SNNUF - Smith & Nephew: Flat FY22 Growth Now An Execution Story

Summary

- Smith & Nephew saw flat top-line growth, declines in earnings and CFFO relative to FY21.

- Management has instilled a new 12-point plan in order to drive performance from FY23 onwards.

- It is now a matter of execution, and we rate SNN a hold at 24x earnings, in-line with the industry multiple.

Investment Summary

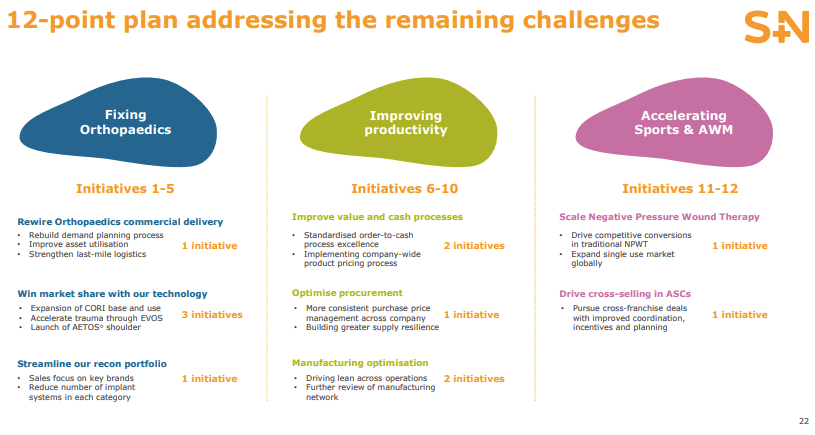

Medical devices behemoth Smith & Nephew plc ( SNN ) reported its Q4 FY22 results with a flat result at the top-line and earnings that missed consensus estimates. After a series of headwinds impacting performance in its orthopaedics segment, reflected in its commercial execution and flat sales growth, CEO Deepak Nath noted that SNN: " made good progress during 2022 and ended the year in a much stronger position than we started. We continued to outperform in Sports Medicine & ENT and Advanced Wound Management and, even though we are early in our work to fix Orthopaedics, performance improved here too". As a reflection of this, the firm noted it has reduced overdue orders in orthopaedics by 35% from their peak in FY21, simultaneously increasing the number of customer orders filled. Further, to address its "remaining challenges", the company has installed a 12-point plan, containing 12 initiatives to drive performance across 3 main areas. In particular, it hopes to address productivity via a multi-pronged plan, looking at its cash conversion, procurement, and manufacturing efficiencies [Figure 1]. Looking at our previous coverage on SNN from September last year, we noted that:

- Semi-annual operating trends have remained seasonal.

- SNN's FCF and return on invested ("ROIC") track each other with striking similarity.

- However, top-line growth has remained flat over several periods

- It also maintained its semi-annual dividend stream, returning capital to shareholders.

You can also observe our FY20 coverage on SNN here.

Net-net, we reiterate SNN as a hold at a 24x P/E, given it is now an execution story, and the company is now in 'prove it' mode. Read on for the full discussion of its results.

Fig. (1)

{kind=link}

Q4 & FY22 results analysis

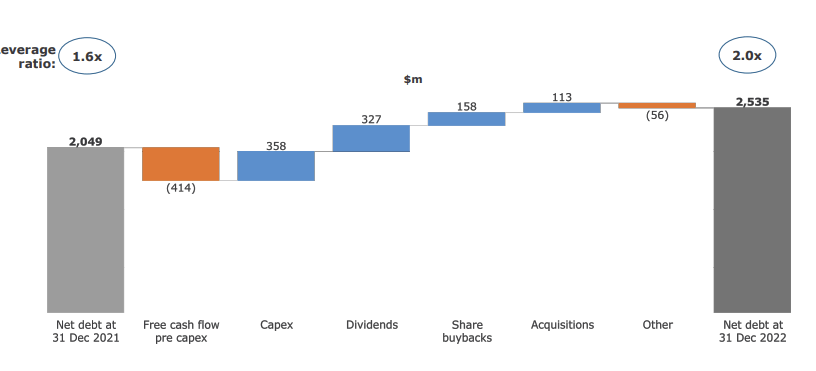

SNN booked Q4 top-line revenues of $1.36Bn, a small 140bps YoY gain from the previous year. Around 540bps of FX headwind is baked into this result. Adjusting for this, the core business growth was 680bps YoY. For the full-year, revenues came in flat with a 460bps FX headwind to $5.215Bn. Moving down the P&L, FY22 gross profit margin was flat at 70.5% on core operating profit of $450mm, down 31% YoY. SNN wasn't immune to inflationary headwinds that impacted its supply chain, particularly freight and logistics costs and marketing expenditures. Alas, its FY22 earnings were crimped ~386bps to $901mm on a margin of 17.3%. It pulled this down to EPS of $0.25, down from ~$0.60 the year prior. Further, it finished the year at 2x leverage with net debt increasing to $2.5Bn from ~$2Bn the year prior.

Fig. (2)

{kind=link}

Looking in further detail, perhaps the largest challenge SNN faced over the 12 months pertained to cash flow - CFFO clipped $581mm versus $1.05Bn the year prior. Underlining the downside was higher input costs related to raw materials and inventories, thereby compressing non-operating working capital. This reflects the language on inflationary pressures, but also reflects the challenges exhibited in its orthopaedics segment, combined with a lack of China exposure due to Covid-19 lockdowns.

Speaking of the quarterly divisional highlights, our takeaways are as follows:

- Core business growth in its orthopaedics segment [i.e., FX adjusted] was 410bps versus Q4 FY21, although this was a ~50bps decline on a reported basis to $549mm . Knees realized a c.90bps YoY growth to $234mm for the quarter. Orthopaedics has been a tension point for SNN investors over the past years. The firm puts this down to "poor operational systems and commercial execution". To this effect, management have instilled a '12-point plan' to improve sequential momentum across all of its core ortho segments. Looking at reported results, [i.e. no FX adjustments] the standout was in robotics, joint navigation and cements, with a 350bps YoY gain. Furthermore, SNN noted that it expects continued headwinds to its hip and knee VBP program due to the slow rollout in China.

- It was a more pleasing result in its sports medicine and ears, nose and throats ("ENT") business. It secured a c.300bps YoY growth underscored by upsides in its shoulder and knee repair segments. Sports med' joint repair was another compounder along with the ENT division that lifted to $41mm for Q4. We'd note the main contributor to ENT growth was driven by its tonsil and adenoid franchise. Core growth in this division came in at 920bps when adjusting for FX.

- Assessing the advanced wound management business, it recognized ~610bps in FX headwind. Underlying growth came to 8%, but just ~2% on a reported basis. We noted solid upsides in its wound care division with ~790bps growth when adjusting for FX headwind, however slipped -110bps on a reported basis. Wound bioactives had a strong quarter and managed to secure a 390bps reported growth, however. Further, SNN reported double digit growth in its PICO negative pressure wound system, helping drive its advanced wound devices portion by ~7% YoY.

Fig. (3) SNN divisional breakdown

Note: YoY growth presented on reported numbers. Forex-adjusted growth percentages aren't shown. (Data: Author, adapted from SNN Q4 FY22' results)

Capital budgeting and management

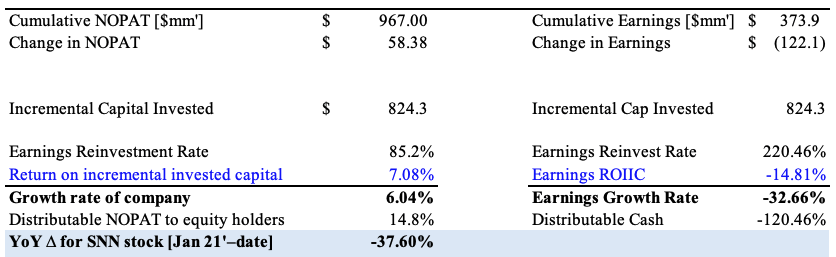

It's important to note that SNN completed its FY22 buyback program in August and repurchased $150mm of common stock. However, management decided to pare this back and withhold on any further buybacks in FY23. Despite this, it maintained its dividend with a $0.23 final dividend, totaling a $0.375 distribution to equity holders, flat on the FY21 payout. Looking at its profitability in greater detail, it's important to note that incremental return on capital was a challenge in FY22 for SNN. From FY21, the ROIC compressed by ~80bps to 12.5%, despite a $58mm YoY increase in NOPAT.

Fig. (4)

Data: SNN SEC Filings, SNN Q4/FY22' financial report

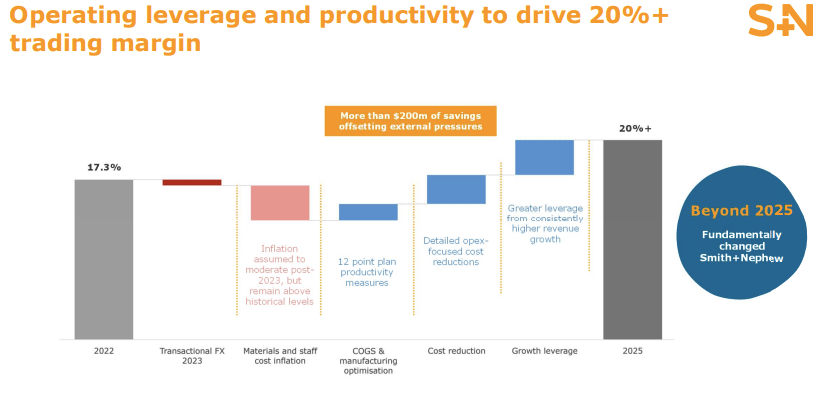

Whilst ROIC provides an excellent measure on the profitability and growth of a company, what really matters is how ROIC and profitability will change in the future - moreover, if the change is different from consensus. Alas, we need a metric to measure the incremental change in profitability. Hence, per Mauboussin (2022), analyzing the incremental ROIC captures the change in post-tax earnings relative to the investments made throughout the period. Looking to SNN, it invested an additional $824mm across the year to drive the $58mm increase in NOPAT, a 7.08% return on the investment. Not to mention, the YoY pullback in net earnings. Specifically, the investment was made up from the Engage Surgical acquisition, and further investments into its Singapore Smith+Nephew Academy, along with the goodwill on top of this, plus changes in working capital mentioned earlier. CEO Nath mentioned that "more than 60% of growth in 2022 [came] from products launched in the last five years" which is a welcomed point, however, looking closer, the incremental ROIC from FY21-22 lagged the 2022 ROIC at 7.08% vs. 12.5%. This tells us that SNN's capital efficiency could be a headwind for future growth, reflected in this report via the company's 17.3% FY22 operating leverage. In fact, this is a measure the company wants to address in its 3-year plan, to drive operating leverage and subsequently recognize a 20% trading margin by FY25 [Figure 6]. Subsequently, our findings show that SNN exhibited a 6% incremental growth in NOPAT, but a negative 32% YoY incremental decline in earnings, and required a heavy reinvestment of capital to fund this. Alas, FCF, measured here by SNN's FY22 NOPAT minus the delta in investments came to $143mm. It would make sense as to why it is withholding on its buyback program for the time being, therefore. Further, as Mauboussin (2022) note, extrapolating the historical ROIIC can help identify potential earnings growth that is not yet priced in by the market. Therefore, this analysis demonstrates the company is still above to generate future economic value above its cost of capital, and that SNN's 12-point strategy described earlier is worth taking note of. As a measure of success of the strategy, it will be imperative to observe the firm driving its incremental ROIC higher in order to maintain a high amount of residual cash flow as distributable profits to equity holders. This will mean it can more than comfortably continue increasing its dividend, and potentially reinstate its buyback program, by estimation.

Fig. (5)

Data: Author, using data from SNN's SEC Filings, and FY22' results

{kind=link}

Fig. (6)

{kind=link}

FY23 Guidance

The company is aiming high with its new strategies for growth and guides for top-line sales growth of 5-6%, calling for $5.5Bn in turnover for FY23. SNN says growth will be driven by upsides in the sports medicine, ENT and advanced wound management segments. The 12-point plan will directly address previous challenges in the orthopaedics segment, the company says. Despite this, it does expect further Covid-related challenges from its China footprint, " reducing surgical-volumes, as well as the continuing headwind of VBP in Orthopaedics". Looking down the P&L, the company is guiding for a 17.5% net margin, calling for $967mm in earnings, driven primarily by cost savings and its focus on increasing operating leverage, as mentioned earlier. Its bottom line guidance also bakes in a 100bps FX headwind and additional cost pressures related to inflation.

Valuation and conclusion

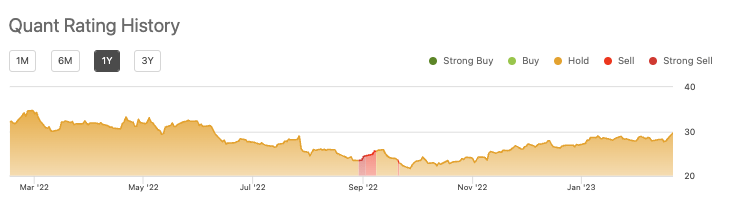

SNN currently trades at 2.3x book value and >20x FY22 cash flow, above the industry's 16x. Moreover, it is above the company's 5-year average of 14.6x, begging the question if this is a worthwhile price, seeing the substantial wind-back in operating cash flows from 5-years ago. Moreover, with the pullback in EPS, the stock's P/E trades at a substantial premium to peers at ~109x FY22 earnings. Even baking in the annual dividend in the denominator, it still trades at >44x P/E [earnings classified as EPS + DPS in this instance]. With the lackluster growth, we believe SNN should trade in-line with the industry multiple of 24x earnings. This is supported by the quant grading system as well.

Fig. (7) SNN Quant rating

{kind=link}

Subsequent to its FY22 earnings, SNN has a hurdle to overcome in order to drive top-bottom line growth into the coming periods. Management have instilled a new 12-point plan to achieve this - with particular focus on the ortho segment - however, until we have further data into FY23 we will have to wait in order to gauge the success of this. For now, we reiterate SNN as a hold.

For further details see:

Smith & Nephew: Flat FY22 Growth, Now An Execution Story