SM - SM Energy: Buying And Holding Through Another Drawdown

2023-12-29 11:29:08 ET

Summary

- SM Energy has experienced extreme volatility in its stock price, with a maximum drawdown of almost 98% in the last five years.

- The company has survived multiple downturns in the oil and gas industry, including the oil bust of 2015-2016 and the pandemic-induced demand problem in 2020.

- SM Energy has improved its financial position, with lower debt levels, positive cash flows, and a focus on returning capital to shareholders. Valuation metrics suggest the company is undervalued.

- The risk-reward seems balanced at this point, and I rate this as a Buy.

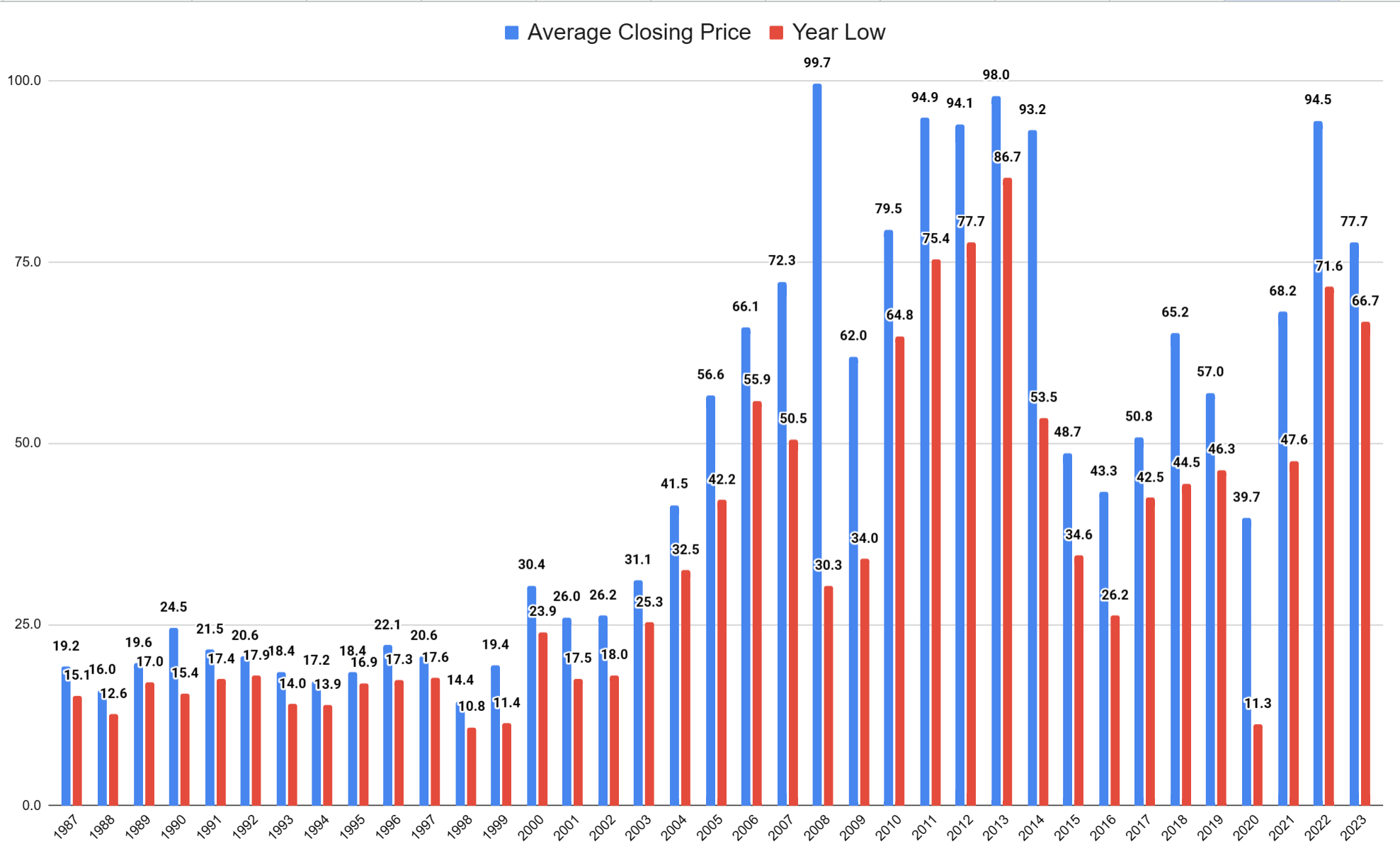

Investors in SM Energy ( SM ) had to contend with the enormous volatility of this stock. Looking at the chart, it's definitely not for the faint of heart. The price had multiple meltdowns over the last 2 decades, and the maximum drawdown over the last five years is almost 98%!

Price action has remained flat for almost 18 years, and it is a long way away from its all-time highs. As a mid-cap Oil & Gas E&P company, this behavior could be quite typical. Stock price movement is tied to the price of oil, and the pandemic saw one of the biggest price swings in the history of oil. Companies routinely go bust during such periods.

- More than 100 oil and gas companies declared bankruptcy in 2020.

- Almost 150 bankruptcies during the oil bust of 2015-2016.

- The Great Recession had rolling effects on the industry much after 2010.

But through all these downturns, the company has managed to survive. Let us examine the company through its journey and what it would mean to buy and hold this stock.

Understanding SM Energy and its Latest Quarter Activity

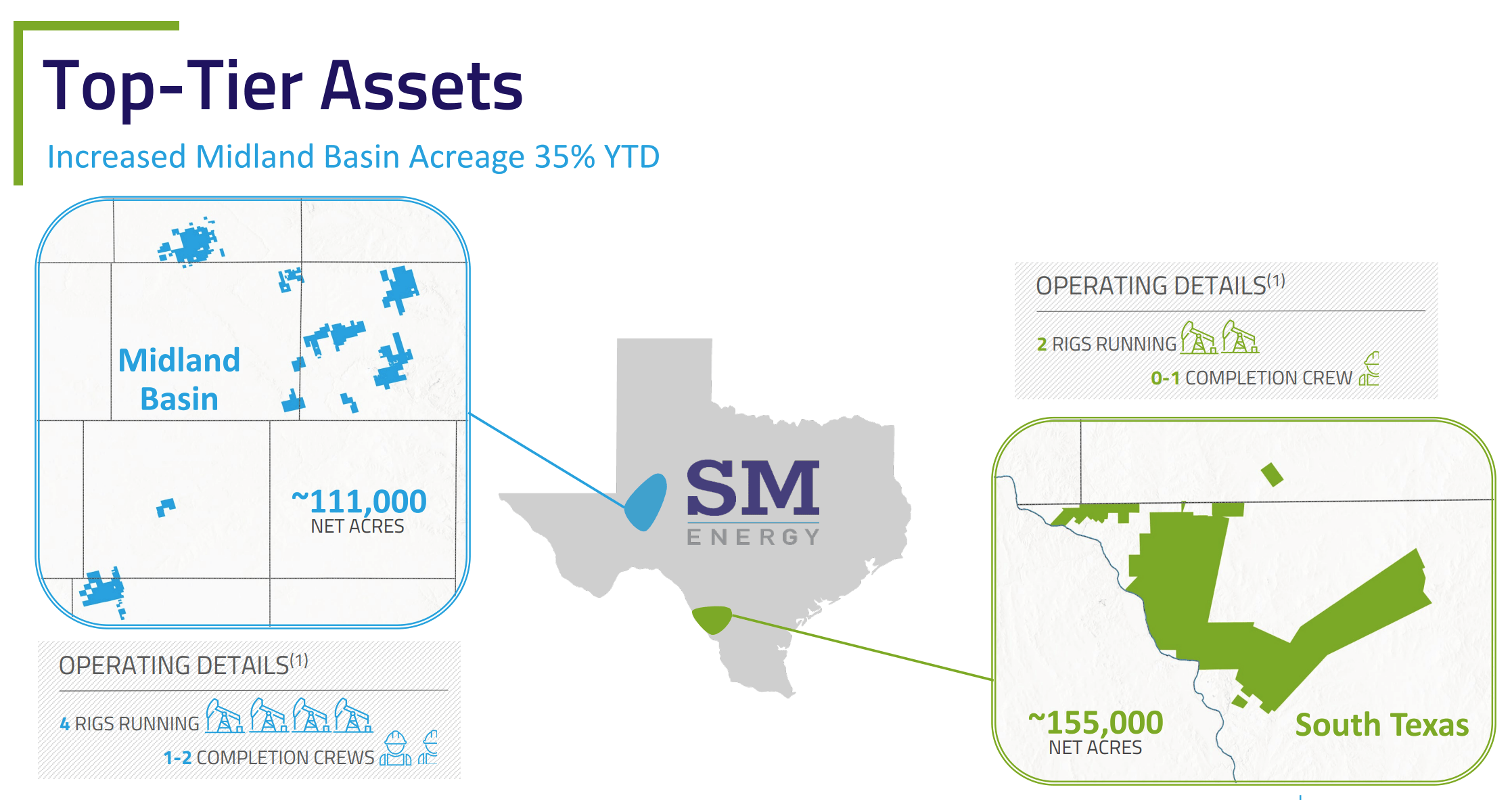

SM Energy Company is an upstream oil and gas company that focuses on the acquisition, exploration, development, and production of oil, natural gas, and natural gas liquids in Texas. The company has significant estimated proven reserves and working interests in productive oil and gas wells in the Midland Basin and South Texas.

{kind=link}

In each of its operating areas, it expects its inventory to last more than 13 years, and nearly 80% of inventory is classified as 3P reserves having economic and geologic certainty. With growing acreage currently standing at 301K, the company is well-positioned for years to come.

The latest quarter saw a production of 153.7 MBoe/d with Oil/Liquid percentages at approximately 40/60. Year to Date, it saw a net of 61 wells drilled across its operating areas and net flowing completions of 81 wells.

{kind=link}

Possible Reasons For its Extreme Drawdowns

When we look at the company itself, its assets, and its operations there are no red flags that stand out (As we saw, its operational roots in Texas are strong, and we can expect this to continue in the future as well). However, its extreme price movements during oil price distress made it look like a company about to go bankrupt. So, I want to see if this was warranted by the market. What would give me the confidence to buy and hold the stock? Would I throw in the towel at the first sign of oil price distress?

Examining past beatdowns

Crude Oil Price History (Author generated chart using the data from MacroTrends)

{kind=link}

The 2007-2009 period saw a big dip in oil prices due to the effects of the great financial recession. Revenue took a dip of almost 36% in 2009, net income went slightly negative, but operational cash flow was still positive.

The 2014-2016 period saw a dip in oil prices due to an excess supply problem that was exacerbated by OPEC. Revenue took a dip of almost 40% in 2015, net income showed a big loss, but operational cash flow was still positive.

2020 was the pandemic-induced demand problem that saw the company trading at the lowest point in its history. Reported revenues dipped by almost 30% from 2019 and were similar to 2016 levels. The year also saw the biggest loss reported in the company's history, but operationally, cashflows only saw a modest change from previous years.

But the biggest items of note in all these instances are its huge dips in free cash flow and its liquidity problems. Understandably, its Capex levels and zero cash positions during these years could have spooked investors.

Present Situation

The management may have learned sufficient lessons and has been steering the company in a positive direction. Year-to-date, the company has seen good FCF levels and has also focused on maintaining sufficient liquidity.

{kind=link}

It has diligently worked to clean up its balance sheet and has significantly brought down its debt levels. Its debt-to-equity ratio is at its best level in a decade, and its debt is well covered by its operational cash flows.

Additionally, it has been working to return capital to shareholders. In the latest quarter, it increased its dividend by 20% and repurchased 2.35M shares (Repurchased 6% of Shares Outstanding since it started the buyback program). So it is safe to say financially and operationally, the company is in a safer position now and is prepared if we see another downswing in oil prices.

Valuation

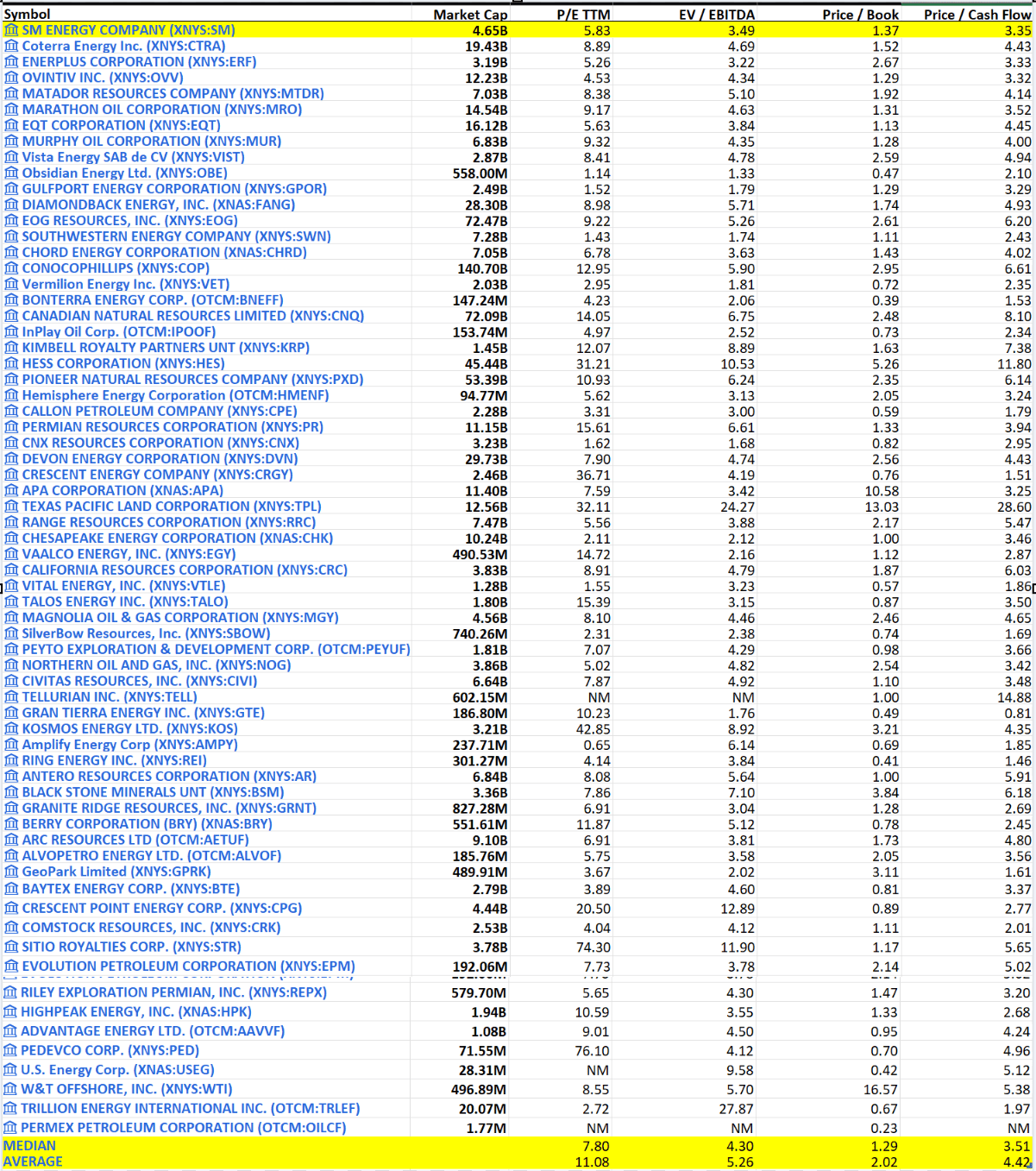

Viewing it from the lens of multiple valuation metrics, the company is quite undervalued not only when you compare it to the sector but also when you zoom into the industry.

| Metric |

| SM Energy |

| Energy Sector |

| PE |

| 5.8 |

| 9.3 |

| EV/EBITDA |

| 3.5 |

| 5.6 |

| PB |

| 1.4 |

| 1.6 |

| P/CF |

| 3.3 |

| 4.6 |

We have seen these multiples expand over the year, which could be an indication of increased investor confidence in the company's prospects.

Valuation Industry Components (SA)

{kind=link}

For a deeper insight, when we look at the company and compare it to the other components of the Oil and gas E&P Industry, it fares quite well. Earnings, EV to EBITDA, and Cash flow multiples are below the median. If the company continues its buyback program, the boost it provides to EPS could play well into our earnings multiple. But at the same time, its earnings are highly dependent on Oil prices as only 25% of its products are hedged, which would pull the multiples in the other direction should the price of oil fall.

Closing Thoughts

Oil prices are self-correcting which means low prices are the cure for low prices, high prices are the cure for high prices and the industry itself is well known to be highly cyclical. So any problems the industry faces could be short term (the price movement from the crude oil chart from earlier also proves this fact). So, my main concern going into any oil and gas company (esp. upstream) is whether I am buying the company at a fair price and if it can survive the drop.

I believe SM Energy's experiences in the last two decades have made it stronger. It knows the levers it needs to pull to survive. When you look at its financials and its operations now, it looks more than ready to survive a depressed environment. On the upside, the company is focused on optimization and returning value to shareholders, which means even in a flat environment we could see positive returns. The risk-reward seems balanced for an investment, and I would rate this as a Buy.

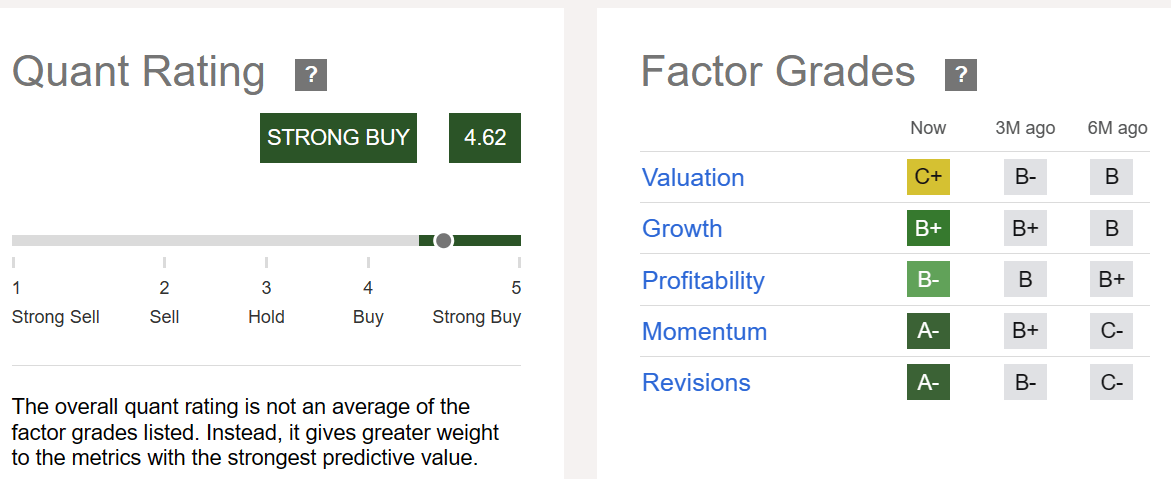

The cherry on top is the company's Quant score. Seeking Alpha's Quant rating puts this company at a Strong Buy (For more than a decade, SA's backtested strategy has delivered returns, beating the S&P 500 every single year).

{kind=link}

For further details see:

SM Energy: Buying And Holding Through Another Drawdown