SKYH - Sky Harbour Group: Harvesting Ultra High Premium From The Ultra Rich (Rating Upgrade)

2023-11-21 07:08:30 ET

Summary

- Sky Harbour Group has seen its stock gain over 50% since May 2023, driven by the scaling progress of its aviation infrastructure development business.

- SKYH's occupancy rates have increased, with improvements in Nashville and Miami-Opa Locka Airport.

- Revenues have grown significantly, and the company expects to achieve break-even on cash flow ahead of schedule.

I initiated coverage for Sky Harbour Group Corporation ( SKYH ) in May 2023 with a buy rating . Since then, the stock has gained more than 50% and even 75% since August when I did a follow-up on the stock to update investors on the scaling progress. In this report, I will be revisiting the stock and assessing the occupancy and results of the company.

What Does Sky Harbour Group Do?

{kind=link}

If you are unfamiliar with Sky Harbour Group, you might want to read how the company describes itself:

Sky Harbour is an aviation infrastructure development company building the first nationwide network of Home-Basing Solutions (" HBS ") for business aircraft. Sky Harbour develops, leases and manages general aviation hangars across the United States, targeting airfields in the largest growth markets with significant aircraft populations and high hangar demand. Sky Harbour's HBS campuses feature exclusive private hangars and a full suite of dedicated services specifically designed for home-based aircraft.

I don't want to look too much into the operations of the company in this report, but only note that Sky Harbour Group is a play to capitalize on the ultra-rich and on the trends of growing private jet fleets and home-basing. The set up is also rather straightforward, Sky Harbour Group leases ground on in-demand airports, builds hangars on them for which costs are optimized due to the acquisition of RapidBuilt which provides the pre-engineered hangars. From there, it is a matter of leasing the available space to private jet owners and operators.

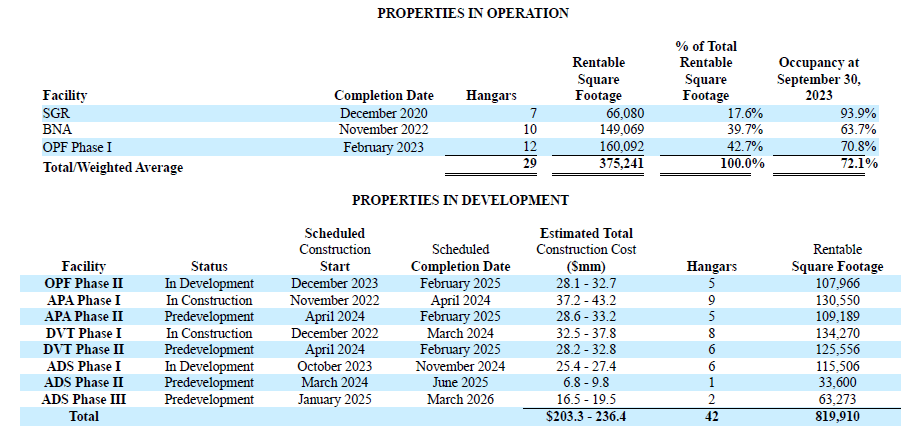

Sky Harbour Group Occupancy Increases

{kind=link}

Quarter-over-quarter, the number of properties in operations remained at 29. However, the occupancy in Nashville improved from 55% to 66% while the occupancy of Miami-Opa Locka Airport increased from 67% to 71% marking a total increase from 67% to 72%.

Interesting to note is that the number of properties in development decreased from 56 to 42 with SGR Phase II being terminated, which decreased the construction costs in the range of $10.3 million to $12 million. SGR Phase II, serving the Houston area, however only accounted for four hangars. So there are some other moving items. OPF Phase II is now expected to feature two hangars less while APA Phase II in the Denver area will feature four hangars less, DVT Phase II (Phoenix area) will feature two hangars less and the third phase of the Dallas-area development will feature two fewer. The estimated costs, however, remained the same for those projects indicating that potential costs for construction have gone up. While construction costs are a significant cash outflow driver, I do note that its vertical integration with RapidBuilt should be a long-term positive for a cost-efficient expansion.

Another noteworthy item is that APA phases have been delayed from February 2024 and November 2024 to April 2024 and February 2025 respectively.

Sky Harbour Group Scaling Drives Down Losses

{kind=link}

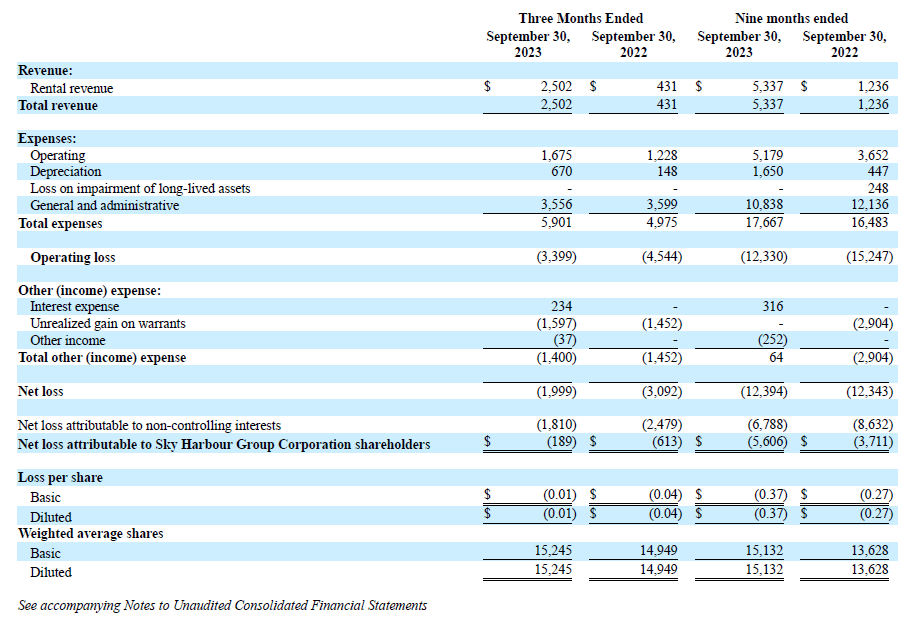

Looking at the results, we see that revenues increased from $431,000 to $2.5 million. That increase in revenues reflects the growing base of lease hangar space to tenants. If we were to assume that all revenues account for leasing, which is not the case, but we have no way to know the lease related revenues, then we get to quarterly rent of $9.25 per square foot per quarter which is up nearly 35% sequentially. Sky Harbour has been talking about rent per square foot increasing from around $32 to $40 now, so there is demand for the space, but it should also be kept in mind this more than likely is about the square footage revenue per year. So, the group is currently at a total annualized revenue of $37 per square foot with further upside as square footage pricing increases as more hangar space gets occupied. Approximating the lease revenue per square foot using the tenant lease obligation would indicate $23.68 per square foot. Essentially, early leases are low in the sense that the early bird gets the worm but as the company itself grows its total hangar base, I also do expect that the company will start leasing at increasing $/square footage figure, which should boost the company to become profitable.

Year-over-year, the costs increased by roughly $1 million driven by higher operating expenses and higher depreciation and its operating loss declined from 10.5x revenues to 1.4x revenues. Also compared to last quarter there is a big improvement as a quarter ago the loss was still sitting at 2.5x revenues.

For the nine months ended, the cash burn was around $6.3 million compared to $25.3 million in the comparable period last year and for the quarter the cash burn was $0.5 million. So, we really are seeing things heading in the right direction and the company also sees break-even on cash flow to be achieved mid-next year which is around six months earlier than the company initially expected.

What Are The Risks For Sky Harbour Group?

I previously discussed the risk that in case of continued cash burn and higher construction costs for future projects, Sky Harbour Group would need to take another PAB loan. I believe that Sky Harbour Group will still be looking to finance expansions with those loans if available to them, but I also believe that the operating cash burn tapering provides a significant tailwind to the company which should leave it in a more comfortable spot for expansion. Previously, the worst-case scenario assumed $20 million in cash burn per year and we are now sitting near even. That tailwind alone already would account for 10% of the construction costs through 2026 on annual basis meaning that towards 2026, not having to burn $20 million per year would save the company $60 million covering 30% of the construction costs and that does not keep in mind that the cash flow will actually turn positive sometime next year. So, the company eventually will be in a position where it can grow without having to fully finance expansion with debt.

Premium Growth Ahead Looking Strong For Sky Harbour Group

With the hangars in Phoenix and Denver opening next year and despite the slide on the schedule for Denver, the company is expecting to break even on operating cash flow way ahead of schedule. It does not stop there for the company as it has openings scheduled all the way to March 2026, and with each opening lease revenues will come in that will allow better cost absorption. Cost will go up as more hangars will also increase the depreciation, which is non-cash, and operating expenses but other than that the cost base should be relatively benign. The company will also execute ground leases for Chicago, which will become its highest grossing area per square footage and there are plans to add two other airports which will have even higher revenue per square footage. So, we also see the company climbing the square footage ladder as it adds more premium locations to its portfolio.

Is Sky Harbour Group Stock A Buy?

I normally use EV/EBITDA valuations to determine stock price targets and the reality is that given the negative EBITDA and the start-up nature of the business, EV/EBITDA valuation is not a sensible way to value the business. The company initially outlined that its peers were trading at 27.5x EBITDA and if we were to apply this 2025 earnings estimates divided by 21.85 million shares outstanding, we get a price target of $17.10 per share providing around 120% upside.

Conclusion: Sky Harbour Group Has A Lot Of Potential

I previously had a hold rating on Sky Harbour Group stock, in part because of the challenges to value the business. There aren't many peers of which valuation is known, but using a simple EBITDA multiple method shows a significant upside. Obviously, since this is a starting business, there are risks but quarter-over-quarter and with the simple EBITDA valuation method, I do feel comfortable reinstating a speculative buy rating for the stock.

For further details see:

Sky Harbour Group: Harvesting Ultra High Premium From The Ultra Rich (Rating Upgrade)