SKY - Skyline Champion: A Robust Balance Sheet Buffers Against Strong Headwinds

2023-03-28 06:24:23 ET

Summary

- Over the past year, the company's share price appreciated by about 21% despite strong headwinds in the industry.

- It utilized the reduced backlogs to boost customer satisfaction, ultimately enhancing the customer experience.

- Skyline Champion can use its robust and stable balance sheet to overcome adverse economic conditions.

Investment Thesis

Skyline Champion Corporation ( SKY ) operates in producing and selling factory-built housing in North America and the United States. It offers modular and mobile/manufactured homes, buildings, park models, accessory accommodation units, and recreational vehicles; it provides installation and set-up services for factory-built homes and transportation of recreational vehicles and constructed houses. The company builds homes under renowned brands in the housing industry.

Over the past year, the company's share price appreciated by about 21% despite strong headwinds in the industry. The company took advantage of the reduced backlogs to enhance customer experience, which, in my opinion, was crucial for the company's resiliency in a very challenging macroeconomic environment. These headwinds include lower purchasing power that lowers the demand for new homes and buildings, high-interest rates, and inflation. In addition, retailers continue to reduce their inventory due to low purchasing power and high carrying costs, affecting distribution along the supply chain.

Despite the adverse conditions, the company has attained high profitability and maintained a strong balance sheet with low debt risk, liquidity, and sufficient cash flows. The aforementioned challenges persist, but with its solid balance sheet, the company is suited to wither the storm and maintain its profit margins. With the company's resiliency demonstrated by its rising share price and good profit margins, its solid balance sheet is a potent weapon for weathering this storm and propelling growth.

Headwinds

As previously mentioned, several challenges affect the homebuilding industry. Firstly, soaring inflations and high-interest rates have lowered consumer purchasing power, reducing demand for new homes and triggering a decrease in houses sold. The number of homes sold in the MRQ in the U.S. decreased by 1.4% to 5749 from 5830 in the prior year. The number of factory-built homes sold in Canada decreased from 336 the previous year to 273.

Inflations in the construction sector hit 6% over the past year, and an average of 4.7% are expected this year. Although inflation is simmering, the prices of building materials and other inputs related to construction projects are still over the top. With high input costs, gross profit margins are bound to reduce, and SKY is no exception. Its gross profit margin was 31.55% and was outperformed by the sector, with a median of 34.99%. This can also be explained by an uptick in selling, general and administrative expenses (SG&A) from $65.8m during the past year to $71.8m due to extra investments in acquisitions, expanding capacity, and improving online customer purchasing experience. The company increased the prices of units sold to offset the inflation and increased SG&A expenses.

Retailers continue to reduce the amount of inventory due to weak demand and increasing carrying costs. Their efforts to adjust to the pace of order placements have affected distribution along the construction supply chain. As a result, SKY's production volumes have decreased slightly, and their total backlogs reduced from $814m as of 1st October 2022 to $532m as of 31st December 2022.

These headwinds are persistent and are expected to continue; however, the company has been able to adapt to the prevailing adverse conditions. It has seen positive demand in certain markets due to normalized backlogs. In addition, the average selling price at which homes are sold in the U.S. has increased to counteract high costs. In my opinion, these events will positively influence their profits and revenues.

Profitability

The sector slightly outperformed SKY's gross profit margin TTM by about 3.44%. However, the company has improved to 31.55% from 26.67% in the preceding year. In my opinion, the company records attractive and promising gross profit margins. It also attained a net income margin of 15.65% which, compared to the industry's median (4.65%), indicates that the sector was outperformed, a fair demonstration of the company's profitability compared to its peers. The figures above can be attributed to the higher average selling price per house sold and increased retail sales. The increased retail sales resulted from the company's retail expansion operations.

It is essential to evaluate the company's effectiveness in generating profits/income from its equity financing. The company's return on equity was 45.19%, while the industry's median was 11.05%. SKY significantly outperformed the industry, signaling that investors are getting good returns on their investment in addition to the company utilizing its equity suitably.

Moreover, SKY has cash from operations at $424.1m, an increase from the past years' $224.5m. An increase in revenues explains the growth in cash flows. The company's CFO also exceeds the industry's ($151.7m). These figures suggest that the company generates more cash from its operations than it uses to fund them.

I expect the company to continue generating profits. The company's higher pricing and supplementary investments will aid the company in earning more revenues and improving its profit margins. SKY also takes advantage of the reduced and normalized backlogs that enable them to meet their clients' demands and mitigate the risk of cost overruns.

Solid Balance Sheet

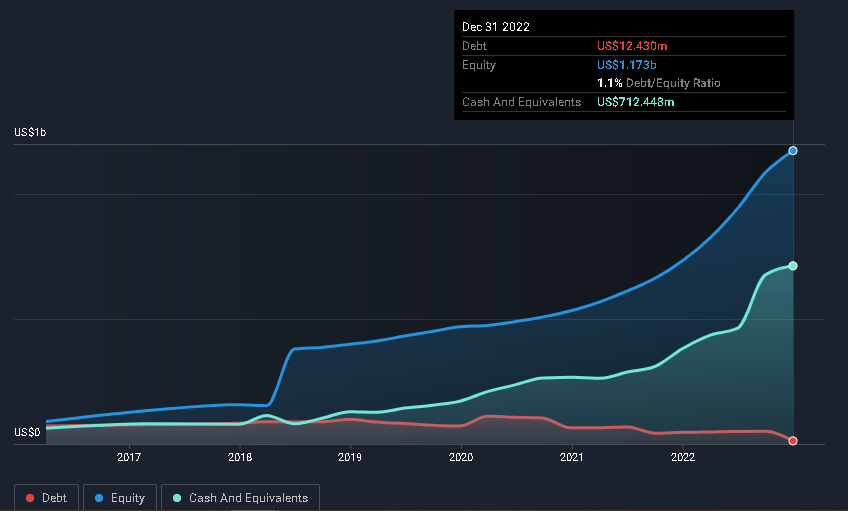

As mentioned earlier, the company has a strong balance sheet. Considering the company's liquidity position, it is reassuring to note that it has a cash balance of $712.45m more than its debt of $12.43m resulting in net cash of $700.02m. Its current ratio is approximately 3.8 conveying the firm's ability to cover its immediate obligations. SKY can cover its current liabilities with its current assets by roughly 3.8x, which assures its financial strength in the short term.

Simply Wall Street

Besides its high liquidity, the company has a debt of $12.43m and a market cap of 3.91b, which is about 314x the amount of debt, showing that the company has very low leverage. Its total equity is at $1.173b and a resulting debt-to-equity ratio of 1.1%, indicating the company is highly deleveraged and, therefore, free from risks such as bankruptcy or an increment in debt due to accumulated interest rates. SKY has been reducing its debt over the preceding five years, with its debt-to-equity ratio reducing from 53.1% to 1.1%.

{kind=link}

The company has cash amounting to $712.45m, more than its outstanding debt. In addition, its cash from operations is at $424.1m, which can cover the debt by about 34x. The interest coverage ratio is 157.08, suggesting that the interest accrued from its debt ($3.6m) can be well catered for by the EBIT ($565.5m) 157x. Ultimately, having this cash available is a positive signal that the firm can easily honor all its financial commitments.

With the existing obstacles, the company can use its robust balance sheet to its advantage and maintain its solvency. The cash flow from operations and the levered free cash flows can be used in furthering its investments in improving its online buyer purchase experience, expanding its capacity, and acquisitions to earn more profits. Additionally, they can be used in innovation and R&D efforts to bring about products and services that meet customers' demand for low-budget housing. The company also has a low debt risk, and with the upsurge in interest rates, it doesn't have to worry about paying the increasing interest obligations, maintaining its solvency.

Conclusion

Although the homebuilding industry is plagued by retailer destocking, high inflation, and interest rates, SKY has remained profitable with increasing revenues and profits. The company has taken advantage of retailers regulating order rates, reducing their backlogs, and bringing them to normal levels from the previous highs. This has enabled them to quickly deliver an excellent customer experience, resulting in increased demand for its products. Setting higher prices helped offset the high costs of inputs, thus improving their profit margins.

The company has a robust balance sheet which can help them overcome the persistent headwinds. Its high liquidity can be used to increase its investments in improving its customer's online home purchase experience, expansion, and operating expenses.

Since the firm is much deleveraged, it faces very low risks, such as increasing debt arising from increased interest charges; and bankruptcy due to defaulting payment. In my opinion, the company is in a promising position; consequently, I am bullish on the stock, and I rate it a buy for growth-oriented investors.

For further details see:

Skyline Champion: A Robust Balance Sheet Buffers Against Strong Headwinds