SLX - SLX: Why I Am Not A Buyer

2023-10-24 16:31:14 ET

Summary

- The VanEck Steel ETF is the closest thing to a pure-play steel ETF currently available.

- SLX carries a relatively high management fee for a passive fund.

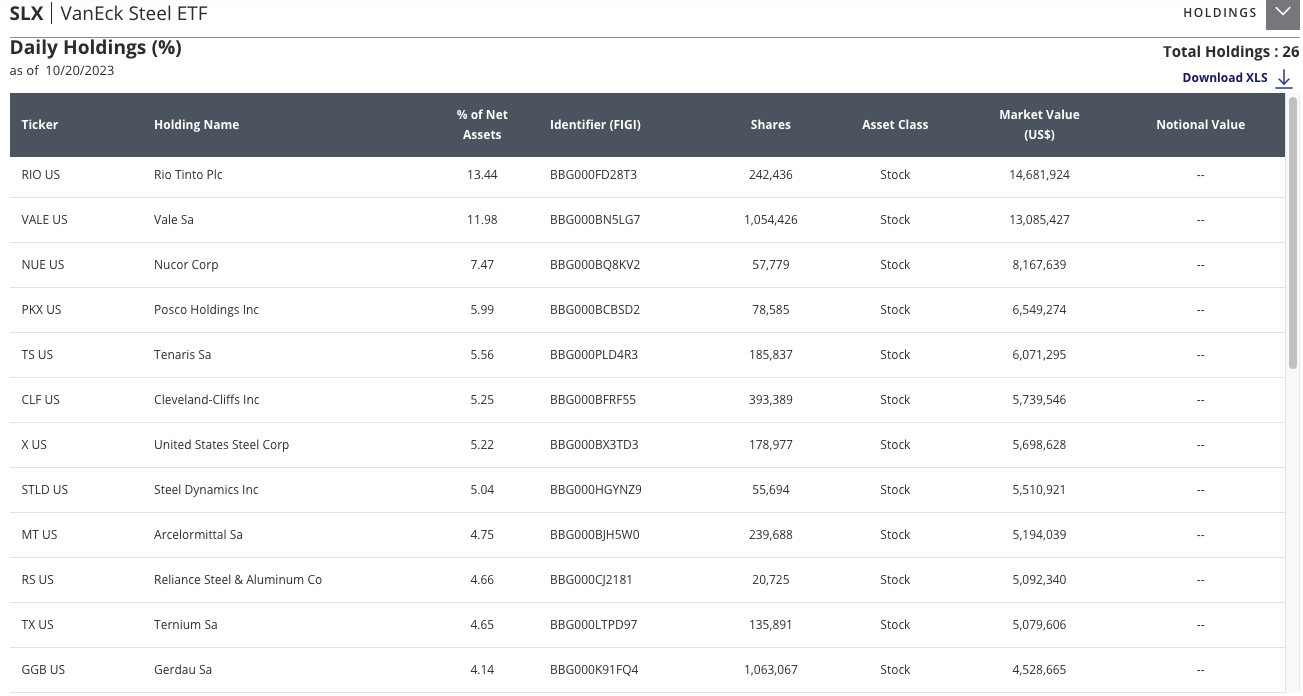

- SLX holds a concentrated group of just 26 stocks and the largest holding, Rio Tino Plc, is not a pure play on steel.

- The steel industry is characterized by a high degree of global competition and SLX has significantly underperformed the S&P 500 over the long-term.

- Investors looking to gain exposure to steel may want to consider individual steel companies with a history of outperformance such as Nucor instead of SLX.

ETF Overview

The VanEck Steel ETF (SLX) seeks to replicate the price and yield performance of the NYSE Arca Steel Index which is intended to track the overall performance of companies involved in the steel sector. SLX is managed by VanEck and currently has ~$109 million of assets.

SLX currently holds 26 stocks, trades at a trailing P/E ratio of 8x, trades at a trailing price-to-book value ratio of 1.3x, and offers a current dividend yield of 4.8%.

High Management Fee

SLX has a gross expense ratio of 0.58% and a net expense ratio of 0.56% as VanEck has agreed to waive certain fees through at least May 1, 2024. Comparably, the Vanguard Materials ETF (VAW) has an expense ratio of just 0.10% while the Materials Select Sector SPDR Fund (XLB) also has an expense ratio of just 0.10%. As an investor, I work diligently to avoid high management fees (active or passive) as I believe they are often an overlooked headwind when investing.

SLX's fee of 0.58% strikes me as particularly high given investors are not getting any active management but rather passive index replication. My sense is the reason for the relatively high fee is that the fund has a relatively low amount of assets (just $109 million) and thus it is not possible to offer this product at a low fee price point. Comparably, XLB has just over $5 billion in assets and thus can still easily cover its operating costs at a 0.10% fee.

Highly Concentrated Holdings

As shown by the table below, SLX is a fairly concentrated ETF with just 26 holdings. The top five holdings Rio Tinto Plc (RIO), Vale (VALE), Nucor Corporation (NUE), POSCO Holdings (PKX), and Tenaris (TS) make up a total of 44.4% of the entire ETF.

Generally speaking, my view is that ETFs earn their fees when they offer investors an efficient way to do something they cannot easily do on their own. It would not be difficult for investors to simply replicate the 26 holdings and weights for SLX and avoid paying the 0.58% in annual fees. Investors who do not want to bother with 26 holdings could just scale up the weights of the top 5 holdings and still get reasonably well-diversified exposure to the same risk factors. Moreover, individual investors have the ability to actively manage their tax position with stocks to a better degree than is the case with ETFs.

{kind=link}

Largest Holding Is Not Steel Pure Play

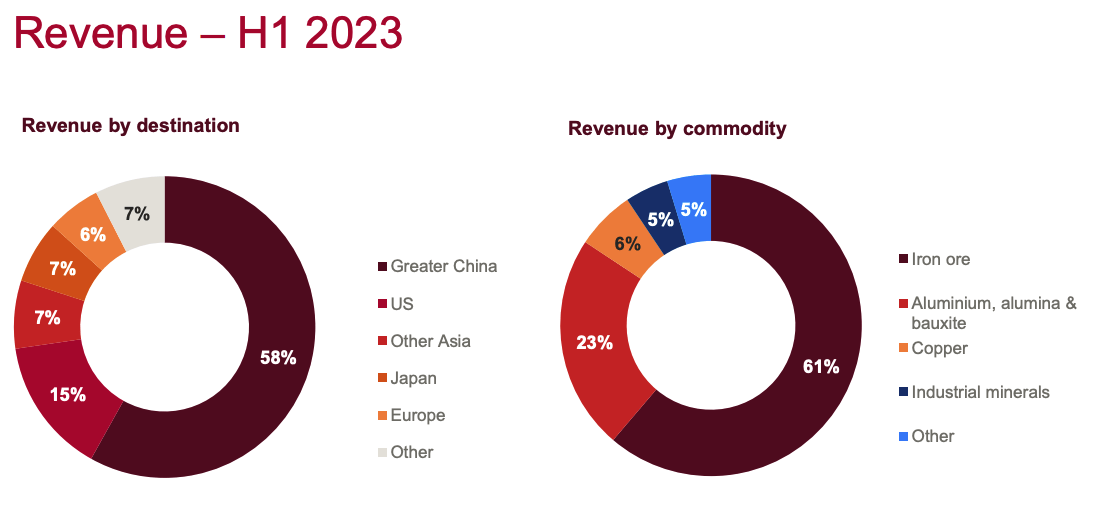

Rio Tino Plc is the largest holding in SLX and makes up 13.4% of the fund. While RIO is significantly exposed to the steel industry, it is far from a pure play. As shown from the chart below Iron ore accounts for ~61% of RIO's revenue. While Iron ore is nearly a steel pure play as almost all iron ore production is used as an input in steel making, the other commodities that RIO is exposed to have different uses. While aluminum, copper, and other industrial mineral prices are often correlated with steel they are in fact different markets driven by different factors.

{kind=link}

Highly Competitive Industry

The steel industry is a highly competitive global industry that is primarily dominated by China. For 2021, China accounted for 52% of global production . The second largest producer, India, accounted for just 6% of global production. The U.S., which was the fourth largest producer accounted for just 4.3% of global production. Due to the fact that steel is a commodity in nature, it is very hard for firms to generate a competitive advantage. For this reason, it has been difficult for the industry more broadly to achieve strong shareholder returns.

Weak Relative Performance Since Inception

As shown by the chart below, since its inception date in October 2006, SLX has significantly underperformed the S&P 500. This does not come as a surprise to me given the highly competitive industry dynamics. Moreover, the underperformance is especially troubling when considering the ~1.7 average historical 3-year trailing beta of SLX. Given the very high beta, one would have expected that SLX would have outperformed given the strong move higher in the S&P 500 since SLX's inception date, but that has not happened.

High Dispersion of Underlying Holdings

As shown by the chart below, SLX's top holdings have exhibited a wide range of performance. Since SLX's inception, the best performer of the top five SLX holdings, Nucor, has returned more than 348%. The worst performer of the top five SLX holdings, Tenaris, has returned just 39%.

Given the high dispersion of the underlying holdings of SLX, I think it is worthwhile for investors to evaluate which stock or group of stocks from the index are worth owning vs simply buying SLX.

An Alternative to SLX

While I am generally not bullish on the steel or iron ore industries due to the significant amount of competition and inability of companies to earn above market returns over long periods of time, there is one name that stands out above the rest: Nucor.

As shown below, both Seeking Alpha and Wall Street analysts currently rate NUE as a buy, In addition to that, as shown by the charts below, NUE has a very strong history of generating shareholder returns well in excess of the S&P 500.

Seeking Alpha

Conclusion

SLX represents a relatively unique ETF as it is one of the only ETFs to focus on the steel industry. However, SLX charges a very high management fee for a passive product. Moreover, while SLX is the ETF that has the most steel exposure it is not a pure play as the largest holding, Rio Tinto generated 39% of its revenue outside the steel value chain.

While the trailing PE ratio of just 8x seems cheap on the surface, I am not attracted to the steel sector due to the high degree of competition and high degree of cyclicality. I am currently of the view that the risk of a recession is currently elevated and thus I prefer to be more defensively positioned.

Investors who have a more bullish macro view and want to consider expressing a bullish trade in the steel space may want to consider NUE as a viable alternative to SLX given NUE's strong long-term performance history along with bullish ratings from both the Seeking Alpha and Wall Street analysts.

For further details see:

SLX: Why I Am Not A Buyer