SLRC - SLR Investment: The Glaring Vulnerability No One Talks About

2023-11-21 15:46:31 ET

Summary

- The BDC regulatory distribution requirements pose critical hurdles that prevent BDCs from recovering capital losses.

- Since the pandemic, SLRC's capital integrity has suffered.

- Despite reporting substantial capital losses, SLRC held its dividend steady, a feat achieved through ramping up leverage.

Investment Thesis

Most of us know that BDCs must legally distribute 90% of their annual income as dividends, making them popular among income-oriented investors. What is less known are the deeper ties to the historical events that shaped the industry and, crucially, led to its greatest vulnerability.

The Small Business Investment Incentive Act of 1980, which amended the 1940 Investment Company Act and created BDCs, was formulated in a climate of urgency. It established the legal structure of BDCs as a swift remedy to the economic disruption of the mid-1970s and the resulting crises within small businesses arising from geopolitical challenges of the Yom Kippur War of 1973 and the subsequent oil embargo, culminating in the 1980 recession. In a bid to increase BDCs' appeal as an investment vehicle and ensure a quick flow of funds to the Small & Medium Enterprise 'SME' sector, Congress took one step further, mandating the distribution of at least 90% of the income from these funds as dividends to shareholders.

While initially intended to encourage investment in smaller ventures, this dividend distribution framework presents significant economic challenges for SLR Investment ( SLRC ). These challenges transform the company's role from a dependable source of income to a more speculative investment. For this reason, we argue for a shift in the investment strategy regarding SLRC from a buy-and-hold income generation approach to short-term opportunistic trading.

The Main Issues

SLRC's management announced shifting their distribution frequency from monthly to quarterly in August. Notably, this change doesn't significantly affect the absolute yield, which remains attractive at 11.5%, garnering the attention of income-focused investors. However, it is important to consider the associated risks with this yield. Unlike standard lenders, who can pause distributions during challenging times to safeguard capital, SLRC faces a different scenario due to federal dividend distribution laws. These laws restrict SLRC's flexibility in managing capital losses or bad debt write-offs. If one of its portfolio companies defaults, SLRC not only loses income otherwise distributed to its shareholders but also loses income necessary to repay debt expense incurred for these investments; a liability, unlike associated assets, isn't written off, posing a long-term financial risk. More than half of SLRC's investments are funded by debt, incurring an annual interest expense of $80 million, and this figure is rising as management ramps up leverage. This creates a cycle where NAV decline is practically inevitable.

Exposure to Biotech

Naturally, SLRC has an inherently high-risk profile, given the mandatory exposure to leveraged SMEs. BDCs must invest at least 70% of their capital in private small companies. This risk is further heightened by their engagement with the drug development market, known for its uncertainty.

SLRC's strategic focus on late-stage biotech companies does offer some mitigation, yet, drawing from my experience in the biotech sector, I can confidently say that the risks here are still quite significant, even for a fixed-income investor such as SLRC. These challenges are multifaceted, encompassing not just the demanding nature of late-stage clinical trials, which are rigorously designed to confirm both the safety and efficacy of a drug, but also to demonstrate it is better than existing drugs on the market. Moreover, the journey doesn't end with drug development. Obtaining approval from the Food & Drug Administration 'FDA' is a significant milestone, but it is just the beginning. The real challenge often lies in convincing physicians to adopt new drugs over the ones they're familiar with. It's a complex task that frequently requires extensive educational efforts by pharmaceutical companies. I've seen this firsthand through lavish industry events.

Physicians are creatures of habit. They tend to stick with medications they know and trust, only venturing to try new options when their preferred choices prove ineffective. This conservative approach is further compounded when FDA labels restrict new drugs to being second-, third-, or fourth-line therapy options, limiting their immediate use.

Another critical aspect is the role of Medical Standards and Practice Guidelines. These are typically set by professional bodies, who are very prudent in adopting a newly authorized drug in their standards, often requesting long-term studies to support a biotech's claim over its drug beyond those established during the FDA-approval process.

Then there's the chicken-and-egg problem with insurance coverage. Physicians are more likely to prescribe drugs that are covered by insurance plans. Conversely, insurers are cautious about covering new drugs unless they see a proven track record of value and acceptance among a significant number of physicians. It's a cycle where each side waits for the other to make the first move.

The bottom line is, don't take SLRC's management assertions of their focus on late-stage biotech companies at face value. More importantly, consider that SLRC's 9% exposure to the biotech industry is quite significant in terms of risk, considering SLRC's reliance on borrowed funds to invest in these biotech companies and its limited ability to retain revenue to repay debt. When one of these companies declares bankruptcy, SLRC removes the loan from its asset balance, acknowledging the loss. However, the debt and interest SLRC incurred to finance this loan persists on its balance sheet, continuing as liabilities that the company must manage.

Is Equipment Financing/Leasing Safe?

SLRC stands out among BDCs for having a specialized team dedicated to equipment financing. However, this distinction has led to a misleading perception of enhanced safety.

Although equipment-secured finance can have advantages over cash-flow financing in terms of valuation and loan recovery, SLRC's Equipment Finance, including Kingsbridge Holdings, constitutes only 23% of the total portfolio. A significant portion of its remaining portfolio is cash-based loans with little asset collateral, such as those loans extended to medical practices, including the recently bankrupt PhyMed, which cost SLRC investors +$30 million.

Secondly, equipment finance has unique risks and is difficult to manage. Unlike cash financing, idle equipment can't be parked in interest-yielding short-term deposits such as treasury; instead, it loses value over time. The financial challenges of GE Capital demonstrate the challenges of running an equipment-based financing business.

The Truth Behind First Lien Debt

SLRC often highlights the quality of its portfolios, emphasizing the high percentages of First Lien / Senior Secured debt to attract investors and give an impression of safety. After all, these debt instruments have priority over the borrower's assets in case of liquidation. What's there to worry about? Well, everything.

Despite all assurances of quality assets and a unique business model, SRLC reported significant capital losses and wrote off significant chunks of bad debt over the years. The inability to retain income to recover these capital losses translates to an inevitable NAV per share loss.

Discount To NAV

During the pandemic, I penned an article expressing a bullish outlook on SLRC. My argument back then hinged on the deviation of SLRC stock price from NAV and the anticipated economic recovery supported by the Fed. In the following months, SLRC's Price/NAV ratio returned to historical levels, allowing for capital appreciation, which, coupled with a 9.5% dividend yield at the time, resulted in enticing double-digit returns.

Fast forward to today, the discount to NAV that SLRC is trading at is comparable to the figures when I initially covered the company three years ago. For example, in August 2020, SLRC was trading at 17% discount to NAV, compared to today's 19% discount. Is this a signal of a repeated buying opportunity? Not so much. The structural integrity of SLRC's balance sheet has deteriorated since the pandemic. Despite reporting substantial capital losses, SLRC held its dividend steady, a feat achieved through ramping up leverage. Management has recently signaled more leverage is to come. However, this strategy hits a wall with the SEC's restrictions on the debt load a BDC can shoulder, making the high-leverage tactic untenable.

With SLRC's debt ratio rising, a deeper discount to NAV seems justified, casting a shadow on the prospects for capital appreciation. Thus, the investment allure that supported our bullish thesis in the previous article appears to have dimmed. Interestingly, SLRC management notes that their regulatory leverage ratio is within the industry average, around 190% (the minimum allowed under Trump's new regulation is 150%). Still, in absolute terms, SLRC's total interest-bearing debt as a percentage of assets has increased, underpinning the adverse dynamics discussed below.

How I Might Be Wrong

Each year, SLRC shareholders vote on a crucial measure: whether to permit management to raise equity below NAV/share. Without their approval, the law restricts SLRC from undertaking this action. Despite that raising equity below NAV/share immediately dilutes existing shareholders, every year, they willingly accept this outcome. The underlying reason ties back to the minimum Asset Coverage Ratio required by law.

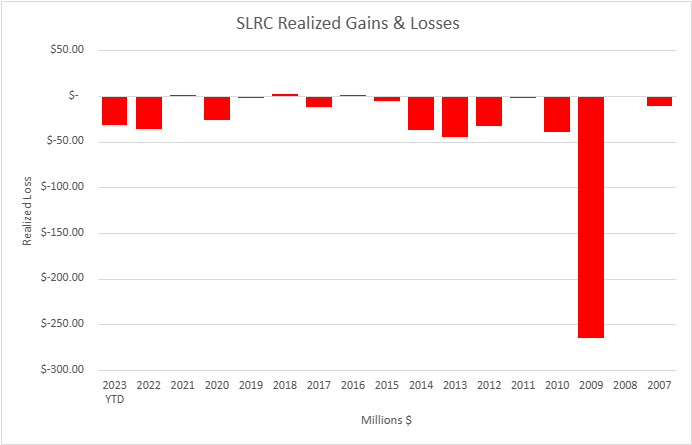

From 2007 through the first half of 2023, SLRC's net realized losses totaled half a billion dollars. In Q3 2023 alone, the company wrote off more than $31 million. Although it wrote off these assets from its balance sheet, the debt incurred to acquire them remains, skewing the mandated Asset/Liability balance. To regain this balance, shareholders endorse the equity raise, bringing Debt-to-Equity back within regulatory limits.

This decision hinges on a long-term outlook. Shareholders are wagering that over time, the dividend yields will compensate for the NAV dilution incurred, countering the adverse effects of raising equity below NAV/share. This long-term strategy could materialize, undermining the short-term trading approach proposed in this piece. In other words, this article rests on the assumption that the risk/reward of holding SLRC as a long-term income investment is unfavorably compared to holding the debt or preferred stock issued by SLRC or other BDCs, drawing insights from the historical losses caused in periods of severe economic disruptions.

{kind=link}

Graph created by the author. Data sourced from SLRC

Summary

SLRC's performance illustrates the limitations imposed by the rigid BDC regulatory framework, which, while aimed at propelling small business growth, significantly curtails BDC's ability to safeguard against capital erosion. I believe it is time to consider the 1980 amendments to allow BDCs such as SLRC more flexibility in determining dividends according to economic conditions.

The company's exposure to the Equipment Finance sector, though argued by some as a shield against loan-to-value dynamics, stands frail given its minor portfolio share and the inherent depreciation risks associated with the financed asset. This, coupled with its exposure to high-risk biotech sector and the inevitability of bad debt write-offs, highlights a glaring vulnerability for long-term investors.

SLRC's debt ratio is near all-time highs, and management promises more borrowing is to come, limiting its ability to leverage through economic disruptions, a tactic that allowed it to maintain dividends despite NAV per share losses. As SLRC increases its debt-to-equity ratio, a deeper discount to NAV is justified. The bottom line is that SLRC's dividend yield comes at risks of capital losses, dilution, and dividend cuts. Your bet is essentially that the dividend yield will compensate for an inevitable decline in share price in the long run.

For further details see:

SLR Investment: The Glaring Vulnerability No One Talks About