SLTTF - Slate: Another Office REIT Slashes Dividends

2023-04-06 10:56:25 ET

Summary

- The pains and pressures of office REITs have been palpable for some time.

- With Slate, just like with True North Commercial REIT, the writing was on the wall before the distribution cut.

- The wreckage leaves the stock at a huge discount to NAV.

- We look at whether you should consider a position here.

Note: All amounts discussed are in Canadian dollars and all prices reference the stock on TSX. No reference is made to the OTC trading stock price.

Sometimes luck plays a bigger role than intelligence or due diligence when it comes to investing. We certainly were extremely lucky as we exited Slate Office REIT ( SOT.UN:CA ) ( OTC:SLTTF ) near $5.00 in late 2021.

While we were aware of the malaise in the sector, we definitely would not have predicted that things would get so bad. Instead we exited as the debt to EBITDA made us uncomfortable. The stock has now halved since then and Slate announced rather difficult news for investors yesterday.

The REIT is also announcing the conclusion of the comprehensive review of strategic alternatives undertaken by the REIT and its external advisors and a corresponding unitholder value preservation plan (the "Plan"), under which the REIT will amend its monthly cash distribution from C$0.0333 per trust unit of the REIT to C$0.0100 per trust unit of the REIT. This amendment of the REIT's distribution policy is expected to provide an additional C$23.9 million of cash annually, which will be used to strengthen the REIT's balance sheet and liquidity.

The Plan will provide the REIT with the flexibility and capital to continue strengthening its core business, including maintaining and growing operating cash flow, proactively leasing vacancies in the REIT's portfolio (the "Portfolio"), and evaluating other initiatives that may surface value for the REIT. The REIT's Board of Trustees (the "Board") unanimously believes the Plan is the most prudent way to preserve value for unitholders in the current macroeconomic environment while also ensuring the REIT is well positioned for long-term performance. As a result of the conclusion of the review of strategic alternatives, the special committee of independent members of the Board was dissolved on April 4, 2023.

Source: Slate Office

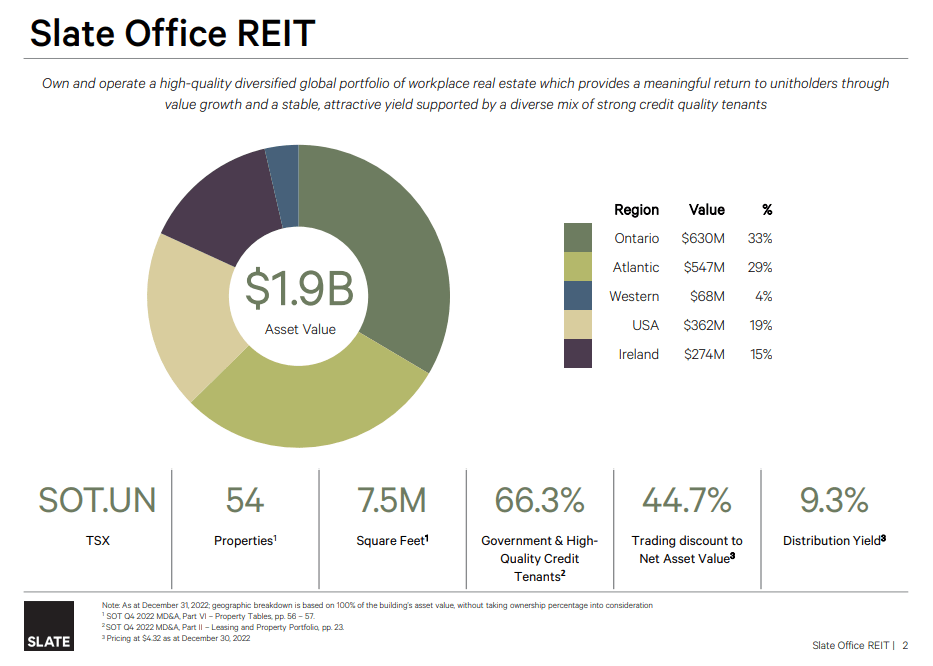

A Brief Overview

Slate owns office real estate in three countries. Based on the Q4-2022 presentation, about a third of this was in Ontario and a third distributed between the US and Ireland.

{kind=link}

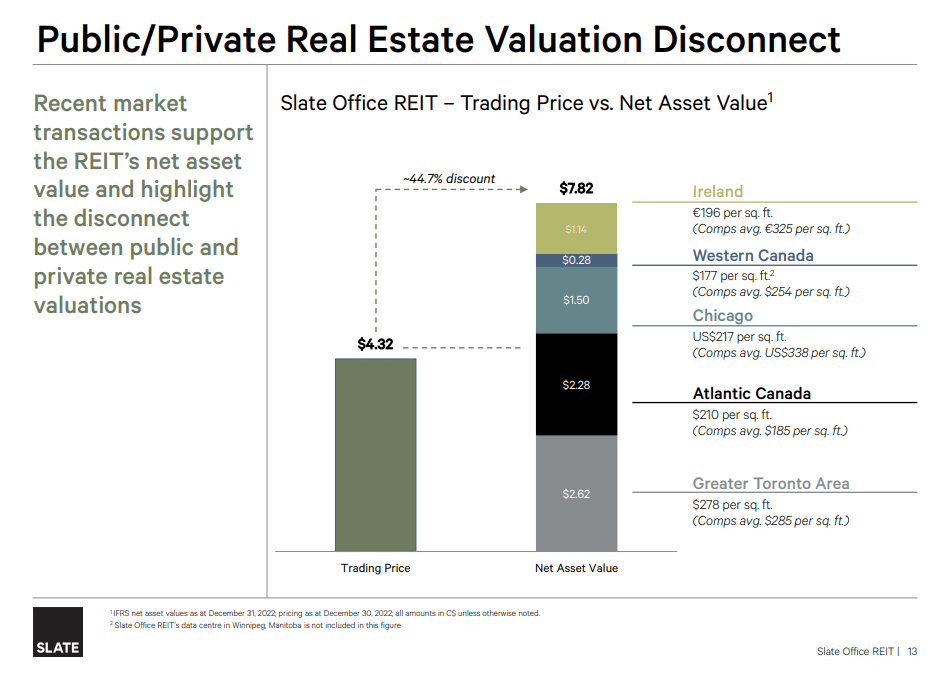

We will note here that the distribution yield is based on the old distribution rate and the discount to NAV is based on a $4.32 stock price. Slate breaks this discount down by region and cited comparatives to make their point.

{kind=link}

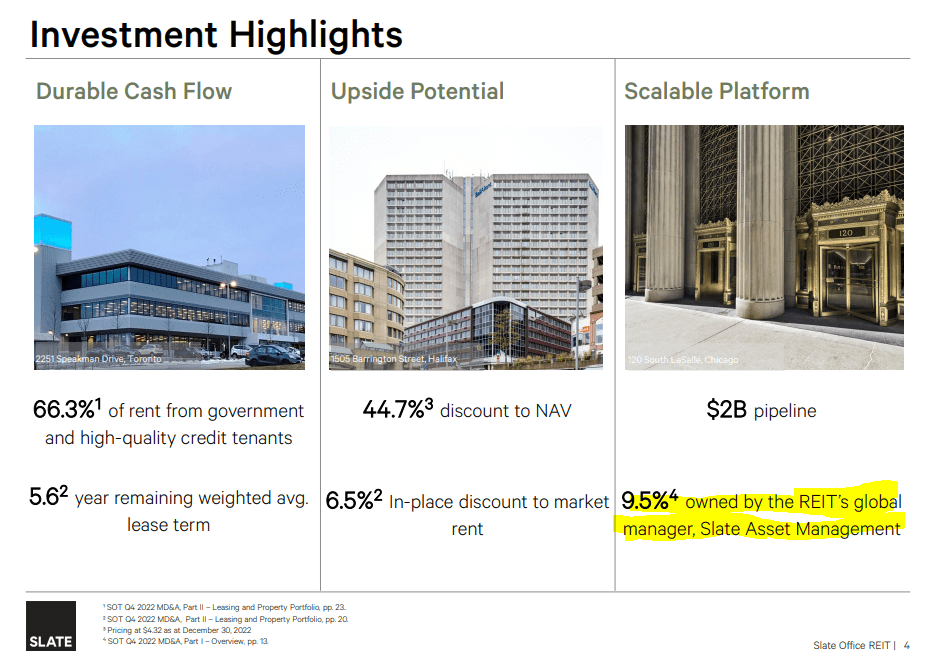

Management was not just involved in this REIT, it was committed. That 9.5% stake means that Slate Asset Management might be really feeling the pain.

{kind=link}

Keep in mind that the IPO occurred at $8.00 per share.

Current Problems

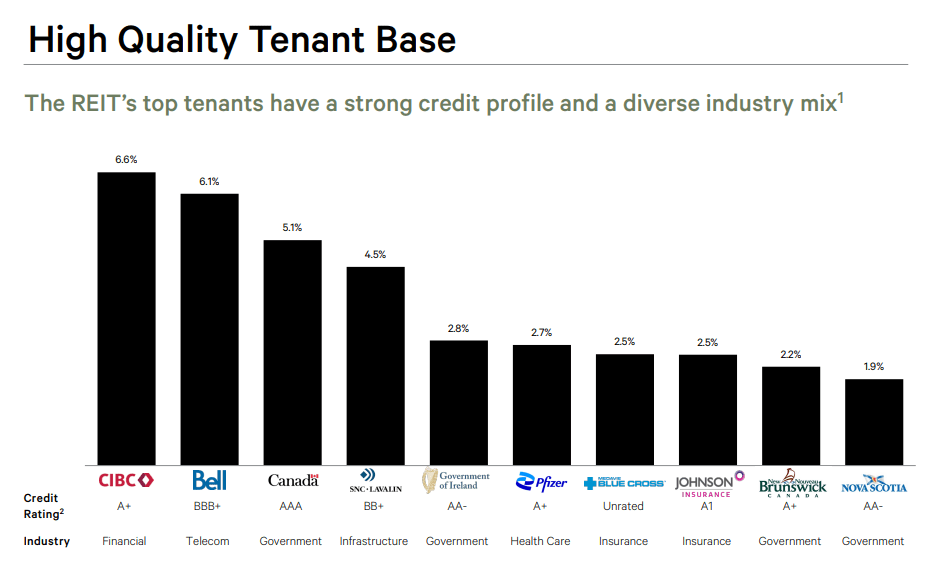

The REIT often brings up the quality tenant profile as a major selling point.

{kind=link}

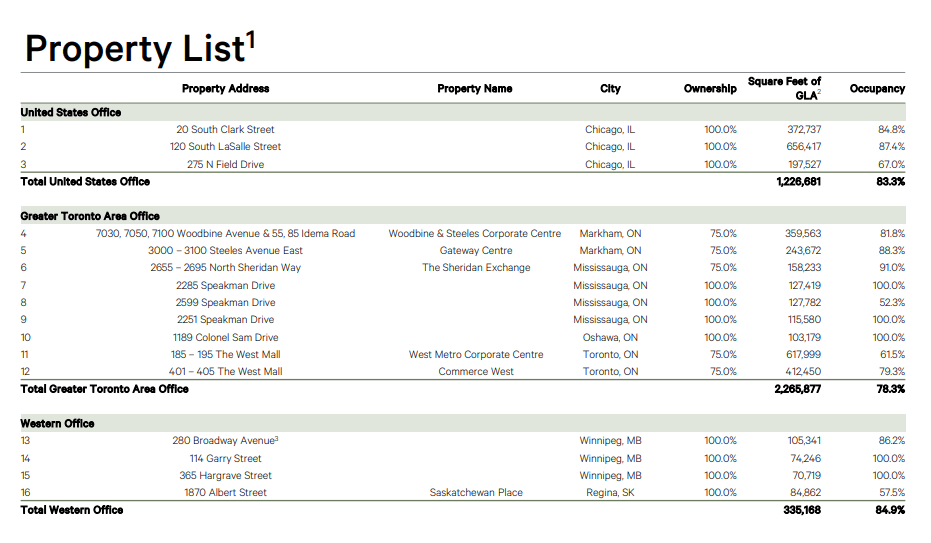

In the office space, we don't generally see that as a positive. Creditworthy tenants have great negotiating power and plethora of new office landlords wooing them day and night. That makes life harder for Slate trying to boost its own occupancy levels up. As seen below, Greater Toronto occupancy is at 78.3%.

{kind=link}

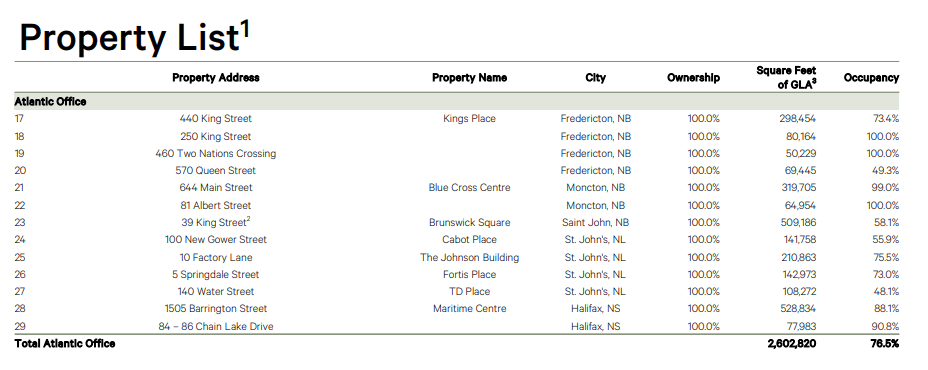

The Atlantic side is worse and almost down to 75%.

{kind=link}

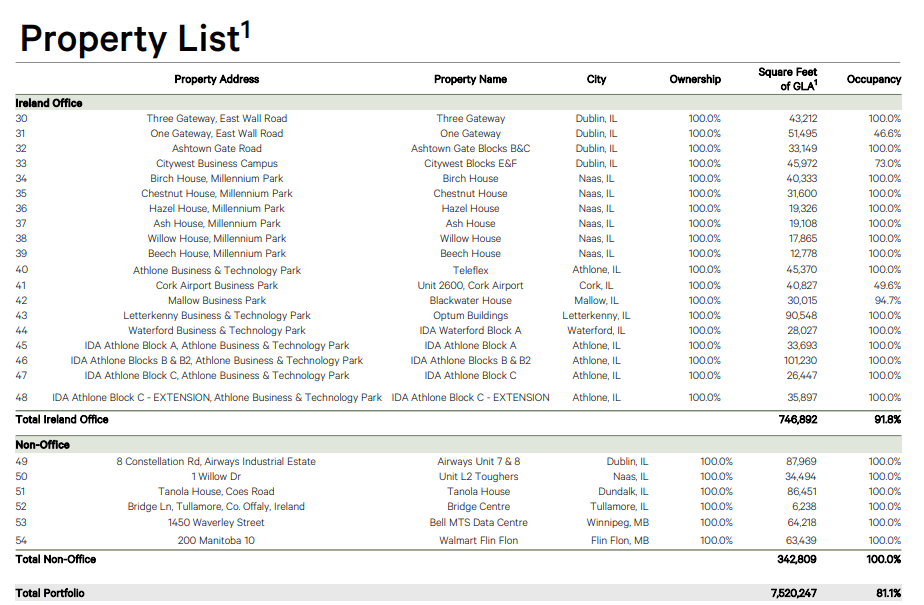

Ireland has held up surprisingly well and is boosting the numbers for the overall portfolio.

{kind=link}

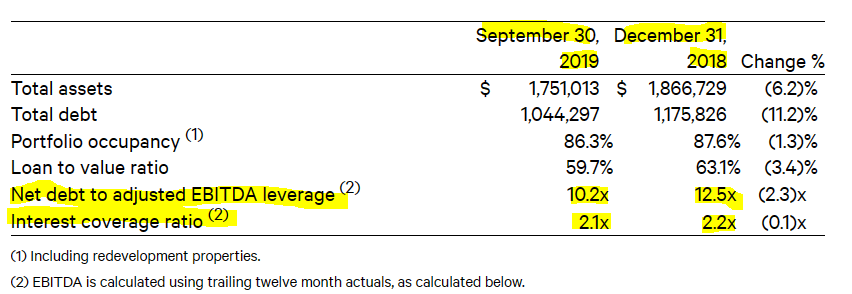

To management's credit, they really tried and worked at boosting the occupancy. We have followed this REIT for many years and the current predicament is not from a lack of effort. That said, they did run extremely high levels of leverage. These levels were absurd even pre COVID-19. They were running 12.5X debt to EBITDA in December 2018 and a shade over 10X just before the pandemic.

Slate Office Q3-2019 Financial Statements

{kind=link}

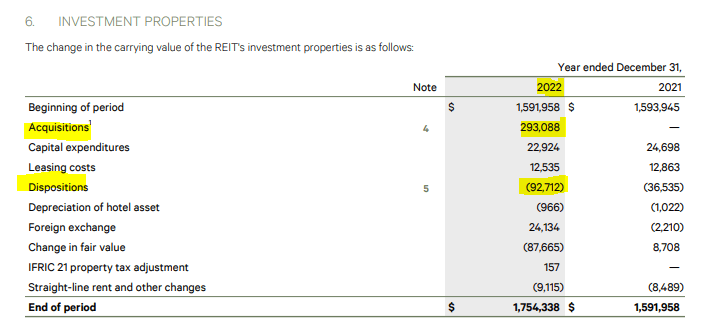

Interest coverage ratio was 2.1X. That was begging for trouble even during good times. But the biggest culprit was being oblivious to how bad things actually were in the office sector. They bought almost $200 million net in office properties in 2022.

Slate Office Q4-2022 Financial Statements

{kind=link}

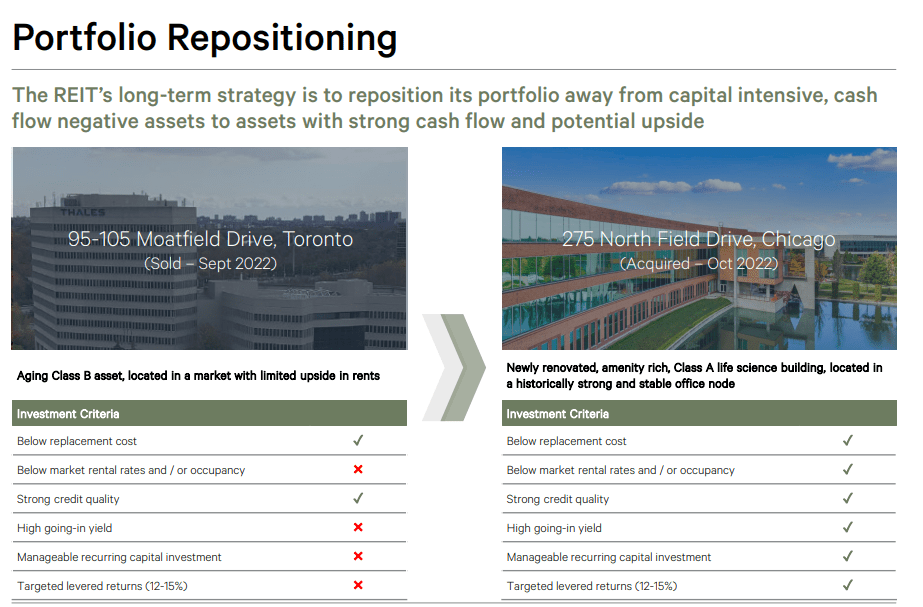

As recently as October 2022, they acquired yet another property.

{kind=link}

The reality hit around the time of redemption of its convertible debentures, when management realized that they had zero liquidity to do so. We will note that there was just a two month time gap between buying property shown above and hitting the panic button on inability to redeem the debentures.

Slate Office REIT an owner and operator of high-quality workplace real estate, announced today that it proposes to amend the terms of its 5.25% convertible unsecured subordinated debentures due February 28, 2023 (the "Debentures") to: (i) increase the interest rate from 5.25% to 9.00%, effective February 28, 2023, (ii) decrease the conversion price from $10.53 per REIT unit to $5.50 per REIT unit, (iii) extend the maturity date from February 28, 2023 to February 28, 2026.

Source: Slate Office

Slate had to increase the interest rate substantially, though reducing the strike price was rather pointless as it is unlikely to go anywhere near $5.50 ever again. So those observing this drama, had to know that the distribution cut was coming. If you cannot pay your maturing bonds totally just $28.8 million, you know that this drama had not reached its finale.

Valuation and Verdict

Interest coverage ratio was near 2.0X and debt to EBITDA was hitting a dozen at the end of December 2022.

Slate Office Q4-2022 Financial Statements

Weighted average interest rate was 4.4% and we saw that they boosted their convertible debentures rate from 5.5% to 9.0%. At a 9% across the board interest rate, their interest coverage becomes less than 1.0X. So anyone jumping in thinking this is a bargain must examine that first. If you think 9.0% is too much to expect for the whole debt structure, here are Office Properties Income Trust's ( OPI ) two year, investment-grade, bonds trading at an yield to maturity of 13.86%.

Interactive Brokers April 6, 2023

{kind=link}

So dial back the enthusiasm and understand that problems are really big. We generally lean pessimistic and are often pleasantly surprised. But in this case, even our dour forecasts from a year back look laughably optimistic today. Slate's equity has now become an option on recovery values. Total equity value is now about $200 million (85 million units X 2.30), while debt stands at an enormous $1.15 billion.

Slate Office Q4-2022 Financial Statements

{kind=link}

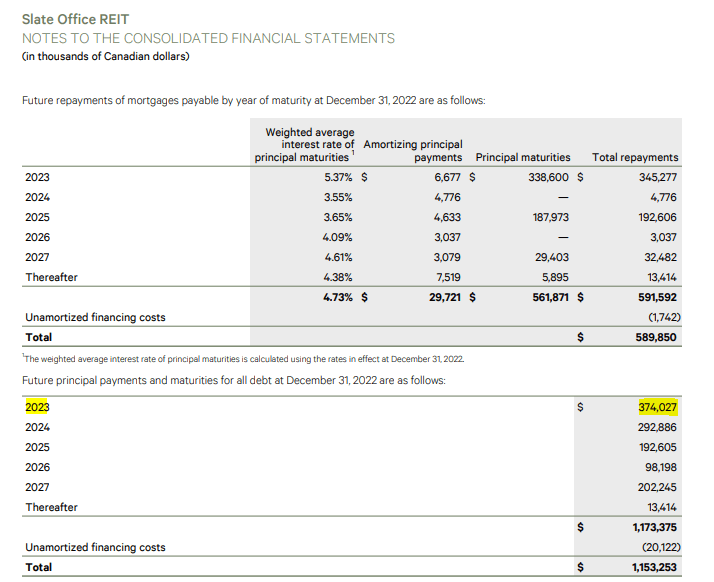

$375 million comes due this year.

Slate Office Q4-2022 Financial Statements

{kind=link}

They struggled with financing $28.8 million. What do you believe will happen with $375 million? Even if you shift the refinancing rate by 2-3% you will really tighten the noose. If that NAV of $7.82 shown in Q4-2022 really held, then Slate would be selling properties and buying back stock.

One solace here is that 60% of the debt is asset specific so it's possible through a lot of strategic defaults that some value is left for the common shareholders. We would not bet on it, but it's possible. At present our verdict may come as a surprise, but we believe it is not too late to sell. We don't the equity will make it through the upcoming recession and the risks look too high to even consider labeling this as a hold. This is no different than our sell rating on True North Commercial Real Estate Investment Trust ( TNT.UN:CA ). These stocks only look cheap due to price anchoring. They will likely go far lower, in our opinion.

For further details see:

Slate: Another Office REIT Slashes Dividends