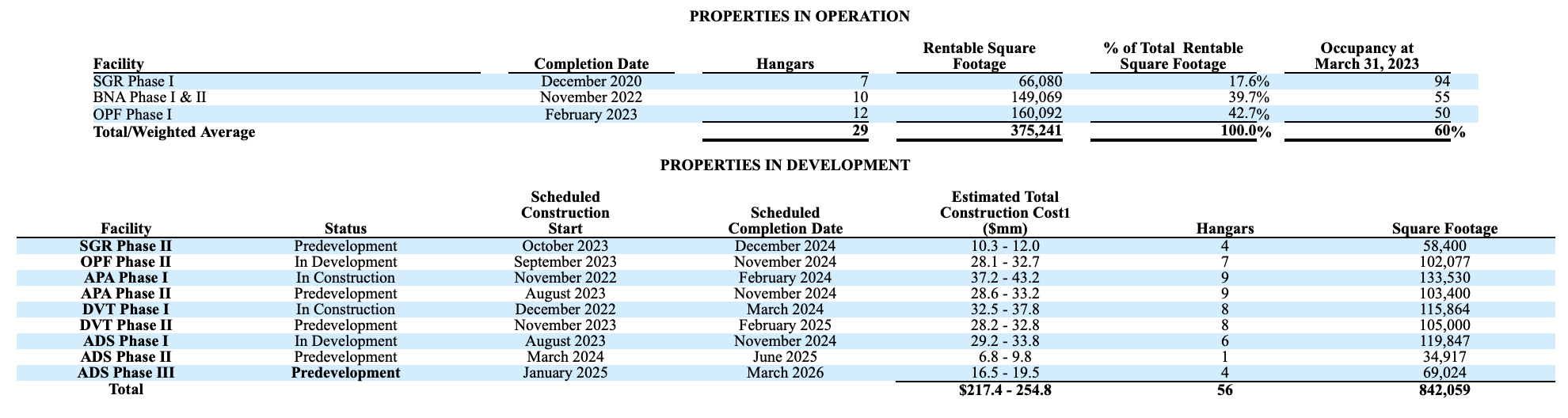

Projects In Development

Projects in Development (SKYH Prospectus)

{kind=link}

Because of the long timeline of these developments, I believe many investors aren't focusing on the traction the company has made thus far. The majority of projects are underway with completion dates as far out as January 2025, but long-term, the company expects net operating income of $27.6 million on 5 of the planned 6 sites by 2025, a 12.29% yield on the projected project cost of $224 million.

The latest earnings for Q2 show rental revenues beginning while hangars are being completed, and an overall decline in SG&A costs. The latest build completed in February of this year at OPF, Opa-Locka Airport, moved from 50% occupancy at the end of Q1 to 67% occupancy in Q2. As each of these developments are completed and topline revenue begins to outpace expenses, the market will take notice.

Outlook

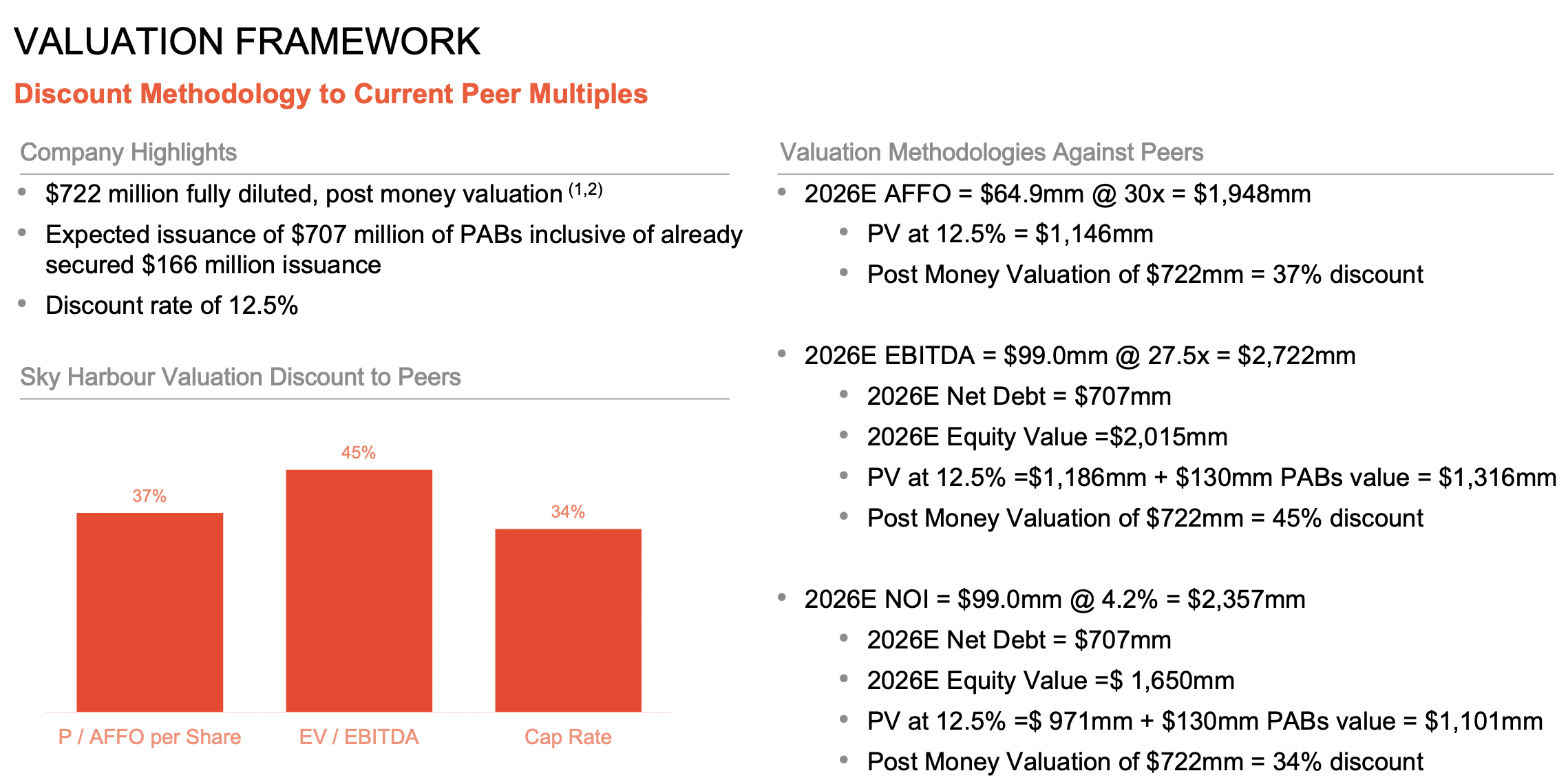

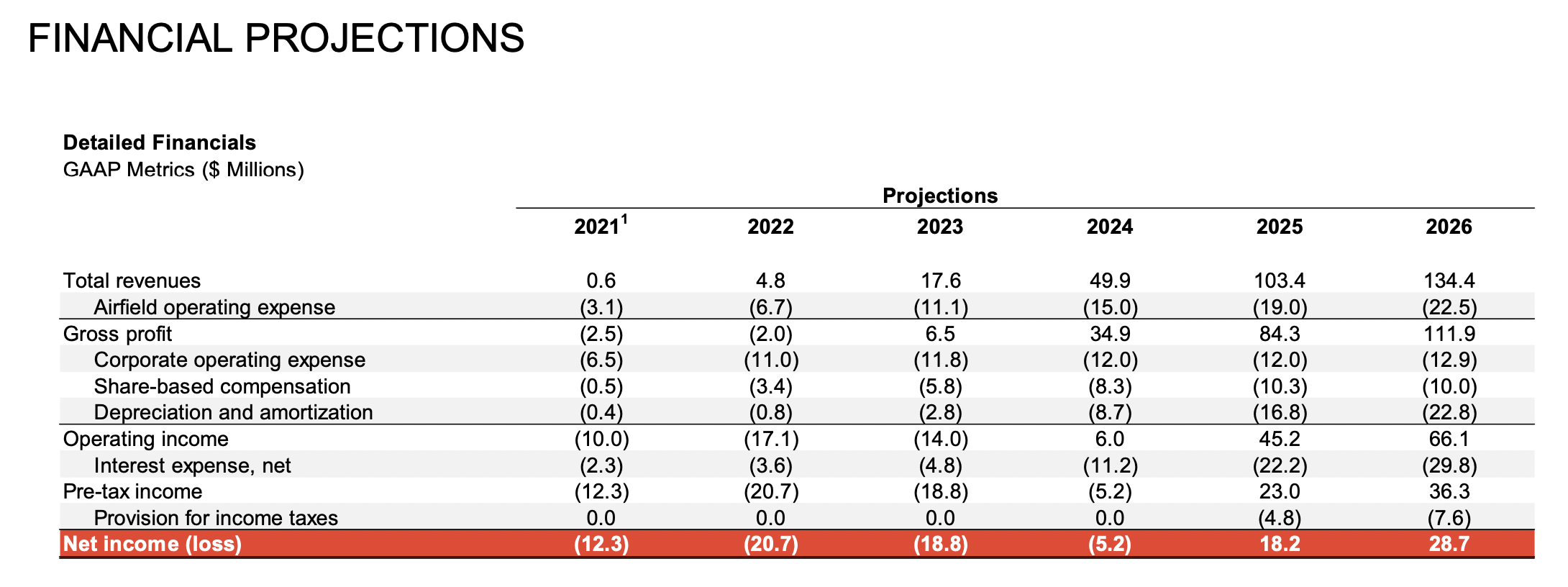

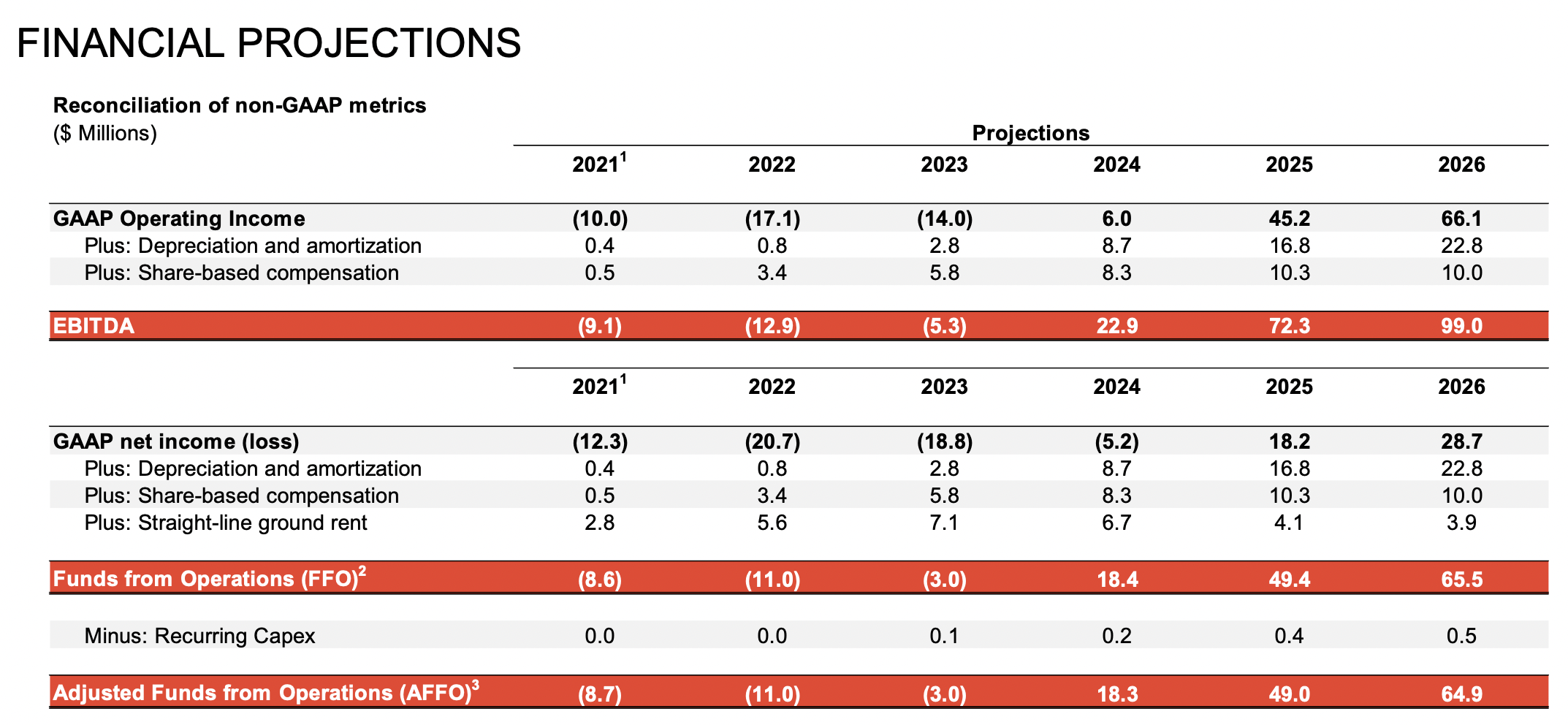

The firm includes their own valuation work in the investor presentation, which is well thought out, but their valuation multiples are a tad aspirational. They expect to hit $99 million in EBITDA by 2026 year end, which will require around 3-4 million square feet of completed developments if they maintain mid-$40 tenant rates. At a 4.2% capitalization rate (cap rate), this values the firm at $2.7 billion by 2027. With almost 1 million square feet under development currently, this doesn't seem unachievable, but will require strong performance gaining airport approvals for future hangar campuses.

However, 4.2% is a very aggressive cap rate when looking at recent surveys and the general decline in the commercial real estate industry. To be more conservative in the valuation approach, I will use an 8% cap rate. This is still on the high end in my opinion, but this is a unique development approach with premium customers.

Valuation Presentation (SKYH Presentation) SKYH Projection (SKYH Presentation) Financial Projection Cont. (SKYH Presentation)

{kind=link}

{kind=link}

{kind=link}

Using the projected $99 million in Net Operating Income for 2026 at an 8% cap rate, would value the projects at $1.24 billion. Less $707 million in projected debt at that time, a $530.5 million valuation in 2026. Present value (12.5% discount rate, 3 years) leaves the firm with a $373.6 million valuation, a price target of $6.23 per share.

This value also doesn't factor in exceeding growth targets and finding other revenue opportunities, like their newly acquired metal building manufacturer RapidBuilt. It also doesn't include the value of their Series 2021 Private Activity Bond ((PAB)), which Sky Harbour places at $130 million. So again, I consider this is a very conservative approach.

Downside Risks

Not offering fuel services in most markets could be a risk to the business plan, as fuel markup is a significant source of revenue for traditional FBOs. They may not be able to create fuel deals that are attractive enough to steal large aircraft customers (that take a lot of fuel) from competing FBO public and private hangars.

Conclusion

While ultra-high net worth consumers would be less affected by a possible recession, it could impact their aircraft buying activity or move them to park aircraft in less expensive locations. Plus, rising interest rates, building costs and lack of development opportunities may slow their growth.

At the time of writing, the stock is only trading at $4.41 per share with a market cap of $252.8 million, which I feel is undervalued given the strength of the business model and Sky Harbour's growth potential. Each time they hit their targets over the next year, particularly as EBITDA begins to climb, there could be a 39%+ upside here.

There are a lot of riskier plays in the private aviation space, but this company seems to be capitalizing on a captive market that puts a lot of value in luxury and convenience, with the cash to spend on it. With bond financing and successful traction thus far in their completed projects, their future looks promising.

For further details see:

Sky Harbour: A Private Jet Play With Room To Grow