CWYUF - SmartCentres: Current Distributions May Remain But Higher Prices Are Not Likely

2023-06-26 11:27:52 ET

Summary

- SmartCentres' 1-year forward dividend yield of 7.8% may be attractive, but the stock's price may not increase in the next six months due to rising interest rates and worsening financial results and debt position.

- The Trust's projects and developments may help it maintain its monthly distributions despite challenges from higher interest rates.

- One significant risk for SmartCentres is the potential difficulty in renewing contracts with non-anchor tenants, which account for about 40% of its total annualized gross rental revenue.

Investment thesis

With a one-year forward distribution yield of 7.8%, SmartCentres (SRU.UN:CA) (CWYUF) price decreased by about 20% in the past 5 months. One might argue that with this distribution yield, and after a 20% price drop, it might be a good time to buy SmartCentres. But I don’t think so!

According to its 1Q 2023 report , the Trust’s 1Q 2023 AFFO with adjustments and cash flow from operating activities were weaker than in 1Q 2022 and 4Q 2022. Despite that, SmartCentres’ monthly distribution didn’t decrease in the past year. However, it is important to know that the Trust's payout ratio to AFFO and payout ratio to ACFO impaired in the first quarter of 2023, implying that to maintain the monthly distribution of $0.1542 per unit, the Trust’s Board of Directors may face some challenges in the second half of the year. Higher interest rates in the past year have hurt SmartCentres' interest coverage ratio and its debt ratios, and with higher interest rates, the Trust’s results may impair further in 2H 2023. It is important to know that on 21 June 2023, to combat inflation, the Bank of Canada increased its key interest rate again by a quarter of a percentage point to 4.75%, the highest since 2001.

Be mindful that I am not saying that SmartCentres’ monthly distribution is likely to decrease in the following months. However, due to the Trust’s current financial position and the current economic condition, the stock’s price may not start increasing even after its recent drop, at least by the end of the year. Thus, if SmartCentres’ current distribution yield is consistent with your investment strategy, it might be an option. However, if you want to buy the stock at $23, receive its monthly distribution for about 1 year, and sell it at significantly higher prices, based on the current financial and market conditions, it may not be likely. Take into account that the stock’s price in the next six months may even decrease further and offset all the rewards from the distributions. Based on these explanations, I put a hold rating on SmartCentres. However, I also should mention the Trust’s projects and developments, that can make its Board of Directors able to maintain the Trust’s current monthly distribution, even with higher interest rates, and also may help the Trust’s financial results to start improving one year from now.

Results and developments

In the first quarter of 2023, SmartCentres reported FFO and AFFO of $97 million (up 5.4% YoY) and $89 million (up 3.4% YoY), respectively. However, it is important to know the Trust’s FFO and AFFO in the fourth quarter of 2022 were significantly higher than in the first quarter of 2023. SmartCentres’ FFO per diluted unit increased from $0.51 in 1Q 2022 to $0.57 in 4Q 2022 and decreased to $0.54 in 1Q 2023. Also, the Trust’s AFFO per diluted unit increased from $0.50 in 1Q 2022 to $0.58 in 4Q 2022, then decreased to $0.51 in 1Q 2023. The Trust’s Board of Directors has been declaring a monthly distribution per unit of $0.15417 for the past 45 months . The Trust’s payout ratio to ACFO (adjusted cash flow provided by operating activities) decreased from 96.7% in 1Q 2022 to 88.6% in 4Q 2022 and increased again to 96.3% in 1Q 2023. Also, the Trust’s payout ratio to AFFO with adjustments decreased from 97.9% in 1Q 2022 to 93.9% in 4Q 2022 and increased again to 99.9% in 1Q 2023, the highest during the past 8 quarters. The Trust’s payout ratio to ACFO and payout ratio to AFFO in the second quarter, third quarter, and fourth quarter of 2023 may not be better than in the first quarter and even may worsen, as interest rates are still increasing and the market condition can get more unfavorable.

SmartCentres’ weighted average interest rate increased from 3.09% in 1Q 2022 to 3.86% in 4Q 2022 and increased further to 3.89% in 1Q 2023. Also, its weighted average term of debt decreased from 4.7 years in 1Q 2022 to 4.0 years in 4Q 2022 and decreased further to 3.9 years in 1Q 2023. SmartCentres’ interest coverage ratio (defined as adjusted EBITDA divided by adjusted interest expense including capitalized interest) decreased from 3.5x in 1Q 2022 to 3.1x in 4Q 2022 and decreased further to 2.9x in 1Q 2023. Thus, compared to a year ago, SmartCentres is now in a more rigid condition to pay its debt.

However, its projects and developments can help the Trust to overcome the current challenges, and remain profitable and solvent. As SmartCentres’ self-storage properties increased from 6 in 2022 to 8 in 2023 (as of 31 March 2023), and its properties under development increased from 19 in 2022 to 20 in 2023 (as of 31 March 2023), the Trust’s total number of properties with an ownership interest increased from 185 in 2022 to 188 in 2023 (as of 31 March 2023).

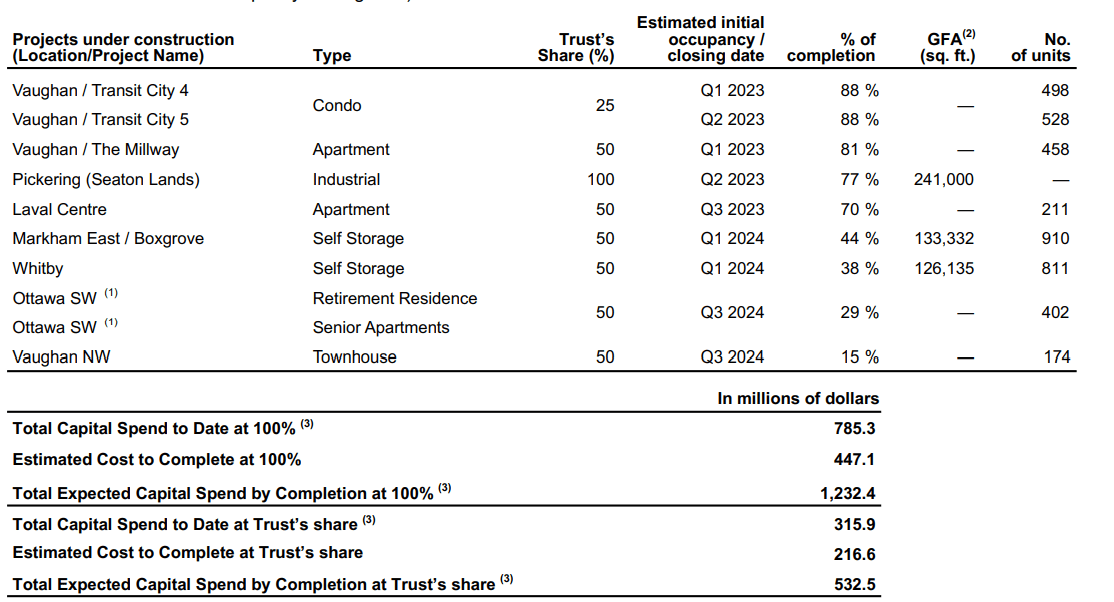

According to Figure 1, SmartCentres has 10 projects under construction, with Trust’s share of between 25% to 100%. The completion rates of five of these projects are more than 70%, and the Trust expects the initial occupancy/closing date for these 5 projects to be at most in 3Q 2023. Also, the estimated cost to complete these 10 projects is $447.1 million (36.3% of the total expected capital spend by completion at 100%), of which $216.6 million (48.4%) is the Trust’s share.

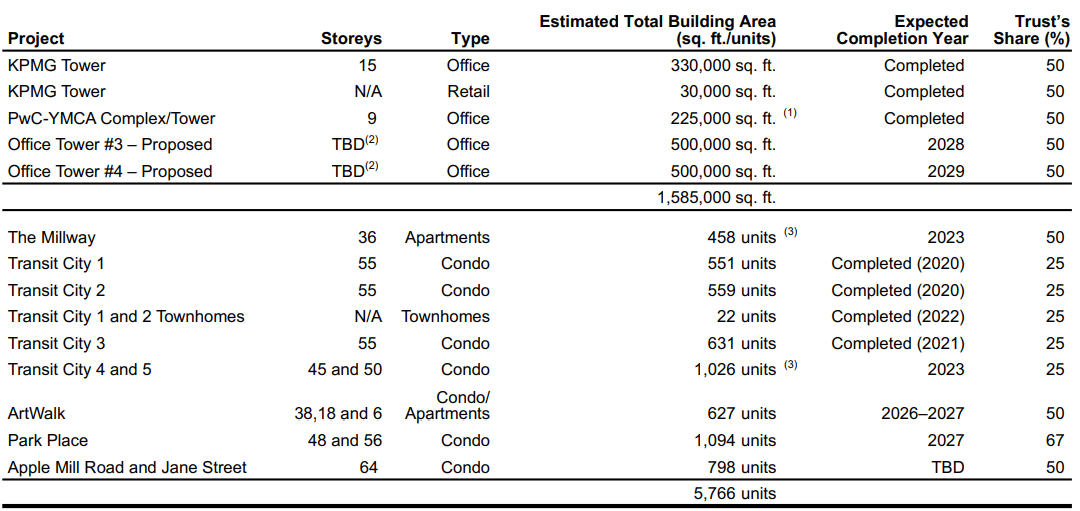

At SmartVMC, the Millway project (a 36 storeys apartment with 458 units) is expected to be completed by the end of 2023 (see Figure 2), and SmartCentres has a 50% share in this project (in December 2021, the Trust acquired a two-third interest in SmartVMC). In addition to the Trust’s development initiatives that are under construction, during the past two years, 7 projects (including 6 self-storage facilities and one residential rental) have been completed, and SmartCentres have a 50% share in all of them.

Figure 1 – Trust’s 10 development initiatives

{kind=link}

1Q 2023 report

Figure 2 – SmartVMC development initiatives

{kind=link}

1Q 2023 report

In the first quarter of 2023, 194 units of 498 units (39%) at Transit City 4 closed. However, there was no closing at Transit City 5 closed. In the first quarter of 2023, 19% of the units at Transit City 4 and 5 closed, and 81% of the units (832 units) were not closed. Based on the 25% share of SmartCentres in Transit City 4 and 5, the Trust’s FFO from the closings of Transit City 4 in the first quarter of 2023 was $3.8 million, or $0.02 per diluted unit. Thus, the Trust’s FFO from the closings of the rest of the units can bring an FFO of $16.2 million, or 0.09 per diluted unit.

One of the biggest risks

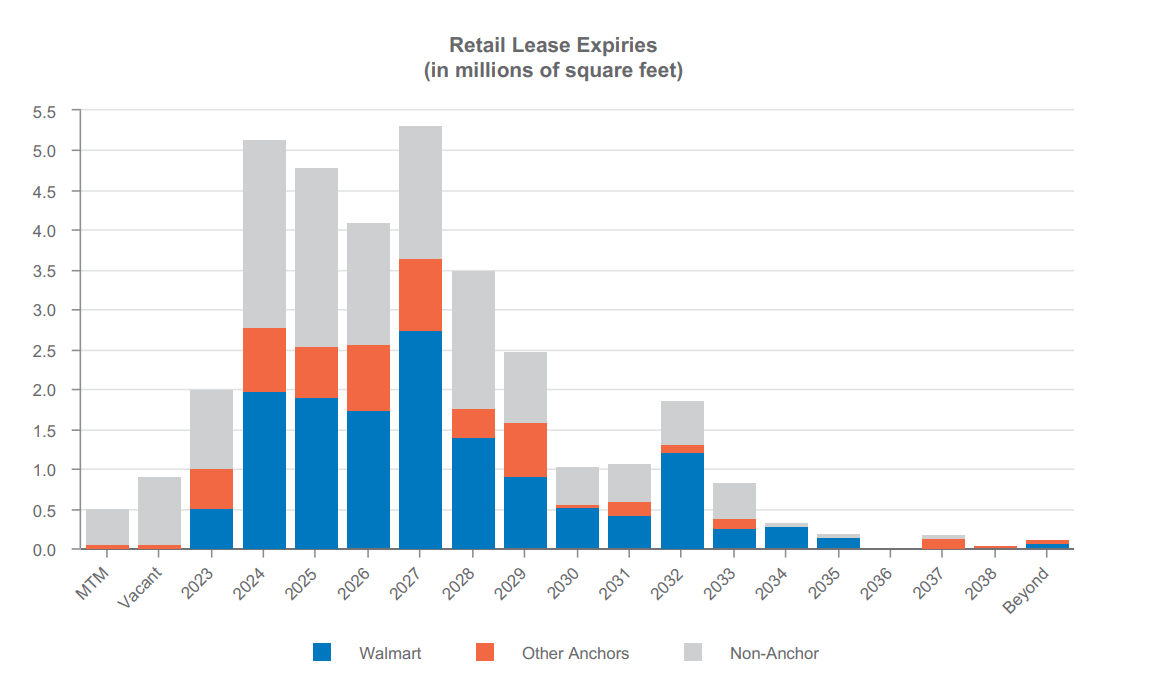

The Trust’s 25 largest tenants (by annualized gross rental revenue) accounted for 60.8% of its portfolio revenue as of 31 March 2023. With 100 stores, annualized gross rental revenue of $197 million (24.3% of total annualized gross rental revenue), Walmart is the Trust’s biggest tenant.

“Walmart is a very strong anchor tenant in good times, and an even stronger one in tough times. Hence, customer traffic to our Walmart-anchored shopping centre portfolio continues to gain momentum which, in turn, is generating steadily increasing levels of leasing activity that began earlier in 2022,” the CEO said .

As the Trust’s revenue from Walmart and other anchor tenants is considerable, one might argue that SmartCentres may not face serious problems in renewing its leases when they expire. However, the Trust’s revenue from non-anchor tenants accounts for about 40% of its total annualized gross rental revenue (28% of its total gross leasable area). According to Figure 3, a significant portion of the Trust’s retail lease which expires in 2023 and the subsequent years, is linked to non-anchor tenants. Thus, based on the current market condition, which is linked to high interest rates and financial tightness, the Trust cannot be sure that it can renew its contracts with its non-anchor tenants as they expire.

Figure 3 – SmartCentres’ retail lease expire (in millions of square feet)

{kind=link}

1Q 2023 report

End note

SmartCentres has a 1-year forward distribution yield of 7.8%, which might be consistent with the investment strategy of some investors. Also, the Trust’s projects and developments imply that the Trust may be able to pay its monthly distributions, despite its payout ratio to AFFO and payout ratio to ACFO impaired in the past year. However, even after the recent drop in its stock price, and even with its current distribution yield, the stock’s price may not increase in the next six months, as interest rates can increase further, and the Trust’s financial results and debt position may get worse. The stock is a hold.

For further details see:

SmartCentres: Current Distributions May Remain, But Higher Prices Are Not Likely