SLVO - SLVO: Converting Silver Volatility Into Yield

2023-07-22 07:29:27 ET

Summary

- The Credit Suisse X-Links Silver Shares Covered Call ETN (SLVO) provides exposure to the iShares Silver Trust ETF (SLV) with a call-writing overlay.

- Despite a 19.4% trailing yield, SLVO's 5-year average annual total returns are only 1.9%, indicating investors are simply paid back their own principal but taxed as income.

- During major rallies in silver, the SLVO will lag significantly because it has capped monthly upside.

- Investors should avoid the poorly designed SLVO product.

While looking through high yielding funds, I came across the Credit Suisse X-Links Silver Shares Covered Call ETN ( SLVO ), with a 19.4% trailing yield. Historically, one of the main drawbacks of owning precious metals is their lack of productivity / yield. Has the SLVO ETN solved the 'lack of yield' problem from owning silver?

Unfortunately, my analysis suggests investors should steer clear of the SLVO ETN. For those seeking silver exposure, the SLVO ETN lags significantly during major rallies in silver due to its call-writing strategy. For investors seeking yield, SLVO's 19.4% trailing yield is accompanied by 5Yr average annual total returns of 1.9%, suggesting investors are simply paid back their own principal but taxed as income.

Fund Overview

The Credit Suisse X-Links Silver Shares Covered Call ETN ((SLVO)) is an exchange traded note ("ETN") offered by Credit Suisse (note, with the shotgun marriage between Credit Suisse and UBS, it is assumed that UBS will take on the ETN products previously offered by Credit Suisse).

The SLVO ETN offers investors exposure to the Credit Suisse NASDAQ Silver FLOWS™ 106 Index ("Index"), which tracks the investment performance of owning the iShares Silver Trust ETF ( SLV ) while writing 6% out of the money ("OTM") call options on the SLV ETF. Variable premiums received from the strategy are paid out to investors as cash coupons (Figure 1).

Figure 1 - SLVO strategy (SLVO factsheet)

The SLVO ETN is designed to generate monthly cash flows in exchange for giving up gains beyond the strike price of the written call options. The SLVO ETN strategy does not provide protection from losses resulting from a decline in price of the SLV ETF beyond the call premiums received.

The SLVO ETN has $125 million in assets and charges a 0.65% expense ratio, compounded daily.

Hidden Risk With ETNs

Unlike an exchange traded fund ("ETF") that owns a portfolio of securities, an ETN is an unsecured debt security issued by an investment bank (in the case of SLVO, the issuer is Credit Suisse/UBS) that tracks an underlying index and trade on a major stock exchange like a stock. At maturity, the ETN will pay the return of the index it tracks, less any fees. The ETN simply provides investors with returns of the underlying index and does not confer ownership of the underlying securities. Hence, investors in the ETN are exposed to the risk that the issuer may default and not honour the contractual total return payout.

In the case of the SLVO, this almost became a reality in March when Credit Suisse was pushed to the brink of bankruptcy before the Swiss government forced Credit Suisse and UBS into a shotgun marriage. If the government had allowed Credit Suisse to fail, then investors in SLVO would have become an unsecured creditor of Credit Suisse.

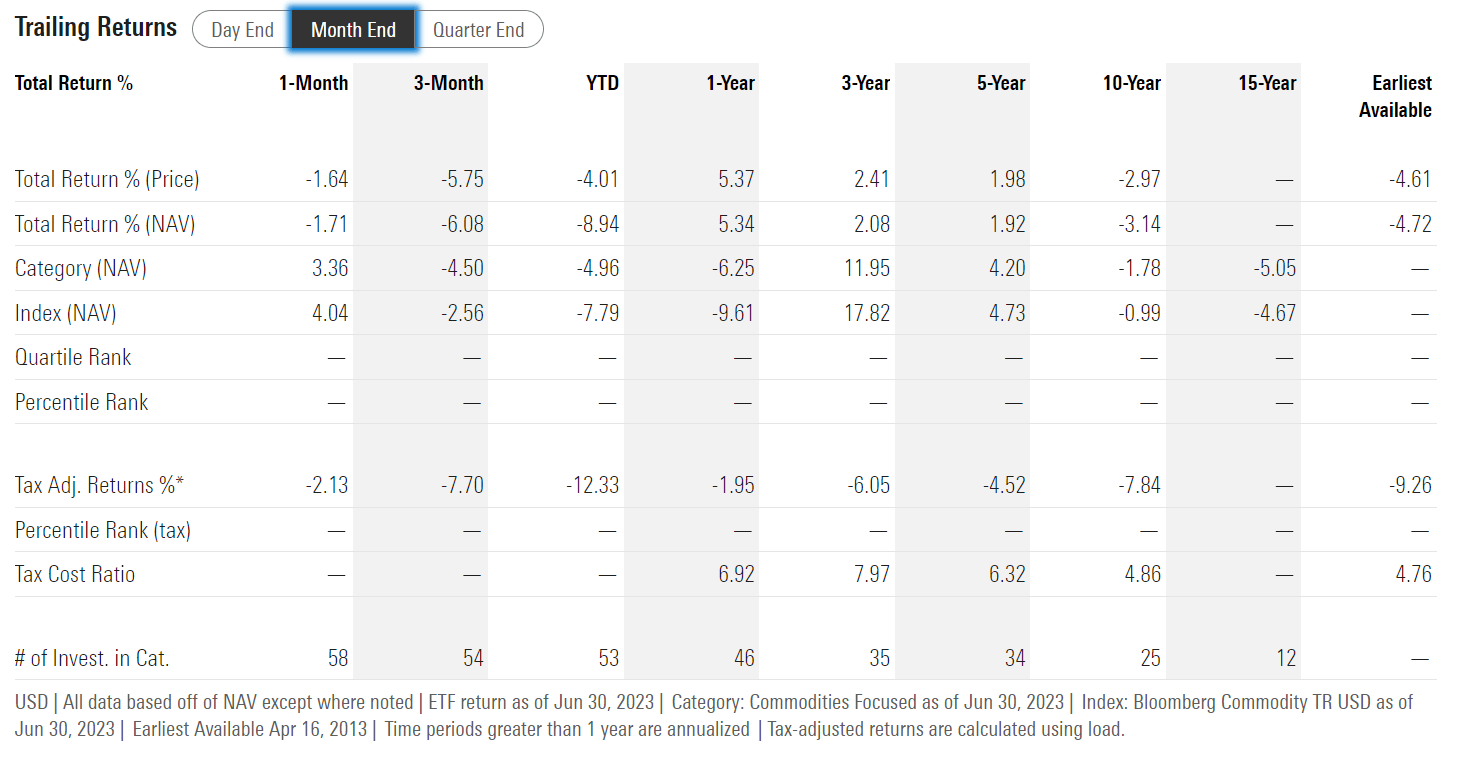

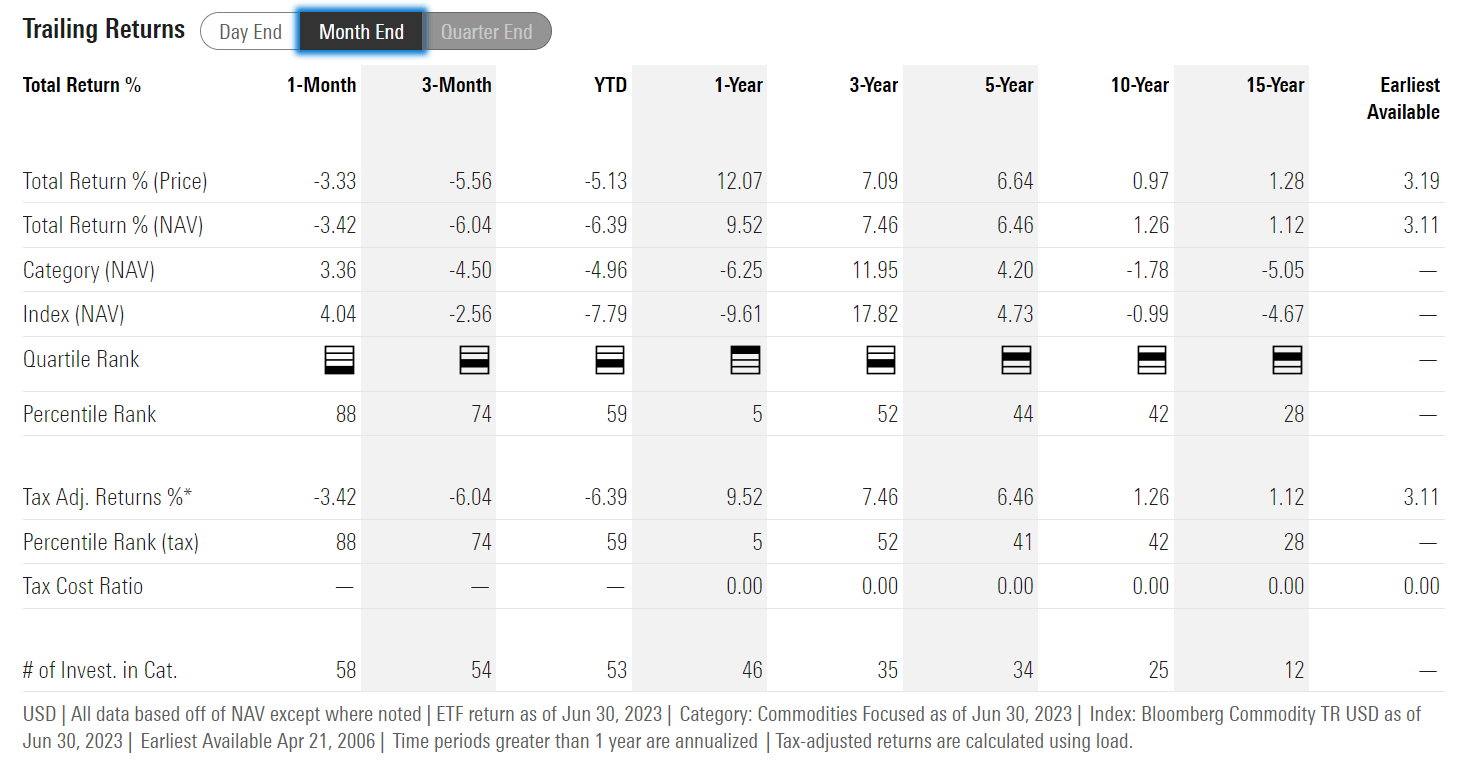

Returns

Figure 2 shows the historical returns of the SLVO ETN while Figure 3 shows the historical returns of the SLV ETF for comparison. As we can see, the SLVO ETN has delivered 3/5/10Yr average annual returns of 2.1%/1.9%/-3.1% respectively to June 30, 2023, compared to 7.5%/6.5%/1.3% for the SLV.

{kind=link}

{kind=link}

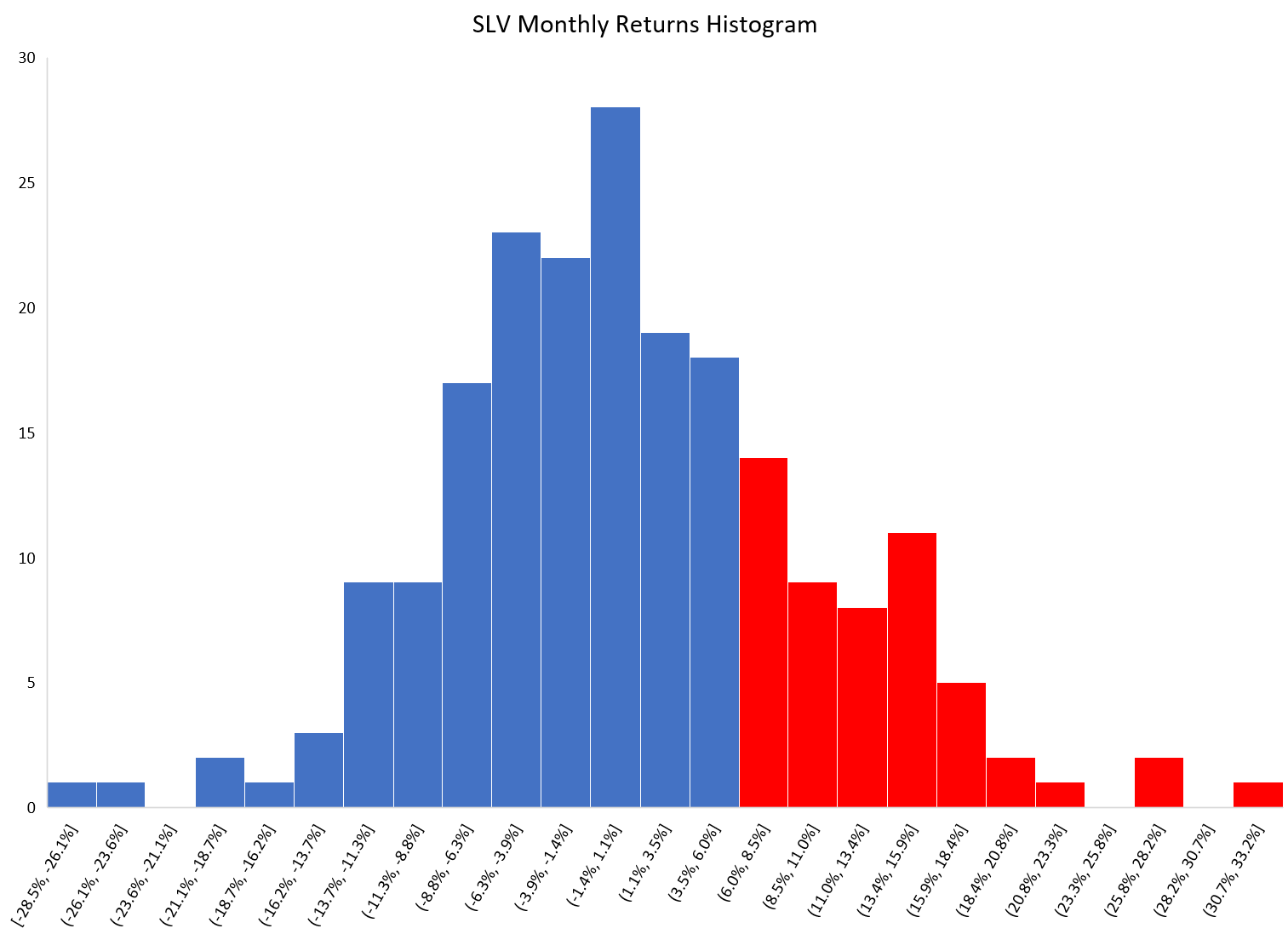

SLVO's underperformance is understandable, as call-write strategies trade off upside for premium income. Figure 4 shows the historical monthly returns histogram of the SLV ETF. SLVO's strategy basically gives up the right-tail distribution of SLV returns in exchange for premium income, which will skew average returns lower.

Figure 4 - SLV monthly returns histogram (Author created with data from Yahoo Finance)

{kind=link}

Distribution

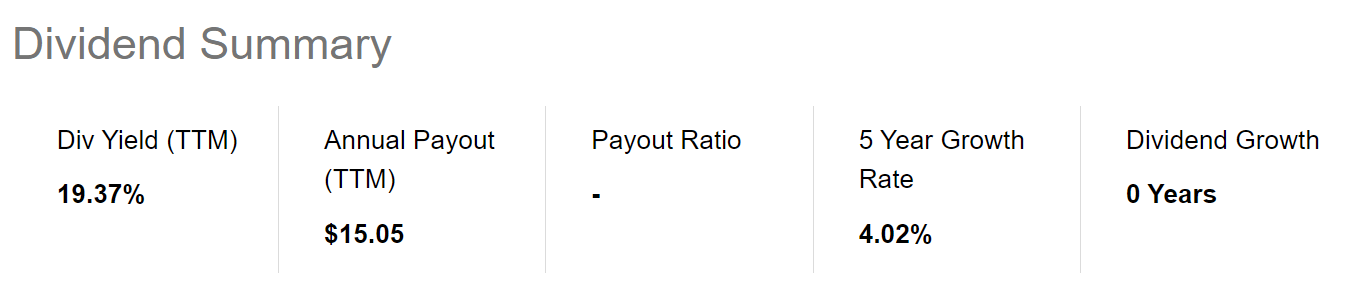

In exchange for giving up SLV upside, SLVO investors receive an attractive monthly distribution, with trailing 12 month distribution of $15.05 / unit or 19.4% (Figure 5).

Figure 5 - SLVO pays a 19.4% trailing distribution (Seeking Alpha)

{kind=link}

Investors should note that SLVO's distribution is variable and depends on the prevailing market price and volatility of the SLV ETF when the calls are written.

Is This The Returns Profile You Were Looking For?

As with most things in life, there is no free lunch. Investors need to understand that with a call-write product like the SLVO ETN, they are no longer receiving the return profile of the SLV ETF, which tracks the price of silver.

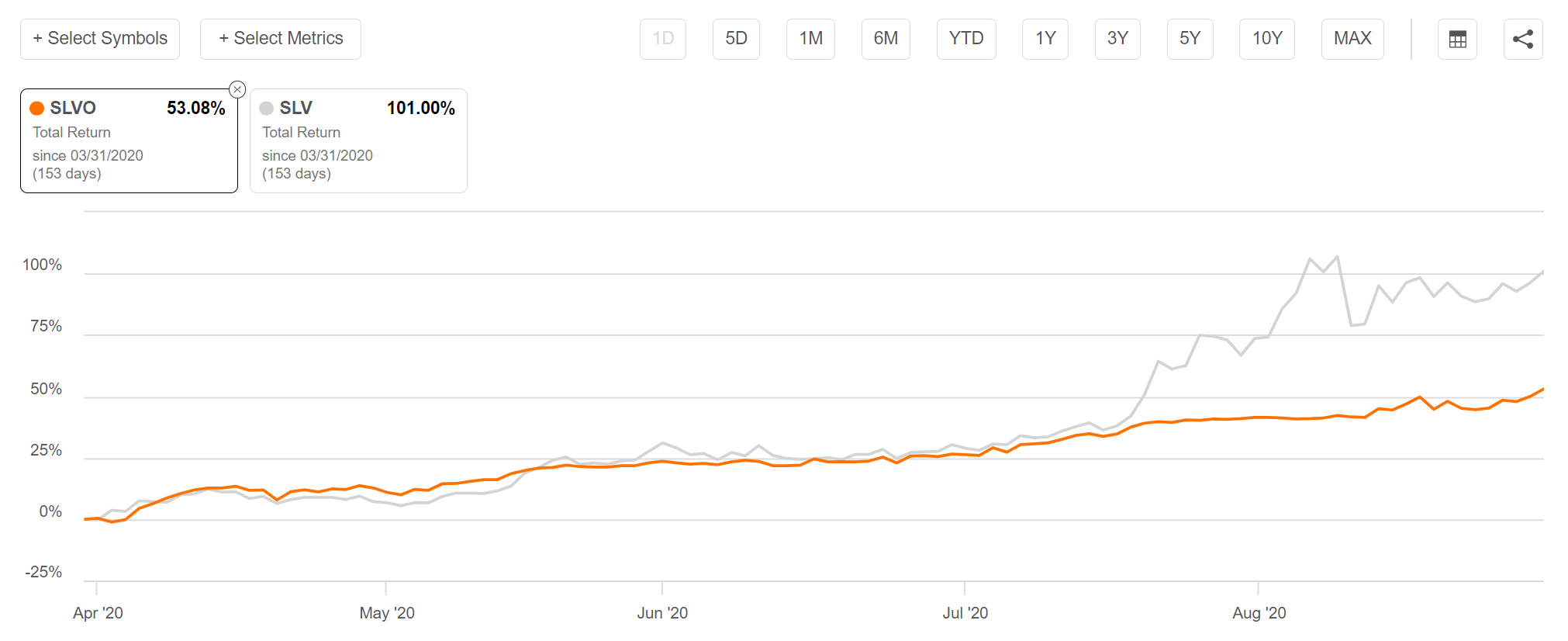

Investors who are bullish on silver but invested in the SLVO ETN may end up with total returns dramatically lower than expected. For example, between March 31, 2020 to August 31, 2020, the SLV ETF returned 101% as the price of silver soared. However, the SLVO ETN, because it gives up monthly returns above 6%, only delivered 53.1% in total returns in the same time period (Figure 6).

Figure 6 - SLVO vs. SLV, March 31, 2020 to August 31, 2020 (Seeking Alpha)

{kind=link}

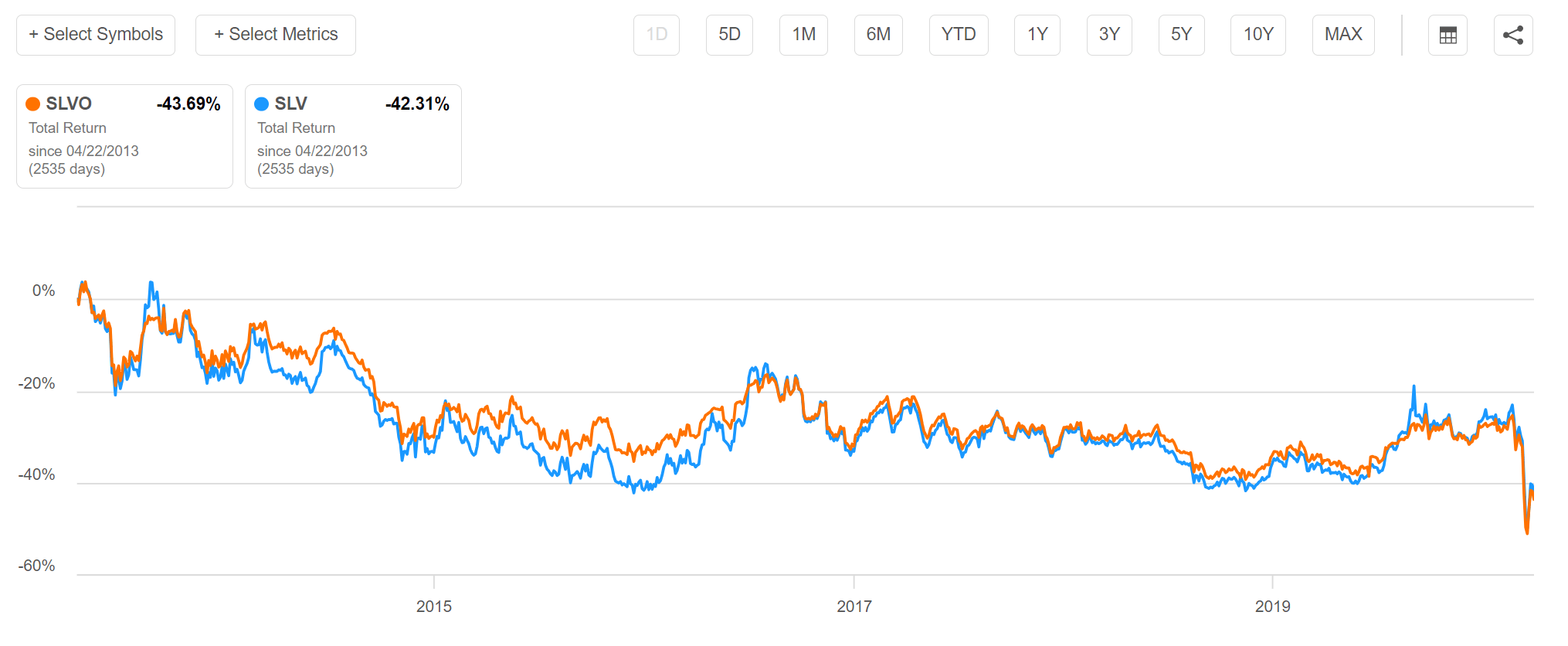

However, during sideways to down markets, the SLVO ETN does approximate the returns of the SLV ETF (i.e. from Figure 4 above, tails you win, heads I lose). For example, from inception (April 22, 2013) to March 31, 2020, the SLVO ETN delivered -43.7% in total return compared to -42.3% in total return for the SLV ETF, as silver was in a general downtrend since peaking in 2011.

Figure 7 - SLVO vs. SLV, April 2013 to March 2020 (Seeking Alpha)

{kind=link}

Investors considering the SLVO ETN need to make the distinction whether they are investing in SLVO because it is a 'silver-linked product with a high distribution yield' , or a 'high yield product harvesting silver's high volatility' . Those in the former camp may be sorely disappointed, as when silver does make a strong run like it did in 2020, the SLVO ETN will lag significantly behind.

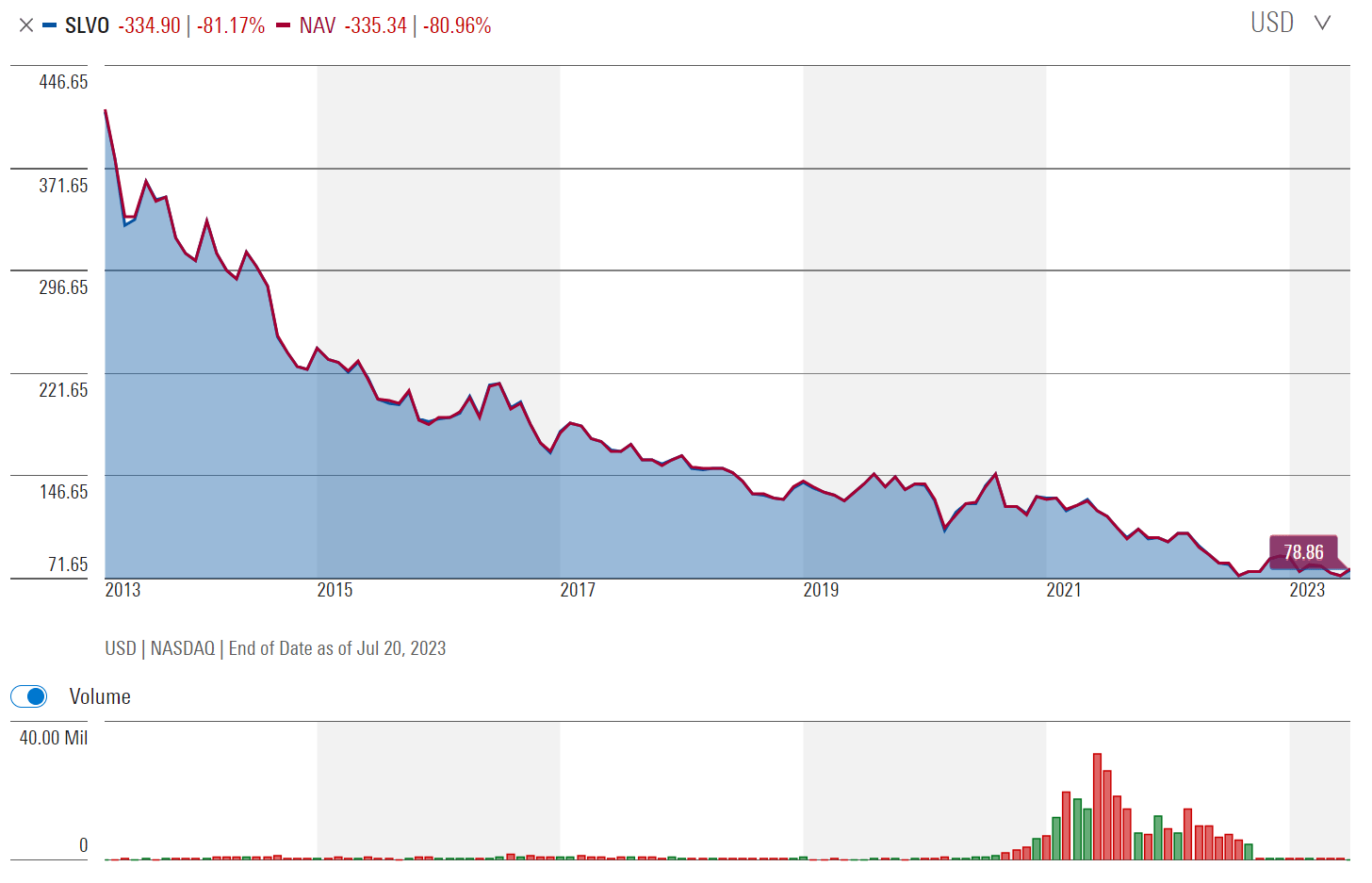

Furthermore, SLVO's poor long-term total return performance, with 5 and 10Yr average annual return of 1.9% and -3.1% respectively from figure 2 above, suggest even those looking to harvest silver's high volatility may walk away with a bad taste in their mouths. SLVO's high distribution yield is accompanied by large declines in NAV (Figure 8). Essentially, investors are just paid back their own capital in the form of the distribution.

{kind=link}

There is also the matter of tax. From my understanding of the prospectus , for U.S. holders of the ETN, coupon payments are treated as ordinary income and the difference between sale proceeds and investors' tax basis is treated as capital gains/losses. This treatment of coupon as income may be less favourable than other 'return of capital' funds. Investors considering the SLVO ETN should consult a tax professional before making any investment decisions.

Conclusion

The Credit Suisse X-Links Silver Shares Covered Call ETN provides exposure to the SLV ETF with a call-writing overlay. Investors considering the SLVO ETN need to understand that, like all call-writing products, the SLVO ETN trades off SLV upside for premium income. This causes the SLVO ETN to significantly lag the SLV ETF during periods of rapid price appreciation.

Furthermore, while the SLVO ETN pays a very attractive monthly coupon, with trailing 12 month yield of 19.4%, SLVO's poor total returns suggest investors are simply paid back their capital in the form of the distribution. And unlike ROC distributions that receive preferential tax treatment, the coupons from the SLVO ETN are considered ordinary income.

I would personally avoid the SLVO ETN.

For further details see:

SLVO: Converting Silver Volatility Into Yield