SM - SM Energy: A Look At Its Potential 2023 Results

Summary

- SM instituted a return of capital program that includes up to $500 million in share repurchases.

- It also increased its dividend from a $0.01 semi-annual dividend to a $0.15 quarterly dividend.

- I've modeled a scenario where SM generates close to $800 million in positive cash flow in 2023 at current strip, while holding production roughly flat.

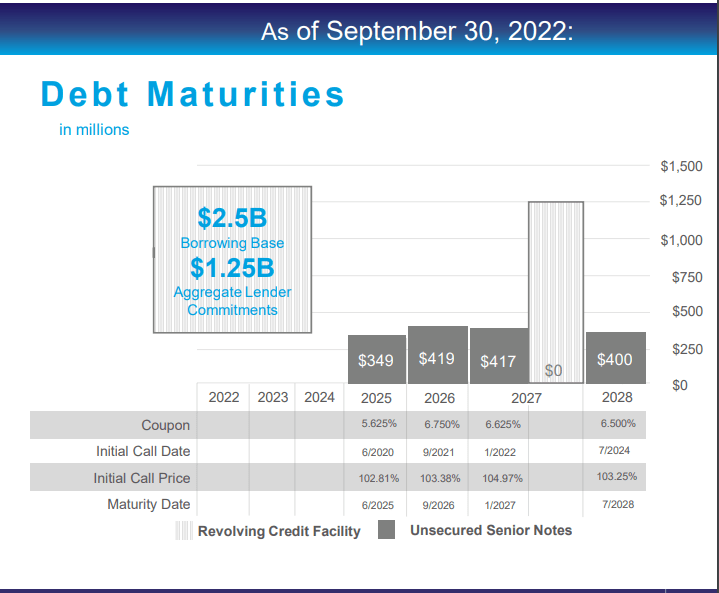

- SM also has the ability to redeem some of its unsecured notes, although this is optional and its next maturity isn't until June 2025.

SM Energy ( SM ) recently instituted a $500 million share repurchase program in addition to its increased dividend of $0.15 per share per quarter. It has not disclosed its 2023 plans yet, but I believe it could roughly hold total production flat compared to 2022 and increase its oil cut slightly while also generating close to $800 million in positive cash flow (before cash income taxes) at current strip prices.

SM's 2H 2022 production was negatively affected by delayed well completions and impacts from offset activity, but its production should be stronger in early 2023. In addition to repurchasing shares, SM also has the option to redeem some of its outstanding unsecured notes. These notes have reasonable interest rates though, so SM may not be in a hurry to redeem them though.

Potential 2023 Outlook

I am currently modeling SM's 2023 production at 145,000 BOEPD (48% oil), although it has not disclosed its plans for 2023 yet. This is essentially the same as SM's expected 2022 average daily production , along with a modest increase in SM's oil cut.

With the natural gas strip for 2023 now down significantly versus a few months ago, I've assumed that SM's 2023 development plans focus more on the Midland Basin along with the oilier portions of its South Texas acreage.

At current 2023 strip of high-$70s WTI oil along with $4.30 NYMEX gas, I project that SM will thus generate $2.58 billion in revenues after hedges. I've assumed a fairly significant natural gas differential at negative $1.05 to NYMEX for 2023. SM realized positive $1.01 to NYMEX in 2021, although this deteriorated to negative $0.62 in Q3 2022.

SM's 2023 hedges have around negative $18 million in value at current strip. In this production scenario, it has approximately 24% of its 2023 oil production along with 28% of its 2023 natural gas production hedged.

| Type |

| Barrels/Mcf |

| $ Per Barrel/Mcf |

| $ Million |

| Oil |

| 25,404,000 |

| $78.00 |

| $1,982 |

| NGLs |

| 7,293,065 |

| $30.50 |

| $222 |

| Gas |

| 121,367,610 |

| $3.25 |

| $394 |

| Hedge Value |

| -$18 |

| Total |

| $2,580 |

I've modeled $975 million in capital expenditures for SM in 2023, which is approximately 10% above its 2022 budget. This reflects the impact of cost inflation . SM's lease operating expense is modeled based on Q4 2022 levels, while its transportation costs are modeled slightly lower than Q4 2022 levels based on SM's expectations for a decrease in South Texas transportation costs in mid-2023.

| $ Million |

| Lease Operating |

| $296 |

| Transportation |

| $167 |

| Production and Ad Valorem Taxes |

| $156 |

| Cash G&A |

| $100 |

| Cash Interest |

| $105 |

| Capex |

| $975 |

| Dividends |

| $74 |

| Total |

| $1,873 |

This results in a projection that SM can generate $781 million in positive cash flow in 2023 at current strip before dividends. SM's current quarterly dividend of $0.15 per share adds up to around $74 million in dividends per year.

This doesn't include any potential impact from cash income taxes.

Return Of Capital

In addition to increasing its fixed dividend from a semi-annual payment of $0.01 per share to a quarterly dividend of $0.15 per share, SM has started repurchasing shares. It currently has the authorization to spend up to $500 million on share repurchases and spent approximately $20 million in Q3 2022 to repurchase 453,000 shares.

SM had $498 million in cash on hand at the end of Q3 2022 and it could theoretically redeem some of its outstanding unsecured notes during 2023 in addition to repurchasing shares. The interest rates on its unsecured notes are reasonable (ranging from 5.625% to 6.75%) and its next maturity isn't until June 2025, so it may decide to take its time redeeming its unsecured notes though.

{kind=link}

Notes On Valuation

SM's value (as a one-year target price) is now estimated at approximately $47 per share in a scenario with long-term (after 2023) $70 WTI oil and $4.00 NYMEX gas. This also assumes that SM's realized natural gas price averages close to NYMEX in the long-term. Each negative $0.30 increase in long-term natural gas differentials reduces SM's estimated value by approximately $1 per share.

Conclusion

SM Energy should see its production rebound from 2H 2022 levels in 2023 and I am modeling its total 2023 production as roughly flat compared to 2022, along with a slightly higher oil cut. The decrease in expected near-term natural gas prices probably will result in SM shifting capital to oilier areas.

At current strip for 2023, SM may be able to generate close to $800 million in positive cash flow. This will help fund its share repurchases as well as potentially allow it to redeem some of its unsecured notes. SM already has nearly $500 million in cash on hand and its next note maturity isn't until June 2025, so it is in pretty good shape debt wise.

For further details see:

SM Energy: A Look At Its Potential 2023 Results