SNN - Smith & Nephew: Orthopedics Growth Continues To Drive Sales Forward

2023-12-28 06:46:15 ET

Summary

- Smith & Nephew shares are down 3.6% since February, but management has increased top-line growth guidance for fiscal 2022.

- The Orthopedics business unit is showing strong growth potential, with momentum in the EVOS franchise and expansion opportunities for REGENETEN in Sports Medicine.

- Technical analysis suggests a potential double-bottom reversal pattern, with shares potentially reaching $30+ and even returning to 2021 highs of over $40 if investors can remain patient.

Intro

We wrote about Smith & Nephew plc (SNN) in February of this year when we stamped a 'Buy' rating on the medical device company. Shares rallied post our buy call to almost $33 per share before finally topping out in April this year. shares then underwent a long period of lower lows before finally bottoming out in late October. Since then, green shoots have begun to form, which means shares are only down approximately 3.6% (since our February commentary) when dividend payments from Smith & Nephew are included in the breakdown.

A negative 3.6% return as opposed to almost a 20% return in the S&P500 over the past 10 months is a sizable opportunity cost that should not be dismissed lightly. In saying this, although fiscal 2022 sales came in flat compared to fiscal 2021, management guidance of 5 to 6% regarding top-line growth for this present fiscal looks like it is going to be beaten as management increased top-line guidance in the company's recent Q3 earnings report (Now 6 to 7% top-line growth expected).

Furthermore, in the previous commentary, we pointed to how strong innovation & an aggressive cost-cutting plan would lead to an improvement in the company's financials, all things remaining equal. These endeavours are all being carried out through the company's rigorous 12-point plan, which came into being in mid-2022. Suffice it to say, with the previously guided 17.5% trading profit margin looking likely to be achieved for fiscal 2023 and with visible improvements over the latter end of 2023 which we will get into, we believe 2024 will turn out to be a solid year for the medical device manufacturer.

Forward-Looking Fundamentals

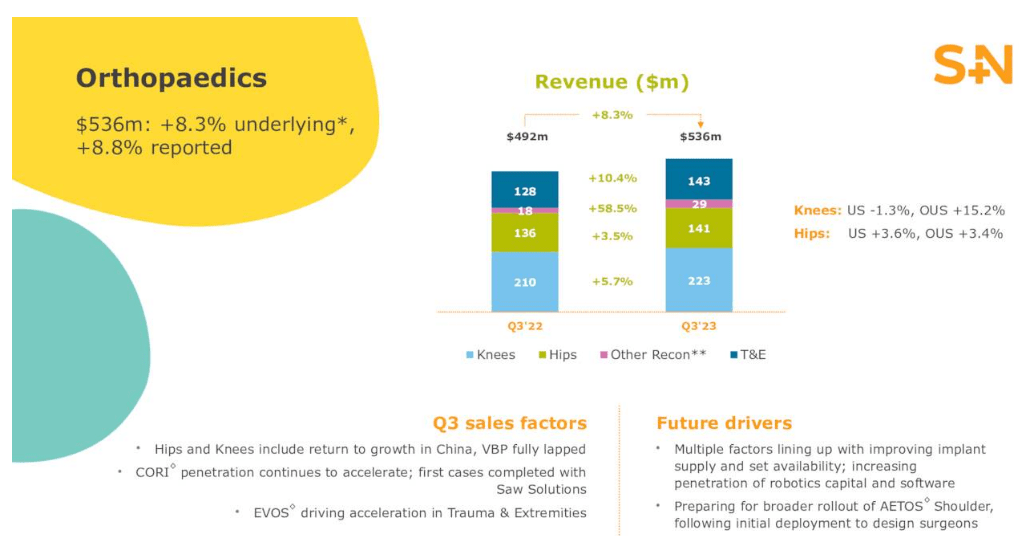

Management's quarterly reports & investor presentations are very much focused on top-line growth potential, as bottom-line profitability invariably follows through as a result. The Orthopedics business unit continued its sequential momentum in Q3, posting 8.3% growth in the quarter. Knees & Hips bounced back to growth in China, with CORI penetration continuing to gain ground. Furthermore, momentum from the EVOS franchise resulted in the 'Trauma & Extremities' segment reporting $143 million for the quarter. Suffice it to say, notwithstanding the company's impressive Q3 results, when one also takes into account the encouraging forward-looking trends in Orthopedics (stronger implant supply & robotics acceleration), we see a strong runway for growth in this business unit going forward, as we see below.

SNN Orthopedics - Q3 Investor Presentation (Seeking Alpha)

{kind=link}

The 'Sports Medicine & ENT' & the 'Advanced Wound Management' segments grew by 11.1% & 3.6% respectively in the quarter. Given the size of these units ($425 million & $396 million in sales respectively in Q3), it remains imperative that their growth drivers also come to the fore to support orthopedic growth. To this point, REGENETEN still has a long runway for growth through expansions in different jurisdictions, as well as additional applications apart from the shoulder.

Furthermore, we expect the AWM segment to grow at a higher clip going forward, especially considering how both PICO & RENASYS reported double-digit growth rates in the quarter. The below-average 3.6% underlying growth rate in AWM came about as a result of a temporary timing issue concerning SANTYL shipments plus being up against a strong comparable last year. The shipments issue has now been resolved, which leads us to believe that better growth rates are ahead for the AWM business unit going forward.

Technicals

Suffice it to say, when shares of SNN bottomed out in October of this year, astute investors were fully area of the respective growth drivers in this play and associated fundamentals. If we look at the bullish volume trends around that time, it becomes evident that we have a bottoming pattern in play in SNN, where shares should at least make it back up to the $30+ level in this latest move. If, indeed, we have a long-term double-bottom reversal formation in play, shares would need to take out the April highs of $32+ to confirm the pattern. The attractiveness of this potential reversal is the height of the pattern ($11+ per share) in that if we do eventually register an upside breakout, shares could quickly return to their 2021 highs of north of $40 per share.

SNN Technical Chart (Stockcharts.com)

{kind=link}

Conclusion

To sum up, we are reiterating our bullish position in SNN due to its growing number of growth drivers, Orthopedics growth as well as bullish technicals. Product availability continues to improve across all business units which should continue to have positive ramifications for top-line growth over time. Remaining bullish. We look forward to continued coverage.

For further details see:

Smith & Nephew: Orthopedics Growth Continues To Drive Sales Forward