CWYUF - SmartCentres: A Look At The Dividend Safety

Summary

- The Q3-2022 results had this REIT firing on all cylinders.

- We were impressed too and we had actually passed on it in 2021.

- Our outlook remains less than rosy and we talk about it in this article.

All values are in CAD unless noted otherwise.

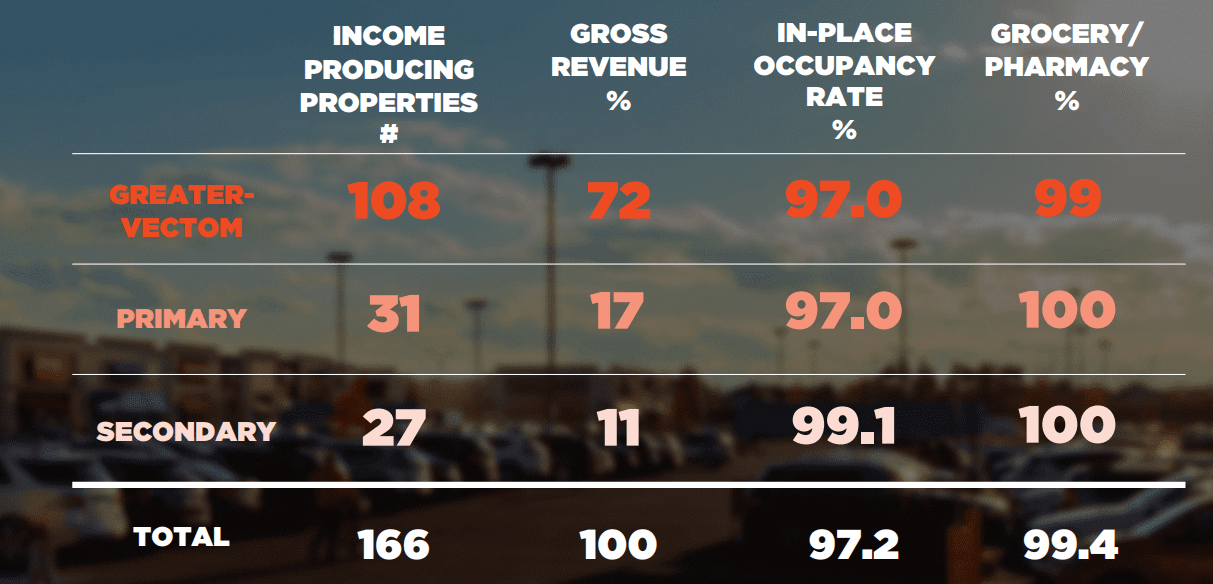

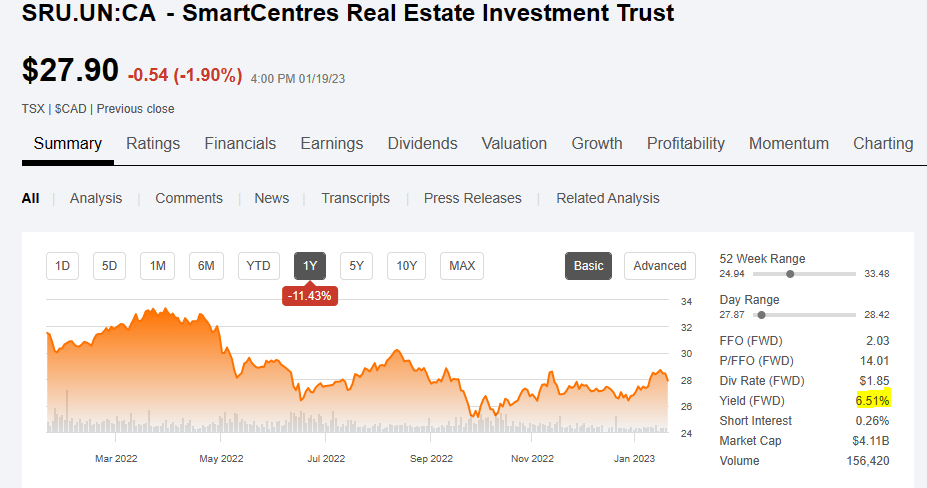

SmartCentres Real Estate Investment Trust (CWYUF) ( SRU.UN:CA ) has 166 income producing properties spanning 34 million square feet enjoying an overall occupancy rate 97.6%.

{kind=link}

Note: VECTOM stands for Vancouver, Edmonton, Calgary, Toronto, Ottawa and Montreal.

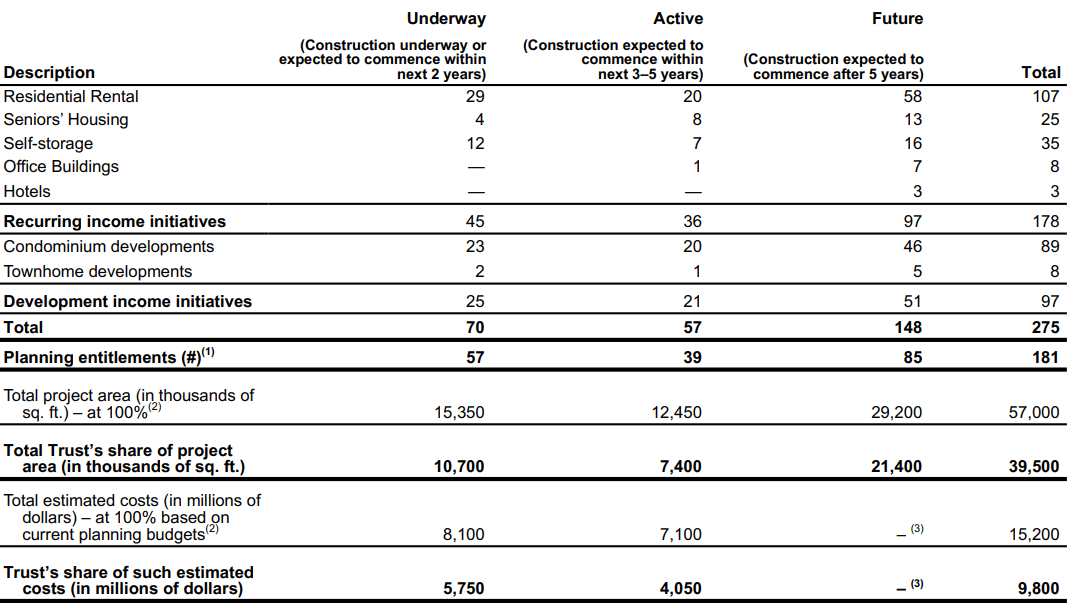

These are predominantly Walmart-anchored ( WMT ) (or shadow-anchored), open format retail shopping centres. The REIT also has 19 properties under development. For the last few years, SmartCentres has had a fever and the only cure has been developing its existing retail centres to become mixed use properties. Their mantra has been "from shopping centres to city centres" while adding residential, office and self storage buildings as extensions to their retail centres. At September 30, 2022, their development pipeline looked like this.

{kind=link}

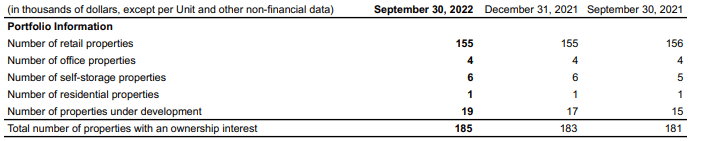

SmartCentres has started reaping some of the benefits of this as they have begun earning rental income from non retail properties, along with some development income from the sale of condominiums and townhomes. At September 30, 2022, their income producing portfolio looked like this.

{kind=link}

They are still primarily a retail REIT with mixed use and office still making up a very small percentage of the total income. At present, only 0.9 million square feet of the total 35.2 million square feet of GLA is dedicated to office, self storage or apartments. The REIT has done decently since our coverage on it back in February 2021. It did very well in 2021, and while 2022 took some of the gains away, it is still well in the positive territory for its investors that stepped in back then.

While we did not find anything glaringly untoward about it, we rated it a hold due to the CAPEX requirements to fund its ongoing transition from a retail to a mixed use entity. We said as much in the conclusion to that piece.

The mixed use properties have huge potential down the line for NAV gains and further improving value of the retail properties in those locations. But they do require lots and lots of capex and progress will be slow. This is likely one of the better REITs for retail exposure as the future Residential properties provide some additional buffer. It trades at close to 12X FFO for 2021, and while that may be cheap from a general market standpoint, it is fair considering the distress in retail. We would not go crazy on it over here and rate it as neutral.

Source: SmartCentres: Getting To Know This Retail REIT

Coming up next is an update to our prior thesis, which is long overdue.

Q3-2022

The most recent results continued to show strength for this retail REIT. In-Occupancy moved up 0.4% over Q2-2022 and is now at 97.6%. Committed occupancy which includes leases yet to commence, moved up 0.5% and cleared the 98% mark. Net operating income ((NOI)), growth was modest, and same property NOI came in at 2.3% (before expected credit losses). While 2.3% is low in the REIT universe, SmartCentres has historically averaged about 1% a year of same property NOI growth. So by that measure it is firing on all cylinders. Renewal rents were up about 2.7% during the quarter.

Interestingly, despite all those positives, funds from operations ((FFO)) was lower year over year by $10.5 million.

Q3-2022 MD&A

After adjustments, both FFO and ACFO were about the same as last year. Unfortunately, thanks to the dilution via new units, the per unit amounts were about 3% lower.

Outlook

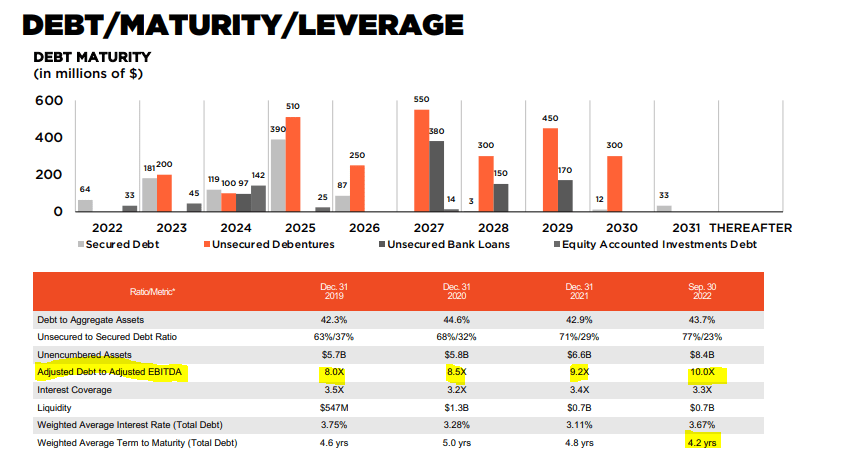

As solid as the quarter was, SmartCentres faces several headwinds in its attempt to create value per unit. The first and most glaringly obvious is its massive developmental undertaking which requires huge amounts of cash flow and equity issuance. Since the company pays out almost all of its FFO in the form of distributions, we still have rising debt, despite equity issuance.

{kind=link}

Debt to EBITDA was at 10.0X as of September 30, 2022. Interest expense was up about 10% year over year. Some of that came from rising rates and some from the higher debt load. As we look at estimates for 2023, interest expenses should be between 16% and 20% higher than the same for 2022. When we combine that with the increased unit counts, we are looking at a possibly an 8-10% contraction in AFFO per share. That is a problem. That is even more of a problem if you run the math on the payout ratio which should be closing in on 110%. Yes, a lot of this is tied to developments and SmartCentres has historically been able to book good gains on asset sales from developments. Whether it can do so in the midst of a recession remains to be seen. Whether it can hold the line of the distribution with a 10X debt to EBITDA and a 110% payout ratio, again, remains to be seen. With a weighted average debt maturity term of 4.2 years, we could see some more aggressive resets on interest rates as we move into 2024. Analysts are who generally an optimistic bunch, see no problems with NOI rising nicely in the middle of a recession. But even they cannot get around to predicting growth in AFFO per share. Most estimates we see are calling for a contraction in 2023 and 2024.

Verdict

Just as we discussed with Allied, we think SmartCentres needs to deleverage. Ideally we would like to see a sub 8.0X debt to EBITDA to get interested. The big attraction for the retail investor is of course the big distribution.

{kind=link}

While we remain agnostic on the possibility of a cut in 2023, you have to know that the risks are rising here. There are other retail REITs with similar yields and no risk from the development pipeline.

Some investors might be interested here for the discount to Net Asset Value or NAV. On a standalone basis, you could make the argument that there is some upside there. We don't believe so and that logic comes from two reasons. The first being that all forms of retail exposure are cheap today. RioCan Real Estate Investment Trust ( REI.UN:CA ) is about as discounted as SmartCentres. H&R Real Estate Investment Trust ( HR.UN:CA ) is even more discounted.

Yes, H&R has some exposure to office, but it also has a huge exposure to industrial and residential, two asset classes that are functioning better compared to retail. The second aspect here is whether there is actually a realistic discount. With 10X debt to EBITDA, small movements in cap rate assumptions can make a big move in NAV. So the NAV discount in relation to SmartCentres' IFRS book value, while helpful, is hardly a reason to get involved with SmartCentres.

Finally, SmartCentres is trading at a 16X AFFO multiple with declining AFFO. That multiple is 2X ahead of RioCan and 4X ahead of H&R. We don't believe that represents any possible upside. Our fair value here is to look for a 14X multiple on 2023 AFFO which gets us to $24.00 per share. Including the dividends, the total return outcome from here is about negative 2% over the next 12 months. That gets us to a "hold" rating.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

SmartCentres: A Look At The Dividend Safety