SNN - Smith & Nephew: Orthopedic Franchise Finally Coming Along

Summary

- Company reports top-line growth in Q4.

- Innovation & operational leverage finally turning the screw here.

- Shares remain cheap. We see higher prices coming for the stock in 2023.

Intro

We wrote about Smith & Nephew plc ( SNN ) in July of last year when we reaffirmed our interest in this value play. The company's high gross margins, strong fundamentals, and oversold shares made us interested in this play at the time. Shares since that commentary over 7 months ago have rallied approximately 10% which means the total return would have been slightly higher when we include the company's dividend payment. Suffice it to say, given the volatility in equity markets in recent times (Where the S&P has only returned approximately 4.7% over the above-mentioned timeframe), SNN's rate of return has not been bad and we believe there are plenty more gains to follow here for long-term holders.

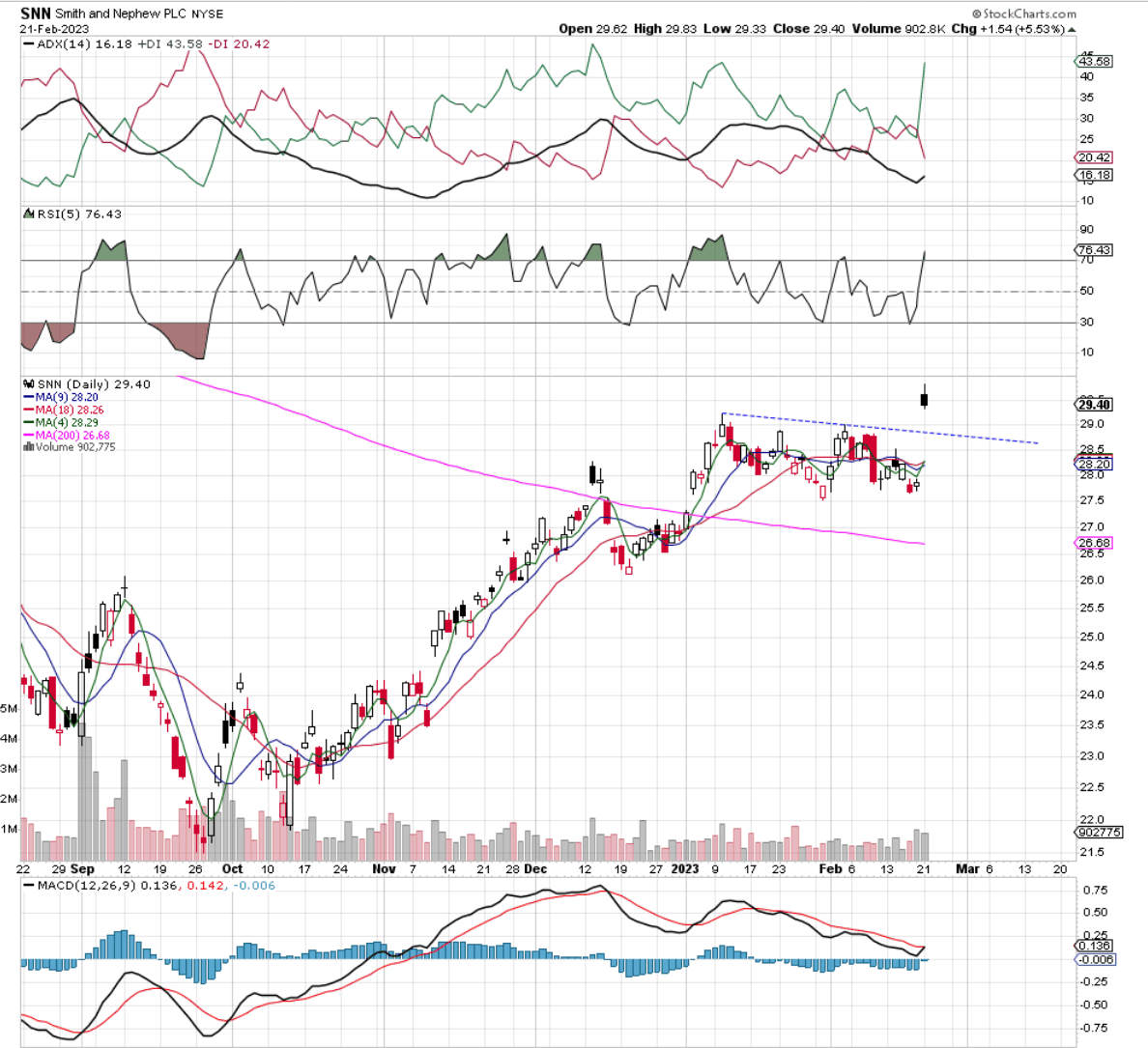

In fact, if we go to the technical chart, we can see that shares spiked up on the release of the company's fourth-quarter earnings . Given the consolidation that has taken place in SNN since the start of the year, the gap shown below could easily be a breakaway gap which are gaps that take place in the initial stages of a sustained trending move. Suffice it to say, if shares can now push on (And thus keep the majority of the gap unfilled), it would stack the odds in favor of a trending move to the upside in SNN which would enable us to enter into a long position very close to underside support.

{kind=link}

Q4 Improvement

We witnessed further sequential improvement in SNN's financials in the fourth quarter and management's outlook regarding FY23 definitely gave room for encouragement. Q4 sales grew by 1.4% which meant that fiscal 2022 sales were more or less flat for the year. Next year, however, despite ongoing macroeconomic headwinds, management guided 5 to 6% top-line growth, a trading profit margin of 17.5%+, and a commitment to deliver more than $200 million in annual savings over the next three years. These numbers (especially on the sales and costs side) are obviously not what the market has been used to over the past few years but trends over the past couple of quarters are convincing the markets that these goals are indeed possible.

What do we mean by this? Well, if we look at how SNN performed over the past few years and especially through the pandemic, we see that the company's growth numbers have disappointed with the Orthopedics franchise being the laggard of the group. Despite the company's 70%+ gross margins, SNN has rather higher costs and these costs were only exacerbated by the company's decision to invest right through the downturn. However, where this decision obviously impaired the share price and profits alike over the short-term, we now are beginning to see the benefits of elevated R&D spending finally come to fruition no more so in the Orthopedics franchise.

Improving Fundamentals

Therefore going forward, we believe the market is finally beginning to price in higher revenues in SNN and lower costs as a percentage of those revenues all things remain equal. This is what operational leverage essentially gives a company in that higher cash flow generation can be used to both further revenue growth and lower operating costs over time. This is all being done through the company's 12-point plan which came into operation in the middle of last year.

On the recent Q4 earnings call, management was pretty confident that its pipeline of products would perform very well once they hit the market. This confidence is founded on how SNN's innovation relates to what competitors are currently offering. One big driver on the orthopedic side is the Coro robotic offering where supply can now meet demand due to supply chain improvements. Furthermore, the improvement within the EVOS system opens up this product to be far more competitive in the trauma market. Suffice it to say, given how innovation has really improved in SNN and the elevated number of launches which are expected to come online over the next 12 months , this should all feed into shares continuing to trade higher from here.

Conclusion

Therefore, to sum up, Smith & Nephew plc reported encouraging trends in the recent fourth quarter presentation which should result in much-improved growth as well as share-price gains in fiscal 2023. We may look at a long-position shortly. We look forward to continued coverage.

For further details see:

Smith & Nephew: Orthopedic Franchise Finally Coming Along