SCCAF - Sleep Country: Sleep Soundly At Night With This Mattress Retailer

2023-04-21 02:26:12 ET

Summary

- Sleep Country is a Canadian mattress retailer growing revenues and EBITDA at double digits with a market dominant position.

- The company has made significant investments over the years in product innovation and has successfully acquired and transitioned business to capture growth in online sales.

- Shares are trading at a discount at 5.7x EV/EBITDA based on its historical valuation and its precedent transactions of acquired mattress brands.

Investment Thesis

Sleep Country Canada Holdings Inc. ( ZZZ:CA ) is a mattress retailer that has grown revenues and EBITDA at a 9.6% and 11.3% CAGR over the last five years. Over the years, the company has maintained a dominant market position in the Canadian mattress industry with recognizable brands and strong customer loyalty. Since 2018, the company has also made a series of acquisitions and investments into e-commerce and product innovation which I view as critical given changing consumer behavior towards online sales channels. With shares trading at the low end of their historical valuation range and shares priced at a discount relative to the mattress companies it previously acquired, I believe the market is overestimating the possibility of a near-term decline in Sleep Country's sales and that its current valuation has more than priced in this risk. Hence, I view Sleep Country's shares as attractive.

Company Overview

Sleep Country is a brick-and-mortar retailer that specializes in the sale of mattresses and sleep-related products including pillows, sheets, headboards, and bedding. It sells a wide-variety of recognizable brands including Serta, Tempur-Pedic, Sealy, and Bloom.

Over the years, Sleep Country has continued to expand its store network with 42 new stores in the last 5 years and has introduced new product offerings. Today, Sleep Country Canada is the largest specialty mattress retailer in Canada, with over 280 stores across the country and a broad range of sleep-related products. The company's focus on customer service, product innovation, and expansion have allowed it to maintain its market leadership position and drive long-term growth.

Store Location Footprint (Annual Report)

Transition to Omnichannel Sales

One of the things that I was impressed by was how quickly Sleep Country has transitioned itself to online sales and omnichannel sales. The company has grown from being the largest brick-and-mortar mattress retailer to becoming an integrated omnichannel sleep retailer with the addition of four direct-to-consumer sleep brands; Endy, Hush, Silk & Snow, and now Casper.

Omni-channel market share has been expanding rapidly over the years and the pandemic has only accelerated this trend towards online shopping for mattresses and sleep-related products. Sleep Country Canada has made investments in its e-commerce platform and has seen a significant increase in online sales in recent years. The e-commerce business represented 19.6% of sales in 2022, which I expect will only continue to grow in the years ahead.

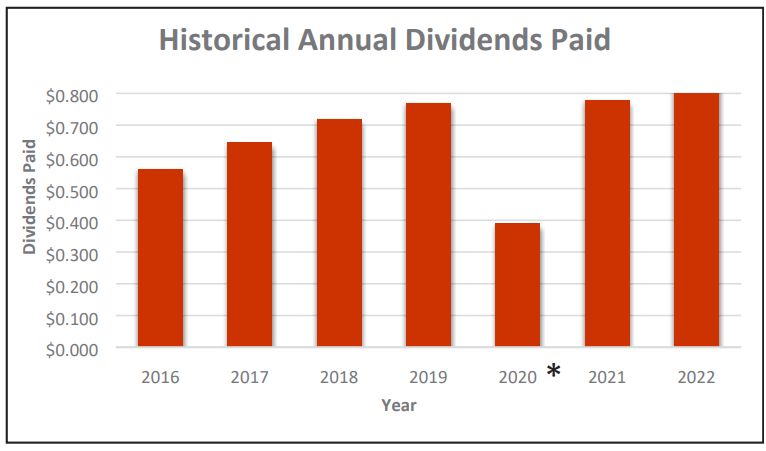

Steady and Growing Dividend

Sleep Country pays a stable and growing dividend of $0.215 per share paid quarterly, which represented about 20% of their free cash flow for 2022 for a 3.6% yield on the common shares. In 2020, the company temporarily suspended its Q2 and Q3 dividends due to the COVID-19 pandemic.

Historical Dividends (Annual Report)

{kind=link}

What I find impressive is that while total cash dividends paid have increased ~4% per year since 2017, dividends per share have actually grown at a faster rate with share count decreasing from 37.6 million to 34.7 million as a result of share buybacks. The company also has a NCIB (normal course issuer bid) whereby the company can buy back up to 10% of its common stock. The company recently bought back 173,400 shares in March for just over $4.3 million.

Acquisitions

A key part of Sleep Country's growth has been through growth by acquisition. One of its largest acquisitions was Endy, an online mattress-in-a-box retailer, which was not only profitable, but had also been seeing explosive growth (150% annual growth in 2018 when Sleep Country acquired them). Sleep Country acquired the business for $88.7 million at about 12x EBITDA. With direct-to-consumer becoming a larger part of the market, Sleep Country brought about synergies with Endy by increasing its participation in online channels while also offering Endy the possibility to capitalize on Sleep Country's back-end operations for logistics and warehousing.

A similar acquisition was done just last week with Sleep Country acquiring 100% of Casper's Canadian operations for $20.6 million in cash . Casper has been one of the most recognizable omni-channel mattress brands and its Canadian operations include the Casper website, six brick & mortar retail locations, and wholesale partners which include Costco, Indigo, The Bay, Loblaws. As direct-to-consumer continues to grow in popularity with consumers, I view this acquisition as attractive with management recognizing a value-enhancing deployment of capital.

Industry Analysis

The Canadian mattress industry is a $1.5 billion market comprised of specialty retailers, department stores, furniture stores, and e-commerce players. It is highly competitive with both brick-and-mortar stores like Sleep Country, The Brick, Leon's, IKEA, as well as online retailers like Douglas and Casper (acquired) who have entered the market.

Sleep Country is the market leader in the space, with over 275 stores in 17 regional markets across the country. The company has a strong brand reputation and a well-established distribution network, which could provide a competitive advantage in the industry.

One of the factors I consider to be key to their market dominance is their in-store experience. The company's stores are designed to provide customers with a comfortable and inviting environment, where they can test out a wide range of mattresses and receive personalized recommendations from trained sleep experts, something that can't be replicated by online retailers. This focus on customer service has helped Sleep Country to build a loyal customer base and differentiate itself from competitors.

In addition to its in-store experience, Sleep Country has also invested heavily in its e-commerce capabilities . The company's website offers a range of online shopping tools, including a mattress selector tool, sleep assessment quizzes, and online chat support. I view this focus on e-commerce to be crucial for Sleep Country to reach customers in new markets and compete with online mattress retailers .

Financials

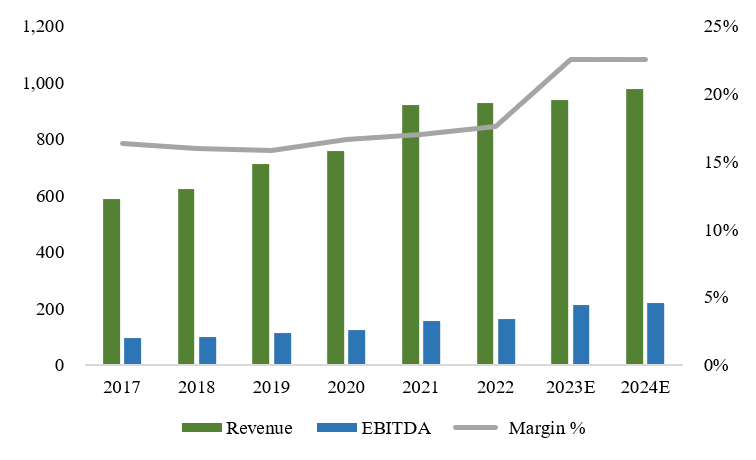

When looking at Sleep Country's financials, they appear to be in good shape, with revenues growing at a 9.6% CAGR and EBITDA growing at a 11.3% CAGR over the last five years. Sleep Country's strong performance has been driven by opening new store locations (42 new stores opened in the last five years) and through acquiring existing retailers, which has allowed them to enter new markets and capture additional market share.

Revenue and EBITDA (Author, based on company filings)

{kind=link}

When looking at the balance sheet, Net Debt/EBITDA has increased slightly over the last five years from 0.9x to 1.6x if we include leases of $275.2 million, but the dollar value of long-term debt has remained the same. This is impressive in my view considering that Sleep Country has grown revenues by over 58% and EBITDA by 71% over this time frame. Return on equity has also improved from 22.9% to 27.1%.

Valuation

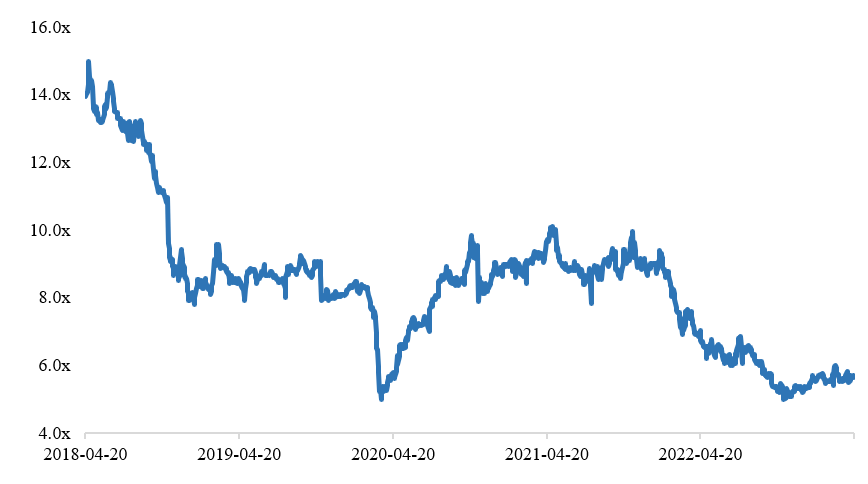

When we look at Sleep Country's historical EV/EBITDA valuation, we can see that it's trading at the low end of its historical range at 5.7x EV/EBITDA, which may suggest that investors see earnings falling in the future. While Sleep Country may have over-earned slightly during the pandemic, even on a normalized EBITDA of the average of 2017-2019 numbers, the company would still generate at least $120 million of EBITDA, which would put the multiple at about 9.7x. If we add expected EBITDA generated from acquisitions since, that would put the multiple at around 7.5x, at below the midpoint of its historical valuation range.

Author, based on data from S&P CapitalIQ

{kind=link}

When looking at the multiples paid for Sleep Country's acquisitions, they are higher than the company's current valuation. Silk & Snow was bought at 5.6x EBITDA , Hush at 9.0x EBITDA , and Endy at 12.0x EBITDA . Even when we consider that the market environments were different for all three of these acquisitions, at 5.7x EBITDA, shares of Sleep Country look undervalued.

Catalysts and Risks

Sleep Country has had very strong growth of expanding its store network across Canada while also accelerating its shift towards e-commerce, with the recent acquisitions of Silk and Snow in January and Casper's Canadian operations last week. As consumers continue to shop online for mattresses and sleep-related products, Sleep Country's online sales should continue to grow. With its partnership with Walmart to open in 7 express stores nationwide, I wouldn't be surprised to see them roll out more of Sleep Country's products in more of their stores if successful.

While Sleep Country has grown nicely over the years, I wouldn't expect to see much growth in the near term. With the overall health of the Canadian economy and consumer spending habits reducing the need for discretionary purchases like mattresses, recessionary conditions and unfavorable consumer sentiment could hurt demand for mattresses and sleep-related products in the near term. While much of this risk is likely priced into the stock at 5.7x EV/EBITDA, it's worth monitoring consumer behavior as it could weigh on the company's sales and profitability near term.

Conclusion

In summary, Sleep Country appears to be a solid investment for investors looking for to buy a market leading retailer at a substantial discount to its historical valuation. The company has a strong market position, stable financials, and a history of paying dividends. While investors should keep in mind the competitive landscape and monitor the company's financial performance for indications that growth may be slowing, I believe there is sufficient cushion for downside protection at its current valuation.

For further details see:

Sleep Country: Sleep Soundly At Night With This Mattress Retailer