SKY - Skyline Champion: The Future Of Housing Dynamics In The U.S. A Hold

2023-10-07 07:38:41 ET

Summary

- SKY’s revenue has grown at a CAGR of 15% during the last decade, while EBITDA has exceeded this with a 60% rate.

- SKY is quickly becoming the premier modular/manufactured home builder, with M&A and internal development driving an improvement in its offering.

- We believe continued investment in its commercial and operational capabilities will drive value, such as expanding its retail offering and developing financing services.

- Changing housing dynamics in the US are contributing to a growing demand for modular homes. Factors such as an aging population, the need for affordable housing, and adverse weather are key.

- Although we are bullish long term, the company is currently suffering due to macro conditions. We await signs of an improvement.

Investment thesis

Our current investment thesis is:

- SKY is a well-managed business with a strong value proposition to markets. It has a strong retail presence across the US, which could be significantly enhanced if the Regional Homes deal closes. Further, it has deep expertise in manufacturing and is focused on innovating to improve customization and quality, both of which will help to convince the market to transition from traditional homes. Finally, Management is incrementally improving the business model in an intelligent way in our view, ensuring it is a leading player as the industry moves toward maturity in the coming decades (such things as creating a financing option, deepening manufacturing capabilities in key States, and acquiring peers with strategic value).

- Its segment of the industry is also highly attractive, with substantial scope for growth. Home value appreciation continues to price out individuals, which will be compounded by an aging population. Additionally, consumers have greater scope for customization, attractive pricing, and enhanced quality. Therefore, individuals are both encouraged and forced toward this segment as an alternative. From SKY's perspective, the scope for efficiency and market-leading margins is high, owing to reduced labor requirements and automation.

- Our hesitancy is due to the continued struggles expected. We await signs of a clear improvement, from which point this appears to be an attractive long-term investment.

Company description

Skyline Champion Corporation (SKY) is one of the largest and most reputable builders of manufactured and modular homes in North America. The company provides a range of housing solutions, including single-family homes, multi-family homes, and retirement community housing.

Financial analysis

{kind=link}

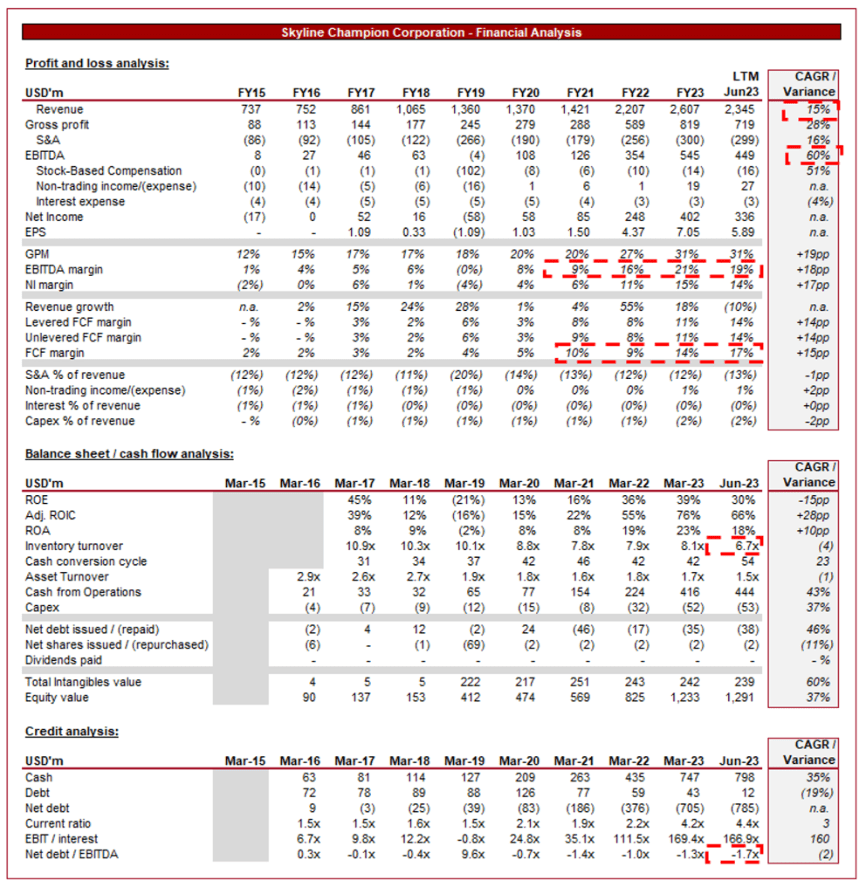

Presented above are SKY's financial results.

Revenue & Commercial Factors

SKY's revenue has grown at a CAGR of 15% during the last decade, although its YoY growth has been highly volatile, influenced by macro conditions and industry developments. EBITDA has outperformed this significantly, with a CAGR of 60%.

Business Model

SKY designs and manufactures manufactured homes and modular homes. Manufactured homes are constructed entirely in a factory and then transported to the home site, while modular homes consist of multiple factory-built modules that are assembled on-site. This is an innovative approach to home building, stemming from an increased need for affordable housing as the US population has rapidly improved. This has been accelerated by changing accommodation dynamics, as individuals have been forced out of metropolitan areas due to house price inflation.

The company offers a diverse portfolio of housing solutions to cater to various customer needs, including single-section manufactured homes, multi-section manufactured homes, modular homes, and park models for recreational use. The company sells its homes through a network of independent retailers, builders, and manufactured home communities. This distribution strategy ensures broad market reach, which is critically important to the development of the modular homes segment as it creates brand awareness.

SKY allows customers to personalize their homes, offering a range of floor plans, finishes, and design options. This customization ability is a major selling point compared to the existing housing market, both the newly built segment and the primary market. SKY reduces the stress associated with the customization process, as it ensures consumers can only search for designs/homes that are in line with state building codes.

SKY has pursued strategic acquisitions to expand its product offerings and geographic presence. We believe this is an important complementary strategy given the rapidly changing industry developments. It is extremely important for SKY to incrementally increase its scale, as well as maintain a market-leading offering, so as to build the segment's barriers to entry.

Most recently, SKY agreed to acquire Regional Homes , which will contribute $523m of revenue and $84m of EBITDA. Regional Homes is the 4th largest company within the industry, with the largest independent retail footprint. It has strong relationships with federal and state disaster relief housing programs in key states such as Florida and Texas. This acquisition would materially bolster SKY's total retail footprint (Regional Homes is providing 43, Champion has 31), while providing it access to the Alabama market and greater penetration in Louisiana and the Carolinas.

Management's rationale for the transaction is:

- The combination of the #2 and #4 largest companies within the industry should ensure material economies of scale and commercial benefits through a shared go-to-market strategy.

- Geographical expansion and access to manufacturing hubs.

- Materially strengthens SKY's retail operations, positioning it perfectly to accelerate its digital, direct-to-consumer, and builder developer channels. This should support margins and enhance growth in the coming years.

- With the expansion of its retail operations, SKY is positioned to expand its finance offering, generating another, more stable, revenue stream. SKY has partnered with ECN Capital/Triad to develop its financing capabilities.

We consider this a very good acquisition. There is a clear development of the business model beyond just acquiring greater scale. We are particularly bullish about the expansion of its retail capabilities, as this will future-proof the company as the industry moves toward maturity.

Home building industry

The US modular construction industry is expected to grow well into 2030, with a CAGR of 7.8%. With historically strong population growth and inward migration, the US market is positioned well for growing demand for homes. When considered in conjunction with technological development and economic growth, the modular construction industry is well-placed to benefit.

The off-site building process provides the benefit of higher efficiency. This is due to reduced labor costs and material wastage given the conditions are controlled in a factory, with large scope for automation and process-driven construction. This has the broader benefit of reducing the issues associated with on-site accidents and increasing quality through standardization. Over the long term, the reduced labor required and consistent quality will mean this segment of the wider home-building industry will have superior margins.

Skyline Champion faces competition from other manufactured and modular home builders, including Cavco Industries ( CVCO ), Clayton Homes, and Palm Harbor Homes.

We believe the following industry trends will materially impact growth in the coming years:

- Affordable Housing Demand - SKY benefits well from the demand for affordable housing solutions, which will only grow in importance given the appreciation of home value is consistently exceeding earnings growth in most regions. Manufactured and modular homes offer a cost-effective alternative to traditional site-built homes.

- Demographic Trends - As the U.S. population continues to age, there is an ongoing need for housing solutions for both first-time homebuyers and retirees, partially due to the point made above. With a strain on pensions already expected, housing will likely also be an issue.

- Customization and Innovation - It is worth reiterating again that customization is a key selling point associated with modular homes. In addition to this, we see greater scope for all-round innovation compared to the traditional market. This innovation can come both on the commercial side, with greater customization and response to sustainability requirements, and also from an operational prospectively, namely cheaper and more automated production.

- Climate Change / Adverse Weather - Climate change / Adverse weather is contributing to property damage, and in many cases, destruction across the US, particularly in States such as Florida. These are key markets for the modular home movement as the value proposition is clear. Homes can be built far quicker and cheaper, representing a reasonable response to the threats associated with destruction.

- Geographic Expansion - The demand for modular homes is currently uneven across the US, with some States naturally more accelerated in the transition (for the reasons stated above, such as price and climate change). We are broadly expecting an improvement across most States over time, however.

- Market Consolidation - The manufactured housing industry will inevitably experience a period of consolidation in the coming years as it moves toward maturity. SKY appears positioned well to continue its selective acquisition approach, with sufficient cash to maintain this approach in the medium term. We would like to see Management be aggressive in developing high barriers to entry and an insurmountable competitive position.

Margins

{kind=link}

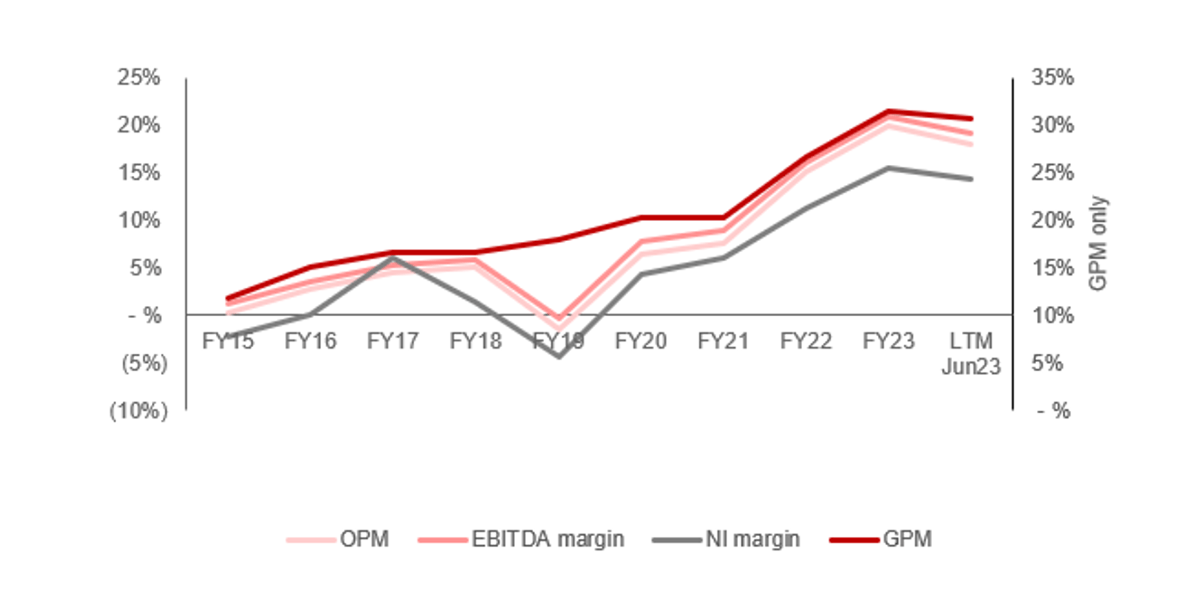

SKY's margins have been difficult to assess, as they have inconsistently improved over the historical period, followed by a substantial increase in the post-pandemic period. This is likely the biggest area of uncertainty in our view, given the lack of normalized trading from which to assess the current earnings potential for the company.

Quarterly results

SKY's financial performance has degraded in recent quarters, with its last 4 top-line growth rates being +53.9%, +8.9%, (23.0)%, and (36.0)%. This is a reflection of current macro conditions, with a significant decline in demand as funding availability is constrained and consumers see a decline in their financial health.

We believe the issues will continue in the coming 6-12 months, although with some improvement in the second half of that period. With inflation remaining concerning, it is unlikely we will see an aggressive move to cut rates, contributing to an extended period of elevated funding requirements. This will have a compounding impact on consumers' finances and dissuade a significant increase in homebuilding.

As the following 3 charts illustrate, the current home buying/affordability situation in the US is far from ideal. US housing affordability has reached a record low, falling below 100. Secondly, US housing starts have sequentially declined and are in a downward trend, implying the outlook by builders is negative (Starts fall if builders believe they will not make an adequate return when the property is ready for sale). Finally, existing home sales are performing even worse, reflecting the inability to finance new acquisitions and a broadly conservative financial approach by individuals.

The key takeaways from the company's most recent quarter are:

- U.S. homes sold decreased (29.3)% - This is the primary revenue driver currently, reflecting macro conditions.

- Total backlog decreased (15.7)% to $260m, implying a softening of this negative trajectory.

- The average selling price ("ASP") per U.S. home sold decreased (8.2)% to $89k, which is better than we would expect. Management is clearly attempting to protect margins to the extent possible.

- Management believes the business is returning to "normal levels" of orders and backlog, which means higher than current orders and a continued decline in backlog. We will be interested to see how this increase in orders develops in the coming months given the decline thus far.

- Management is focusing on what it can control, operational improvement. operational capabilities have assisted with mildly offsetting the substantial margin pressures, despite lower production rates and consumer shifts to smaller, less optioned homes.

Balance sheet & cash flows

SKY's balance sheet is fairly clean, with no material debt usage. Given the risks associated with the business and its financial volatility, this is the correct decision and limits downside risk. This reiterates that the company is positioned perfectly to conduct further M&A in the coming years to consolidate a market-leading position.

The slowdown faced is illustrated in the company's inventory turnover, which has declined substantially relative to its pre-pandemic levels. We believe monitoring this statistic relative to revenue will be critical to understanding when demand levels begin improving.

Cash flows have been materially retained and reinvested within the business. Given its current size and trajectory, we are broadly comfortable with this strategy. We suspect distributions will be lacking in the coming years.

Outlook

{kind=link}

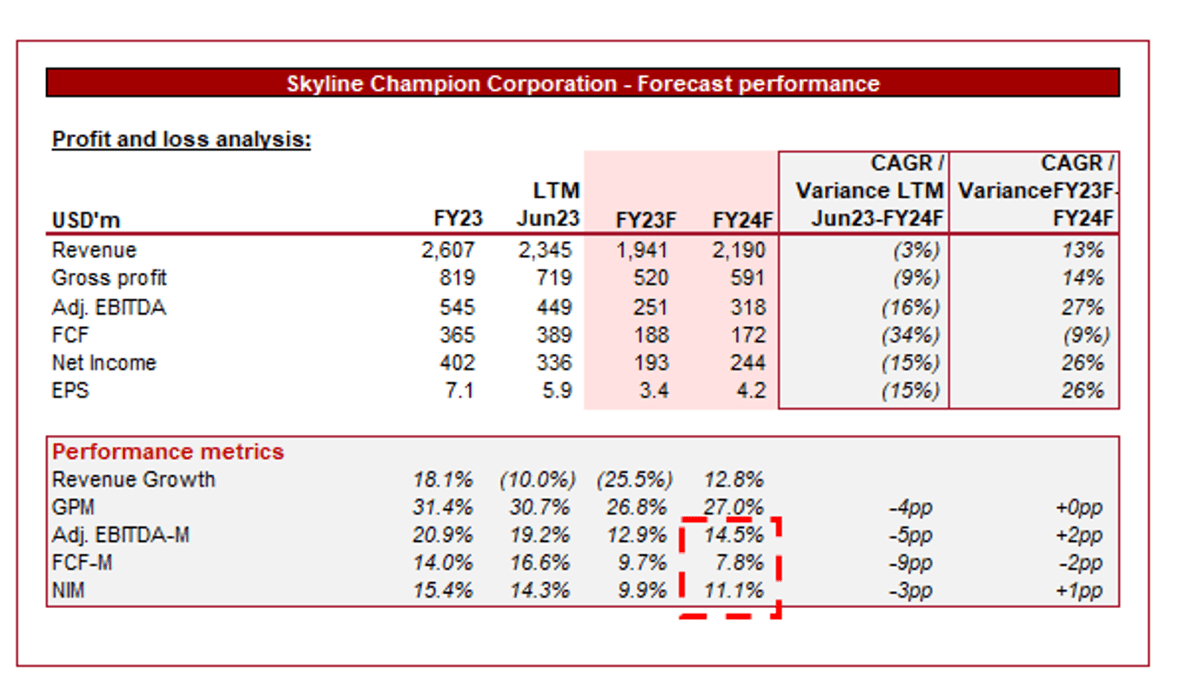

Presented above is Wall Street's consensus view on the coming 2 years.

Analysts are forecasting a decline in revenue growth, with a CAGR of (3)% into FY24F. In conjunction with this, margins are expected to also decline, although importantly, remain above a 10% EBITDA (pre-pandemic level). This likely excludes any assumptions associated with Regional Homes.

We concur with the revenue assessment, as cooling demand for homes and higher interest rates mean that home-building activity will rapidly soften. This is highly likely in the near term, as the impact of affordability and rates will likely overhang in the years to come.

Further, as demand softens, a natural development is for margins to follow suit, likely to an aggressive level given how fast revenue increased after FY21. We are less confident that the business will normalize at an EBITDA-M of 13-15%, mainly due to the business already being at this level while revenue continues to fall. This said, exceeding 9% appears reasonable given the increased scale and product innovation. We would conservatively suggest 11-14%, which implies the acquisition of Regional Homes would be accretive.

Industry analysis

{kind=link}

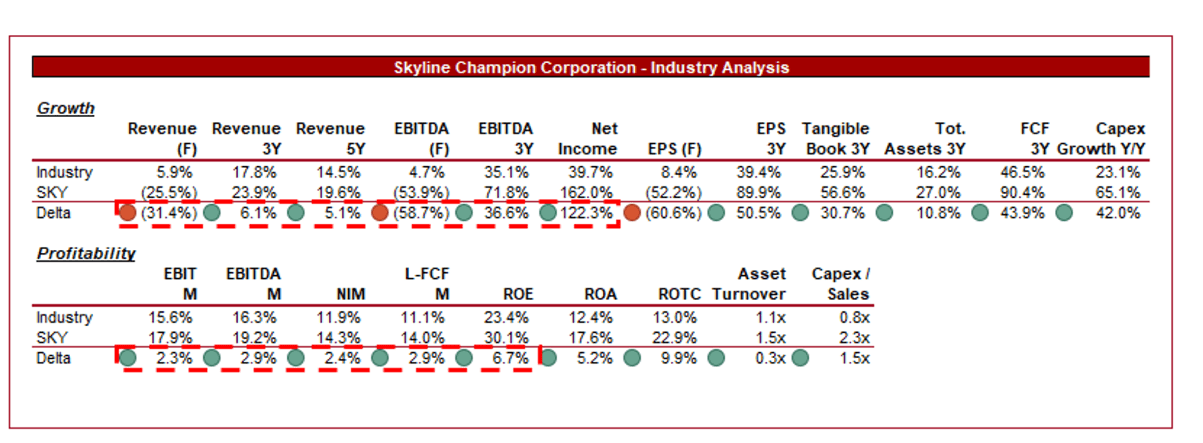

Presented above is a comparison of SKY's growth and profitability to the average of its industry, as defined by Seeking Alpha (23 companies).

SKY performs respectably relative to its peers, all of whom are currently struggling with macroeconomic conditions. The company has achieved superior revenue growth, while its margin improvement has also allowed it to outperform in profitability growth. This is a reflection of its innovative product type, with demand spillover as supply has lagged. This said, its non-traditional approach leaves SKY more susceptible to a downturn, with its forward revenue materially behind the market.

SKY's profitability is currently comfortably above the industry average, owing to the impressive run-up achieved in recent years. This said, the business is on a downward trajectory and as the forward estimates suggest, SKY is more greatly exposed on the downside. Based on our estimate, SKY is likely to fall below the industry average.

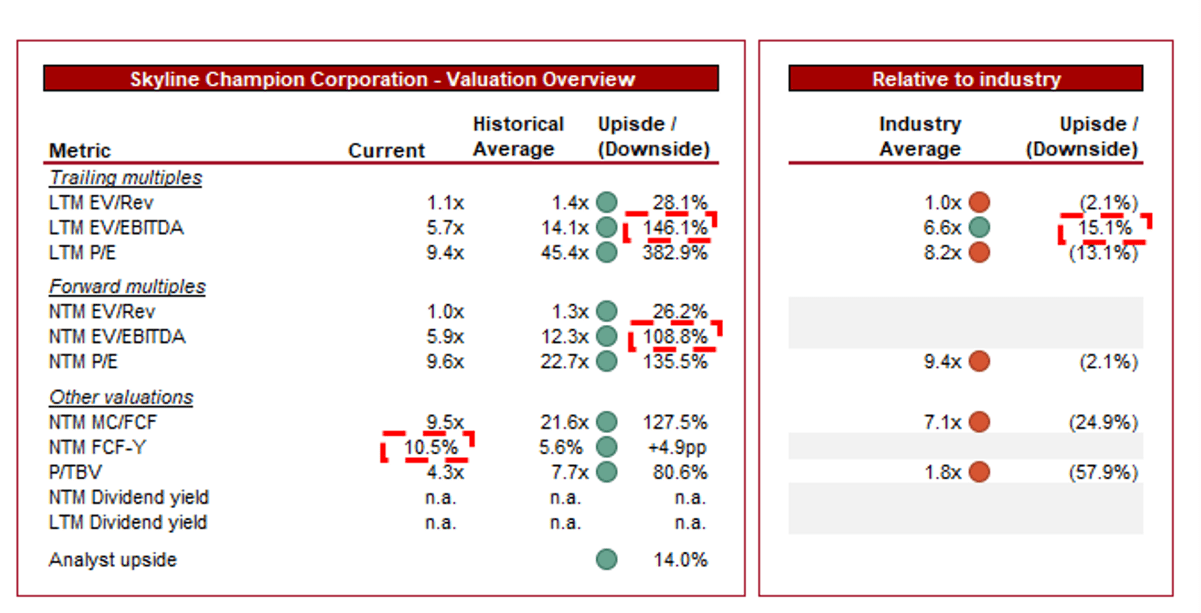

Valuation

{kind=link}

SKY is currently trading at 6x LTM EBITDA and 6x NTM EBITDA. This is a discount to its historical average. SKY's historical trading period is limited and so this consideration is not deemed wholly valuable.

SKY is trading at a small EBITDA discount to its peers, while all other metrics are at a premium. We are hesitant to suggest a near-term premium is justifiable, owing to the struggles ahead and the difficulty with achieving consistent growth and margin stability. This said, many of the issues the company faces are shared by its peers, which limits the valuation concerns.

From an absolute basis, SKY is trading at a 10.5% NTM FCF yield, a level we consider attractive but not necessarily when considered relative to risk levels. With margin erosion and a lack of demand, this FCF yield will likely fall. An alternative way to look at this is the Regional Homes transaction multiple, which was 5.5x '22 EBITDA. This implies a small upside. With the lack of near-term catalysts to drive share price appreciation, we believe patience is key.

Final thoughts

SKY is a highly attractive business that is positioned to perform extremely well in the coming decades. Its business model has develop well, with Management clearly extremely competent and cognizant of incrementally improving the business through the various levers at their disposal.

The industry is experiencing tailwinds that are expected to accelerate over time, contributing to a step change in demand sequentially in the coming decades. As one of the largest players in the market, we believe SKY will enjoy a disproportionate share of this growth.

The company is far from perfect, however, although this is attributable to the market today. The industry is still highly cyclical and the building segment is currently in a bear market. Given this is expected to continue, it is difficult to rationalize a buy rating currently. We await signs of an improvement.

For further details see:

Skyline Champion: The Future Of Housing Dynamics In The U.S., A Hold