SKY - Skyline Champion: Capitalizing On The Unaffordable Housing Crisis

2023-03-26 10:00:00 ET

Summary

- It is estimated that 60% of the US population can't afford a traditional house.

- Skyline Champion is a leading player in the factory-built housing market, an option more than 50% cheaper than traditional housing.

- Factory-built housing sales could double over the long-term to return to its long-term average.

- Skyline has seen a phenomenal increase in its profitability in recent years and is an interesting play in this uncertain housing environment.

Housing has been a hot topic the last few years, with real estate prices continuing to climb throughout a decade of low-interest rate mortgage rates. While rising prices are great for investors, they can be devastating for a population. This trend has played out and Redfin estimated that for 2022 60% of the US population couldn't afford to buy a traditional home (assuming <30% of income spent on mortgage rates. If traditional housing construction is not an option, cheaper alternatives could see a rise in business. This is why today we'll look at Skyline Champion Corporation ( SKY ), the #2 player in the factory-built housing industry in North America.

60% of US population can't afford a traditional home (SKY Investor Presentation, Data from Redfin)

The factory-built housing industry

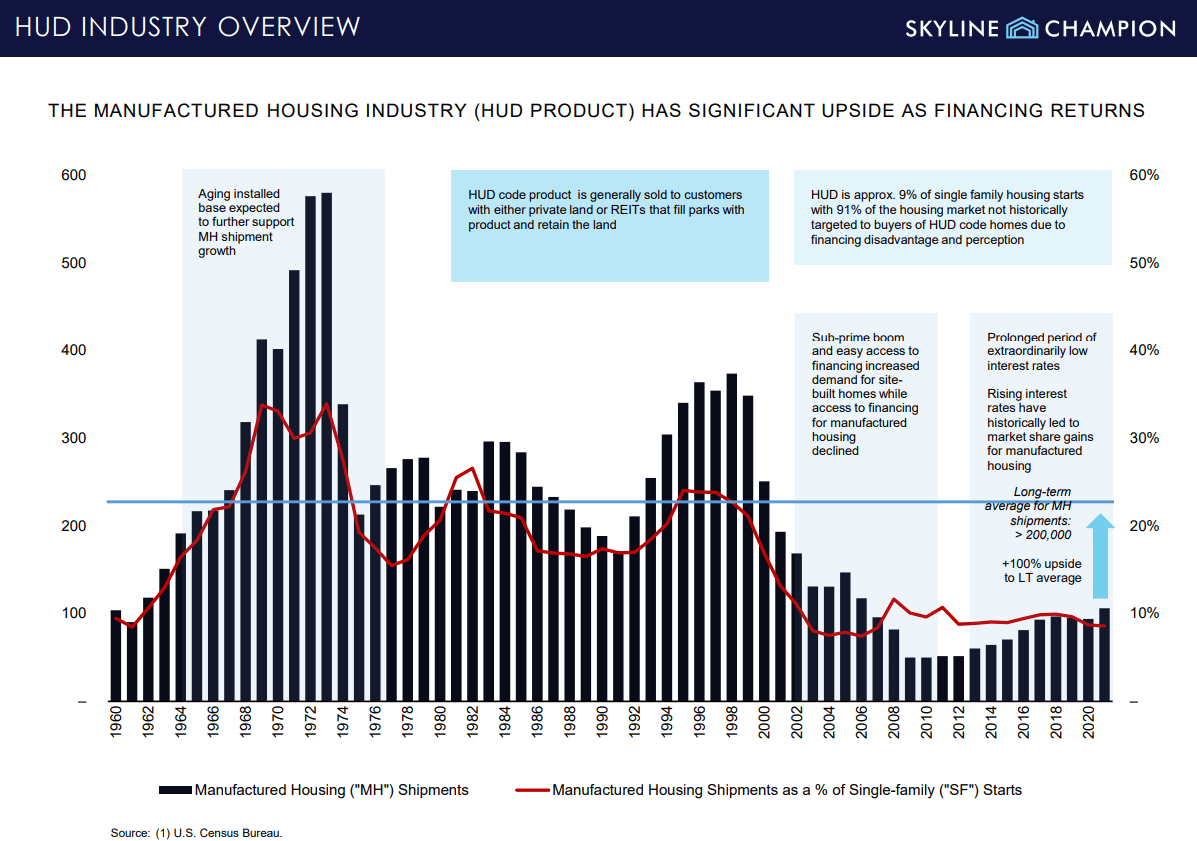

The housing industry is one of the largest and most necessary industries on the planet, thus very competitive. The chart below shows the market share and units sold for manufactured housing. HUD stands for U.S. Department of Housing and Urban Development and refers to the HUD code (National Manufactured Housing Construction and Safety Standards Act of 1974) and are guidelines for building houses. Houses that do not abide by HUD will struggle to get competitive financing options. We can see that manufactured housing is just a tiny 9% market share and has been on a secular decline since the 1970s. Especially since 2000, we can see a substantial decline in market share. A manufactured home is significantly cheaper than an on-site-built house. According to the company, the average cost of a new factory-built house within the HUD code was $106,600 in 2022, while the average cost of site-built homes was $351,700 (excluding land) in the same period.

{kind=link}

HUD Industry Overview (SKY Investor presentation)

Factory-built houses can achieve these significant savings by manufacturing in centralized, indoor facilities with standardized processes and automation. Manufacturers also can leverage scale to drive material costs down with suppliers. Factory homes are less prestigious to own than a freshly built house and thus, people would prefer to build an on-site house if they can. The era of low-interest rates has pushed shipments and market share of factory homes down significantly due to the cheap availability of mortgages. According to FRED , the national average 30-year fixed mortgage is 6.42%, a rate last seen in 2008, with the low coming in at under 3% in 2021. As mentioned above, 60% of the U.S. population can no longer afford a normal house, so I see a strong case for factory homes to gain market share and inch up closer to its long-term average of 200,000 shipments per year versus around 100,000 shipments last year. This leaves SKY in a prime position to benefit from the demand for cheap housing. According to the company, the market is valued at approximately $11.5 billion, and they have market share of 19.3% based on 26,165 homes sold in North America. Three big players make up the majority of the market:

- Clayton Homes is the largest player and a subsidiary of Berkshire Hathaway ( BRK.A ) and thus doesn't report standalone earnings. Its market share is estimated to be above 30% .

- Skyline Champion Corporation is the second largest player, with 19.3% in FY22.

- Cavco Industries ( CVCO ) is the third largest player, with around 12% of the market.

SKY has been gaining market share in recent years and if we see an increase in total shipments, then all of these three players should benefit from the additional demand.

Operating leverage

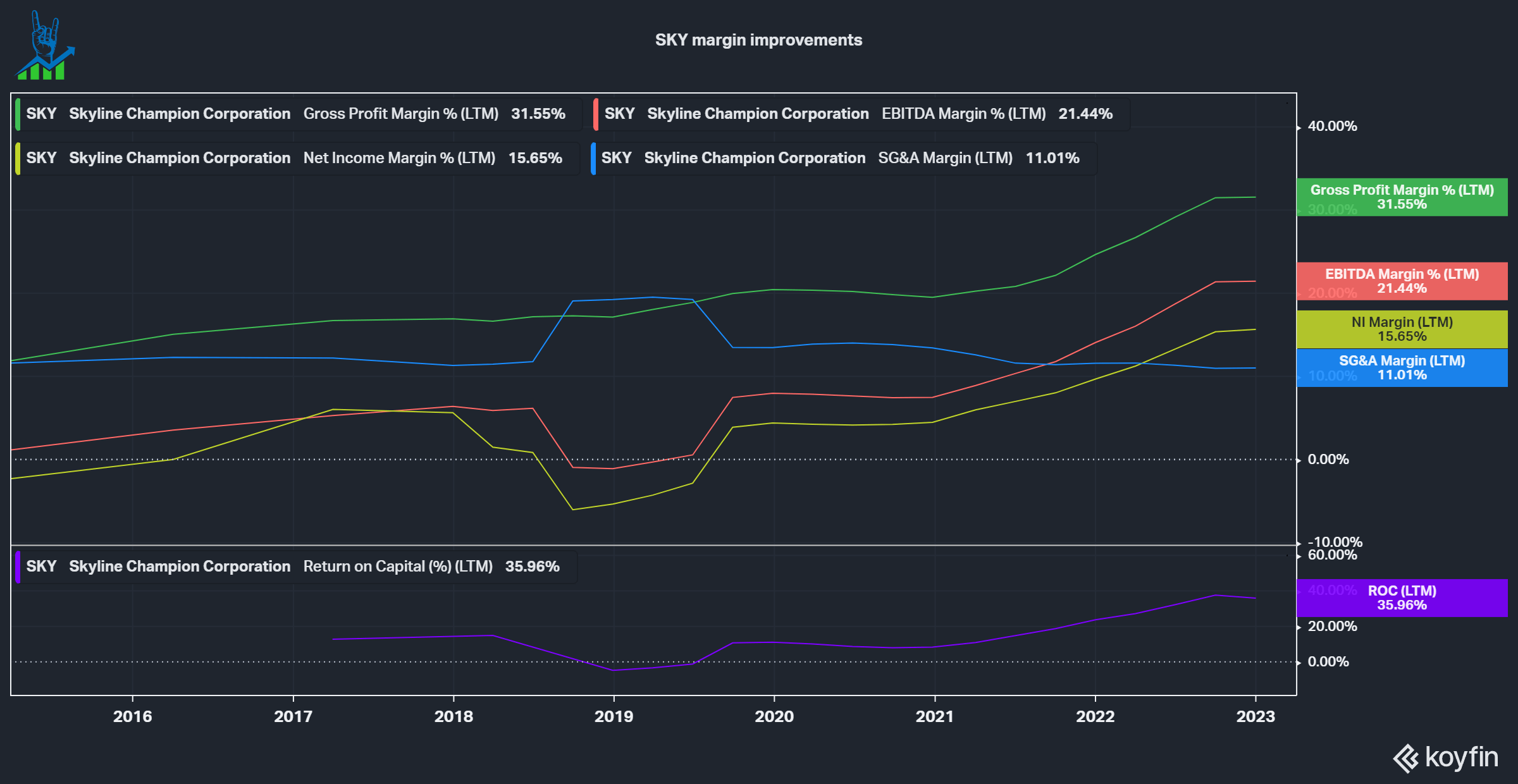

Over the last few years, the company saw remarkable gross profit and profit margin improvements. This was caused by economies of scale, continuous improvement initiatives related to procurement, operational and labor cost savings, and standardizing manufacturing processes. The company also is leveraging automation to reduce material waste, improve precision and reduce the reliance on labor. Decreasing the dependence on labor is critical because the home-building industry is no stranger to labor shortages. Furthermore, SKY is investing in its customer's digital experience. The order process is streamlined for direct customers and retailers, with dynamic display selections, options and pricing. Besides a better customer experience, SKY can also harvest more data this way and learn more about its customers' behaviors. This margin increase led to a meteoric rise in Return on Capital, which came in at 35% LTM compared to a cost of capital of around 11% .

{kind=link}

SKY operating leverage (Koyfin)

Cash flows and valuation

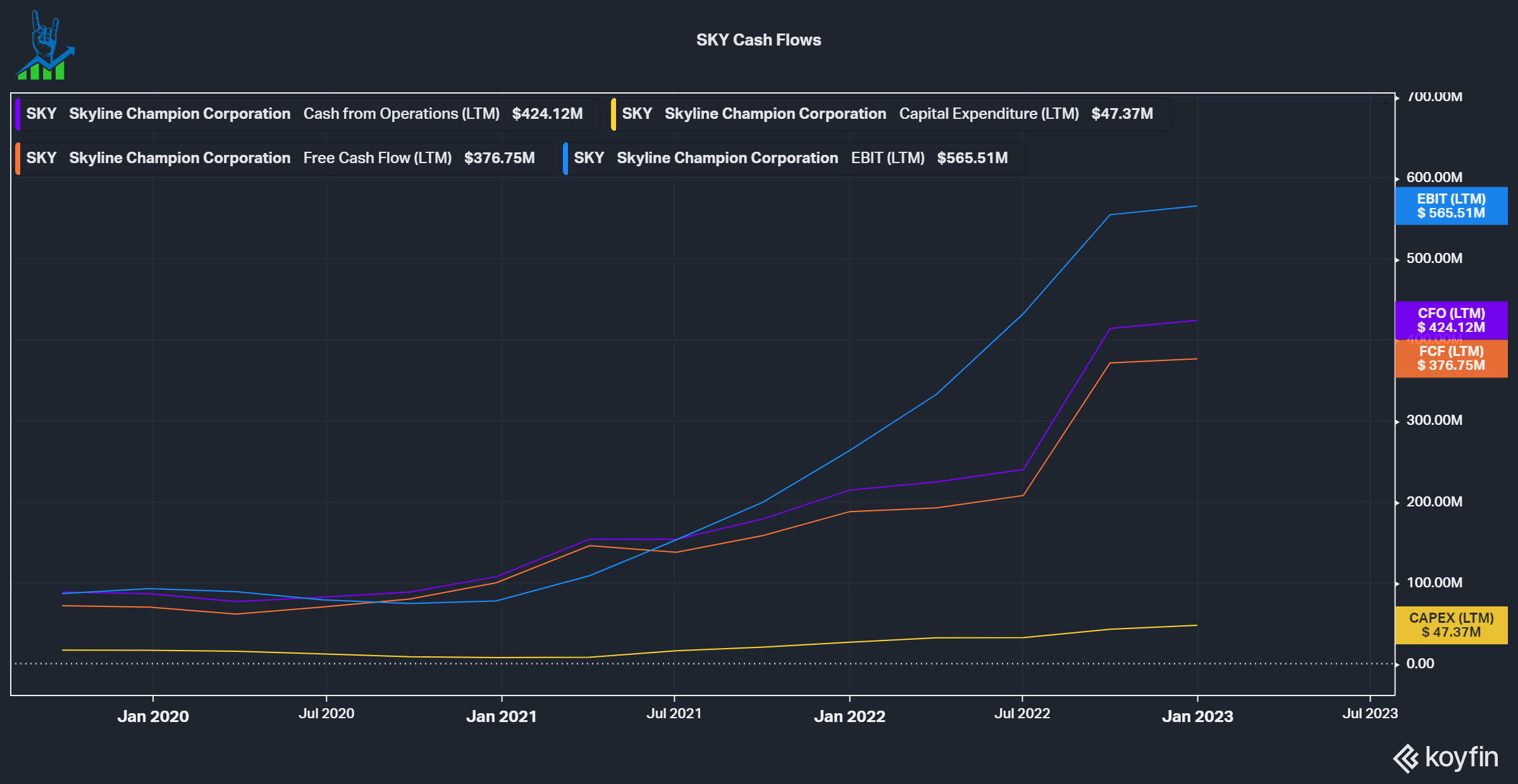

Alongside its profits, Skyline also grew its cash flows significantly. Over the last year, the company has generated $424 million in operating cash flow and $376 million in Free cash flow. CapEx came in at $47 and the company discloses that each production plant needs between $200-300k maintenance CapEx per year. The company has 41 operating manufacturing facilities, so total maintenance CapEx is between $8.2-12.3 million, leaving >$35 million of growth CapEx. I like to look at Owner earnings, which I define as Operating Cash Flow - Maintenance CapEx, to get a better view of the real cash flow to owners; for Skyline Owner earnings are around $412-416 million.

{kind=link}

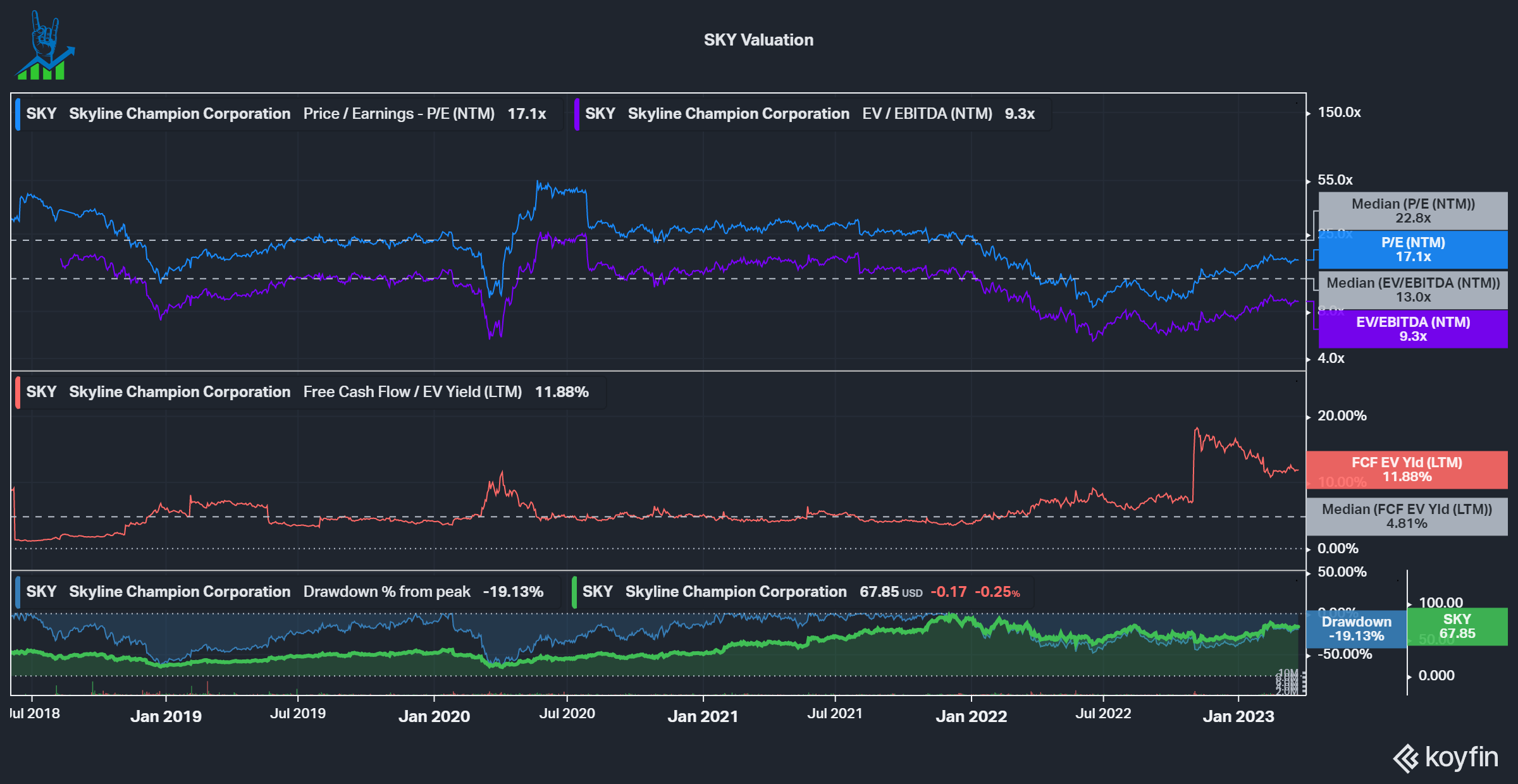

Looking at the historical valuation multiples for the company, we can see that all values are better than the average since the company merged into its current form. Especially the 11.8% FCF yield, 13% if we take owner earnings, seems very attractive, and the stellar balance sheet with $700 million in cash and just $12 million of debt. SKY looks like a good buy at these levels to benefit from a possible rebound in factory-built home sales due to the current housing affordability crisis.

{kind=link}

For further details see:

Skyline Champion: Capitalizing On The Unaffordable Housing Crisis