SM - SM Energy: Strong Free Cash Flow At An Attractive Valuation

2023-12-28 13:29:19 ET

Summary

- SM Energy has seen solid performance, gaining nearly 20% despite recent pressure on commodity prices.

- The company has improved productivity from its cap-ex program, generating more free cash flow.

- SM Energy's oil-centric production profile and strong financial performance make its shares attractive at their current level.

Shares of SM Energy (SM) have been a solid performer, gaining nearly 20%, even as commodity prices have come under pressure recently. This year, the company has seen far better productivity from its cap-ex program, helping it to generate more free cash flow. Oil generates the vast majority of its revenue, which I view positively. Even in a $75 oil/$2.50 natural gas environment, SM can generate $450-500 million in free cash flow, making shares attractive at their current level.

{kind=link}

SM Energy is a midsized oil and gas producer. It has111,000 acres in the Midland basin (up 35% this year via bolt-on acquisitions and asset swaps) and 155,000 in South Texas. With its current asset base, SM has over 10 years of economic inventory, limiting the need to do more than modest M&A. Oil accounts for 44% of its production and 78% of revenue. Natural gas is 13% of revenue, and NGLs are 9% of revenue.

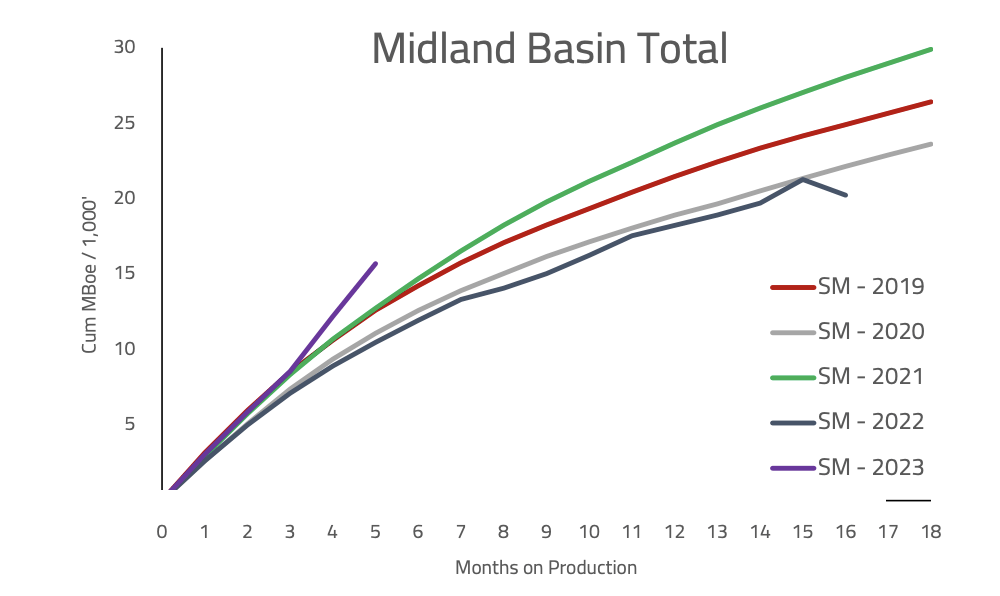

In the company's third quarter , SM earned $1.73 in adjusted EPS. This was down from $1.82 last year as natural gas prices were substantially lower. Including hedges, realized oil prices of $78 were up 10% from last year while natural gas was down 49% to $2.84. Total realization of $45.22 were down about 10% from $50.58 last year. Despite significantly lower commodity prices, adjusted EBITDAX of $476 million rose by 3% from last year, a very strong performance, aided by higher production and low costs. In fact, Q3 production of 153.7mboe/d eclipsed guidance. Oil volumes rose by 9%, natural gas by 6%, and NGLs by 35% for 12% total growth. Management is targeting a further mid-single digit pace of oil production growth in 2024. As you can see below, SM is getting more oil out of the ground more quickly in its key Midland basin play this year, as new acreage has paid off. 2021 had been a record year, but 2022 results were less impressive. In 2023, SM is back to setting new company records, meaning its cap-ex spending is more lucrative, generating more cash flow more quickly for the company, which is why we are seeing SM manage through this commodity price environment fairly well.

{kind=link}

Additionally, as noted earlier, SM gets nearly 80% of revenue for oil. And with oil production growing more quickly than gas production as SM focuses its cap-ex spending on oil-heavy acreage, this weighting should continue to grow, which I view positively, given what I see as a more favorable commodity supply/demand environment.

In 2022, natural gas surged as investors anticipated a significant shortage following Russia's invasion of Ukraine. This was a rally that I thought could sustain for several years, given the impact of Russia ceasing exports of gas to Europe. However, Europe managed through the winter better than most expected, which has helped to normalize prices. In fact, European natural gas prices are down by 2/3 from a year ago. I would note that European gas prices are different than American natural gas prices because the natural gas market is still a local, not global market. The world has limited LNG export and import capacity, with liquefication costly and tankers scarce.

While LNG can certainly marginally impact prices, because a producer cannot route all of their production to the export market, wide differentials in natural gas prices around the world can persist. In other words, investors should not bet on US and European gas prices ever converging entirely because we have an abundance of domestic gas. The International Energy Agency does expect natural gas demand to grow globally in coming years, but the majority of this demand growth comes from overseas with our domestic demand forecast to fall slightly. This is likely to limit NYMEX natural gas appreciation in my view, and all else equal, US producers would benefit if demand growth were coming domestically rather than internationally. This is why I have expressed a preference for oil to gas producers, all else equal.

IEA

Indeed, as you can see, natural gas prices have plunged over the past year. The expected tailwind from LNG exports has proven to be quite small, while domestic production continues to rise, thanks to our abundancy of gas, pushing prices lower.

{kind=link}

Now, as you can see below, oil prices are also lower, but the drop has been far more modest, at just 7%. And unlike for gas, there is an international cartel, OPEC+, which has limited its own production in an effort to support prices. Moreover, by 2028, the International Energy Agency (IEA) expects global oil consumption to be more than 5% above 2022 levels. Even as renewable energy usage rises, growth from EM will continue to propel oil demand higher over the medium-term. This pace of growth is a bit lower than natural gas, but because oil is a global market, the geography of the growth is much less important. As a consequence, I have more confidence in this supporting the price of oil realized by US energy companies. Moreover, the cartel-nature of global production can help to limit supply growth. Given all of these factors, I prefer E&P companies that are focused on oil rather than gas.

{kind=link}

This is why I view SM's oil-centricity as a positive attribute of its production profile. Importantly, this fact and solid drilling results are supporting strong financial performance. Operating costs are running less than $11/boe, supporting solid margins. SM has generated $353 million in free cash flow this year, about 2/3 of that has gone to shareholders and 1/3 to acquisitions. Excluding working capital, it generated $208 million in free cash flow in Q3.

{kind=link}

SM has a stellar balance sheet with $402 million of cash and $1.2 billion of net debt with no maturities until June 2025. As a result, it has just 0.7x net debt to EBITDA. I view below 1x as strong for an E&P company, meaning SM does not need to reduce debt further and can return cash flow to shareholders. It does this via a base dividend and share repurchases. SM is increasing its dividend by 20% to $0.18 beginning in Q1 2024, providing a ~1.8% forward yield. Since announcing its capital return program in September 2022, it has retired 7.7 million shares, returning $335 million to investors, with $73 million of dividends and $262 million in repurchases.

Next year, I expect modest production growth based on guidance for mid-single digit oil production increases. SM also has about 20% of natural gas hedged next year as of 9/30, at about $3.50. It aims to get to 25-30% hedged by year-end. This provides some protection from lower prices. With about $1 billion in sustaining cap-ex needs and roughly flat operating expenses, SM can generate $450-$500 million in 2024 free cash flow at current commodity prices of $75 oil and $2.50 natural gas.

My own calculation

At its current market capitalization, that provides a 10.5% free cash flow yield. SM's cash flow also moves about $18-20 million from each $1 in oil price realizations. So if we return to $85, free cash flow would likely be over $650 million, providing significant upside should commodity prices recover. With a soft landing appearing more likely and the Federal Reserve set to begin lowering rates, I view prices as likely to remain at least around current levels, if not poised for some appreciation as demand proves resilient.

Now, all investments have risks. For SM, I would highlight both macro and company-specific risks. Oil companies do not control the price they sell their product, and if oil prices fell a lot, this would be a negative. For SM, the company can stay free cash flow neutral after its dividend down to about $45-$48 oil aided in part by its 20-25% hedge position. If I am wrong that there is likely to be a soft landing, and we see a recession in the US, or other major economies (like China or Europe), that would push oil demand lower and reduce commodity prices. For investors negative on the economic outlook, I would avoid oil companies as a sector. Additionally, if we saw Saudi Arabia and Russia start to produce more oil, doing an about-face from their current policy of constraining production, that supply would likely reduce prices and be a headwind for the sector. I do believe that SM has set its base dividend to a level that should be safely sustained even during significant downturns.

On company-specific risks, my primary focus for SM will be its cap-ex productivity. As noted above, the company has seen production eclipse guidance, lowering per-barrel costs, thanks to a return to record production from new wells, after a disappointing 2022 result. With increased core acreage position in the Midland Basin, I do expect strong drilling results to continue; however, if we see results slip back to 2022 levels, sustaining cap-ex would likely be closer to $1.15-1.2 billion vs the $1 billion level I estimate. At that level of cap-ex, its free cash flow is only ~$300 million for a 6% free cash flow yield, which would argue for shares being at fair value.

As such, investors should continue to closely watch the interplay between cap-ex guidance and production and new well output. If we begin to see degradation in results, that could argue for less upside than I expect. I believe, given its acreage additions and results this year, this is a manageable risk, but it should be monitored regularly.

A double-digit free cash flow yield in an oil-centric E&P company with a solid balance sheet is attractive in my view given medium-term projections for modest demand growth. With this cash flow, its dividend is safely covered, and SM can retire over 8% of the share count next year or do some further bolt-on M&A to build more scale and find more efficiencies. Given its smaller size, SM may not reach an 8% free cash yield, which I view as appropriate for a firm with its cost base and balance sheet. That would yield a price of $52. While I could justify that price as a fair value, I do not expect that much multiple expansion in the next year. Still, I would expect shares to move to $45-48 if oil prices remain around $75 over the next year for a ~9% capital return yield, with further upside if commodity prices recover. With a 15% total-return potential, SM is an attractive investment for value investors.

For further details see:

SM Energy: Strong Free Cash Flow At An Attractive Valuation