SLYG - SLYG: Small-Cap Growth Stocks Are Clearly Undervalued

Summary

- SLYG invests in small-cap U.S. growth stocks.

- On a sub-consensus earnings growth projection, the fund is very much likely to be undervalued.

- SLYG is well-diversified and offers a strong headline IRR of over 10%, with a potential near-term boost to valuation of 10-20%.

SPDR S&P 600 Small Cap Growth ETF (SLYG) is an exchange-traded fund that provides investors with exposure to small-cap growth stocks. The fund corresponds with the S&P SmallCap 600 Growth Index , the fund's chosen benchmark (and essentially its "target"). Given the fund's benchmark and strategy, SLYG is limited exclusively to the United States. Stocks are drawn from the S&P 600 index, which is basically the smallest 600 stocks within the wider S&P 1500 index. Growth stocks are drawn from this index on the basis of three factors: sales growth, price/earnings growth ratios (i.e., the "PEG" ratio), and momentum.

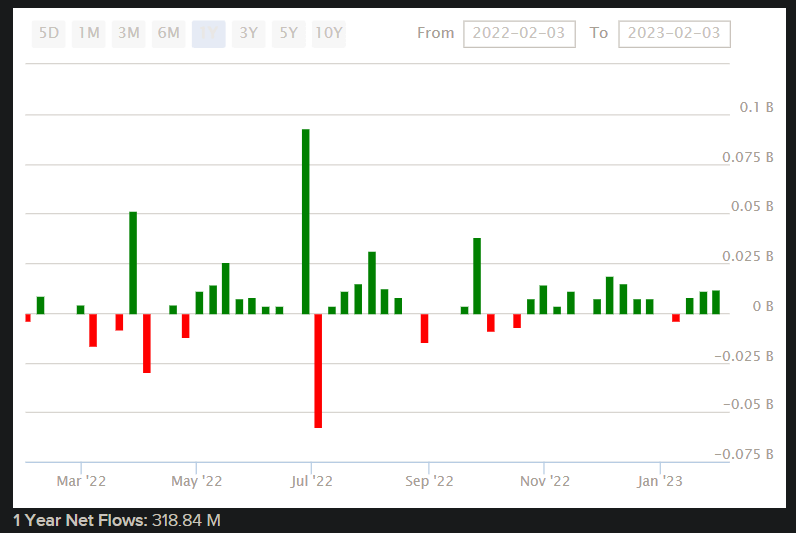

SLYG's net assets under management were $2.48 billion as of February 3, 2023. That follows a year of positive inflows (see below) of over $300 million.

{kind=link}

The fund is relatively popular. The gross expense ratio is low at just 0.15%. Small-cap stocks traditionally offer an elevated equity risk premium, which is another way of saying "higher returns", in exchange for perceived higher risk. If earnings come in as projected, you earn the additional premium through higher distributions (dividends, buybacks) and/or higher capital appreciation. However, sometimes elevated equity risk premiums prove prudent, as earnings come underneath prior projections. Earnings, as ever, are critical. That should focus the mind on one's assumptions, and whether one is comfortable to invest with conviction in those assumptions.

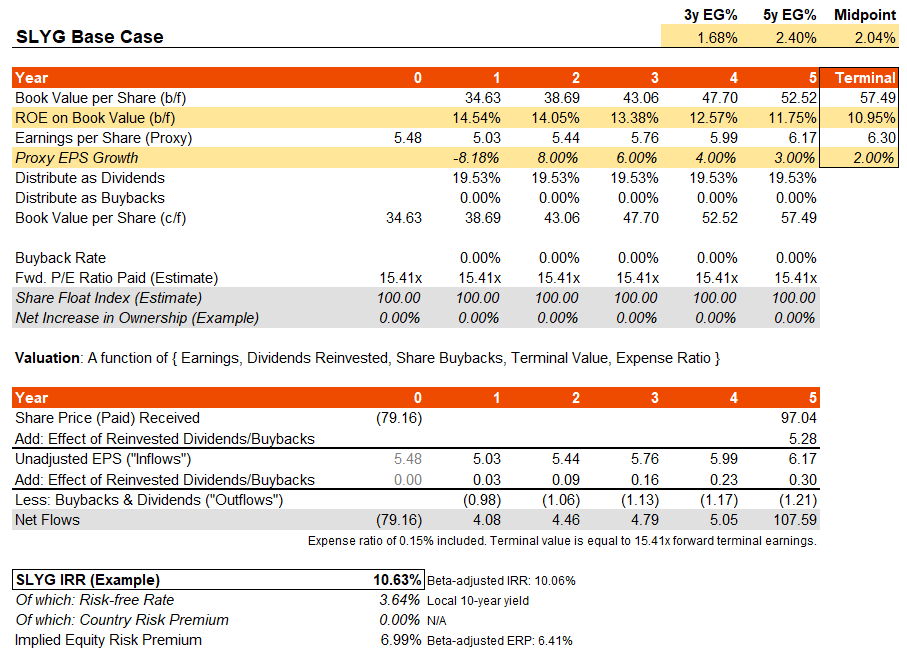

SLYG's benchmark index 's most recent factsheet, as of January 31, 2023, offers trailing and forward price/earnings ratios of 14.15x and 15.41x, respectively, with a price/book ratio of 2.24x. This data implies a forward return on equity of about 14.5%, with a forward year-one earnings growth rate of -8.18% (yes, negative). Morningstar meanwhile think the three- to five-year earnings growth rate will run to about 12% (at the consensus average). That seems unlikely to me, however I am willing to at least estimate a bounce back in earnings in the year following the forward negative growth, and then a gradual decline thereafter to find a 2% earnings growth to perpetuity rate. Keeping the earnings multiple constant and assuming no buybacks, my IRR potential comes to 10.63%.

{kind=link}

That is after the modest expense ratio, etc., and also assumes dividend distribution rates are similar as to the past. Given the diversification of the fund, with 339 holdings, SLYG's historical beta is only about 1.1x, so the adjusted equity risk premium derived from my apparently sub-consensus assumptions comes to 6.41%. That is higher than the 4.2-5.5% range I'd anticipate for U.S. equity funds (on a beta-adjusted basis). So, SLYG looks undervalued, plain and simple. Whether or not the small-cap premium still exists in general, I think it's evident that it exists across SLYG's portfolio.

Should SLYG even approach more optimistic long-term expectations of earnings growth, shareholders will do exceptionally well. However, with a forward return on equity of 14.5% already considered, I think my projection of a portfolio-wide drop in the ROE to 11% by my terminal year six is a good conservative basis with which to build a valuation gauge (as above). The headline IRR of 10.63% is good in nominal terms, but also relative to the risk involved: I would assume an IRR of sub-9% as being fair. On valuation alone, I therefore think a boost of 10-20% to SLYG's share price would be unsurprising.

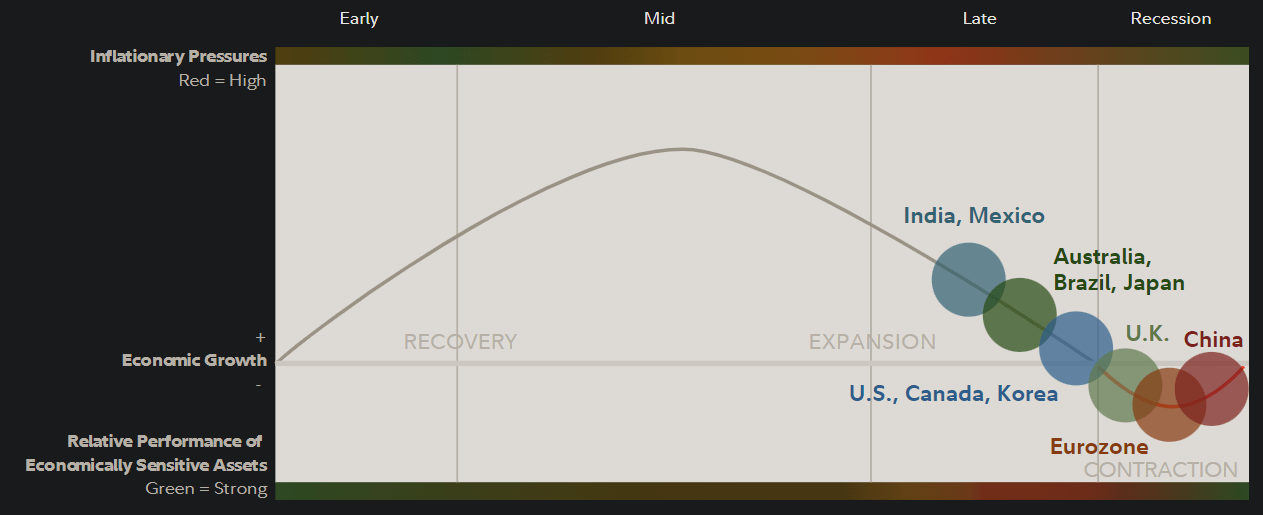

SLYG is therefore also ripe for out-performance potential. The fund has, roughly in line with its historical beta, out-performed the S&P 500 so far this year. I think will continue, however the market cycle is important. Last year was terrible for investing. Should the business cycle begin to properly turn, the market cycle should turn 6-18 months ahead of any business cycle trough (downturn or recession). It is very possible we have already seen the trough in the market cycle, so I would take a bullish view on SLYG. The image below illustrates business cycle positioning as of Q1 2023 (estimated by Fidelity).

{kind=link}

SLYG should perform well over the next five years. Some ask why I might take a bullish view on a fund whose earnings are expected to fall in the near term; I am comfortable with taking the view because those lower earnings are likely already priced in. Even after accounting for this near-term dip as projected, SLYG looks like it is trading at a discount.

For further details see:

SLYG: Small-Cap Growth Stocks Are Clearly Undervalued