XSD - SMH: Downside Risks To Consider For Semiconductors In The Event Of Recession

2024-01-11 14:36:39 ET

Summary

- Downside "risk" for investors in the semiconductor industry is abnormally high, if the AI boom in semiconductor stocks proves short-lived, as a recession hits and competition mushrooms in 2024.

- Recessions in particular have proven difficult to overcome in the notoriously cyclical semiconductor space.

- Sector ETFs like the VanEck Semiconductor product are sitting on the potential for a -30% to -50% price decline over the next 12-18 months.

With NVIDIA ( NVDA ) and Advanced Micro Devices ( AMD ) reaching for new all-time highs this week, I thought I would more clearly spell out the downside potential for investors in the industry. If the artificial intelligence [AI] boom in semiconductor demand proves either transitory or less profitable than current forecasts, an oversized sector decline is likely during 2024. A major recession in capital spending by Big Tech firms during late 2024 and 2025, plus increasing competition for high-end chips, could mean sales and income expansion are peaking for the industry as we speak.

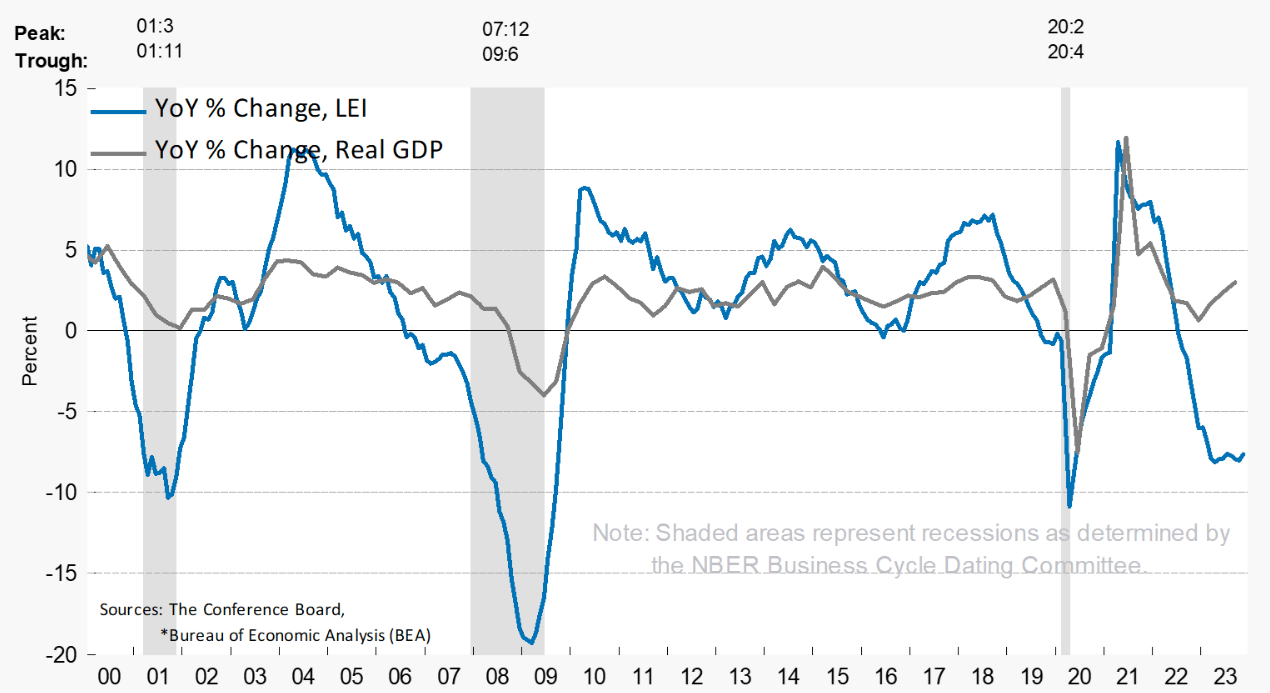

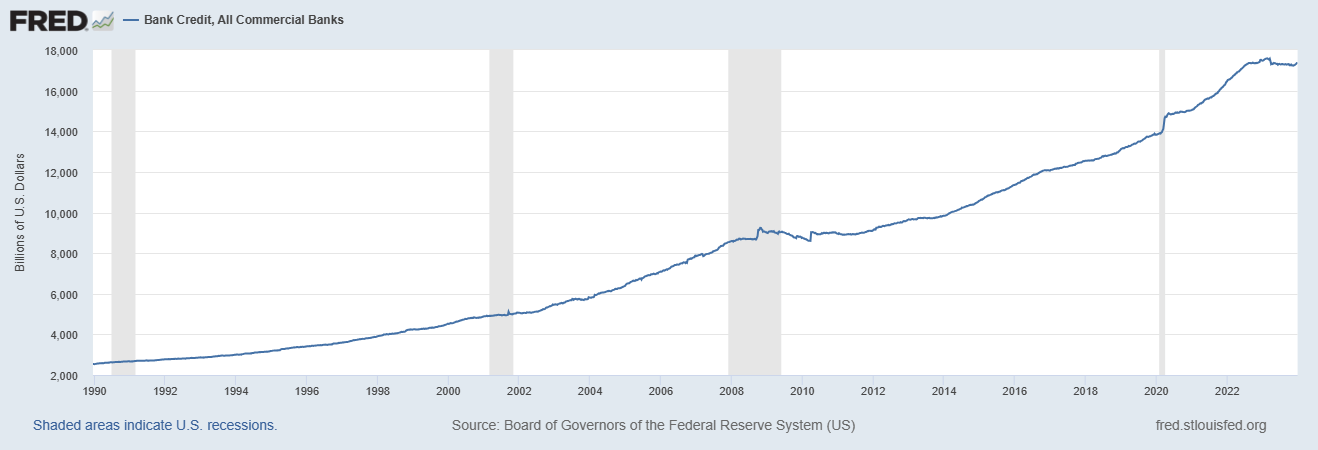

I know I am playing devil's advocate, and my message may not be well received by bullish AI chip readers/owners. Nevertheless, a dose of common sense is now called for in the sector, especially with the government's main index of leading economic indicators [LEI] signaling a recession is well past due in January 2024. Total banking credit has also been in contraction YoY since the summertime, last occurring in 2009-10 at the end of the Great Recession. Both are highly correlated with contractions in GDP.

{kind=link}

The Conference Board - LEI Index, Since 2000, Recessions Shaded in Grey

{kind=link}

St. Louis Federal Reserve - Total U.S. Banking System Credit, 1990 to Present, Recessions Shaded in Grey

The Boom Phase

After an incredible run measured from the Great Recession bottom in early 2009, my opinion is "all good things must come to end" for the Big Tech winners held by VanEck Semiconductor ETF ( SMH ). Economic forces driven by chip supply/demand do matter. While Wall Street and main street investors alike seem to be focused only on the upside arguments for ownership, a recession in the overall economy would absolutely hurt expected sector sales for 2024-25 negatively, while mushrooming competition in AI chips should drive pricing and profits far lower than current projections later in the year. Basically, the boom could turn to bust sooner than stakeholders in the industry believe possible. That's my view. The SMH price advance of 4x the S&P 500 index total since early 2009 may well be setting up for a steep underperformance span lasting several years, despite overall sales gains by the main players in high-end chips.

YCharts - SMH vs. SPDR S&P 500 ETF, % Price Change, Since Jan 2009

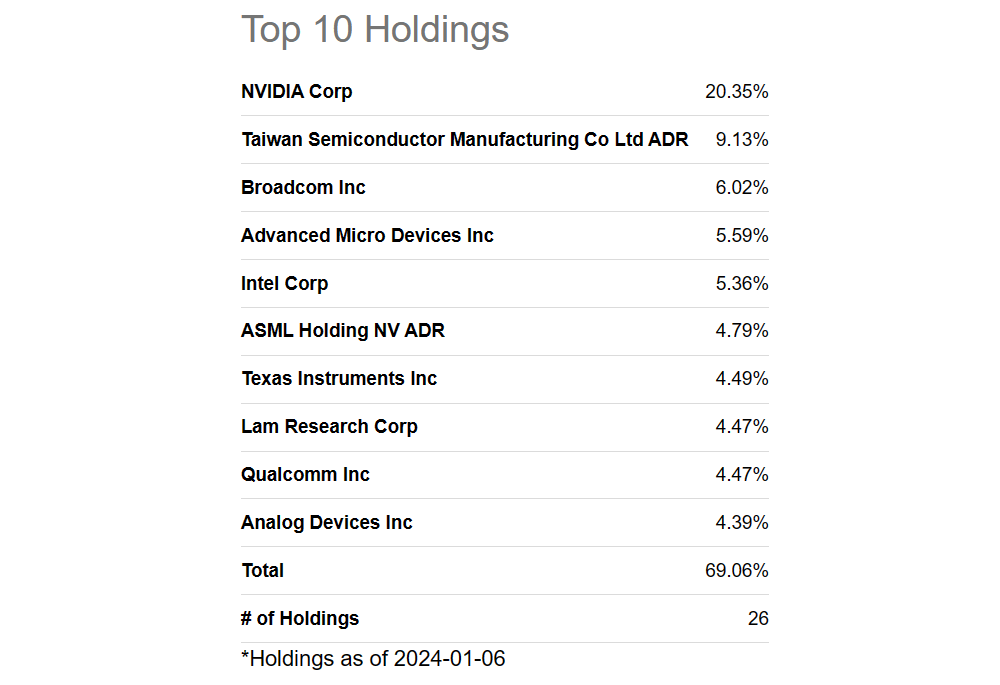

It's hard to argue with a straight face that the semiconductor group has not been experiencing a boom in investor buying, with the price gains witnessed since November 2022. Most all of the advance has been concentrated in the largest companies by market cap focused on AI excitement, which are heavily weighted in the SMH ETF product. The Top 10 holdings by index weight include NVIDIA, Taiwan Semi ADR ( TSM ), Broadcom ( AVGO ), AMD, Intel ( INTC ), ASML Holding NV ADR ( ASML ), Texas Instruments ( TXN ), Lam Research ( LRCX ), Qualcomm ( QCOM ) and Analog Devices ( ADI ).

{kind=link}

Seeking Alpha Table - SMH, Top 10 Holdings, January 6th, 2024

YCharts - SMH Top 10 Holdings, % Price Change, Since November 2022

YCharts - SMH vs. SPDR S&P 500 ETF, % Price Change, Since November 2022

The 20% weighting in NVIDIA and steep concentration of nearly 70% in the biggest semiconductor companies could mean SMH will be an underperformer in a bust situation vs. peer sector ETFs. The script of extra gains in 2023 pumped by NVIDIA's run could morph into general underperformance for SMH during 2024 vs. iShares Semiconductor ( SOXX ), SPDR S&P Semiconductor ( XSD ), and Invesco Semiconductors ( PSI ).

YCharts - SMH vs. Major Semiconductor ETFs, Total Returns, Since November 2nd, 2022

What A Bust Could Look Like

The first semiconductor boom setup in sentiment and pricing, fueled by wild expectations and the initial development of network computing in the Dotcom Era , saw rampant investor speculation in the 1990s eventually turn to bust. While today's semiconductor situation is not a carbon copy, investors have gotten overly bullish on the sector right before a recession, leaving plenty of downside risk.

2000-2002

Between June 2000 and September 2002, the VanEck Semiconductor ETF fell -81% in value, as recession hit. This bust loss was roughly double the rate of S&P 500 index decline. My sobering suggestion: don't say something similar cannot happen again today.

YCharts - SMH vs. SPDR S&P 500 ETF, % Price Change, June 2000 - September 2002, Recession Shaded

2008-09

Another semiconductor bust took place during the Great Recession. Between the middle of 2007 and early 2009, SMH declined by -60%, top to bottom. I have charted this period below, underperforming the S&P 500 company average.

YCharts - SMH vs. SPDR S&P 500 ETF, % Price Change, July 2007 - June 2009, Recession Shaded

2020

The 2020 pandemic panic and recession also knocked semiconductor names with a quick -30% drop into the final week of March. The good news silver lining (if you will) is SMH fell about the same rate as the S&P 500 index.

YCharts - SMH vs. SPDR S&P 500 ETF, % Price Change, January to April 2020, Recession Shaded

2022

Calendar 2022 was a disappointing time to own all stocks, particularly Big Tech names. No recession appeared, but stretched overvaluations reversed on the rise in inflation and interest rates during the year. SMH doubled the decline rate of the S&P 500 index with a -43% drop between December 2021 and October 2022.

YCharts - SMH vs. SPDR S&P 500 ETF, % Price Change, December 2021 - October 2022

Industry Valuations Are Double 2016 Level

I have written bearish articles on both NVIDIA and AMD, trying to explain the overvaluation setup for each, assuming a recession in the U.S. and fierce competition between the two in the AI chip area of the marketplace are next in 2024. Enterprise valuations on EBITDA for the Top 10 ETF holdings are running nearer 5-year highs, despite dramatically higher interest rates as competition for your investment dollars. While a median average ratio of 20x was somewhat acceptable during a period of economic growth and low interest rates, my argument is this number is way too expensive going into a potential recession with the highest interest rates since 2008 (just before the Great Recession).

YCharts - SMH Top 10 Holdings, EV to EBITDA, 5 Years

For a valuation comparison, the Big Tech boom really got going in early 2016 (from my count). At that point, this group's median average EV to EBITDA ratio was closer to 10x, while interest/inflation rates were far lower than today. Note: eight years ago, AMD didn't have EBITDA.

YCharts - SMH Top 10 Holdings, EV to EBITDA, 2015 to January 2016

One bubble attribute of the "madness of crowd behavior" in the stock market revolves around quickly rising quotes, despite business trends expanding less rapidly. The combination of a sizable advance in Big Tech pricing since October 2022 and a huge jump in interest rates while the economy continues to slow (both usually bring down valuations), does not add up to a great foundation for future chip-sector gains. While the financial media is running with the idea outlier industry growth is assured to back up 2023's share price gains, I am not as confident.

Final Thoughts

The basic conclusion of this research is you don't want to own semiconductor stocks during contractions in U.S. GDP output. So, if you believe a recession is all but inevitable in 2024, keeping weightings for chip names on the low side of your portfolio makes rational sense. The AI boom spike in 2023 highlights a unique setup where industry valuations/sentiment are extremely high going into a potential sector bust.

Using history as our guide, downside projections of -30% to -50% in the VanEck Semiconductor ETF over the next 12-18 months are quite realistic, depending on how weak the global economy gets.

My view is long-term investors should be looking to sell SMH, not buy this semiconductor-focused ETF. To outline a bullish advance for 2024, we have to escape the year without recession while corporate profits remain high. If corporate profitability in the general economy declines markedly, the capital and incentives to invest heavily in new high-speed datacenter products could disappear. Then the whole sector has a problem, since today's expectation is calling for solid growth over 2023's amazing demand numbers.

Gartner is projecting AI-related chip sales to grow at a 20% clip annually into 2027. My view is this forecast may prove overly optimistic at the same time as chip demand elsewhere in the industry stalls from recession effects.

AI semiconductor revenue will continue to experience double-digit growth through the forecast period, increasing 25.6% in 2024 to $67.1 billion (see Table 1). By 2027, AI chips revenue is expected to be more than double the size of the market in 2023, reaching $119.4 billion.

Table 1. AI Semiconductors Revenue Forecast, Worldwide, 2022-2024 (Millions of U.S. Dollars)

2022

2023

2024

Revenue ()

44,220

53,445

67,148

Source: Gartner (August 2023)

For sure, the boom/bust cycle is still at play in the semiconductor industry. The laws of supply and demand have not been repealed. The AI marketplace will act no differently than past chip cycles. If you believe excessive pricing/profits will create competition, like I do, my suggestion is to consider selling the Big Tech semiconductor names in January 2024. Avoiding SMH until a recession drop plays out may be the smartest decision. Almost every major Big Tech name, semiconductor or not, has announced plans to design and build their own AI chips, from Apple ( AAPL ) to Intel to Alphabet-Google ( GOOG ) ( GOOGL ) to Qualcomm and a long list of overseas suppliers.

The bullish semiconductor industry argument centers on a soft landing or no landing scenario for the U.S. economy. If you believe a growing economy will be part of the 2024-25 investment equation, SMH could continue rising. I fully understand if you want to hold shares with this optimistic outlook.

What's the upside potential? That's a terrific question. Had I written this article in October, gains of +20% to +30% in SMH would have been missed. In terms of overexcitement and bubble trading patterns, I cannot guarantee a similar gain is impossible over the next 2-3 months. Bubbles tend to blow up in size like a balloon, until they pop.

But using my decades of experience trading through four recessions, I feel now is the correct time to rate SMH a Sell for a 12-month outlook. If you must remain long, please tread carefully, and be ready to liquidate with tight sell-stops to protect your gains.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

SMH: Downside Risks To Consider For Semiconductors In The Event Of Recession