MNDY - Smartsheet: The Smart Thing To Do Is Long The Stock

2023-10-16 10:59:54 ET

Summary

- I recommend a buy due to SMAR potential accelerated growth driven by innovative products, converting Excel users, and shifting to paid users.

- The company has demonstrated strong financial performance and I expect it to reach $1.57 billion in revenue by FY26.

- The incorporation of AI and success in landing large deals highlight Smartsheet's product innovation and market strategy.

Summary

I am recommending a buy rating for Smartsheet ( SMAR ), as I am optimistic that the business can accelerate its growth back to 30%, driven by its innovative product offerings, secular tailwinds in converting existing Excel users, and the conversion of free to paid users. Importantly, as SMAR shows a recovery in growth rate, the market should rerate its valuation back up to its peers’ level.

Business

SMAR is a cloud-based platform for work collaboration and project management that mainly targets large enterprises. Commonly known peers are monday.com ( MNDY ) and Asana ( ASAN ), which offer similar products. SMAR mainly generates revenue by selling subscriptions to its cloud-based platform. As of 2Q24, subscription revenue contributed over 94% of revenue. The SMAR pricing model is based on a per-seat basis, with different pricing plans that vary depending on the capabilities being offered. As of 2Q24, 80% of SMAR ACV comes from customers with more than $50k ACV.

Financials / Valuation

{kind=link}

Based on author's own math

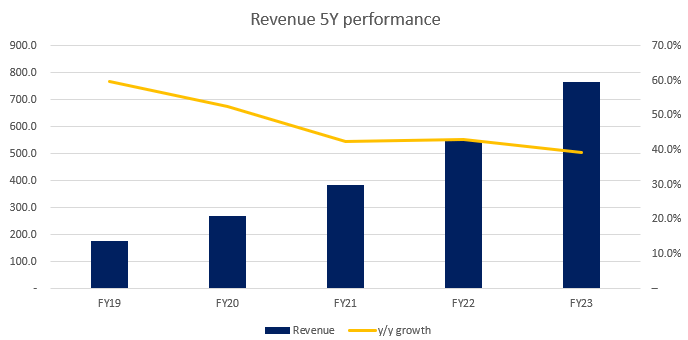

SMAR has demonstrated tremendous performance over the past 5 years, more than tripling the revenue base from sub-$200 million to a little over $750 million in FY23. This strong growth was driven by continued success in penetrating the work collaboration industry, which is significantly underpenetrated—most businesses still use Microsoft Excel to manage their project timelines, for example. Contrary to what the macro environment is indicating—businesses are pulling back on IT spend—SMAR performance clearly indicates otherwise, suggesting that its value proposition significantly outweighs the cost to businesses. However, like many high growth software companies, the time came for SMAR to balance growth vs profitability, and SMAR did not disappoint. The business improved EBITDA margin significantly from -20+% margin to ~-11% over the LTM. At the pace of growth, SMAR should be reaching positive profit regions over the next few quarters. SMAR’s balance sheet also remained strong through the years, maintaining a net cash position over the past 5 years (current balance sheet profile: $549 million in cash and $57 million in debt).

While growth has slowed down to 26% in the recent 2Q24 quarter, I remind investors that 26% beat consensus expectations and is still a very strong growth figure, especially in today’s uncertain macro environment. The beat relative to consensus expectations was driven entirely by subscription revenue, which grew by 28%. SMAR is also working hard to steer the business towards higher profitability (pro-forma EBIT came in at 8% margin), which beats consensus expectations by 500bps.

Based on author's own math

Based on my view of the business, SMAR should be able to accelerate its growth back to 30% as the economy gradually recovers over the next 2 years. FY24 should be the trough in weak performance, as per management guidance, followed by improvements in FY25 and FY26. Management guidance is a good benchmark because over the past 16 quarters, management has always beat its own guidance. In FY26, I expect SMAR to generate $1.57 billion in revenue. Based on my outlook on the business, I believe it should be trading at least in line with peers’ multiples and not the lowest among the pack. SMAR is expected to grow at similar rates to its peers’ (20+%), and it has a better profit margin profile than peers like Freshworks and Asana. As such, valued SMAR at 6.4x forward revenue multiple, the median of the group. With these assumptions, I believe SMAR is worth $78 in FY25. One reason why SMAR is trading at a discount is because peers were growing faster than SMAR previously, which the market might be worried that SMAR growth will continue to be slower.

- Workiva: 7.5x EV/forward revenue

- monday.com: 7.1x EV/forward revenue

- Freshworks: EV/6.4x forward revenue

- Asana: 5.2x EV/forward revenue

(Peers forward multiple source: Bloomberg)

Comments

The latest 2Q24 results show that SMAR is continuing to perform well, with revenue and PF EBIT margin both exceeding expectations. The calculated billings and ARR metrics also demonstrated the quarter's strength. Billings increased by 18% year over year and annual recurring revenue [ARR] by 27% year over year. Importantly, net-new ARR saw strong sequential growth relative to 2Q23 vs. 1Q23, a period in which there was no severe macro pressure. Bearish investors might nitpick that the dollar-based net retention rate contracted 200 bps sequentially to 121%, but I point out that gross churn rates remain stable at 4% and SMAR has a healthy pipeline of potential deals (hence giving management visibility to 2H24 billing guidance) entering 3Q24. While management guided a 116 to 117% dollar-based net retention rate, I expect this figure to improve as the economy turns for the better.

" But what we also saw on top of that was the pipeline entering Q3 was healthy. And when you couple both those elements with the fact that our close rate on pipeline we entered the quarter with is strong and maintaining strength, that's what gave us the confidence in the back half guide on billings ." Source: 2Q24 earnings

Importantly, if we look beneath the revenue growth, it speaks very well of SMAR traction in landing large deals, as evidenced by the fact that the company added more million-dollar ACV customers in 2Q24 compared to 2Q23 (4 as compared to 2 in 1Q24 and 3 in 2Q23). In addition, management highlighted the success of Capability-based offerings (i.e., capability in this context refers to modules or functions such as JIRA Connector or Bridge . Refer to this link for all capabilities ), which were included in each of the top 10 deals closed during the quarter. The latter gives me faith that SMAR's product innovation is keeping pace with the demands of businesses and that its go-to-market strategy for selling these products at higher prices is successful. Cisco, one of SMAR's earliest customers, has signed a multi-year, multi-million dollar extension deal in 2Q24, providing strong evidence for this claim. Therefore, in terms of the future of SMAR, I anticipate the upcoming innovations, especially in AI, to continue fueling expansion. In its most recent ENGAGE 2023 presentation, management emphasized the seven areas in which it is currently implementing AI:

- Generate formulas,

- Generate text and summaries,

- Analyze data,

- Create a custom solution,

- Get help,

- Tag people,

- Caption images.

The third point (data analysis) is where I anticipate the most significant change to occur. This function allows for the generation of graphical charts through the use of natural language prompts, drastically cutting down on the amount of time spent on chart creation for power users. And while this feature is currently tied to questions on just one sheet, management has promised that it will expand to allow users to gain insights across thousands of active projects in the future. Viewed from another angle, this transforms SMAR into an actual database visualizer—think of Oracle or SAP databases, but with an easier user interface—which further improves its value proposition. One more useful AI ability is the ability to save users a lot of time by developing custom solutions based on simple conversational prompts. These solutions can include full end-to-end project plans, workflows, and dashboards.

As the macro environment, particularly for enterprise customers, appears to be stabilizing, I think SMAR may be able to speed up its expansion plans. If SMAR can grow by 26% even when the economy is at its worst, it should have no trouble expanding even further when things improve.

" In Q2, we saw some signs of macro stabilization, particularly with our enterprise customers and with Smartsheet Advance." Source: 2Q24 earnings

The impressive performance in a still uncertain macroeconomic landscape is a source of encouragement for me. As I look ahead to the upcoming year, numerous avenues for growth become apparent, including an increase in the conversion of free users to paid users, driven by the introduction of premium AI services, as well as the momentum generated by AI-based offerings and the greater adoption of Capability-based solutions. Consequently, my outlook remains largely positive regarding SMAR's ability to solidify its position as the leading player among large enterprises in the market.

Risk & Conclusion

Over the past decade, Smartsheet has built an impressive list of blue chip customers that have helped it become a category leader. Competition from companies like MNDY and ASAN, which appear to offer the same service to an outsider, poses a threat to SMAR's ability to grow revenue, increase profit margins, and keep existing customers happy. In addition, if large vendors like Microsoft or Google, create products with similar functionality to SMAR, SMAR may have trouble competing because those companies can afford to offer deep discounts or even free products as part of larger customer engagements. The way I would monitor this risk is by tracking functions that competitors offer to see if they are matching the capabilities that SMAR is offering. Another risk would be a major recession that basically forces businesses to shut down, which will impede SMAR growth potential.

Overall, I recommend a buy rating for SMAR due to my optimistic outlook on its potential for accelerated growth. SMAR's innovative product offerings, the conversion of Excel users, and the shift from free to paid users position the company for a return to 30% growth. As the macroeconomic environment stabilizes, I anticipate SMAR's valuation will re-rate in line with its peers. SMAR's success in landing large deals and the adoption of Capability-based offerings underscore its product innovation and market strategy. The incorporation of AI in various areas bodes well for future expansion.

For further details see:

Smartsheet: The Smart Thing To Do Is Long The Stock