SKYH - Sky Harbour Group: A Genius Investment Or Was I Wrong?

2023-08-18 10:48:07 ET

Summary

- Sky Harbour Group Corporation is an aviation infrastructure development company that leases hangars to general aviation and private jet owners.

- The company has seen a 322% increase in revenues year-over-year and a 56% increase sequentially.

- The main risk for Sky Harbour is funding its expansion, but it has options such as partnering with real estate developers or using private activity bonds.

In my previous report covering Sky Harbour Group Corporation (SKYH), I marked the stock a speculative buy to capitalize on the needs of the ultra-rich. There are many ways to accumulate wealth. One way is to look at what the rich are doing and apply the translation/interpretation, imitation and emulation principle where one translates or interprets, imitates, and as a final step tries to do things better. Another way, by simply investing your money in whatever services and products the rich and ultra-rich need. Think about private jets but also liquors, fashion items, watches, expensive bags amongst others and the company that makes Moët Hennessy - Louis Vuitton ( LVMHF ) is worth considering.

In this report, I will be revisiting Sky Harbour Group and see whether that name is still worth considering for investment after a 14% decline in share prices. Perhaps I was wrong after all.

About Sky Harbour Group

Sky Harbour describes itself as an aviation infrastructure development company, building the first nationwide network of Home-Basing Solutions (“ HBS ”) for business aircraft. Sky Harbour develops, leases and manages general aviation hangars across the United States, targeting airfields in the largest growth markets with significant aircraft populations and high hangar demand. Sky Harbour’s HBS campuses feature exclusive private hangars and a full suite of dedicated services specifically designed for home-based aircraft.

Putting it really simply, Sky Harbour leases hangars to general aviation and private jet owners as well as associated services.

{kind=link}

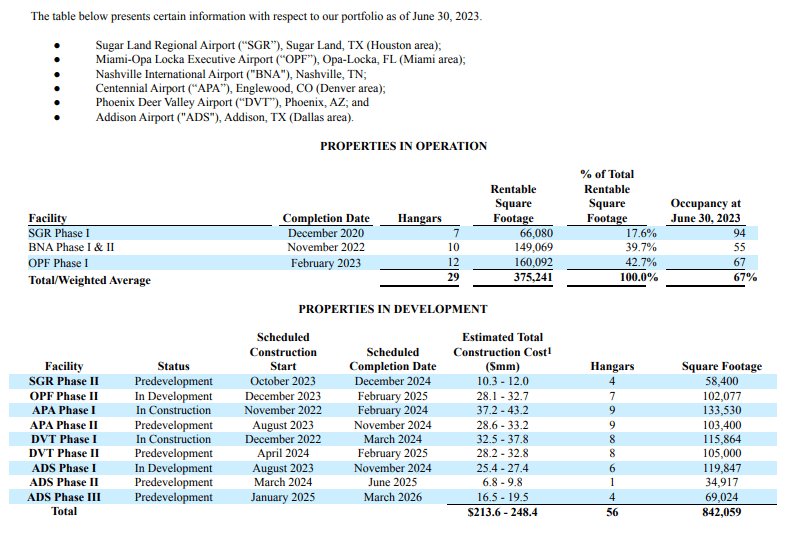

The company currently has 29 hangars in Houston, Miami, Nashville, Dallas, Phoenix and the Denver area with occupancy standing at 67% up from 60% in the prior quarter. Another 56 hangars are scheduled to be completed between 2024 and 2026 adding 2.25x the current square footage. So, Sky Harbour bets big on demand for home-basing private jets and making things as comfortable as possible for business jet owners.

Sky Harbour Group

The company also works with a smart principle, allowing lights, fans and doors to be controlled via an app. The app also allows users to request additional services and 24/7 surveillance. So, it looks a lot like a smart home setup - but for hangars. I am pretty sure the business jet owners are big fans of having the ability to conveniently arrange everything from the app.

A Look At The Results For Sky Harbour Group

{kind=link}

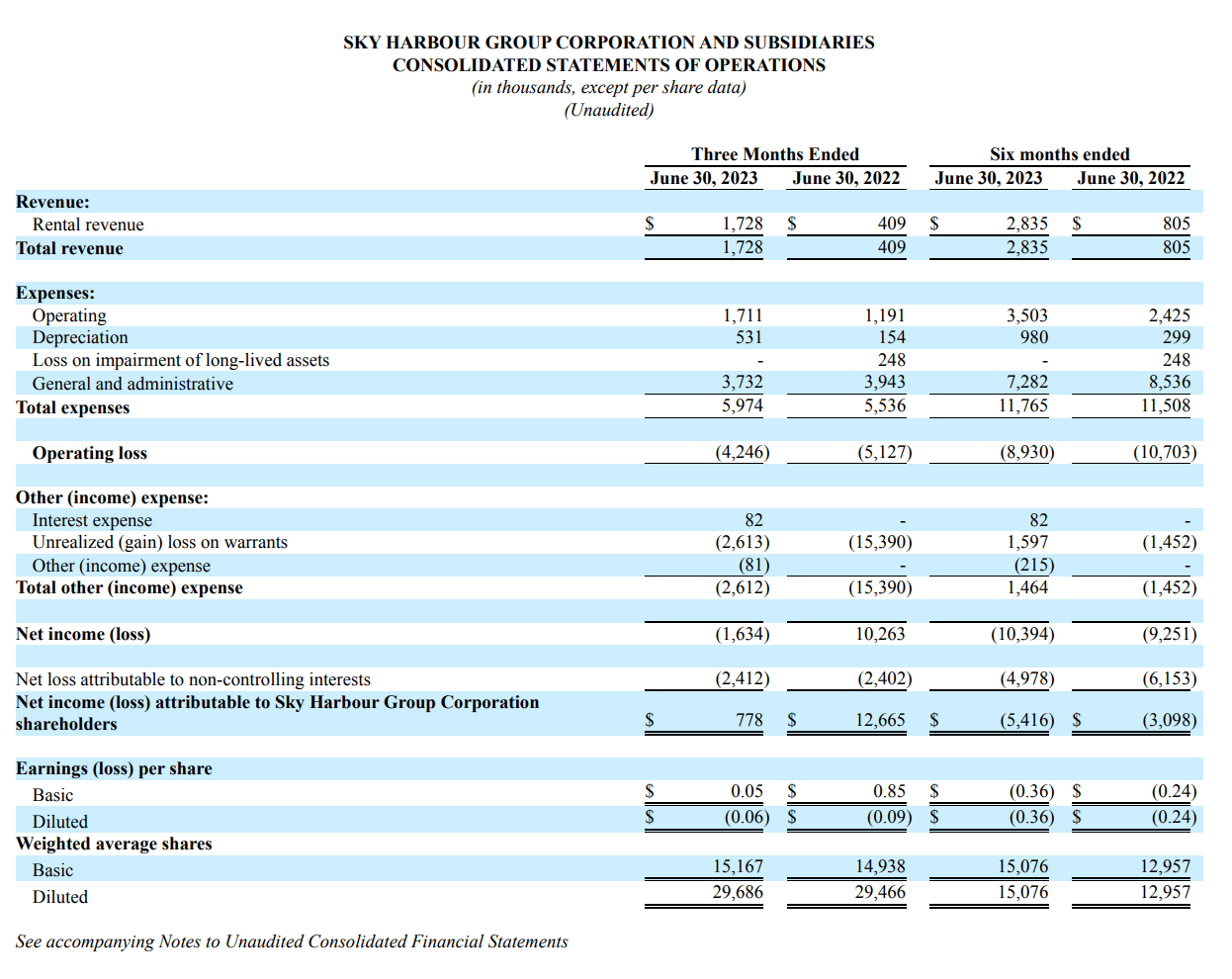

Revenues are up 322% year-over-year and 56% sequentially. As can be seen, the company is still loss-making, but with a 67% occupancy rate and full occupancy expected in Houston, Nashville and Miami things are looking promising. Furthermore, the acquisition of RapidBuilt which manufactures pre-engineered metal buildings provides a vertical integration which can benefit the cost of expansion for Sky Harbour. Total cost rose 8%, with the operating loss declining 17%. Sequentially, those numbers were a 3% increase in costs and a reduction of almost 10% in operating losses.

Operating cash burn of $4.5 million in the second quarter was in line with the performance in the first quarter.

The Risks For Sky Harbour Group

From the demand side, I would not expect major headwinds for Sky Harbour Group. If people have the money to buy a business jet worth up to $50 million, they will also want to take great care of it and put in a hangar suiting their needs, and Sky Harbour Group focuses on home basing, making things as easy as possible for the ultra rich and getting a good buck for that. The challenges are more into the aspect of scaling and getting the business to be cash flow positive for further growth to be funded by the operations. If that is not the case, shareholders are at the risk of being diluted and while management said during the second quarter earnings call it will only raise equity at attractive terms for shareholders, the reality is that once businesses that need to scale to become profitable need to raise equity it does not happen at attractive terms for existing investors.

So, the capital needs could be a risk to Sky Harbour Group and even more for existing investors. However, the company was quite clear during the second quarter earnings call that it has several paths, with projects either being funded via partnerships with real estate developers where profits are optimized through management fees and 60% leverage on future developments.

What is perhaps somewhat disappointing is that the company significantly increased its rental revenues, but its operating cash burn remained the same, and it makes one wonder where the inflection point is. Perhaps, the good thing is that the company has $150 million in cash , equivalents and restricted cash. The flip side of the strong liquidity is that most of the cash equivalent namely $114.2 million is held in restricted investments and there is restricted cash of $16.6 million held for interest payments for the Series 2021 PABs.

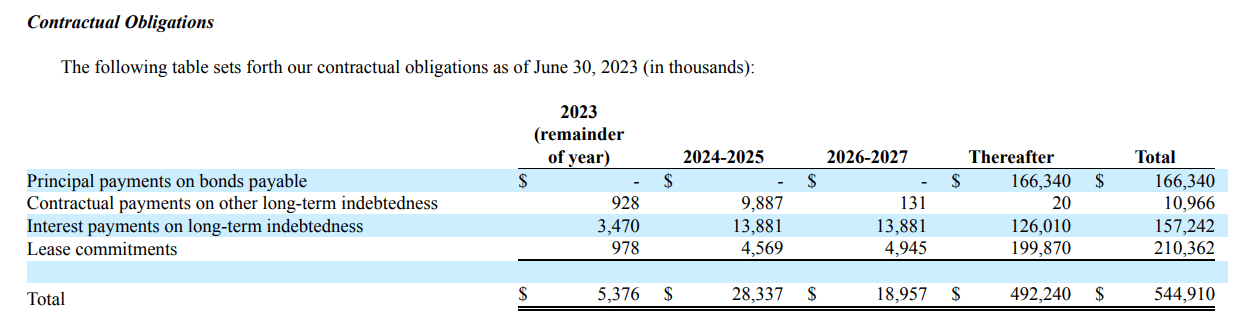

{kind=link}

So, there is $19.65 million in unrestricted cash and investments. For the remainder of 2023, there is $5.376 million in contractual obligations, which would reduce cash to $9.65 million. Furthermore, there is around $10 million in construction costs each quarter, which would fully consume the cash pile. Is this a major issue? I wouldn’t say so. If we assume there is no improvement in the operational cash burn, we would see up to $20 million in operating cash burn per year and $40 million in construction costs, which gives $60 million in cash burn. Around $100 million in restricted investments will become available within one year, which will more or less fund the construction costs for a year and a cash burn if that is set to continue at the current rate. Additionally, the contractual obligations through 2025 would also be covered and then there still will be money left.

The upcoming projects have an average cost to complete of $15.4 million to $18 million per month or $50 million per quarter, compared to $10 million in construction costs currently. With around $134 million in cash and equivalents, excluding restricted cash, Sky Harbour Group heavily relies on taking out another PAB to fund the developments that are not covered by the Series 2021 PAB.

So, the challenge Sky Harbour faces is that it needs to build hangars to scale its business to generate a cash flow, but those construction costs will be significantly higher in the coming years than the construction costs the company currently has.

Is Sky Harbour A Good Stock To Buy?

I view Sky Harbour as an investment opportunity focusing on capitalizing on the ultra-rich. Instead of the ultra-rich capitalizing on you, you can capitalize on them as Sky Harbour caters to their needs and habits. I would mark shares a speculative buy on their expansion in rentable square footage and the expansion projects that are planned in the coming years. As the hangars are rented to wealthy individuals and most likely also to companies, I don’t see any non-payment issues. The main risk for Sky Harbour centers on funding their CapEx and ramping the results towards projected levels. The 2022 revenues came in at 37.5% of the projected value which is not great and so far in 2023, the H1 revenues are at 16% of the values that Sky Harbour initially had projected, and the current growth rates would suggest revenues to come in at around 55% of the targeted value.

Currently, the business still burns cash despite a significant growth in revenues, but the positive is that occupancy rate increased from 60 to 67 percent suggesting that by next year the current rentable space could be fully rented and as the occupancy increases, the rent on the remaining hangars also increases. In Miami, the leases started at $32 per square ft. and they are now in the mid-40s showing that there is a 40% increase from early leases to final spot while in Nashville the rent has increased around 25%. Both increases in the price per square meter also include inflationary effects.

Sky Harbour does not have the funds available to fund its expansion, but the company is also not aiming for that. It has various levers to fund its growth that do not require shareholder dilution. The main options are co-developing with real estate developers where Sky Harbour would invest less and manage the hangars but would likely get a juicy profitable management fee and the other path would be via the private activity bonds which have long-term maturities but do require adherence to debt covenants.

For the time being, I don’t consider Sky Harbour Group Corporation stock a buy, but rather a hold and a very speculative buy at best. I do like the concept, but we see that revenues are not where they were supposed to be with little guidance on cash flow generation. In the quarters ahead, I will be keeping an eye on the revenue generation to see whether the company comes even close to its initial projections for ramping up revenues.

For further details see:

Sky Harbour Group: A Genius Investment Or Was I Wrong?