EM - Smart Share Global: May Be A Good Bet On Foot Traffic Normalization

2023-10-05 18:40:42 ET

Summary

- The company's revenue increased by 50% YoY, and operating margin reached 1.3%.

- The lifting of Covid restrictions supports the operational and financial performance of business.

- I believe the company will continue to deliver strong results in the coming quarters.

Introduction

Shares of Smart Share Global ( EM ) have fallen 25% YTD. I believe there is an attractive entry point for investors to go long at the moment. In my article, I would like to analyze current business trends and share my own expectations about future financial and operating results.

Investment Thesis

In my personal opinion, the easing of Covid restrictions in the Chinese market, the recovery of citizen mobility and the increase in the amount of time people spend outside the home provides an excellent opportunity for investors to take a long position in Smart Share Global shares. First, I think the company's revenue will continue to show strong growth rates due to the recovery in mobility and the relatively low base of comparison last year. Secondly, I believe that increasing economies of scale and increasing the share of POI ((points of interest)) under the network partner model will contribute to the growth of operating profitability of the business. In addition, quotes have dropped significantly, and the company's shares are still relatively inexpensive in accordance with the multiples. I believe the financial results for the coming quarters could be a catalyst/driver for the stock.

Company Overview

Smart Share Global company provides mobile device charging services, and also sells and rents power banks. The main revenue segments are direct revenue (29% of revenue) and network partner model (71% of revenue). At the end of the 2nd quarter of 2023, the company manages 1,109 POI (points of interests), about 62% of the total number of POI under the network model. The company was founded in 2017 and operates in the Chinese market.

2Q 2023 Earnings Review

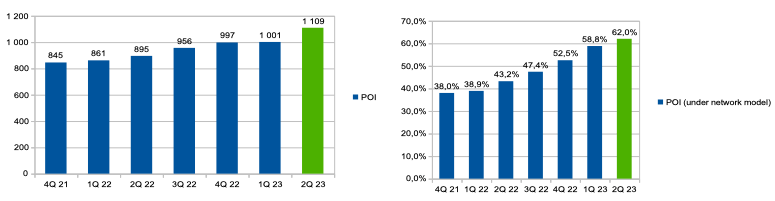

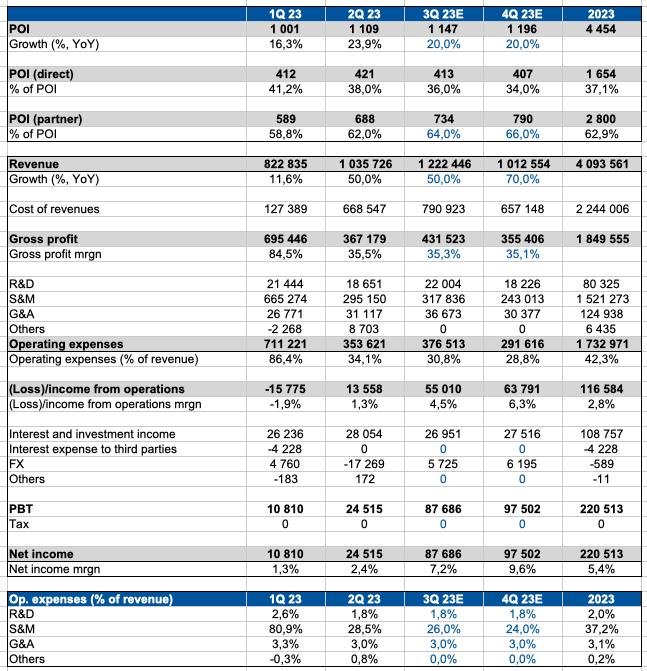

The company's revenue increased by 50% YoY . The largest contribution to revenue growth was made by the mobile device charging segment, where revenue increased by 49.6% YoY, and in the others segment sales increased by 107.8% YoY. The number of POIs ((points of interests)) increased by 23.9% YoY and reached 1,109, and the number of registered users increased by 16.7% YoY and reached 362.5 million.

POI and POI under network model (Company's information)

{kind=link}

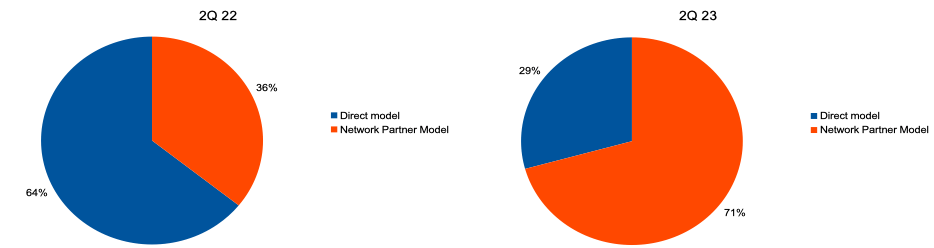

It should be separately noted that the share of POIs under the network partner model continued to increase and reached 62% of the total number of POIs. Thus, the share of direct revenue decreased from 64% in the 2nd quarter of 2022 to 29% in the 2nd quarter of 2023, and the share of revenue in the network partner model segment increased from 36% in the 2nd quarter of 2022 to 71% in the 2nd quarter of 2023. You can see the details in the graph below.

Revenue by channel (Company's information)

{kind=link}

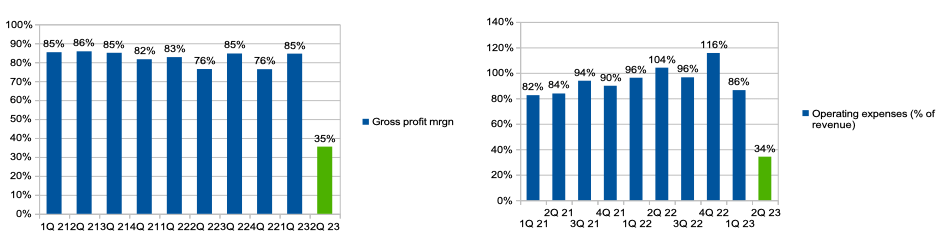

Gross profit margin decreased from 76.4% in Q2 2022 to 35.5% in Q2 2023. Operating expenses (% of revenue) decreased from 104.1% in Q2 2022 to 34.1% in Q2 2023. The largest contribution to the reduction in operating expenses (% of revenue) was made by sales & marketing expenses, which decreased from 96.3% to 28.5%.

Gross profit margin & SGA (% of revenue) (Company's information)

{kind=link}

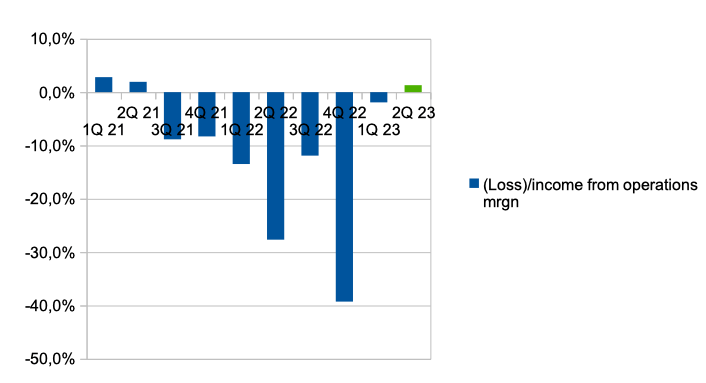

Thus, the company demonstrated a positive operating margin of 1.3%, while in the 2nd quarter of 2022 the operating loss (% of revenue) was 27.7%.

Operating income (loss) margin (Company's information)

{kind=link}

My Expectations and Forecast

In my personal opinion, the company will continue to show both solid revenue growth and improved operating margins in the coming quarters. Firstly, the company is a direct beneficiary of the lifting of Covid restrictions in China, since the recovery of traffic on the streets can provide significant support to the growth rate of business revenue.

Secondly, I expect that the operating profitability of the business will continue to improve due to: 1) management's desire to focus on increasing the number of POIs under the network model 2) the recovery of economies of scale and network effects. Despite the fact that a decrease in own POI leads to a decrease in gross profit margin, development through the partnership model allows you to accelerate the rate of business growth, continue to increase market share, reduce fixed costs and lead to an improvement in unit economics. Thus, the company was able to demonstrate positive operating profit for the first time in the previous 8th quarter. Separately, I would like to note management's expectations during the Earnings Call after the publication of financial results.

I think it's also important to note that we are very optimistic on the recovery of overall foot traffic and consumption in China. The sequential recovery is very clear. For us, we will continue focusing on doing the right thing, which is to efficiently expand the coverage of our service through the direct and network partner models

For a more detailed understanding, I would like to share my own forecasts, which are based on my own expectations, historical values ??and comments from the company's management. Thus, I conservatively believe that the company will continue to demonstrate revenue growth rates of about 50% and 70% in 3Q and 4Q 2023, respectively, thanks to the recovery in traffic in China and a stable pace of opening new POIs.

I believe the company will continue to increase the number of POIs under the network partner model, so I think the gross margin level will continue to decline slightly to 35.1% by Q4 2023. In addition, I forecast that sales & marketing expenses (% of revenue) will continue to decline to 24% by Q4 due to the recovery in business scale and network effect.

{kind=link}

Drivers

Revenue: the recovery of offline traffic in China due to the lifting of Covid restrictions may contribute to both an increase in revenue growth and the possibility of accelerating the pace of opening new POIs.

Margin: an increase in the business scale effect, an increase in the network effect and an increase in the share of POI under the network model can have a positive impact on the level of operating profitability of the business in the next quarters.

Risks

COVID: the return of COVID restrictions could have a significant negative impact on both revenue growth and profitability due to reduced traffic and economies of scale.

Competition: increased competition can lead to both a decrease in market share and a decrease in profitability due to the need for additional investments in prices for own services, increased commissions for partners and increased marketing costs.

Valuation

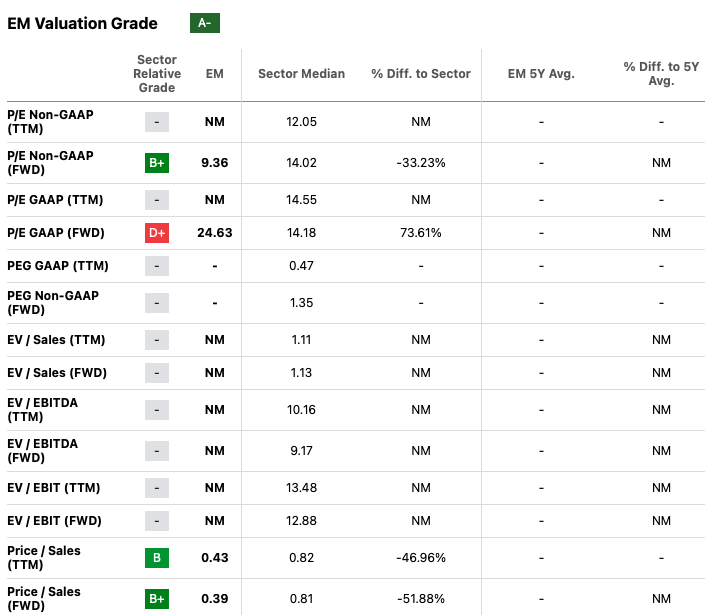

Valuation Grade is A-. In accordance with the FWD P/E and FWD P/S multiples, the company is trading at 9.4x and 0.4x, which implies a discount to the sector median of about 33% and 52%, respectively. I believe that the current valuation level looks attractive, both in view of the relatively low multiples and the high revenue growth rates that the company can continue to demonstrate, in my personal opinion, in the coming quarters. I believe further recovery in offline traffic and improving operating margins could be catalysts for the stock's growth through the end of 2023.

{kind=link}

I prefer to value a company based on a multiple because valuation using the DCF model is too sensitive to inputs, especially for high-growth companies. So, I use my own net profit forecast and P/E multiple at 10.0x, which is still lower than the sector median. Thus, the fair price of shares is about $1.4 with an upside potential of 82%.

Valuation (Personal calculations)

Conclusion

Thus, at the moment, my recommendation is buy. I think the company will continue to deliver strong financial and operating results in the coming quarters, which could serve as a catalyst for growth in the stock. In addition, I believe the downside potential is limited given the stock's relatively low valuation based on multiples.

For further details see:

Smart Share Global: May Be A Good Bet On Foot Traffic Normalization