SNN - Smith & Nephew: Entering New Markets But Growth Is Slow Still

2023-08-01 04:44:27 ET

Summary

- Smith & Nephew plc is a long-standing company in the medical device sector, focusing on developing and manufacturing internationally.

- The company has recently received FDA clearance for its AETOS Shoulder System, aiming to gain market share in the shoulder replacement market.

- SNN's strong margins and presence in multiple markets provide potential for sustainable growth, but improvements in cash flows and margins are needed.

Investment Outline

Smith & Nephew plc ( SNN ) has been in the sector for a very long dating back to 1856. The company these days focuses on developing and manufacturing medical devices internationally. The headquarters are in the United Kingdom where operations first began, but have since grown to an international presence.

With a broad set of product offerings, the company has grown its market share efficiently and in the hip and knee replacement market, they hold an 11% share . The revenues that the company generates from these sources still account for a large amount of the total revenues. I don't expect to see any drastic improvements here, but steady growth as the company makes operational performances better and passes down costs to consumers SNN can still pass value to shareholders. The dividend sits at 3% but I don't think the valuation makes sense given the growth. The stability of the business could justify the p/b of 2.5 given debt seems to provide no additional risk as cash flows are sustainable and EBITDA growing. I can't help but think there are better growth opportunities out there and this leads me to rate SNN a hold for now.

Recent Developments

Not long ago SNN announced they have gotten 510k clearance for its AETOS Shoulder System. On June 12 SNN said they have gotten the green light from the FDA for the AETOS Shoulder System. This marks SNN's attempt at gaining more market share in the shoulder replacement market. The industry is valued at $1.7 billion right now.

The technology that SNN has developed is meant to restore patients' range of motion and help minimize arthritic shoulder pain. For healthcare professionals, this new technology will provide a broad solid portfolio of various solutions to help with the surgical experience through improved flexibility.

The market opportunity that this opens up is quite big. A reasonable bet would be that SNN can gain an equal market share as in knee and hip implants where they hold around 11% of it. The capital for SNN is strong with a cash position of $350 million and TTM FCF of $138 million, and I think given their history and reputation in other markets will give them an advantage here in growing their revenues. Once everything gets rolling I don't see it as unreasonable that SNN will add another $100 - $200 million to the annual revenues.

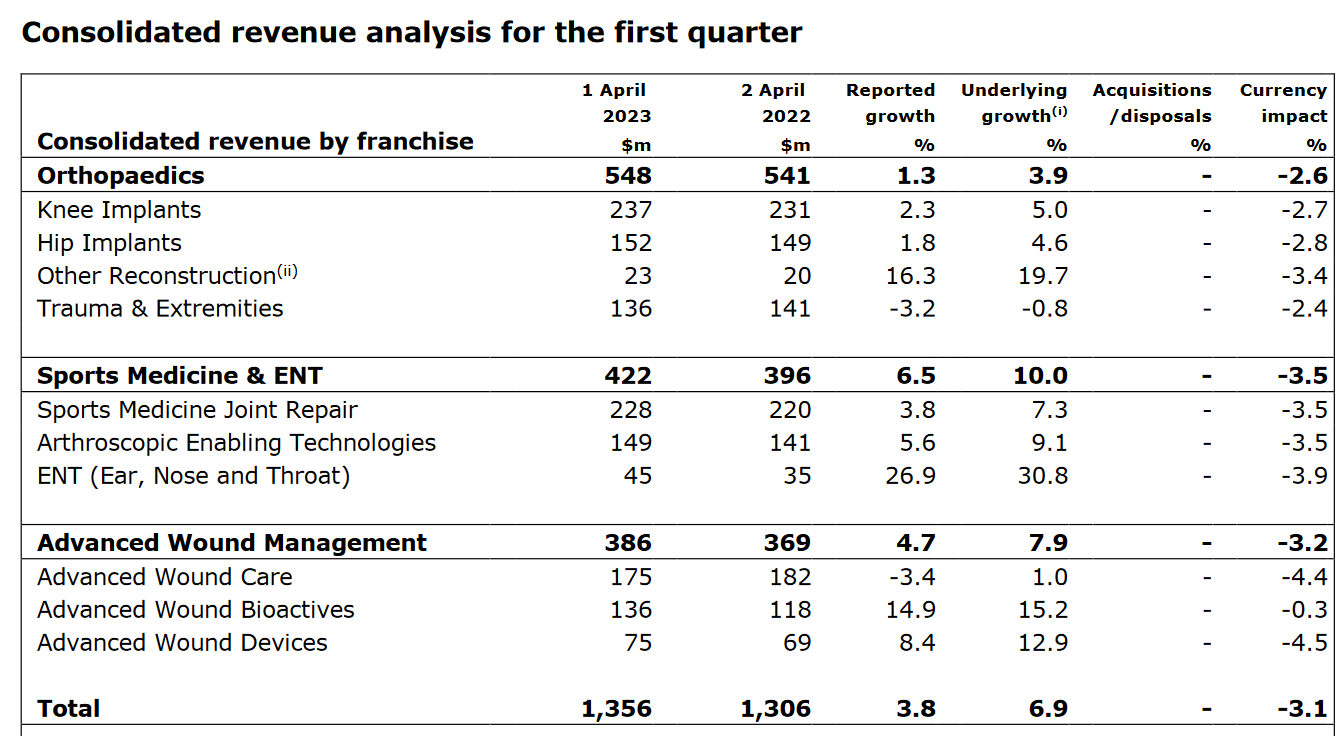

Revenue Breakdown (Earnings Report)

{kind=link}

A broader set of markets they are present in will bring more sustainable and stable growth I think. The revenues from orthopedics are still the leading source of revenues for SNN but sports medicine & ENT are not far behind. This is perhaps one of the more important parts to look at when assessing SNN right now. The market is expected to grow at a very respectable 5.8% CAGR until 2026. As we see from the last report from SNN they outpaced this and achieved a YoY growth of 6.5% instead. This shows that SNN has a strong position in the market and can still offer some sort of growth opportunity.

Margins

Margin Profile (Seeking Alpha)

The margins of SNN are very strong and beats out the sector on many fronts. The net margins do however sit at some of its lowest levels the last few years and are 59% below the 5-year average for SNN. This seems to come off the back of inflation and higher interest rates. As materials and costs are rising SNN needs to provide investors with strong progress in margin improvements.

Valuation

DCF Model (My Own Model)

SNN has a very tough task right now to recover its FCF and justify the current valuation. The intrinsic value here doesn't portray the value of SNN perhaps for its actual position in the market and the initiatives it's taken to broaden its line of solutions. But it does highlight the fact that SNN needs to take strong measures in reigniting its FCF and return to where it was a few years ago generating over $600 million. This will likely come from lower interest rates and a market environment where inflation won't be eating up earnings as costs rise.

The data points I have used are assuming a quite slow return to former cashflows, but given what I think is still a tough market to operate in I don't think any significant catalyst will catapult the FCF anytime soon. Given the reputation of the company though and its market share I have leaned towards a lower discount rate than what I normally do of just 1.08.

I think that SNN will going forward be better off as a hold. The position they hold lends them some stability regarding revenues, but stronger cash flows and bottom-line margins are necessary to view SNN as anything other than a hold.

Risks

The current state of the sector reflects its expensive nature, making it challenging to find genuine bargains. As investors seek value in an overpriced market, the pressure to meet higher expectations may lead to increased risk associated with investments.

Navigating an expensive market requires a cautious approach, as inflated valuations may create an environment of heightened risk. Investors must carefully scrutinize potential opportunities, conducting thorough due diligence to identify companies with true underlying value. While higher expectations can be indicative of strong growth potential, they also raise the bar for companies to deliver consistent and robust performance. This creates a scenario where even minor setbacks or unmet expectations could trigger negative market reactions.

Company Plan (Earnings Report)

The company needs to be very proactive in developing its revenue streams and move as far away from slowing growth or decreasing sales year-over-year. But this is especially implant because the valuation

Investor Takeaway

For investors that want a stable and divided distributing company then SNN does look quite good. The company has however seen a quite disappointing development for its FCF and the DCF model I made highlights the fact that SNN has a lot of improvements to be made before a buy could be suggested. As a result, I am rating SNN as a hold right now. The market position they have is impressive and new initiatives are promising but results need to be visible first.

For further details see:

Smith & Nephew: Entering New Markets But Growth Is Slow Still