SM - SM Energy: Not A 'Premier' Operator (Neither A Compelling Dividend Payer)

2023-03-28 07:47:27 ET

Summary

- Last August, I suggested energy investors take a pass on SM Energy due to its relatively gassy production, its weak hedge book, and lack of dividends compared to peers.

- SM stock is down significantly since that article was published, but the company made strong progress paying down its debt load and has begun a $0.15/share quarterly dividend.

- Today, I'll take a fresh look at SM Energy and see if it might be an oil & gas company worthy of an allocation of your hard-earned investment dollars.

As mentioned in the bullets, last August I wrote a Seeking Alpha article suggesting energy investors take a pass on SM Energy ( SM ) due to a number of negative headwinds: a relatively high gas-to-oil ratio ("GOR"), a weak hedge book that kept it from taking full advantage of the O&G price rally, and a high debt-load that kept it from returning cash to shareholders like the real tier-1 shale operators were doing (see SM Energy: Don't Be Fooled ). I got a lot of pushback from SM Energy bulls, but it was a fairly easy call to suggest O&G investors would be much better off in shares of companies like ConocoPhillips ( COP ), EOG Resources ( EOG ), or Pioneer Natural Resources ( PXD ) - all of which were returning tons of free-cash-flow to shareholders in the form of dividends (base+variable) and stock buybacks. Since the article was published, that narrative played out much as expected (see chart below). However, given the severe price decline in shares of SM, today I'll take a fresh look at the company to see if I should change my SELL rating.

Investment Thesis

In a February Presentation , SM Energy detailed its leaseholds in the Midland Basin of the Permian and in the Austin Chalk play of South Texas.

{kind=link}

SM Energy

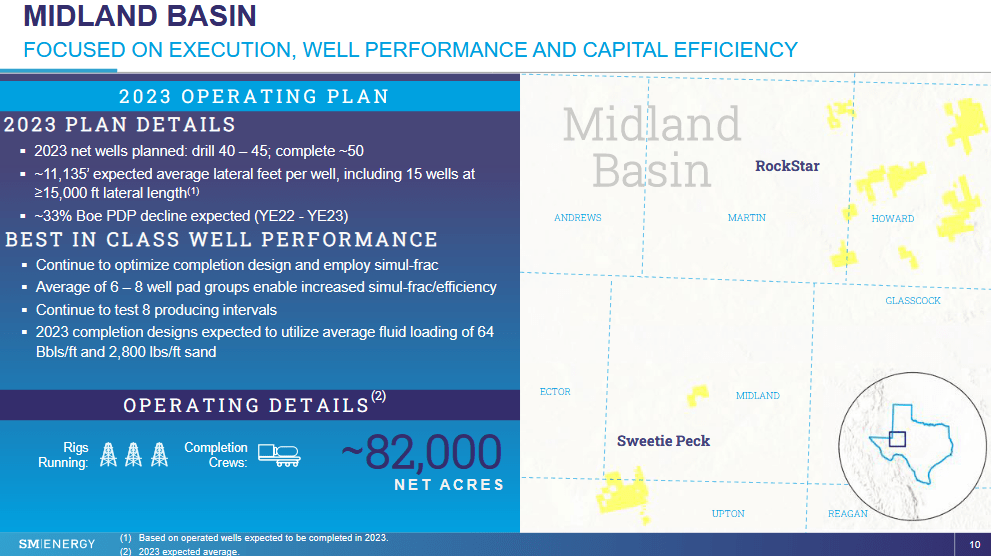

In the Midland Basin (shown above), SM holds 82,000 net acres but note they are relatively dispersed across 4-counties. Typically leaseholds like to be more continuous in order to drill longer laterals as well as to have production more or less centralized for better terms on off-take agreements with pipeliners. That is especially the case when you are competing with companies that have much more than SM's average of 140-150,000 boe/d of production.

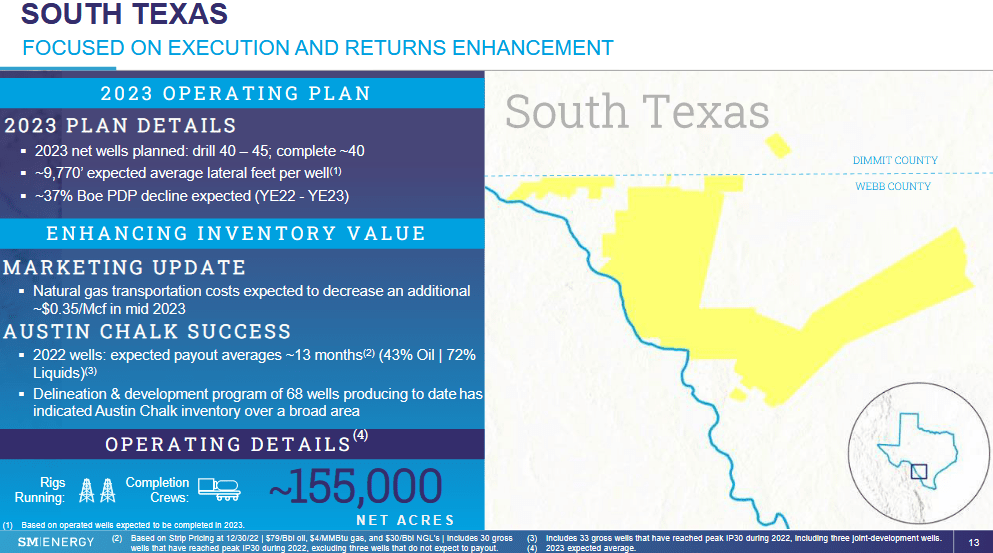

In the Austin Chalk play (shown below), SM has 155,000 net acres that are relatively contiguous:

{kind=link}

SM Energy

However, the Austin Chalk is a much gassier play.

SM Energy promotes itself as a "premier operator" with "top-tier" assets. However, I would argue with both those adjectives, but in the end its the financial results that ultimately matter. So let's take a closer look.

Earnings

SM Energy reported Q4 and full-year earnings in late February that were generally considered to be a top- and bottom-line beat , even as revenue of $673.1 million fell 21.5% yoy. Highlights for FY22 included:

- Net income for the full-year 2022 was $1.11 billion compared to $36.2 million in FY21. But for Q4, net income was $258.5 million - significantly lower as compared to $424.9 million in Q4 of FY21.

- For full-year 2022, the company reported it generated adjusted free cash flow of $848.7 million, more than double the adjusted free cash flow generated in 2021. Obviously, there was good progress made here.

Given the uptick in profitability, SM was able to take several steps that were supposed to increase shareholder returns. These include:

- Announced a return of capital program on September 7, 2022 that enabled the company to buy back 1,365,255 shares for $57.2 million.

- Announced a $0.15/share quarterly dividend ($0.60/share on an annual basis).

I said supposed to increase shareholder returns, but note that the $57.2 million the company spend on share buybacks in FY22 was almost 3x what it paid in dividends last year (only $19.6 million). Not only that, the estimated average share price for the shares repurchased was $41.90/share and the stock is currently trading at $27.83. What a waste - clearly investors would have been much better off with additional dividends directly into their pockets.

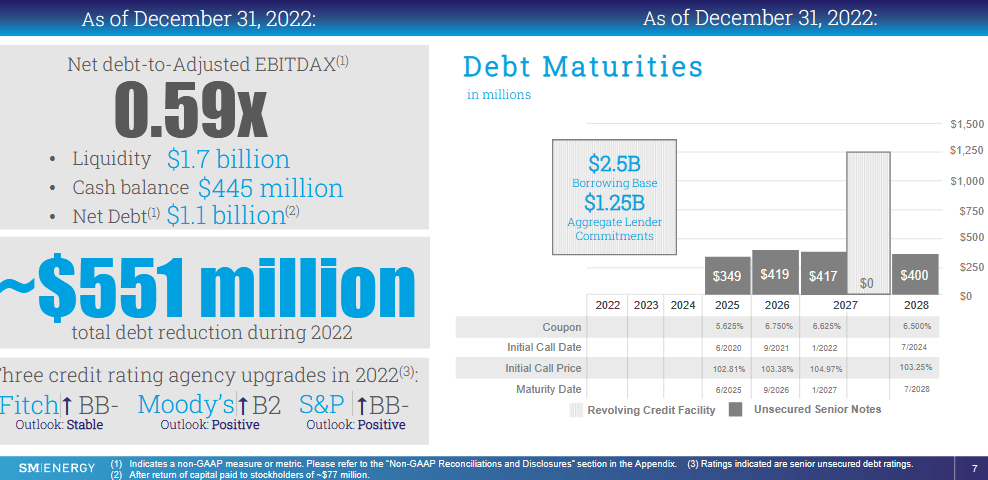

The good news is that cash and cash equivalents at year-end 2022 were $445.0 million and that was after SM redeemed $551.4 million of long-term debt during the year and ended 2022 with a net debt-to-Adjusted EBITDAX ratio of 0.59x. So, significant progress on the debt-load was made last year , leaving the company with no debt maturation this year or next:

{kind=link}

SM Energy

Going Forward

Yet, as far as the rock goes, SM is much the same company as it was before - quite gassy. I say that because Q1 guidance was for:

Production: is expected to range between 12.9-13.1 MMBoe, or 143-146 MBoe/d, at 42-43% oil . Production volumes consider the expected effects of offset activity and curtailments.

Clearly, the GOR is still very high, and as I have been writing lately, the price of natural gas in the U.S. has just cratered (see The Demise of NYMEX (Not To Mention Waha )).

But I will mention Waha because it is important to know that SM Energy reported it has ~25% of 2023 production hedged, including this gem taken from the previously referenced February presentation:

900 BBtu is hedged to Waha at a weighted-average price of $3.98/MMBtu, and we have ~9,100 Bbtu of Waha basis is hedged with a weighted-average price of $(1.23)/MMBtu

Note the parenthesis around the $1.23 ... that means SM will be paying $1.23/MMBtu to have a pipeliner take away that production - 10x the volume of the $3.98/MMBtu hedges. So not only is SM a gassy producer, it is effectively giving away much of that gas production. The company obvious has not locked up pipeline capacity for its relatively large gas production.

This matters. SM reported its pre/post realized price for full-year 2022 were $63.18/boe and $49.76/boe , respectively. That compares to ConocoPhillips - which is 100% un-hedged, which achieved an average realized price last year of $79.82/boe , or more than $30/boe more than SM Energy . Now that is "premier operator" with a "tier-1" asset base.

In addition, SM said it will continue to over-emphasize share buybacks over the dividend and expects to spend a whopping total of an estimated $500 million on buybacks through 2024 (say $250 million/year). For comparison's sake, SM's current market-cap is $3.2 billion.

Reserves

There was some good news on the reserves front, notably:

- The RRR (reserves replacement ratio) came in at 205%.

- Total proven reserves were 537 million boe.

- Total inventory was estimated at 10-13 years, with ~80% of reserves being categorized as 3P (proven, probable, possible).

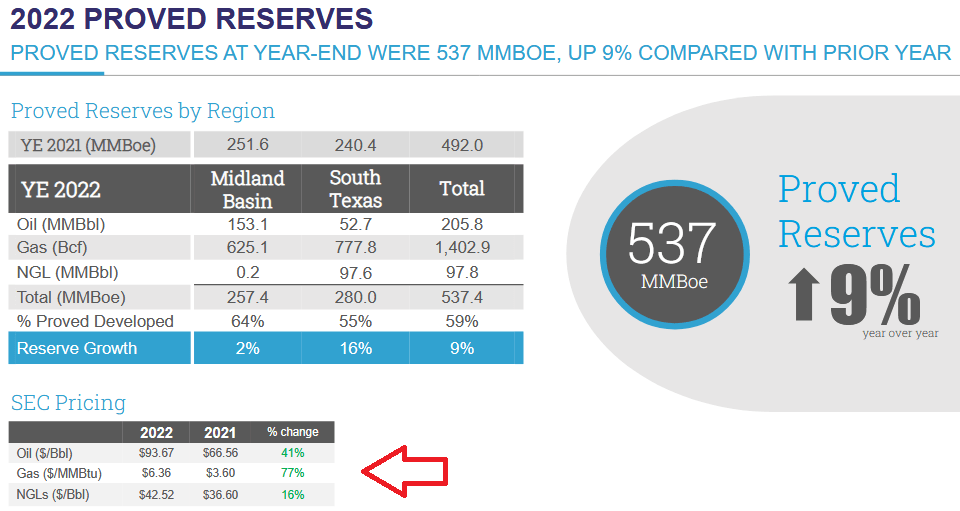

However, before shareholders get too excited, note the SEC pricing (red arrow) at which these reserves were based on:

{kind=link}

SM Energy

That is, oil was at $93.67/bbl and more importantly for a gassy producer like SM, dry gas was at $6.36/MMBtu (NYMEX is currently at $2.24/MMBtu ). And, as I have been writing on Seeking Alpha, I think there is a good chance that Waha goes negative (once again ...) this year.

Valuation

SM Energy currently trades with a TTM P/E of 3.0x and a forward P/E of 4.0x. The $0.60/share annual dividend equates to a yield of 2.35%.

Summary & Conclusion

In my opinion, and despite all the positive steps the company took during the high-priced oil & gas cycle last, the company is still less than compelling. I say that because today it still has many of the same problems it had going into 2022: primarily gassy production and a weak hedge book. That said, the balance sheet is certainly much improved - as is the valuation level.

However, it is clear that management will continue to short-change investors on the dividend in favor of massive share buybacks that arguably are much more beneficial to the executive management team as they are for ordinary shareholders. Yet the management team is certainly getting a better deal at today's stock price as compared to the average $41.90/share it paid for the $57.2 million spent on shares last year.

Put it altogether and I am raising my rating from SELL to HOLD. However, for investors that don't own SM Energy stock, I strongly encourage them to consider COP instead. It does have tier-1 shale assets (for real ...), excellent exposure to Brent oil pricing, a strong global LNG portfolio, and its (base+variable) dividend policy. Even though COP is also over-emphasizing share buybacks, the company did deliver total dividends of $4.99/share last year ( see COP : Strong APLNG Results Will Buoy Thursday's Q4 Report).

For some longer-term perspective, I'll end with a 10-year total returns comparison of SM Energy to some of its L-48 shale peers: COP, EOG, PXD, and Occidental Petroleum ( OXY ):

For further details see:

SM Energy: Not A 'Premier' Operator (Neither A Compelling Dividend Payer)