SKY - Skyline Champion: Worth Considering At Last

- Skyline Champion has exhibited attractive growth over the past several months despite fears associated with the broader economy.

- Despite its strong performance, shares have fallen at a pace that was faster than the market's decline.

- While the business could very well experience some pain in the future, it is fundamentally robust and finally attractive enough to consider buying for the long haul.

Generally speaking, references to the housing market are references to companies that build traditional homes. But there are other forms of accommodation out there that warrant attention. One example of this would be factory-built housing which, in the age of ever-rising property prices, has become an affordable means for those who are lower income to participate in the housing experience. One significant player in this market, with a roughly 19% stake in the manufactured housing space in the US and with a 2.6% share of the total housing market in the country, is Skyline Champion ( SKY ). General fears concerning the broader economy, combined with the fear that higher interest rates will weaken the demand for housing, have ultimately led to shares of the business taking a dive in recent months. However, the overall fundamental condition of the company remains robust and its growth recently has been encouraging. Although the company may face some headwinds in the near term, the stock does now look cheap enough to warrant some serious consideration from value-oriented investors.

The picture has improved

Back in January of this year, I wrote an article detailing what I thought was the investment worthiness, or lack thereof, of Skyline Champion. In that article, I said that the company's growth had been really impressive recently, particularly during its 2021 and 2022 fiscal years. Ultimately, I said that if that growth continued, shares might offer investors some nice upside potential. But given how expensive shares were at that time and considering all that was going on with the housing market and the economy, I ended up rating the enterprise a ‘hold’, reflecting my belief that its returns would more or less match the broader market for the foreseeable future. So far, this conclusion was not too far off. While the S&P 500 is down by 16.1% since that article's publication, shares of Skyline Champion have generated a loss of 23.7%.

{kind=link}

Author - SEC EDGAR Data

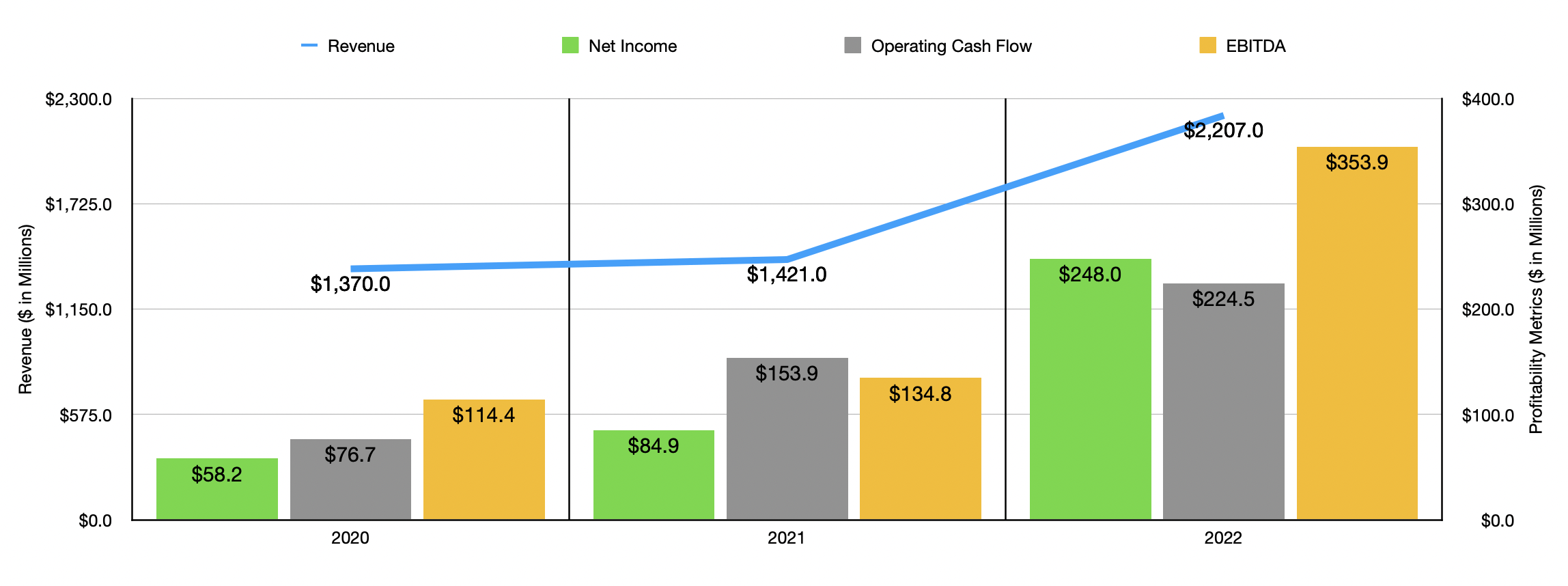

Given how poorly shares have performed on an absolute basis, your first thought might be that the fundamental condition of the firm was deteriorating. But that couldn't be further from the truth. When I last wrote about the firm, we only had data covering through the first half of its 2022 fiscal year. As of today, data now extends through the entirety of its 2022 fiscal year . For that year as a whole, revenue for the company came in strong at $2.21 billion. That represents an increase of 55.3% over the $1.42 billion the company generated just one year earlier.

This rise in sales was driven by a couple of different factors. For instance, the number of homes that the company sold in the US market came in at 24,686. That represents an increase of 23.5% over the 19,983 homes that it sold in the US market in 2021. In addition to benefiting from a rise in properties sold, the company also saw the average selling price of its properties rise by 27.3% from $63,400 to $80,700. In Canada, the company sold 1,479 homes, up 20.1% from the 1,231 it sold in 2021. And the average price per home there rose from $82,300 to $107,600. This rise in revenue brought with it a significant increase in profitability. Net income rose from $84.9 million in 2021 to $248 million in 2022. Operating cash flow went from $153.9 million to $224.5 million, while EBITDA increased from $134.8 million to $353.9 million.

{kind=link}

Author - SEC EDGAR Data

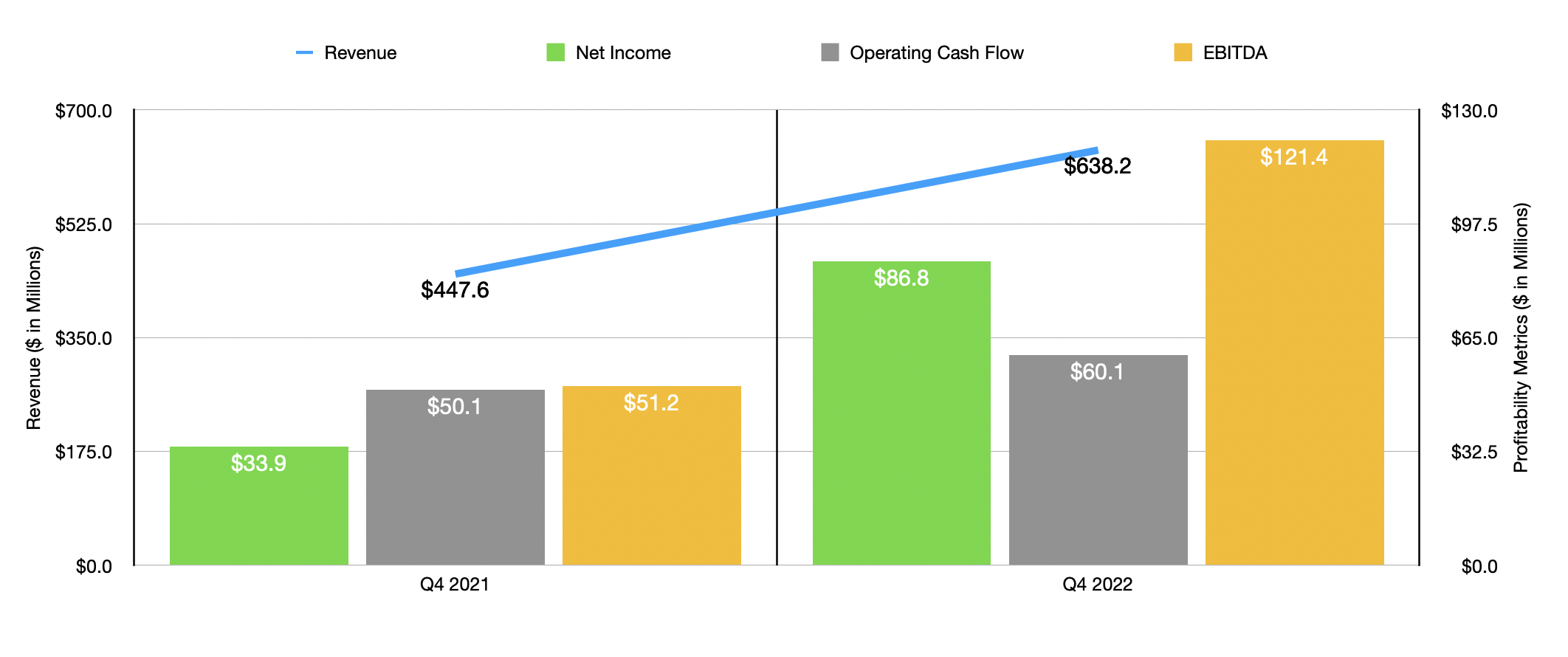

To be clear, the company's strength remained strong in the final quarter of the year. Revenue of $638.2 million achieved in the final quarter of its 2022 fiscal year translated to a year-over-year increase of 42.6%. Over that same window of time, net income skyrocketed from $33.9 million to $86.8 million. Backlog rose from $50.1 million to $60.1 million, while EBITDA more than doubled from $51.2 million to $121.4 million. Unless the company experiences a meaningful change in the contracts that it currently has, it's also likely that the near-term outlook for the firm is positive. After all, the latest quarter ended with the company having backlog of $1.6 billion. That's up from the $1.5 billion reported just one quarter earlier and it compares to the $858.6 million in backlog the company had at the end of its 2021 fiscal year. Even if the company does experience a weak spot, it's worth noting that the firm has cash in excess of debt right now of roughly $423 million. That's quite a lot of excess cash that it can rely on should times get difficult.

{kind=link}

Author - SEC EDGAR Data

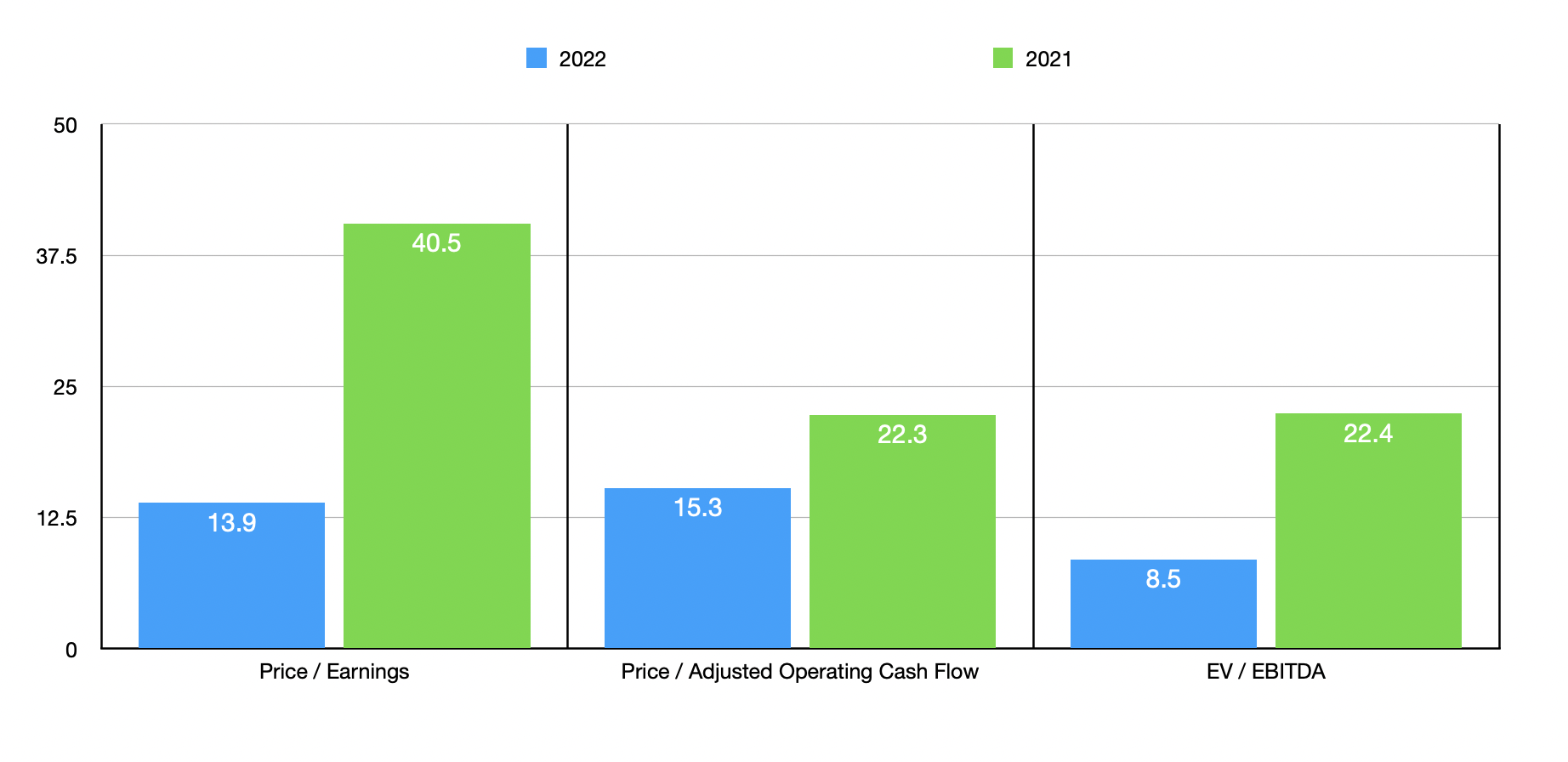

Based on the most recent data available, shares of the company might still be considered expensive compared to other housing firms. But on the whole, I would consider shares to be fairly affordable. Using 2022 results, the firm is trading at a price-to-earnings multiple of 13.9. That compares to the 40.5 reading that we get if we use 2021 results. The price to operating cash flow multiple should be 15.3, down from the 22.3 if we use 2021 data. And the EV to EBITDA multiple should come in at 8.5. That compares to the 22.4 we get from the 2021 results. To put the pricing of the company into perspective, I also compared it to five other housing companies. On a price-to-earnings basis, these companies ranged from a low of 2.9 to a high of 10.2. And using the EV to EBITDA approach, the range was from 3.5 to 6.6. In both cases, Skyline Champion was the most expensive of the group. Meanwhile, using the price to operating cash flow approach, the range was from 5.6 to 25.7. In this case, our prospect was cheaper than all but two firms.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Skyline Champion |

| 13.9 |

| 15.3 |

| 8.5 |

| Meritage Homes ( MTH ) |

| 4.1 |

| 25.6 |

| 3.5 |

| Century Communities ( CCS ) |

| 3.5 |

| 25.7 |

| 3.8 |

| Beazer Homes USA ( BZH ) |

| 2.9 |

| 16.9 |

| 6.6 |

| Legacy Housing Corporation ( LEGH ) |

| 10.2 |

| 5.6 |

| 5.4 |

| Lennar Corporation ( LEN ) |

| 5.7 |

| 13.4 |

| 4.6 |

Takeaway

The data shown right now suggests to me that the fundamental condition of Skyline Champion is quite robust. The company has plenty of cash to weather a rather difficult market. Having said that, while shares of the firm are definitely affordable from an absolute basis, they are rather pricey compared to other, admittedly more traditional, homebuilders. But given the low price point of the homes that it sells and the persistent housing shortage in this country, I have to imagine that it will fare better than other types of companies in this space should we actually experience some pain. In all, I feel as though the risk-to-reward payoff now tilts slightly in favor of buying the stock, leading me to increase my rating on it from ‘hold’ to ‘buy’.

For further details see:

Skyline Champion: Worth Considering At Last