SMICY - SMIC: U.S. Bringing The Hammer Down

- Following the report of the potential ban on ASML from supplying DUV equipment, we expect this to be a threat to Semiconductor Manufacturing International as its FinFET/28nm accounts for 18.9% of sales.

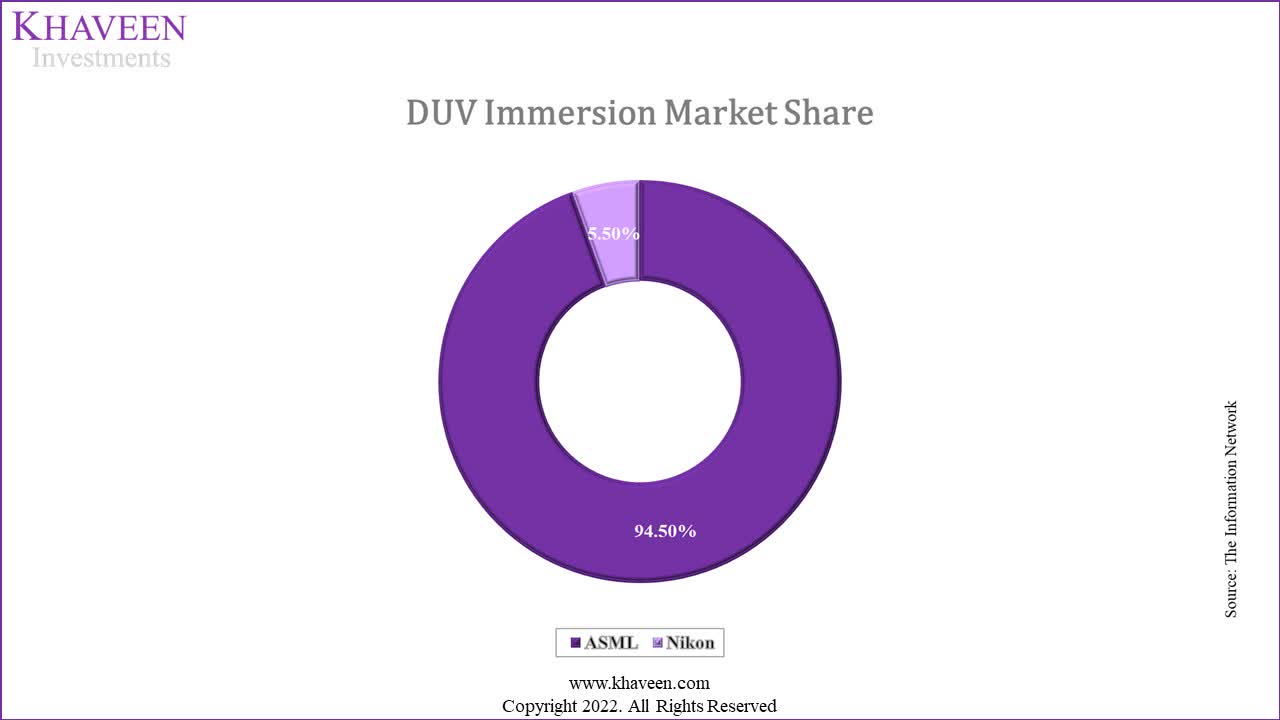

- Although Canon and Nikon are alternative suppliers, we believe ASML's market dominance over DUV (94.5% share) could limit its ability to procure alternative supplies.

- We estimate a revenue impact of 10.1% to SMIC accounting for the potential loss in shipment and limited ASP growth should the ban take effect.

In July, Bloomberg reported that the US government was pushing the Netherlands to restrict the sale of deep ultraviolet lithography ((DUV)) systems to Semiconductor Manufacturing International Corporation ( SMICY ). Recently, Lam Research ( LRCX ) and KLA ( KLAC ) confirmed that the government was tightening restrictions on the sale of semiconductor equipment with below 14nm process capability. This follows after the US Department of Commerce had previously placed restrictions on SMIC by adding the company to the Entity List in 2020 which requires US companies to obtain a license to export to the company. Additionally, the US CHIPS and Science Act with $52 bln in grants and research programs as well as tax credits for new facilities was passed in July and we believe this highlights a threat to SMIC, which derived 22% of revenue from North America based on its annual report, by moving the manufacturing supply chain from China and instead promoting US chip manufacturing. Thus, we analyzed the potential impact of the increasing restrictions on the company in terms of its process technology advancement and revenue growth in terms of shipments and ASP impact and the availability of alternative suppliers.

Threat to Company’s Process Technology Advancements

{kind=link}

Based on the chart above, SMIC’s revenue contribution from its FinFET/28nm node has grown over the past year and had become its 3rd largest contributor to revenue, accounting for 18.6% of revenue in Q4 2021 behind its 0.15/0.18nm and 55/65nm nodes. Its revenue from FinFET/28nm was the fastest-growing segment at an average of 64.36% QoQ in the past 5 quarters. Previously, SMIC was reportedly to achieve a 95% yield with its 14nm process according to industry sources.

Based on a report by Reuters, the US Department of Commerce was believed to be

examining the possibility of prohibiting the exportation of chipmaking tools to companies in China that can make logic chips using 14nm-class manufacturing nodes and thinner.

Furthermore, Bloomberg reported that the US seeks to block ASML (ASML) from supplying deep ultraviolet lithography systems to China. Previously, ASML was restricted from supplying EUV equipment to SMIC for 10nm chips and below. Also, SMIC was placed on the Entity List by the US Commerce Department in 2020 restricting its ability to acquire advanced US technology.

Thus, we believe that the reported prohibition of equipment exports to SMIC for 14nm chips could affect the company’s process technology advancement. SMIC had also previously begun development on its 12nm, N+1, and N+2 process technologies which relied on DUV lithography and were reported to have canceled the development.

Limited Availability of Alternative Equipment Suppliers

{kind=link}

Based on the chart above, ASML was the market leader in DUV Immersion equipment with a 94.5% market share according to The Information Network . However, compared to the EUV equipment market which ASML has a monopoly as the only company producing EUV systems in our previous analysis of the company, alternative DUV equipment suppliers include Nikon ( NINOF ) and Canon ( CAJ ). EUV systems use smaller light wavelengths up to 15x than DUV systems and are used by chipmakers for advanced process nodes 10nm and below with lower power consumption and area reduction. However, EUV has higher cost barriers than DUV which inhibited its adoption among a few major customers such as TSMC ( TSM ), Samsung ( SSNLF ), SK Hynix, Micron ( MU ), and Intel ( INTC ). In terms of the financial impact, while the cost of EUV equipment is higher than DUV, however, advanced nodes command superior pricing than older nodes and could lead to better margins if the increase in ASPs is higher than the increase in unit production costs.

Therefore, if the reports come true, the export ban of DUV systems to SMIC could impact the company. Despite there being alternative suppliers, ASML has a monopoly in EUV and also a strong prominence in DUV systems with a 95% market share which we believe could highlight a limited availability of alternatives for SMIC. In relation, based on its annual report , SMIC’s major supplier accounted for 31% of purchases and its top 5 suppliers for 56% of total purchases in 2021, which we believe highlights its high dependency on selected suppliers.

Negative Revenue Impact of 10.1%

| SMIC Revenue Projections ($ mln) |

| 2020 |

| 2021 |

| 2022F |

| 2023F |

| 2024F |

| 2025F |

| 2026F |

| Wafer Shipments (With Impact) |

| 5,968 |

| 7,407 |

| 8,142 |

| 8,153 |

| 8,920 |

| 9,688 |

| 10,456 |

| Growth % |

| 12.2% |

| 24.1% |

| 9.9% |

| 0.1% |

| 9.4% |

| 8.6% |

| 7.9% |

| Wafer ASPs (With Impact) |

| 655 |

| 735 |

| 845 |

| 884 |

| 916 |

| 942 |

| 960 |

| Growth % |

| 11.7% |

| 12.2% |

| 15.0% |

| 4.6% |

| 3.7% |

| 2.8% |

| 1.9% |

| Revenue (With Impact) |

| 3,907 |

| 5,443 |

| 6,880 |

| 7,206 |

| 8,175 |

| 9,125 |

| 10,033 |

| Growth % |

| 25.4% |

| 39.3% |

| 26.4% |

| 4.7% |

| 13.5% |

| 11.6% |

| 9.9% |

| Wafer Shipments (Without Impact) |

| 5,968 |

| 7,407 |

| 8,142 |

| 8,989 |

| 9,835 |

| 10,682 |

| 11,528 |

| Growth % |

| 12.2% |

| 24.1% |

| 9.9% |

| 10.4% |

| 9.4% |

| 8.6% |

| 7.9% |

| Wafer ASPs (Without Impact) |

| 655 |

| 735 |

| 845 |

| 888 |

| 924 |

| 952 |

| 972 |

| Growth % |

| 11.7% |

| 12.2% |

| 15.0% |

| 5.1% |

| 4.1% |

| 3.1% |

| 2.1% |

| Revenue (Without Impact) |

| 3,907 |

| 5,443 |

| 6,880 |

| 7,980 |

| 9,087 |

| 10,171 |

| 11,204 |

| Growth % |

| 25.4% |

| 39.3% |

| 26.4% |

| 16.0% |

| 13.9% |

| 11.9% |

| 10.2% |

| Revenue Impact |

| 0 |

| 775 |

| 912 |

| 1,046 |

| 1,171 |

| % of Revenue |

| 9.7% |

| 10.0% |

| 10.3% |

| 10.5% |

Source: SMIC, Khaveen Investments

To account for the potential impact on SMIC’s shipment growth in our previous revenue projections of the company, we estimated its capacity for 14nm chips in 2024 based on its FinFET/28nm revenue share of 18.6% divided by 2% (9.3%). Based on this assumption, we reduced its shipments by 9.3% in our estimates, assuming the crackdown comes true. According to IC Insights, it forecasted the share of installed wafer capacity for process nodes between 10nm to 20nm to shrink to 26.2% by 2024 from 38.8% in 2019. Whereas it expected the advanced nodes below 10nm to increase from 4.4% to 29.9% by 2024.

In terms of pricing, the estimated pricing for wafers increases with higher process nodes. For example, TSMC’s estimated 5nm is 81% higher than its 7nm and its 7nm is 56% more expensive than its 10nm. Thus, we expect the company’s limited process technology advancement if it is unable to procure equipment to affect its revenue growth through wafer ASP growth. Thus, we expect its ASP could be weighed down if its 14nm production is impacted. We estimated its ASP growth previously based on its 5-average growth and multiplied it with its 14nm share assumption (19.3%) to estimate its ASP growth with the impact. Overall, we estimated an average revenue impact to the company of 10.1% of its total revenue should the company’s 14nm production be impacted.

Risk: SMIC May Be Developing 7nm Technology on Its Own

According to Tech Insights, through their reverse engineering analysis, SMIC appears to have used 7nm technology to produce an SoC. This is despite the restrictions on the company to procure EUV equipment from ASML, which they believe SMIC overcame by utilizing DUV lithography instead. Thus, this indicates that SMIC could be developing its 7nm technology on its own. However, Tech Insights mentioned that there is no confirmation through their analysis as:

there is no way to specifically identify which semiconductor processing tools were used to fabricate the chip.

Moreover, SMIC has not announced any 7nm-related breakthroughs. Interestingly, since Q1 2022, the company had also stopped reporting its revenue breakdown by process node from its investor presentation slides .

Admittedly, SMIC's financials have been stellar over the past year in terms of revenue growth and margins, as previously analyzed by Dr. Robert Castellano, of The Information Network.

Overall, we believe there still is no concrete evidence that the company has 7nm technology commercially but will monitor their ongoing revenue growth closely.

Verdict

{kind=link}

All in all, we believe the reported restrictions on SMIC to obtain DUV equipment for the production of its 14nm chips could impact the company as its FinFET/28nm segment accounts for 18.6% of its revenue and is part of its 3 rd largest segment by process node. Also, we believe its ability to procure alternatives could be limited due to the market leadership of ASML and the limited number of suppliers including Nikon and Canon. In terms of the potential impact on its revenue, we estimated an average of 10.1% revenue impact based on shipments and ASP growth. SMIC's shares are listed on both the Hong Kong Stock Exchange and Shanghai Stock Exchange. Overall, we updated our DCF analysis from our previous analysis and downgraded our rating on the company to a Sell with a price target of $1.91 (HKD15) for its Hong Kong Exchange-listed shares (0981.HK) which translates to a downside of 16%.

For further details see:

SMIC: U.S. Bringing The Hammer Down