CWYUF - SmartCentres: Yield Jumps To 7.7% And Outlook Improves

2023-09-08 03:37:12 ET

Summary

- SmartCentres has reached the target price mentioned in early 2023.

- RioCan and H&R have outperformed SmartCentres, validating our previous stance.

- The valuation is a bit more compelling today for SmartCentres, and we tell you how we would play it.

On our last coverage of SmartCentres REIT ( SRU.UN:CA ) we took the stance that investors were unlikely to see good returns, despite the high yield. We were looking for a 14X forward multiple to play out and leave investors trailing money market returns.

Finally, SmartCentres is trading at a 16X AFFO multiple with declining AFFO. That multiple is 2X ahead of RioCan REIT ( REI.UN:CA ) and 4X ahead of H&R REIT ( HR.UN:CA ). We don't believe that represents any possible upside. Our fair value here is to look for a 14X multiple on 2023 AFFO which gets us to $24.00 per share .

Source: A Look At The Dividend Safety

That was in early 2023 and since then the stock has acknowledged the risks and gone straight to our target price, trading as low as $23.24 a few days back. Our relative performance also paid off, with both RioCan and H&R outpacing SmartCentres.

We update our thesis today, taking into account the recent results and the macro environment.

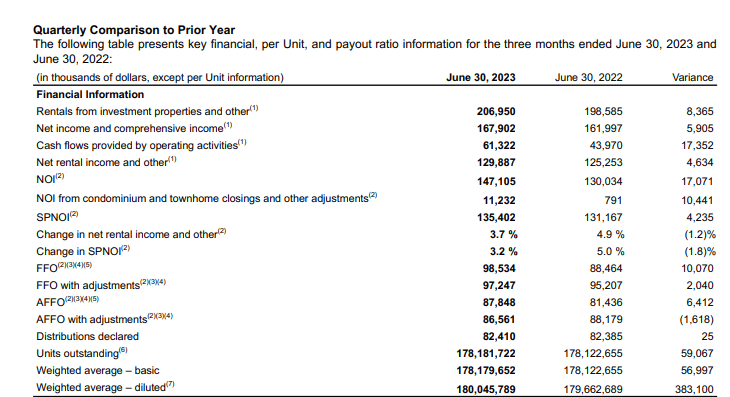

Q2-2023

SmartCentres has an extremely strong second quarter marked by strong rental growth and over $11 million in net operating income from condo and townhome sales. Same property NOI was up about 3.2% and occupancy was at 98.2%.

SmartCentres Q2-2023 Financials

{kind=link}

Despite the jump in interest expense, funds from operations (FFO) and adjusted FFO (AFFO), both were higher. The AFFO payout ratio stayed high as the company continued its commitment to the large distribution.

SmartCentres Q2-2023 Financials

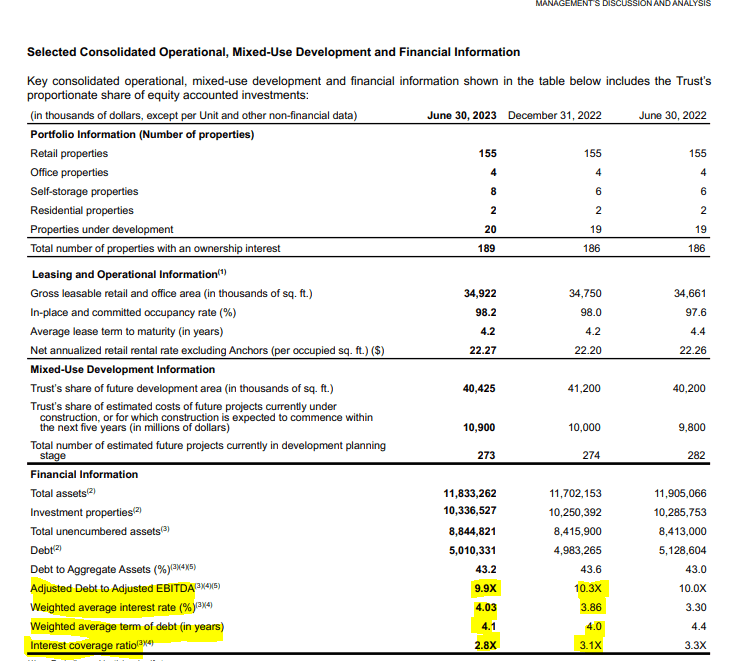

The REIT's NOI has generally outpaced our expectations. This has been driven by extremely strong population growth in Canada (high levels of immigration) and a limited supply of new properties. While the interest rate hikes have slowed the housing market, the broader economy has still proven resilient to these central bank measures. We are seeing the company continue to derive high percentage rent income (the portion tied to tenant sales).

On the other end, the company has a large capex plan in place to develop and intensify several properties. That along with the big distribution keeps the relative levels of debt on the high side. Total debt as shown below was up since December 2022. Debt to adjusted EBITDA is still flirting with that 10.0X mark. A couple of bright spots here include the fact that the weighted average debt term continues to be comfortable at 4.1 years and interest coverage is still on the healthy side at 2.8X.

SmartCentres Q2-2023 Financials

{kind=link}

On that front, the financing markets continue to be wide open for the company. During the quarter, the REIT issued $300 million of notes at 5.354%. This was partly a replacement for the $200 million of maturities during the quarter.

Outlook

Despite interest rates stabilizing and NOI outperforming expectations, we don't see FFO or AFFO exceeding 2021 levels in either 2024 or 2025. This comes from the base effects of a very low interest rate on debt which will keep resetting higher. As of last quarter SmartCentres is paying about 4% on its weighted cost of debt and as seen earlier in this article, this will likely move to over 5.0% over time. So you won't grow from an increasing AFFO. You will most certainly not get any distribution increases in the near future either. The best hope of price appreciation is from a valuation expansion.

The REIT is trading at about 13.5X AFFO for 2024. That is perhaps a tad on the low side but our gripe remains with that 10X debt to EBITDA. That argues for a low multiple. So you might get at 14.0X or even 15.0X but that is the best case. On the downside, in a recession, you could see a 11.0X-12.0X easily.

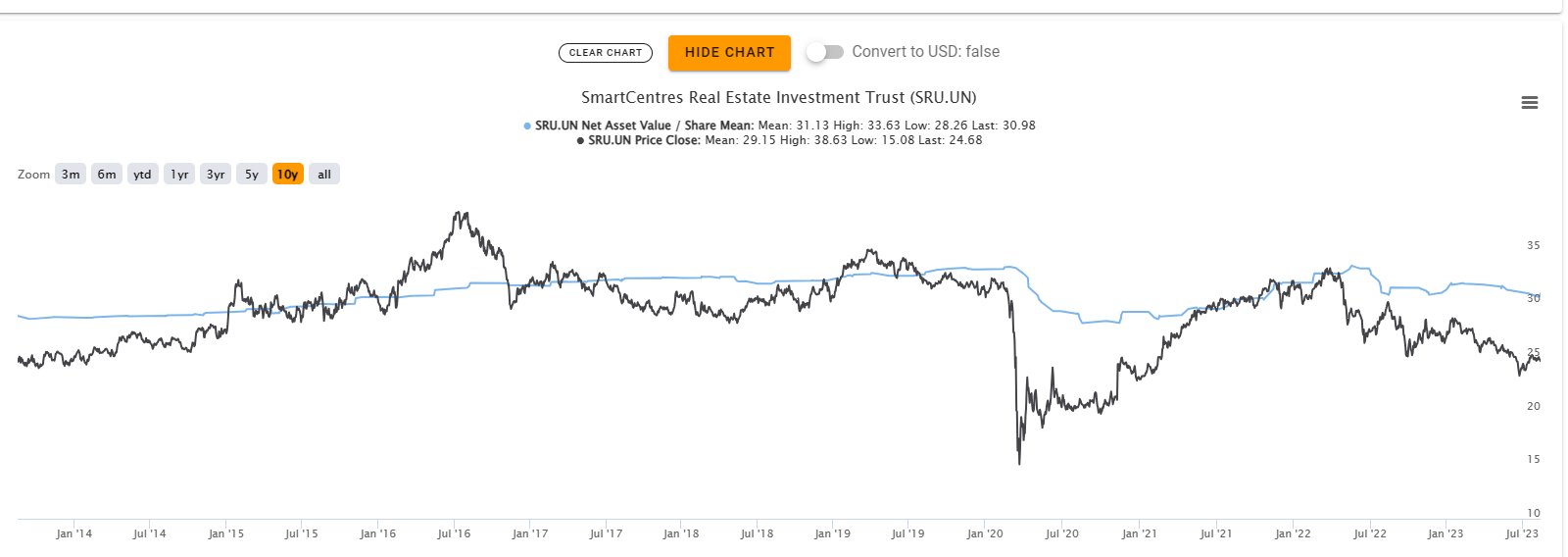

The other side is the valuation of the properties. The bull case is that the REIT is trading below consensus NAV. We agree there, and the current price is below even the very low end of analyst estimates. But this chase has been a "value trap" of sorts. As you see below, consensus NAV has been flat for almost a decade.

{kind=link}

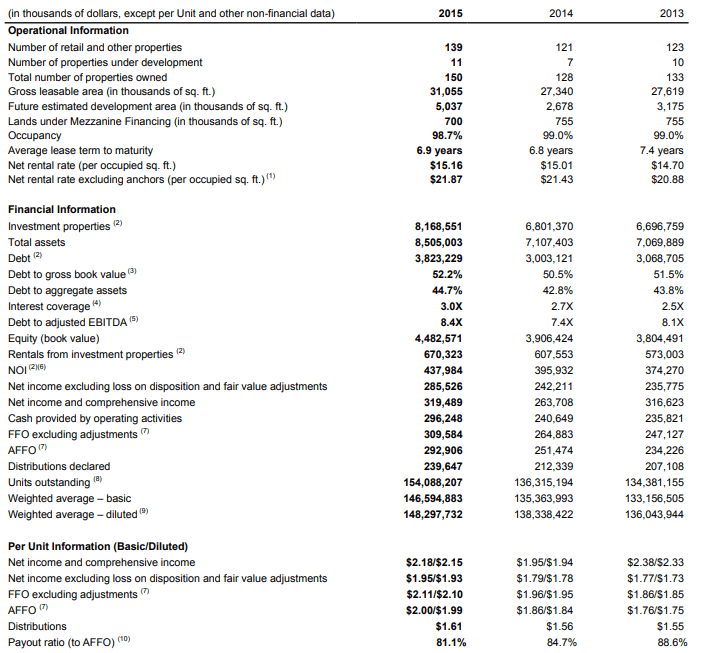

How exactly can that be when properties appreciate over time and NOI increases? Some of it could be a by-product of cap rate expansion. That is certainly true in the 2022-2023 era as interest rates have exploded up. But even between 2014 and 2020 NAV estimates from the perpetually optimistic analysts, stayed flat. Here is the answer to that question. Examine the FFO and AFFO per unit for 2015 and compare them to the estimated amounts for 2023 and 2024.

{kind=link}

They are going to be at about the same level. Even though SmartCentres was using 2 turns of debt to EBITDA less back then. So if you cannot grow your numbers over a decade, even after using more leverage, that answers almost everything.

Verdict

At the current price, we are close to a 7.5% implied cap rate for the REIT. We will dare say that it is a bit high and the REIT is worth a little more. Someone could come in and pay a small premium here for these assets. The REIT's underperformance has also fixed the valuation gap with both H&R REIT and RioCan. So color us a little more optimistic at $24 versus at $30. We are not ready to give this a straight buy rating yet, but think that investors can consider doing some covered calls to create a buffer and additional income. You could easily get a 12-14% annualized yield from the call premium and the dividends. So that method today would make a more acceptable risk-reward versus buying at $30.00 direct in January 2023. We think if we see $21-$22 or a reduction in debt levels, we might be interested. As it stands, we like the low capex REITs for our retail exposure.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

SmartCentres: Yield Jumps To 7.7% And Outlook Improves