CWYUF - SmartCentres: Solid 8% Yield But AFFO Payout Could Breach 100% Soon

2023-11-20 10:00:00 ET

Summary

- SmartCentres REIT had a good Q3-2023, with high occupancy levels and strong rent uplifts.

- The company's debt load and interest expenses are increasing, impacting key metrics like AFFO payout ratio.

- We give you our buy point for this REIT and tell you why we are still going with a hold rating.

Note: All amounts discussed are in Canadian Dollars

When we last covered SmartCentres REIT ( SRU.UN:CA ), we gave it a pass while noting that the valuation was coming in-line for a more constructive outlook. For the impatient, we suggested an alternative method to get involved, that would reduce risk and give them a better return profile. Specifically we said,

We are not ready to give this a straight buy rating yet, but think that investors can consider doing some covered calls to create a buffer and additional income. You could easily get a 12-14% annualized yield from the call premium and the dividends. So that method today would make a more acceptable risk-reward versus buying at $30.00 direct in January 2023. We think if we see $21-$22 or a reduction in debt levels, we might be interested. As it stands, we like the low capex REITs for our retail exposure.

Source: Seeking Alpha

How did that turn out? Well not too bad on all fronts. The stock did not deliver positive returns since then, even if you count the distributions. So you lost nothing by staying out. But it did find a bottom in our suggested range of $21-$22.

We look at the current results and tell you how we see this evolving.

Q3-2023

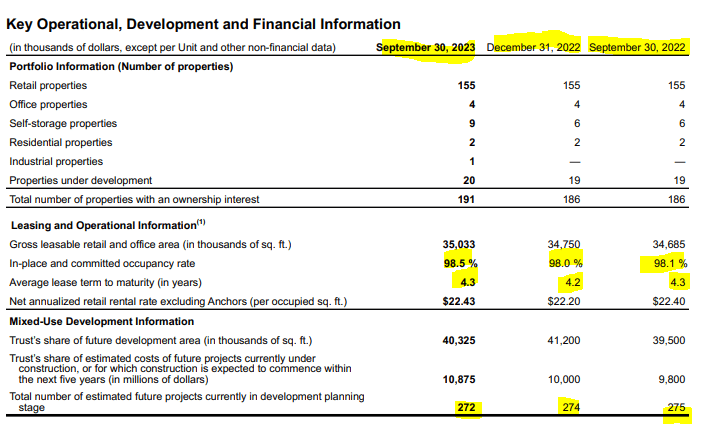

Q3--2023 was a good quarter with funds from operations (FFO) (excluding gains from asset sales), beating the street consensus of 47 cents a share. What was possibly not being modeled here was the additional increase in occupancy levels to 98.3%.

{kind=link}

This is the highest level of occupancy for this REIT and the tightness in the market is also leading to strong rent uplifts. As the slide above shows, the weighted average lease term is also small, so in a strong market, SmartCentres remains positioned to that advantage of rent increases.

While those were good numbers, we want to stress here that all of these developments are not having any impact on the key metrics. Here, by key metrics we do not mean net operating income (NOI) which powered ahead by 10% versus last year.

SmartCentres Q3-2023 Results

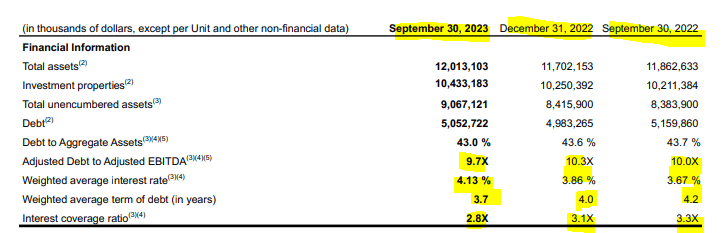

We are referring to the AFFO payout ratio which actually increased year over year, despite the distribution remaining the same. That reason for that increase can be gleaned in the very next picture.

{kind=link}

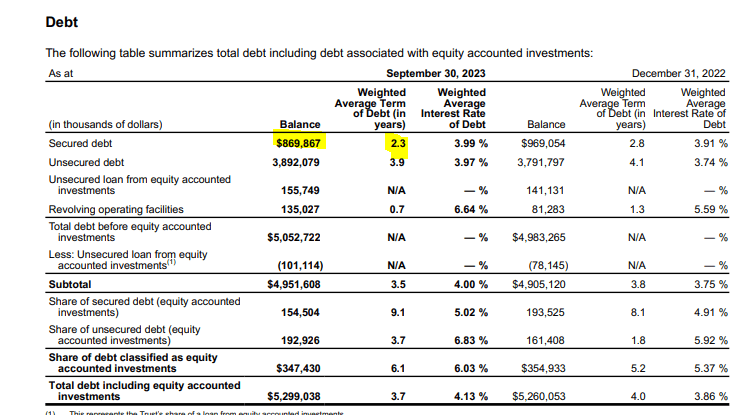

Total debt while down slightly year over year (up from December 2022 though), is costing the company 27 basis points more in interest expense. We are still flirting with a 10X debt to EBITDA number. More worrisome for investors is the fact that the weighted average debt maturity has moved to 3.7 years from 4.2 years 12 months back. Secured debt has just a 2.3 year weighted average term to maturity.

{kind=link}

There have been few good refinancing opportunities since the bottom in interest rates in 2021 and the stresses are showing in AFFO and the interest coverage ratio. Conservatively, we think new debt can be financed at over 6% in the next 12-24 months. On the maturity side, we have mainly secured debt coming due in 2024 and then big tranches of both secured and unsecured debt in 2025. Key point though is the interest rate on all of this in the mid 3's. Refinancing won't be pleasant.

Outlook

We all know that Canada is short on key properties on both residential and retail side. That burden has been increased with the unmitigated disaster of the immigration policy in place . So if you look at the commentary on the development side and the sales related to that, it looks pretty good.

Occupancy and condo closings for Transit City 4 and 5 continued with an additional 274 units closed during the third quarter generating $6.9 million of FFO(1) . The remaining 106 units are expected to take place in Q4 2023.

The Millway, a 458 rental unit apartments project is nearing completion. Leasing continues to benefit from strong demand and is ahead of budget. As of the end of the quarter, 67% of the 331 completed units were leased. The remaining units are expected to be completed and ready for lease by the end of 2023.

Siteworks at ArtWalk condominium Phase 1 commenced in September 2023, with all 320 released units sold out and the remaining units expected to be released for sale in Q4 2023.

The second phase of the purpose-built residential rental project in Laval, comprising 211 units, opened on July 1, 2023, and reached 82% occupancy at the end of Q3 2023. Occupancy for the first phase has reached 99%.

Source: SmartCentres Q3-2023 Results

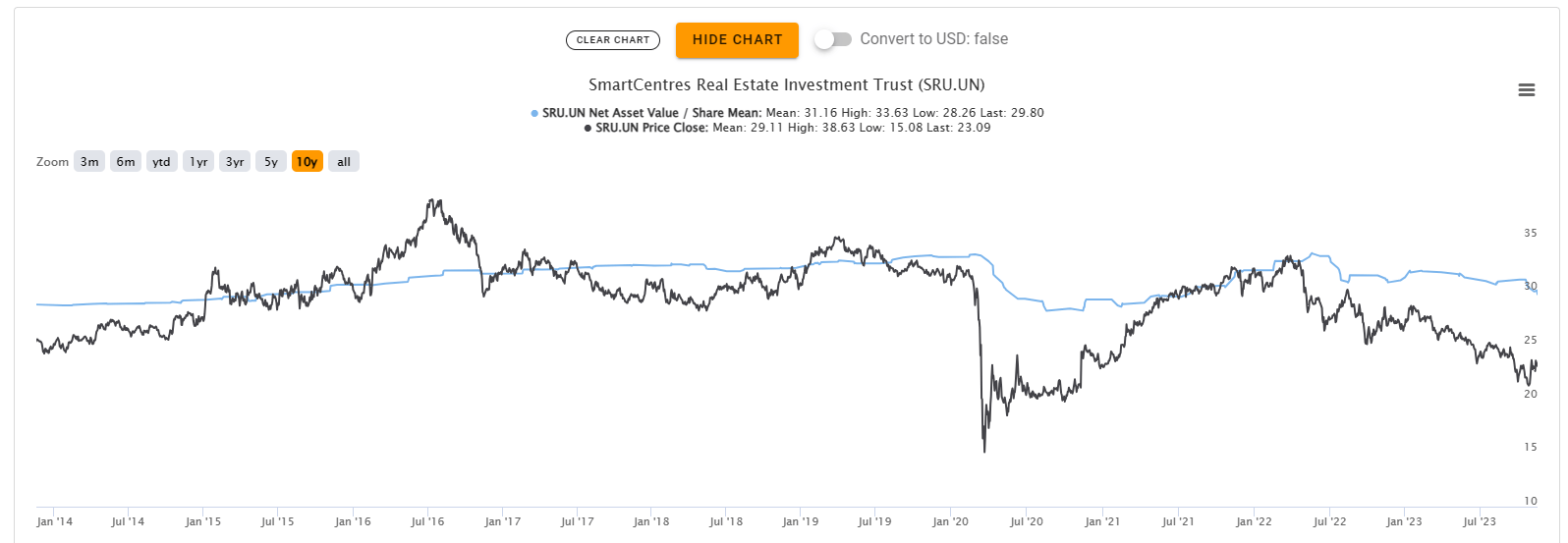

As impressive as all of that sounds, SmartCentres has not been able to make dent in its debt load and its AFFO and AFFO payout ratios are all headed in the wrong direction. Consensus estimates, which never ever forecast a recession, let alone a big one, are forecasting a decline in AFFO in 2024 and a further one in 2025. This will be led by rising interest costs. So the most optimistic bunch think that AFFO will fall in 2024 and 2025. Through this all, your solace has to be that this is trading a good deal below consensus NAV and at close to a 7.7% implied cap rate.

{kind=link}

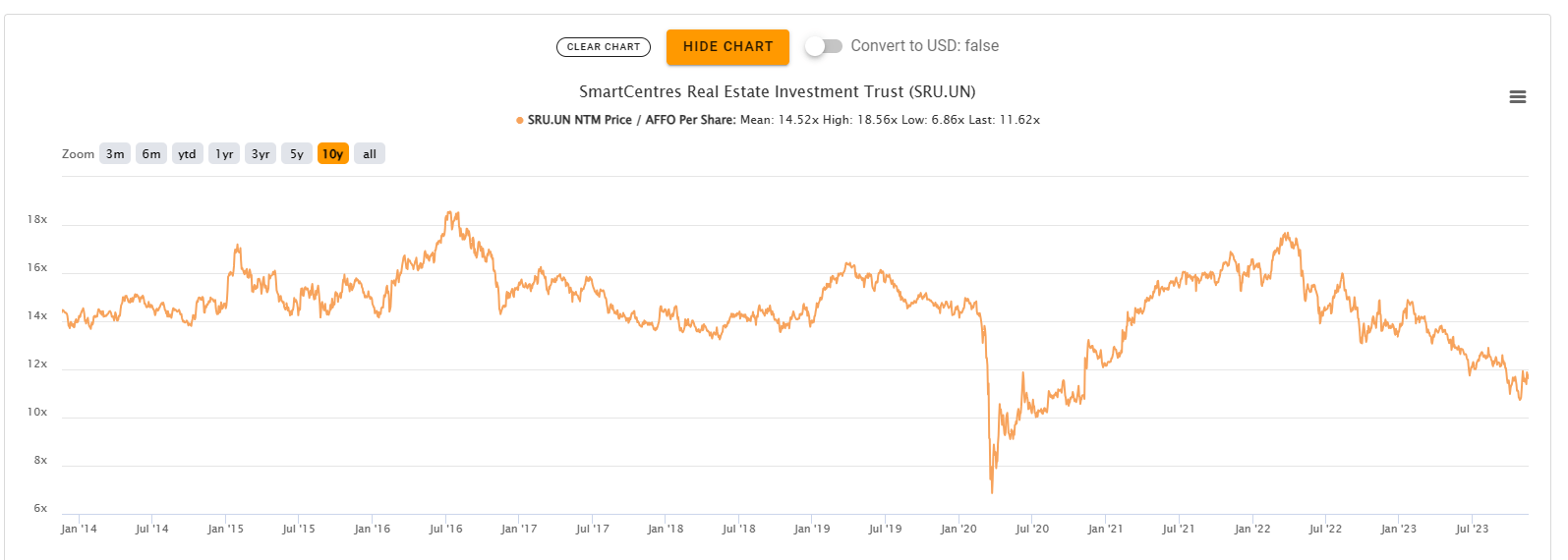

The FFO/AFFO multiples are also at their historical lows, but they can go lower in a recession.

{kind=link}

It is hard not to see the overall value in the portfolio and at the same time it is hard to be very positive with the model in place. Bears have a huge carry cost here and that is the large distribution, which still looks covered in 2024. Even if we breach 100% on the AFFO payout ratio, we doubt there will be a cut in the next 12 months. So based on the positives, you still won't us find us taking a Sell rating. But unless there is a marked change in the model and the debt carried, we won't give this a Buy. We cannot get excited about a REIT carrying a 10X debt to EBITDA unless our implied cap rates jumped at least 1.5% over where we think the market is. That would get us around $21.00 today and that is the minimum we require for a Buy.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

SmartCentres: Solid 8% Yield, But AFFO Payout Could Breach 100% Soon